EB - Eventbrite Ups Guidance While Reducing Operating Losses On Marketplace Approach

2023-06-22 16:22:04 ET

Summary

- Eventbrite published its Q1 2023 financial results on May 9, 2023.

- The company operates an online events marketplace with related services.

- EB has increased its 2023 revenue guidance range and has restructured its operations around its increased focus on an events marketplace model.

- With lowered operating losses, increasing revenue and other improving financial metrics, my outlook for EB is a Buy at around $8.60.

A Quick Take On Eventbrite

Eventbrite ( EB ) reported its Q1 2023 financial results on May 9, 2023, beating both revenue and EPS consensus estimates.

The firm operates an online marketplace for users to create, market and manage events, sell tickets and gain insights.

With operating losses being reduced combined with a greater focus on a marketplace approach, rising revenue guidance and private equity interest in the sector, my outlook for EB in the near term is a Buy at around $8.60.

Eventbrite Overview

San Francisco, California-based Eventbrite was founded in 2006 to develop and maintain a platform for users to plan, promote and produce live events, thereby allowing creators to reduce friction and costs, increase reach and drive ticket sales.

Management is headed by Co-Founder and CEO Julia Hartz, who was previously Manager of Current Series at Fox Networks Group.

The Eventbrite platform supports events ranging from fundraisers, seminars, wellness activities and music festivals to classes and cultural celebrations worldwide. Anyone can create or discover events on Eventbrite.

Services include:

-

Event listing marketplace

-

Event marketing

-

Event analytics and reporting

-

Ticketing and payments

-

Mobile app

Eventbrite's Market & Competition

According to a 2022 market research report by MarketsandMarkets, the total event management software market was valued at $7.0 billion in 2021 and is projected to grow to $14.1 billion by 2026.

This growth would represent a CAGR of 14.9% during the forecast period.

The main factors driving the market growth are the need for effective event management and the increasing adoption of event planning software and event registration software by Small and Medium-sized Enterprises [SMEs].

Additionally, event marketers seek data insights from event attendance and activity to enhance future event configuration.

Major competitors that provide event management or discovery software include:

-

Live Nation ( LYV )

-

Cvent

-

XING Events

-

ACTIVE Network

-

etouches

-

EMS Software

-

Ungerboeck Software International

-

SignUpGenius

Eventbrite's Recent Financial Trends

-

Total revenue by quarter has continued to rise; Operating losses by quarter have trended lower in recent quarters:

Total Revenue and Operating Income (Seeking Alpha)

-

Gross profit margin by quarter has trended higher; Selling, G&A expenses as a percentage of total revenue by quarter have trended substantially lower:

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

Earnings per share (Diluted) generated negative results in the most recent quarter:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

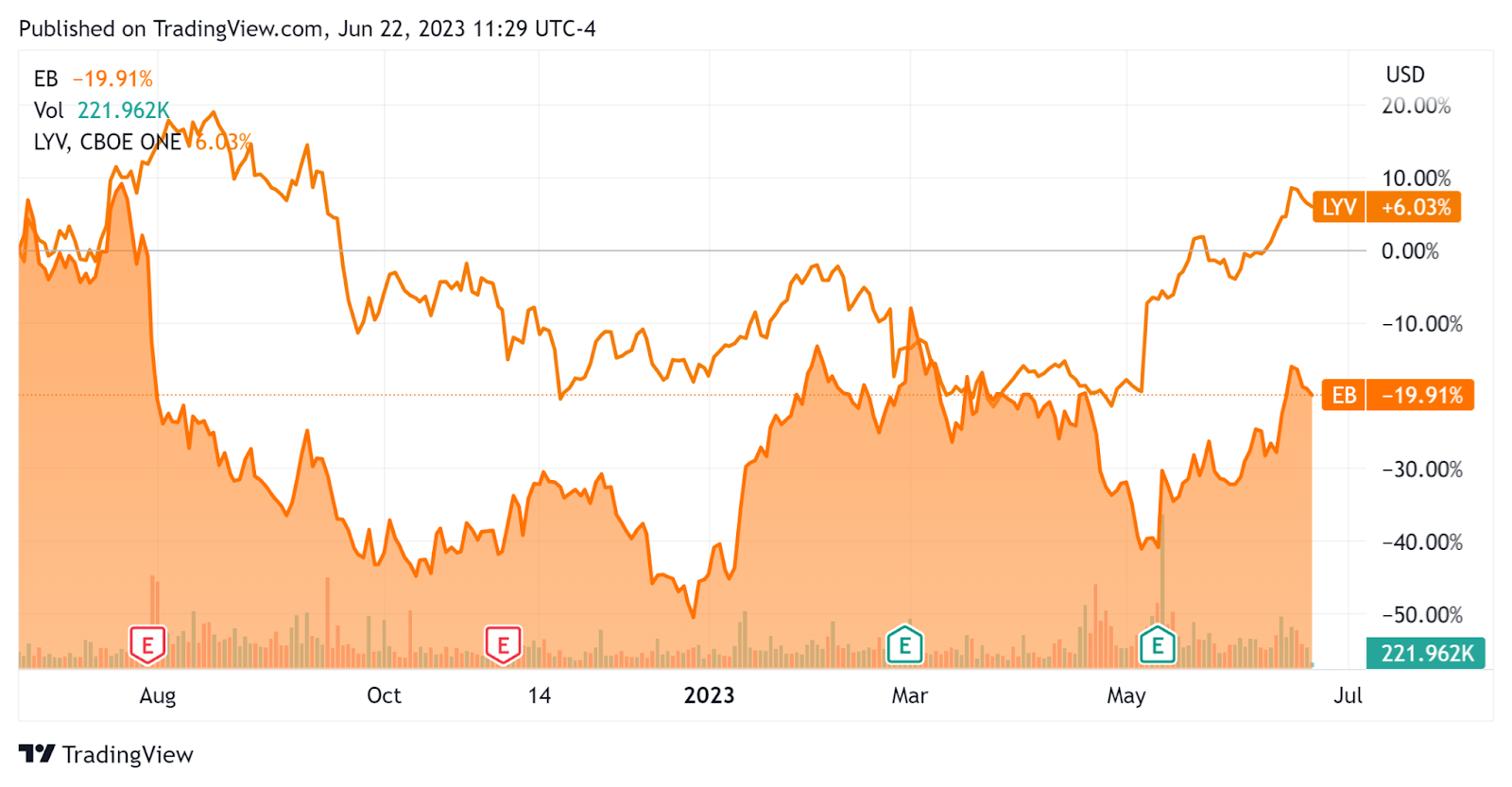

In the past 12 months, EB's stock price has fallen 19.91% vs. Live Nation's ((LYV)) rise of 6.03%, as the chart indicates below.

{kind=link}

For the balance sheet, the firm ended the quarter with $698.9 million in cash, equivalents and short-term investments and $356.1 million in total debt, none of which was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was only $4.9 million, during which capital expenditures were $1.4 million. The company paid $16.5 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Eventbrite

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 1.9 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 3.0 |

| Revenue Growth Rate |

| 31.5% |

| Net Income Margin |

| -17.6% |

| EBITDA % |

| -9.5% |

| Net Debt To Annual EBITDA |

| 12.7 |

| Market Capitalization |

| $868,940,000 |

| Enterprise Value |

| $531,260,000 |

| Operating Cash Flow |

| $6,320,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.50 |

(Source - Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

EB's most recent Rule of 40 calculation was 22.0% as of Q1 2023's results, so the firm is in need of improvement in this regard, per the table below

| Rule of 40 Performance |

| Current Quarter |

| Revenue Growth % |

| 31.5% |

| EBITDA % |

| -9.5% |

| Total |

| 22.0% |

(Source - Seeking Alpha)

Commentary On Eventbrite

In its last earnings call (Source - Seeking Alpha), covering Q1 2023's results, management highlighted its recent restructuring efforts designed to reduce non-revenue-generating roles to focus on its Marketplace approach.

The firm prioritized marketing and demand generation as a recent survey indicated more than half of an event's revenue 'comes from sources other than ticket sales.'

Eventbrite is in the midst of a transition from a ticket processing platform to a 'demand-generating events marketplace'.

Management did not disclose any company or revenue retention rate metrics or characterize them.

Total revenue for Q1 2023 rose an impressive 39.4% year-over-year as post-pandemic in-person events rebounded and gross profit margin increased by 2.8 percentage points.

Selling, G&A expenses as a percentage of revenue dropped 11.2% YoY, a very positive signal indicating much higher efficiency in generating incremental revenue and operating losses decreased by 58.2% year-over-year.

Looking ahead, management increased its full-year 2023 revenue guidance slightly to $324 million at the midpoint of the range, or 24.2% topline revenue growth.

If achieved, this would represent a material drop in revenue growth from 2022's growth rate of 39% over 2021.

The company's financial position is quite strong, with high liquidity, some long-term-only debt and a small amount of positive free cash flow.

EB's Rule of 40 performance has been only moderate.

From management's most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below.

Earnings Transcript Key Terms Frequency (Seeking Alpha)

I'm most interested in the frequency of potentially negative terms, so management or analyst questions cited 'Challeng[es][ing]' once, 'Macro' two times and 'Drop' two times.

The negative terms refer to analyst questions about macroeconomic headwinds. Management noted that Q1's results were quite positive and encouraged them to raise forward revenue guidance as a result.

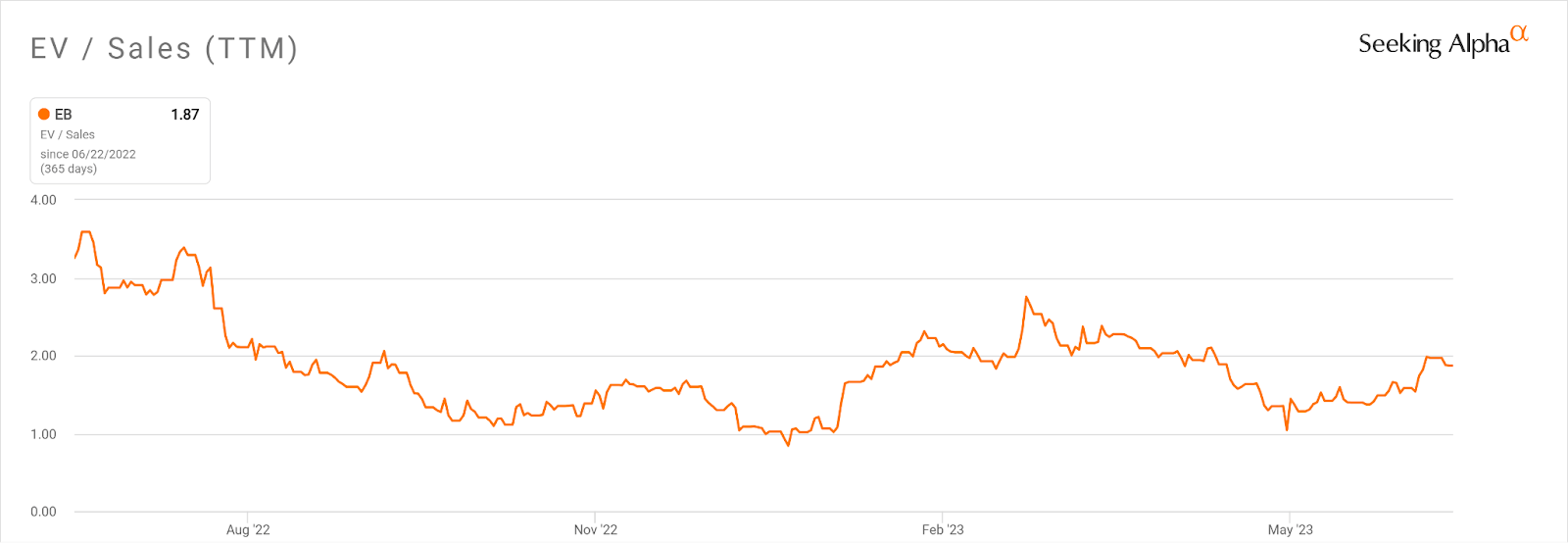

In the past twelve months, the firm's EV/Sales valuation multiple has dropped 41.6%, as the chart from Seeking Alpha shows below.

{kind=link}

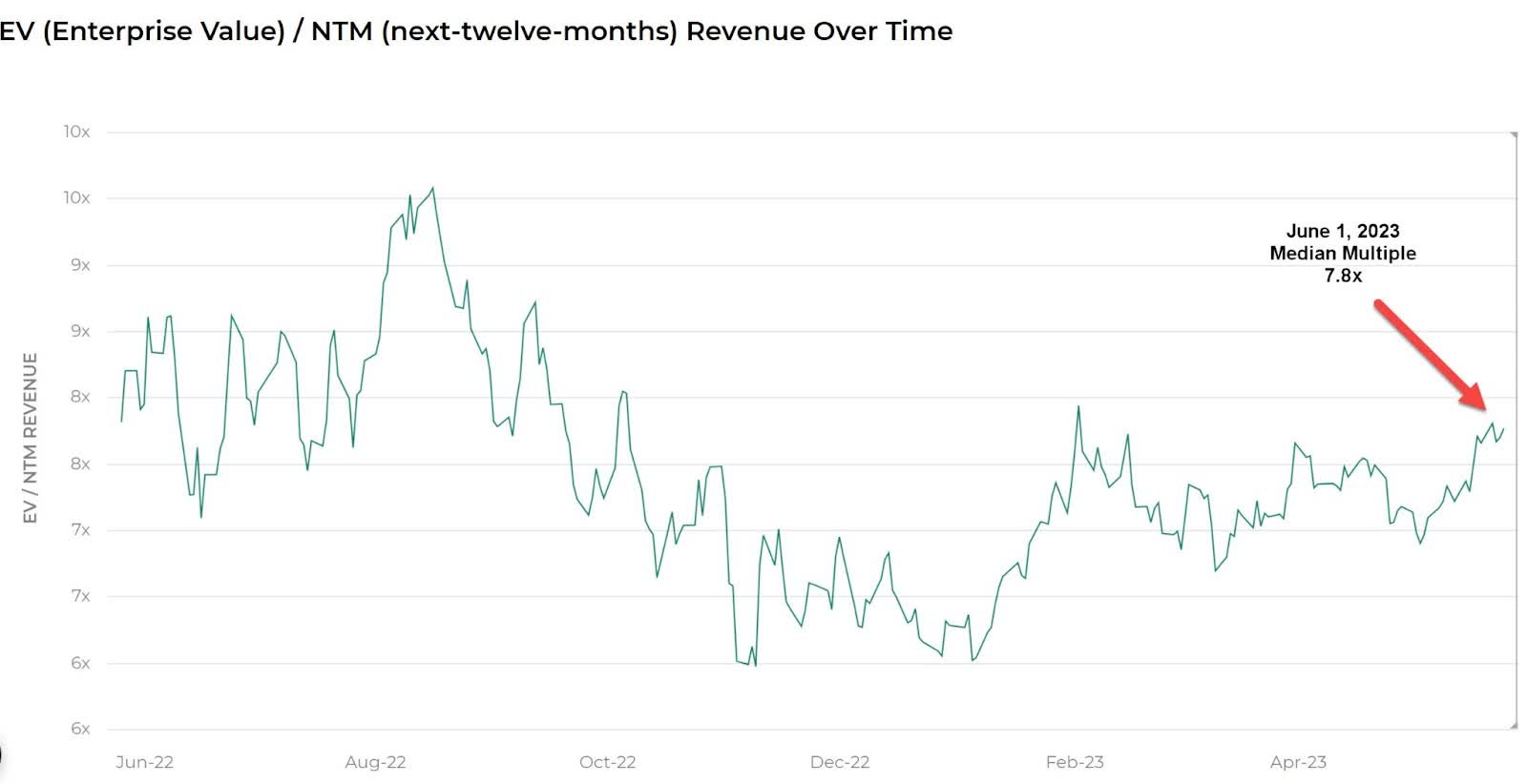

The Meritech Capital Index of publicly held SaaS application software companies showed an average forward EV/Revenue multiple of around 7.9x on June 1, 2023, as the chart shows here:

EV/Next 12 Month's Revenue Multiple Index (Meritech Capital)

{kind=link}

So, by comparison, EB is currently valued by the market at a significant discount to the broader Meritech Capital SaaS Index, at least as of June 1, 2023.

Risks to the company's outlook include an economic slowdown that may be underway, reduced credit availability which may affect customer/prospect spending plans and lengthening sales cycles which may reduce its revenue growth potential in the near term.

Notably, Blackstone's acquisition announcement of Cvent had virtually no effect on EB's stock price.

A potential upside catalyst to the stock could include positive results from its transition to an events marketplace focus, recent headcount reductions, and restructuring.

With operating losses being reduced combined with a greater focus on a marketplace approach, rising revenue guidance and private equity interest in the sector, my outlook for EB in the near term is a Buy at around $8.60.

For further details see:

Eventbrite Ups Guidance While Reducing Operating Losses On Marketplace Approach