EB - Eventbrite: Positive Growth And Margin Outlook

2023-04-12 03:57:52 ET

Summary

- Eventbrite is expected to deliver a revenue CAGR in excess of +20% for the long run leveraging on the new products and geographic expansion growth drivers.

- EB sees its EBITDA margin doubling to 20% or higher with cost-cutting measures in the short term and a more favorable revenue mix for the long run.

- I assign a Buy rating to Eventbrite; EB's positive financial outlook hasn't been fully priced into its valuations given that the stock trades at a meaningful discount to its peers.

Elevator Pitch

My investment rating for Eventbrite, Inc.'s ( EB ) shares is a Buy.

Looking ahead, EB expects to continue growing its top line at a CAGR of +20% or better, and double its EBITDA margin to at least 20%. My opinion is that Eventbrite can meet the company's financial targets with ease, and its valuation discount to peers is unwarranted. Therefore, I have made the decision to award a Buy rating to Eventbrite.

Company Description

In its fiscal 2022 10-K filing , Eventbrite refers to itself as a "self-service platform" which helps "event creators to plan, promote and sell tickets."

The Key Factors That Drive Eventbrite's Top Line Expansion

EB's February 2023 Investor Presentation

{kind=link}

EB has operations in approximately 180 markets around the world, but the US is the key market for the company. In terms of revenue, the US accounted for three-quarters of Eventbrite's FY 2022 sales, while foreign markets contributed the remaining one-quarter of the company's top line last year as indicated in its 10-K filing. Also, 61% of paid tickets sold for EB's events in the previous year was derived from the US market, with the other 39% of paid tickets came from international markets in 2022 as highlighted in EB's investor presentation .

Eventbrite's Revenue Growth Prospects

EB guided for a +23% increase in its top line from $261 million for FY 2022 to $321 million in FY 2023 based on the mid-point of the company's guidance disclosed at its Q4 2022 earnings briefing in late February. At the company's most recent quarterly results call, Eventbrite also reiterated its goal of delivering a revenue CAGR of +20% or better for the long run.

In my view, both Eventbrite's short term and long term revenue targets are realistic and achievable.

For the near term, a price hike initiated at the beginning of this year should be a major factor supporting EB's +23% top line growth target for 2023. At Morgan Stanley's ( MS ) Technology, Media and Telecom or TMT Conference on March 8, 2023, Eventbrite revealed that it has implemented a +10% price increase for events which aren't governed by long-term agreements and account for around 70% of the company's ticketing volume since January 3 this year. For the rest of the events that contribute the remaining 30% of its ticketing volume, EB also expects to initiate a +10% price hike when these events' respective long-term agreements expire.

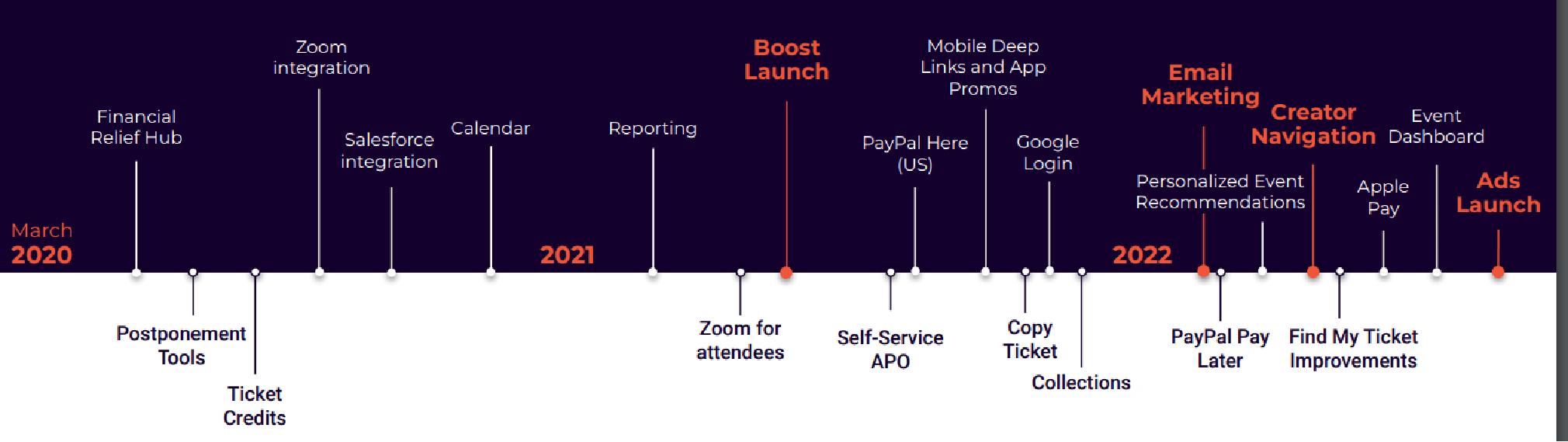

New Features Introduced To Eventbrite's Platform In Recent Years

EB's February 2023 Investor Presentation

{kind=link}

Separately, Eventbrite's revenue in 2023 should be boosted by an increase in the number of paid creators thanks to a faster pace of new product feature introductions in the prior year. As disclosed in its investor presentation, the number of new product features for EB's platform roughly doubled from 30 for 2020 to 60 in 2022, which will help Eventbrite to retain existing creators and attract new creators.

In the long run, new product categories and new geographic markets will be the key growth drivers for Eventbrite.

Eventbrite highlighted in its FY 2022 10-K filing that it earns "substantially all of our revenues from ticketing services." Based on EB's internal estimates indicated in its investor presentation, about 8% of ticketing revenue is allocated to ticketing services, while marketing accounts for as much as 20%-40% of ticketing revenue. The company launched its new products, Eventbrite Boost (event marketing tools subscription plans) and Eventbrite Ads (advertising campaigns) in 2021 and 2022, respectively to expand beyond ticketing services. In Q4 2022, Eventbrite Ads and Eventbrite Boost in aggregate only represented a mere 2% of EB's revenue, so there is significant potential for growing top line contribution from these two new products.

With regards to geographic expansion, I mentioned earlier in this article that the US still accounts for the majority of Eventbrite's revenue and paid ticket sales volume in the previous year. In other words, there is lots of room for EB to grow its presence in foreign markets. EB also highlighted in its investor presentation that its current six biggest markets including the US have a total population of just 477 million, which indicates that the company isn't fully capitalizing on the growth potential of many large international markets with huge populations.

EB's Profitability Outlook

Eventbrite is targeting an improvement in EBITDA margin from 8.6% in fiscal 2022 to 10.0% for fiscal 2023, and the company has a target of achieving a 20% EBITDA margin for the long term.

In the short term, cost optimization will drive margin expansion for EB. Eventbrite had previously disclosed at its Q4 2022 earnings call in late February that it was "eliminating roughly 8% of existing roles" and "relocating approximately 30% of remaining roles to (low-cost) locations." EB has guided for expense savings of around $13-$14 million on an annualized basis (or about 4% of 2023 revenue guidance) to be realized from these recent cost optimization measures.

For the long term, the increase in revenue contribution from Eventbrite Boost and Eventbrite Ads will result in a more favorable sales mix for EB. Eventbrite's core ticketing services business is less profitable than the company's new businesses, Eventbrite Ads and Eventbrite Boost which don't have the cost burden associated with expenses involved in processing ticketing transactions. As EB's revenue mix shifts towards higher margin Eventbrite Ads and Eventbrite Boost, the company's EBITDA margin should go up over time.

Eventbrite's Valuations

EB is valued by the market at a discount to its peers based on the forward Enterprise-to-Revenue valuation metric, even though its expected top line expansion for the current fiscal year is superior to that of peers.

Peer Valuation Comparison For EB

| Stock |

| Consensus Forward Next Twelve Months' Enterprise Value-to-Revenue Valuation Multiple |

| Consensus Current Fiscal Year Revenue Growth Rate Estimate |

| Eventbrite |

| 1.73 |

| +24.1% |

| Vivid Seats Inc. ( SEAT ) |

| 2.58 |

| -1.0% |

| Zoom Video Communications, Inc. ( ZM ) |

| 3.41 |

| +1.7% |

Source: S&P Capital IQ

Concluding Thoughts

Eventbrite shouldn't trade at a substantial discount to its peers, taking into account its reasonably favorable growth and margin outlook. As such, EB's stock deserves a Buy rating.

For further details see:

Eventbrite: Positive Growth And Margin Outlook