EVR - Evercore Remains A Solid Income Pick But Maintains Limited Price Upside

2023-10-07 01:08:00 ET

Summary

- Evercore achieved a Q2'23 revenue of $503.60mn, a 20.71% YoY decline, and a net income of $37.20, a 61.09% decline.

- Evercore's stock has outperformed the broader financial services industry in the past year.

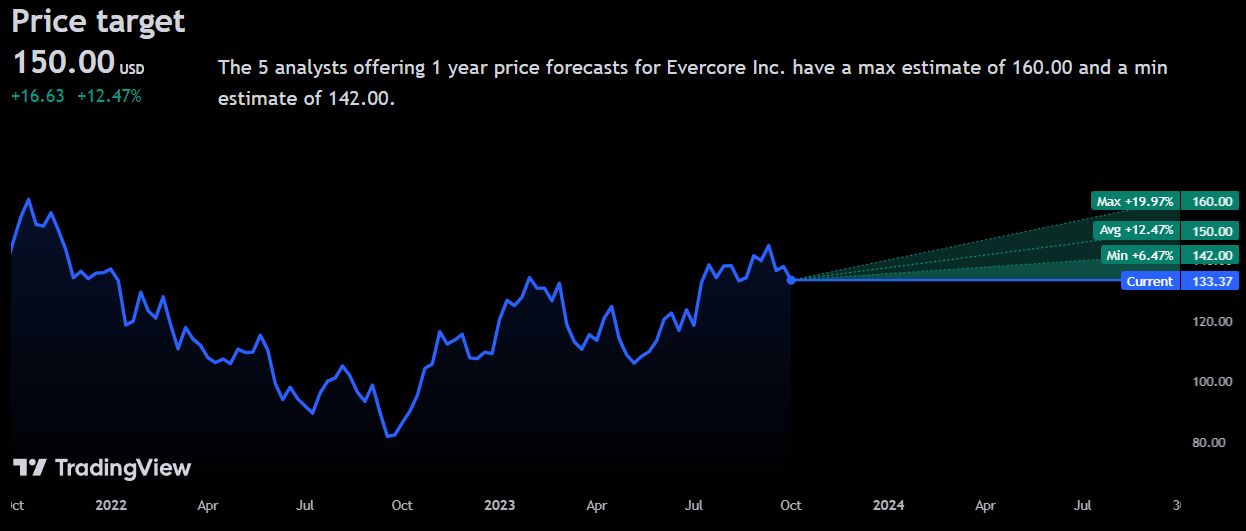

- Analysts have a positive but cautious view on Evercore, with an average 1Y price target of $150.00.

Evercore (EVR) is a New York City-based multinational investment banking advisory firm with operations across M&A advisory, restructuring, IPOs, and so on. The firm remains focused geographically on developed markets with growth vectors principally across Asia.

{kind=link}

Through these activities, Evercore has achieved a Q2'23 revenue of $503.60mn- a 20.71% YoY decline- alongside a net income of $37.20- a 61.09% decline and a free cash flow of $170.24mn- a 45.46% decline driven by declining operating and financing cash flows.

Introduction

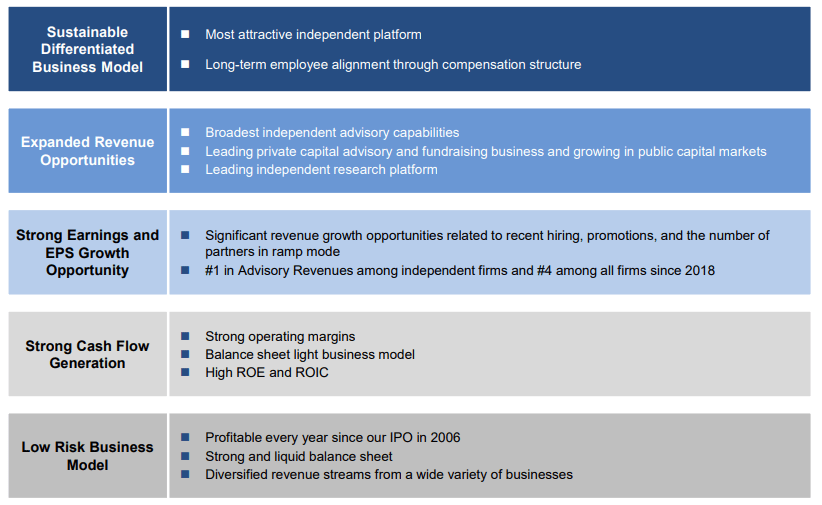

At the centre of the Evercore organization and its strategic success remains its fivefold value proposition; as an investment bank, Evercore maintains an outsized employee-aligned capital allocation focus which enables long-run relationship building and greater organizational flexibility, in parallel with Evercore's aggressive revenue and earnings growth driven by scale in high margin segments such as private capital advisory and independent research. Moreover, with a lighter cap structure, high free cash flows, and the ability to generate returns on their capital, Evercore effectively remains a more low-risk business able to return cash to shareholders judiciously.

{kind=link}

However, while Evercore remains strong operationally and sound financially, the combination of Evercore's overperformance in the past year and general macro uncertainty limit any potential upside and may induce volatility, leading me to rate Evercore a 'hold'.

Valuation & Financials

General Overview

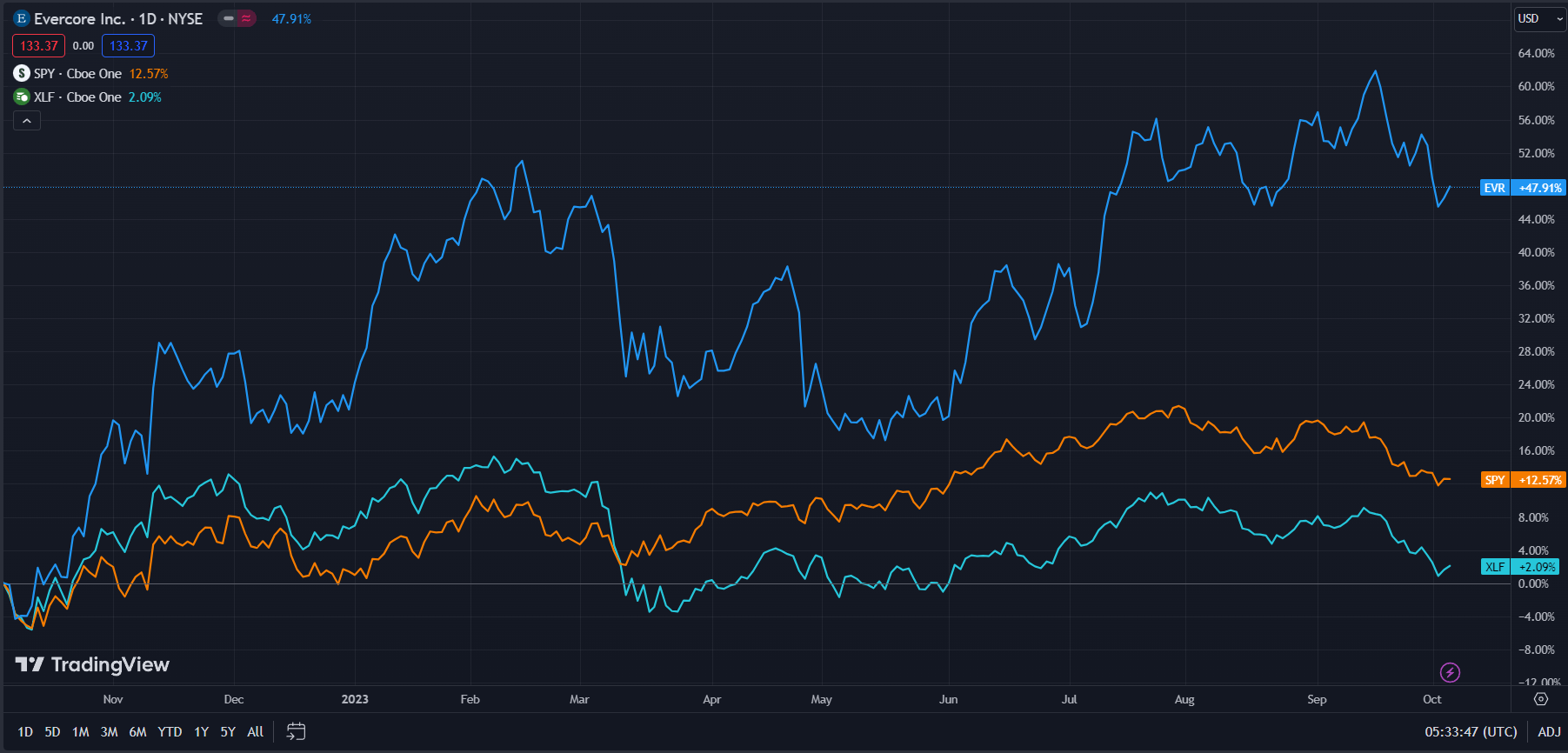

In the TTM period, Evercore's stock- up 47.91%- has outperformed the broader financial services industry, as represented by the Financial Select Sector SPDR Fund ( XLF )- up 2.09%- and the general market- as represented by the S&P500 ( SPY )- up 12.57% in the same period.

Evercore (Dark Blue) vs Industry & Market (TradingView)

{kind=link}

Evercore's outperformance has largely seemed to be a product of the company consistently meeting or beating earnings expectations while sustaining both its capital return and capex obligations.

On the other hand, the financial services industry has been hit hard by poorly performing equity portfolios- with developed market equities down 3.4% QoQ - in recent months, sticky interest rates, and multi-year lows for many bonds.

Comparable Companies

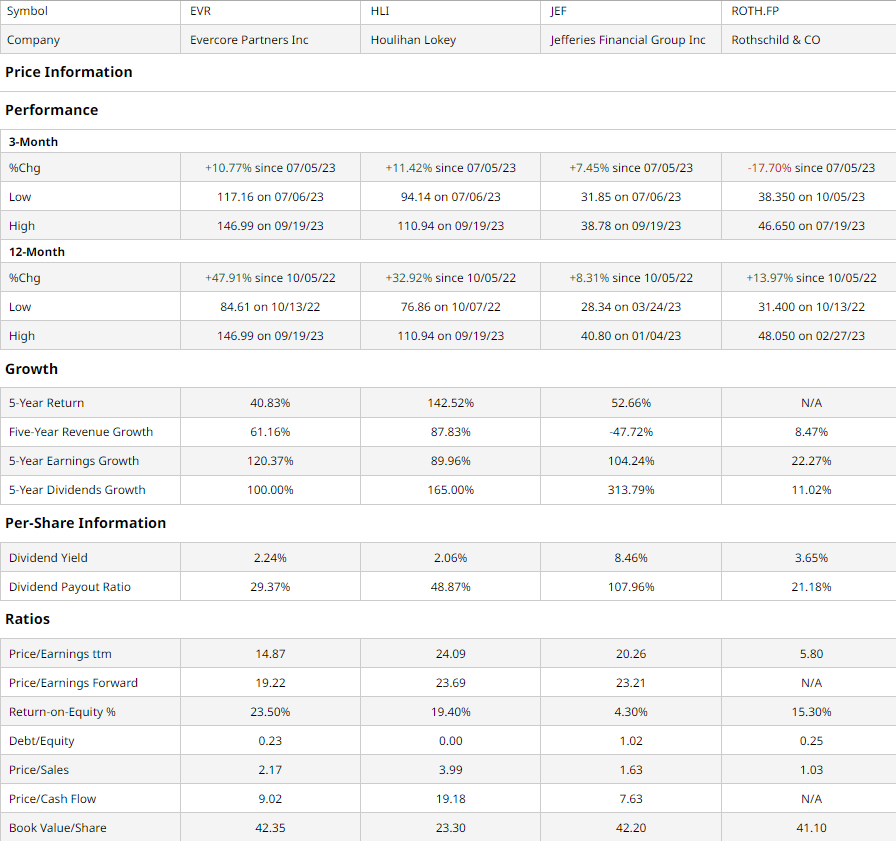

As an elite boutique investment bank, Evercore's competition is limited to either private markets or tends to be smaller in market capitalization and thus operates on different price dynamics. As such, I sought to compare Evercore to similarly sized boutique and middle-market banks. This group includes Los Angeles, California-based investment bank Houlihan Lokey ( HLI ), middle-market, New York City-based Jefferies Financial ( JEF ), and London-based multinational private and merchant bank Rothschild & Co. (PIEJF)(ROTH.FP).

{kind=link}

In the past year, Evercore has seen best-in-class price action, well-supported by the second-best quarterly price action. Although Evercore's rally was justified by its multiples-based value and growth capabilities- some of which it retains- I believe that in many aspects, Evercore has met fair value and has limited room for growth.

For instance, Evercore has seen peerless earnings growth in addition to the second-highest revenue growth, enabling Evercore to double its dividend in the past 5 years.

However, while Evercore still maintains value on a trailing P/E and book value per share basis, the company also either meets or performs worse than peers on debt/equity, P/S ratios, and P/CF ratios, demonstrating restraints to growth.

Valuation

According to my discounted cash flow analysis- which is applicable despite Evercore being a bank due to its balance sheet light approach- the base case net present value of Evercore is $138.53, meaning, at its current price of $133.37, the stock is undervalued by 4%.

My model, calculated over 5 years without built-in perpetual growth, assumes a discount rate of 9%, incorporating the rising cost of capital with the company's lighter overall capital structure. Additionally, in spite of a trailing 5Y average revenue growth rate of 11.80%, I estimated a forward 5Y revenue growth rate of 6%, with growth discounted for global recessionary pressures- particularly acute in Asian markets such as China- and overall slowed investment banking activity.

{kind=link}

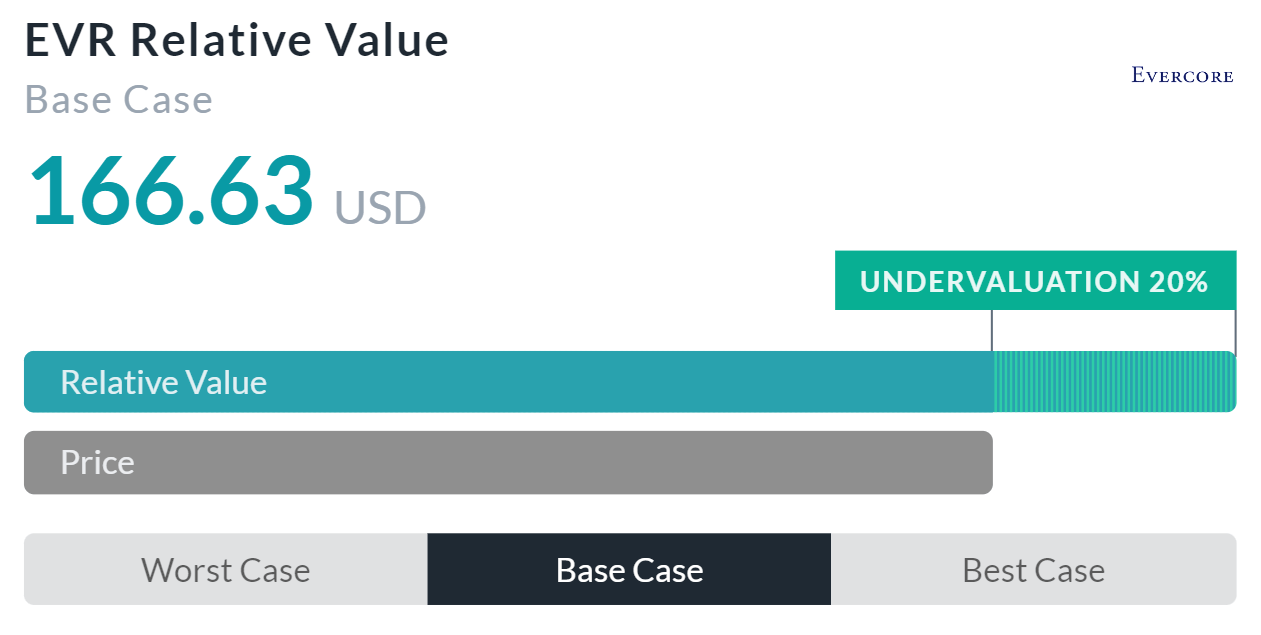

Alpha Spread's relative valuation tool estimates a much higher price ceiling for Evercore, estimating a base case relative valuation of $166.63, a 20% undervaluation.

Despite this, Alpha Spread's model's inability to adequately account for forward concerns or discount dividends means the model fails to effectively value the company.

Therefore, taking a weighted average of the company's relative value and net present value- skewed towards the NPV- the fair value of Evercore is $143.11- a 7% undervaluation.

Evercore Maintains Industry Leading Margins With Leading Cross-Industry Expertise

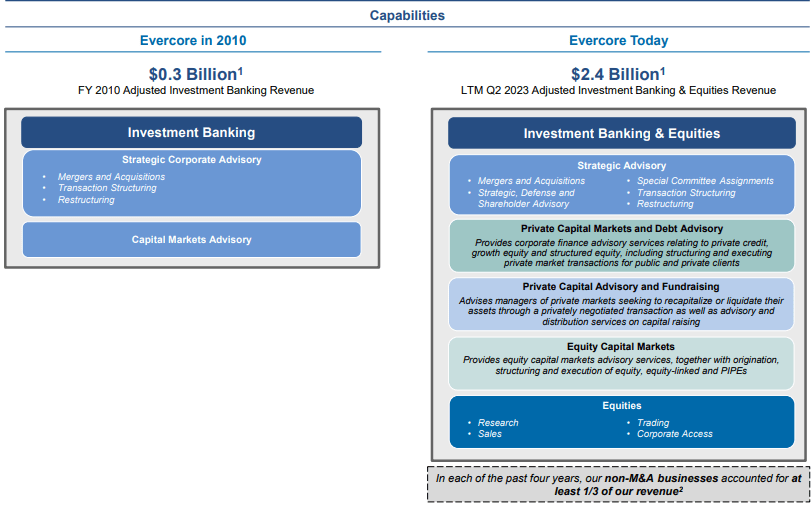

In the past decade-plus, Evercore has developed into a leader in the investment banking industry, with the fourth highest investment banking advisory fees in the past 5 years after Goldman Sachs ( GS ), JPMorgan Chase ( JPM ), and Morgan Stanley ( MS ). Much of this can be attributed to the firm's accelerated development of its capabilities and client offerings. Evercore has successfully evolved from solely offering strategic corporate advisory and capital markets advisory to those plus leading private capital markets and debt advisory, private capital advisory and fundraising, and a range of independent competencies in equities. This has resulted in investment banking revenues growing eightfold.

{kind=link}

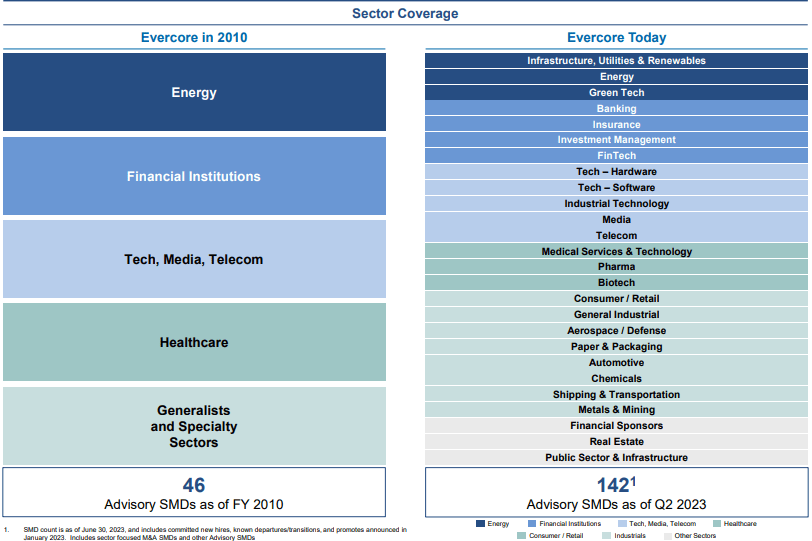

In parallel with Evercore's growth in offerings has been its growth in sector expertise. The boutique currently offers deep knowledge across highly specialized industries, manifesting the benefits of fostering in-house talent. The company is able to attract niche industry players and provide financing proficiencies superior to peers and across a wider suite of products.

{kind=link}

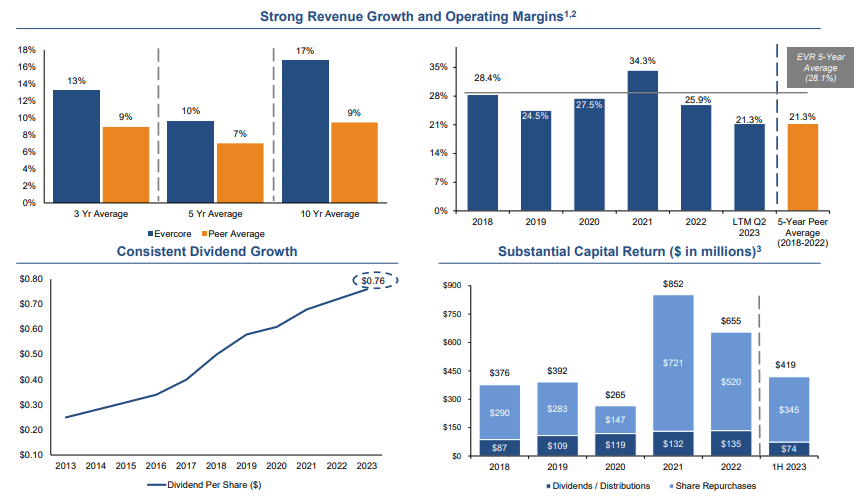

The latter two developments have largely driven Evercore's impressive, industry-leading revenue growth and operating margins. For investors, this not only means greater reinvestment in Evercore's capabilities and longer-run growth, but greater returns; investors have seen highly consistent dividend growth to $0.76 over the past decade, alongside an opportunistic multi-hundred million dollar share repurchase program.

{kind=link}

Wall Street Consensus

Analysts echo my positive but cautious view on Evercore, estimating an average 1Y price target of $150.00, a 12.47% increase from today.

{kind=link}

However, analysts are more optimistic than I am, projecting a minimum price target of $142.00, which still represents a 6.47% price increase.

I believe that analysts are underpricing the impact of recessionary pressures and economic uncertainty on the demand for Evercore's services.

Risks & Challenges

Global Recessionary Pressures Diminish Growth

The confluence of rising interest rates and slower global growth- especially in the increasingly uncertain Chinese financial market- may reduce any potential growth Evercore can capitalize upon. Moreover, Evercore's M&A is likely to see reductions in volume similar to the rest of the industry. This will lead to reduced cash flows and potentially compressed profitability.

Market is Overly Optimistic, Which May Lead to Volatile Price Declines

In accordance with Goldman Sachs, which has downgraded Evercore to neutral , I believe that the market has remained overly optimistic when concerned with the maintenance of Evercore's margins and the continuance of its operational growth. Thus, potential challenges in forward earnings may result in the market overreacting and a rude awakening of sorts, increasing the company beta and therefore associated equity risk premiums.

Conclusion

Going forward, while Evercore may be secure in the long run thanks to a strong operational strategy- which stresses expansion into Evercore's strategic capabilities and investment banking competencies- its medium-term upside seems limited by the macro environment and its previous run-up.

For further details see:

Evercore Remains A Solid Income Pick But Maintains Limited Price Upside