EVR - Evercore: Cautious Look After Movements On Rates And Recent IPOs

2023-10-07 06:11:04 ET

Summary

- Recent results reflect a tough environment for deals, with Evercore's revenues steadily decreasing due to rising rates.

- Concerns arise about whether deal flow will pick up as expected weigh on valuation, as longer-dated bonds yields increase, suggesting higher rates for longer.

- Three scenarios are considered for Evercore's future: best case, moderate case, and worst case, with fair prices ranging from $95 to $175 per share.

The recent weeks have been characterized by important developments for the M&A industry. First, some large IPOs hit the market in a sign that the dealflow might soon pick up again. However, after a week the performance of firms like ARM and Instacart remains somewhat disappointing, and more VC firms are asking portfolio companies to remain on hold with their IPO plans. Then there was a strong move on longer-term bonds that might suggest higher rates for longer. Definitely not good news for a firm like Evercore (EVR) and its deal flow-dependent revenues.

The recent results reflect a tough environment for deals

As rates have been steadily rising, Evercore revenues have been steadily decreasing. The exposure is mainly indirect, as many of the advisory fees that Evercore collects come from M&A deals and other transactions that exploded during the zero-rate environment.

Evercore - Revenues (Seeking Alpha)

After 2021 these fees took a hit and started going back to pre-zero-rates levels. This phenomenon particularly impacted net income, as the cost structure has some limits on flexibility. Indeed, layoffs are sometimes slow to benefit the bottom line, and many advisory shops like Evercore get caught with a good degree of operating leverage. This is clear in 2023 results, with revenues declining less than 25% YoY, but net income dropping more than 50%. Compensation, the largest single item impacting the topline, is in fact down only 12%, and this weighed on EPS.

But instead of punishing the stock, the market decided to put faith in Evercore. This is the reason behind the increasing valuation - both in terms of P/E and P/TBV multiples - and overperformance relative to the S&P (up 17% YTD against 11% of the S&P).

We definitely do not like these developments much as they could mean that the vast majority of deal flow pickup might be priced in already, but there might be some room for further expansion.

The concerns: will deal flow really pick up this soon?

The entire market, from equities to credit, has been expecting one main event to happen: lower rates in the (immediate) future. This can be grasped by looking at yield curves, FED meeting minutes, inflation data, and most importantly equity valuations. In the case of Evercore, it is no different. The market is expecting this deal flow growth that we are mentioning and expects it to positively impact earnings.

The company is expecting this deal to pick up as they have announced zero layoffs in 2023, and compensation expenses are only down 12%.

However, this creates a clear and immediate risk: what if the capital markets remain closed for longer?

{kind=link}

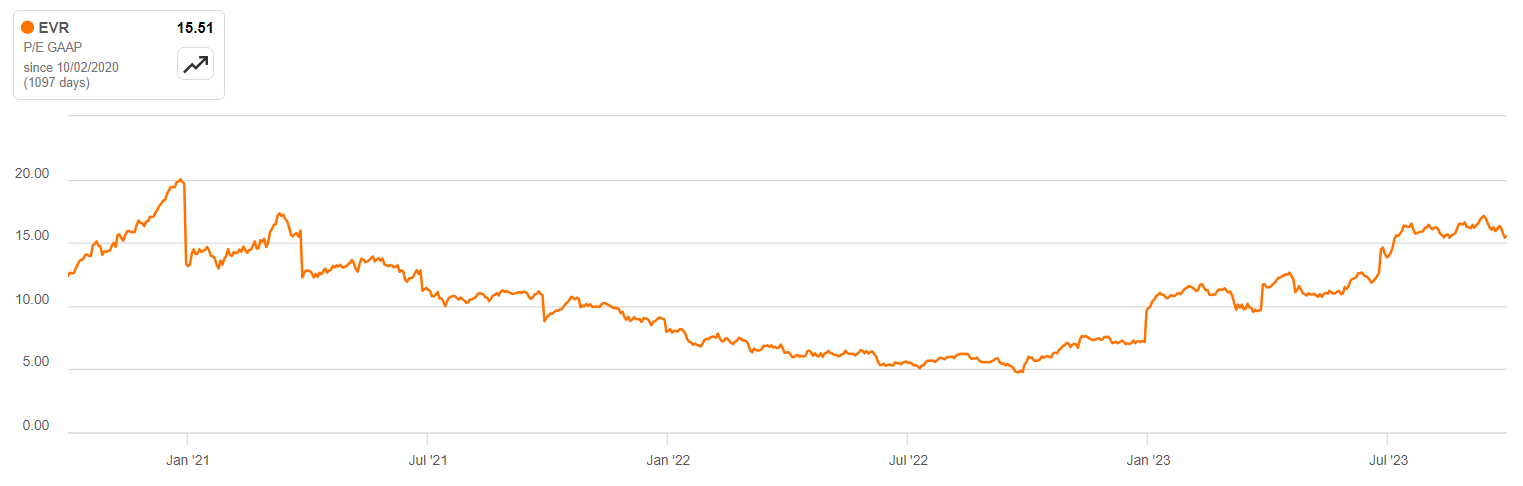

Right now valuation is back to multi-year highs with the P/E multiple in the 15 range, which is much higher than the industry's average P/E of 8. This means that little changes from the expected results in 2023 and 2024 will weigh a lot on the stock price.

EVR - Comps Valuation (Seeking Alpha)

This is the relative valuation, in comparison to competitors. The median values are almost half Evercore's multiples.

Our concerns around the deal flow are coming from one main point: higher financing costs will reduce M&A, while lower equity valuations will reduce IPOs. This week has been marked by an aggressive increase in long-term yields, which are particularly bad.

US Treasuries Yield Curve (Ustreasuriesyieldcurve.com)

The wild increase between 10Y and 20Y and 30Y yields is concerning as it seems that the market is expecting higher inflation, and thus higher rates, for much longer. So now the idea of having "another 2021" (another period of super-low rates) behind the corner seems much farther away than just 2 months ago.

To deal or not to deal? Hunting for a fair price in between

To find a fair price for Evercore stock it is of the essence to make very precise assumptions around this aforementioned dealflow. That will affect the topline growth and with basic assumptions around margins and compensation expenses, we can then easily derive net income and EPS.

We believe that the best way to approach this is to prepare three different scenarios:

-

Best case scenario: deal flow picks up very aggressively as the FED cuts rates back to the 2-2.5% range in the first half of 2024. This is likely because of a steep reduction in inflation. In this case, Evercore would see revenues grow at 10-15% rates, and net income margins would be around 25%

-

Moderate case scenario: rates remain higher for all 2023, and the FED starts cutting slowly in the first half of 2024. In this case, we should expect revenues to remain flat through H1 2024, and then grow slowly in the 5-8% range thereafter. Net income margins would thus be lower at around 18% to reflect lower flexibility in compensation expenses.

-

Worst case scenario: the FED is not cutting rates for another year. Thus financing markets remain closed and the deal flow remains depressed. This means lower revenues and profits for longer, in particular, flat revenues through the end of 2024, and net margins in the 10-15% range.

We put these assumptions into a DCF model to derive a fair price. Even if Evercore is classified as a financial company, its business is not primarily driven by its balance sheet - as most of its income is from advisory and not underwriting - and thus it can distribute the majority of net income.

We find these fair prices for each scenario:

-

Best case: fair price around $175 per share, which implies an upside potential of 30% from the current price. We associate a probability of 30%

-

Moderate case: fair price of $140 per share, which is close to the current price of $135 per share. We associate a probability of 30%.

-

Worst case: fair price of $95 per share. We associate a probability of 40%.

Note that we put a higher probability weight on the worst-case scenario as the market is already implying that it is not happening. We however like to be more conservative, especially in light of the recent developments in the longer-dated bonds market. The higher probability weight makes sure that we capture these concerns.

The final weighted average fair price is around $132, which is very close to the current price of $135. We conclude that while there is a very limited downside, the upside is virtually zero as the market seems to be already pricing-in a very optimistic scenario.

Conclusions

Evercore is a well-positioned advisory firm that often overperforms peers and has a strong presence in advising some of the largest companies in the US. However, we are concerned with its very generous valuation in terms of P/E multiple, which already prices in a strong market for M&A and aggressive deal flow pickup. We remain cautious and see a fair price around $130.

For further details see:

Evercore: Cautious Look After Movements On Rates And Recent IPOs