RE - Everest Re: Diversified Written Premiums Drive P&C Scale

2023-04-28 11:25:10 ET

Summary

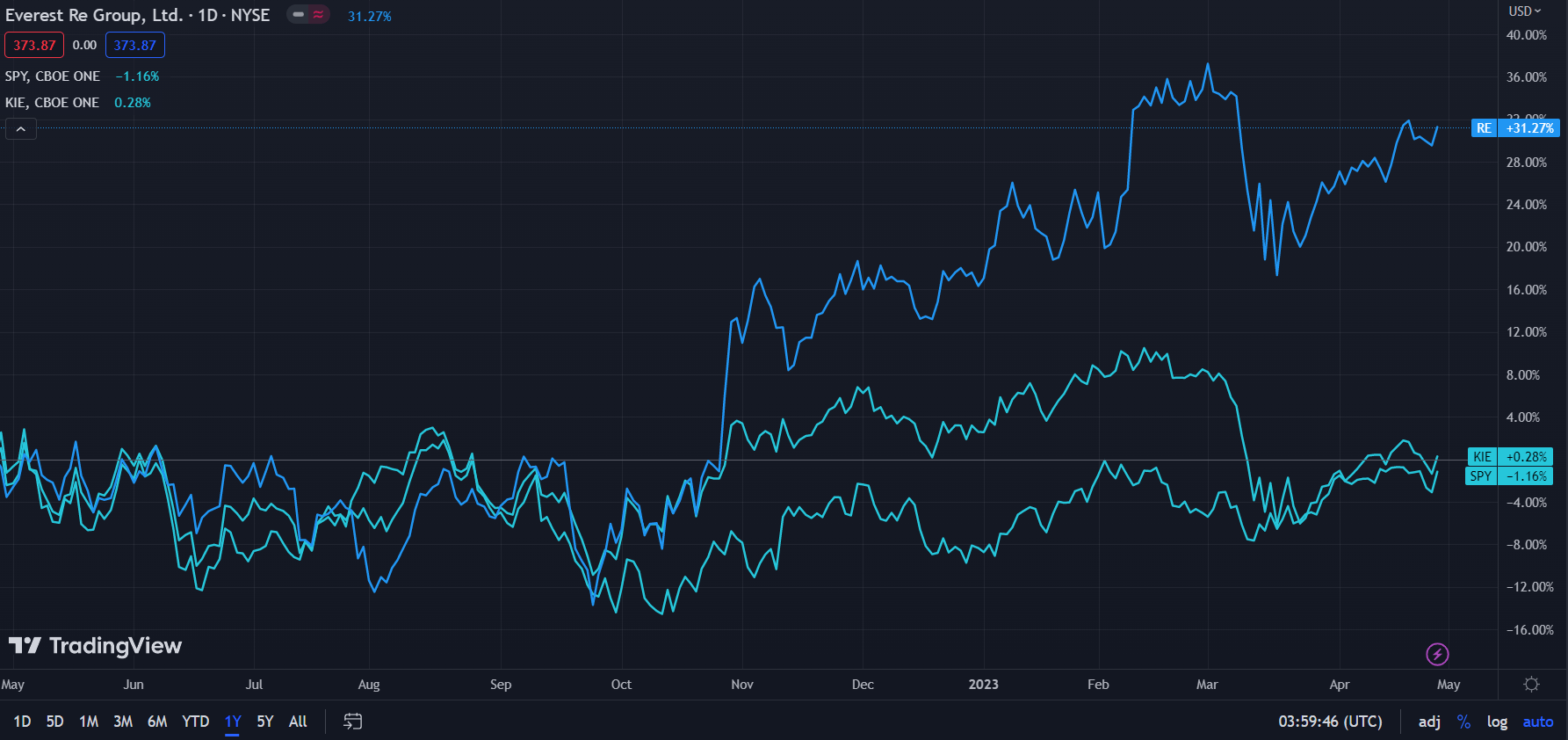

- Everest Re's 1Y performance (+32.47%) exceeds that of both the broad market (SPY: -2.82%) and the insurance industry (KIE: -0.78%).

- This growth exemplifies Everest Re's sustained revenue growth in spite of macro factors, growing annual revenues from $7.36bn in 2018 to $12.06bn in 2022.

- The insurer has experienced such growth both through the generation of operational efficiencies and exemplary risk appraisal in reinsurance and through their expansion into specialty insurance products.

- Combined with their global presence and ongoing economic-demographic trends and Everest has positioned itself for maintenance of the growth seen in the trailing 5 years.

- The synergy between existing and upcoming product lines of the company and Everest's continued commitment to quality capital management lead me to rate the company a 'buy'.

The Everest Re Group (RE) is the world's 7th largest reinsurance company, with a growing footprint in specialty insurance products, encompassing Workers' Comp insurance, short tail property insurance, and accident and health insurance among others.

This strategy has led the company to record 1Y revenues of $12.06bn in 2022, alongside a modest pre-tax income of 587.97mn.

Introduction

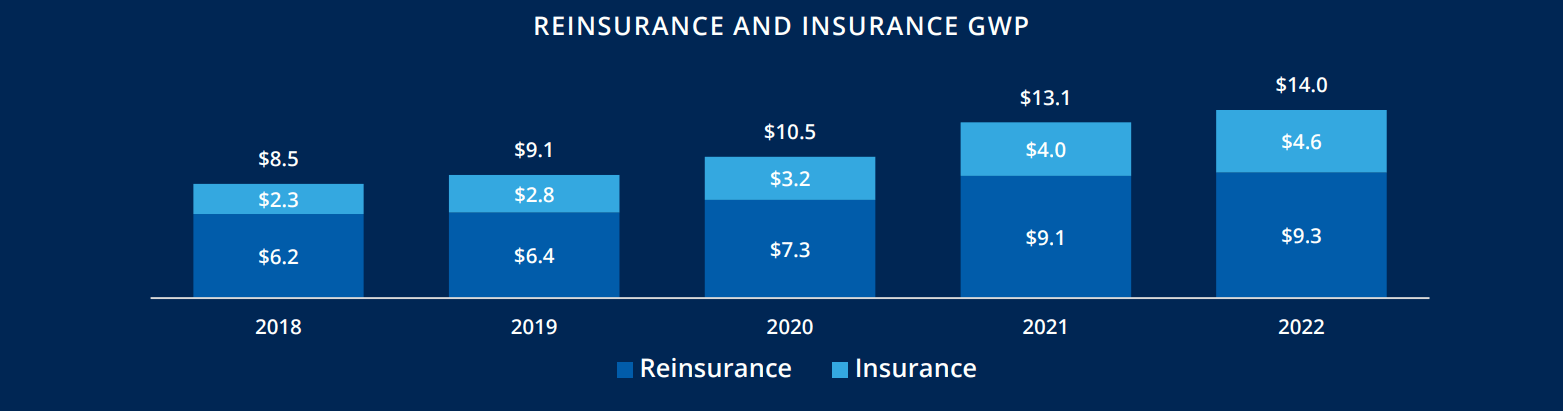

As aforementioned, Everest divides its business into two aspects; reinsurance, which includes financial lines, casualty, and property, accounted for $9.3bn in 2022 sales while primary insurance accounted for $4.6bn.

{kind=link}

While reinsurance remains the chief vertical, specialty insurance has driven revenue growth over the past few years, doubling from $2.3bn to $4.6bn since 2018, versus a 50% increase in reinsurance sales in the same time period.

Valuation & Financials

General Overview

Everest Re has experienced significantly superior returns to both the broad market ( SPY ) and the general insurance index ( KIE ).

{kind=link}

While the Everest group has demonstrated marked resilience, in spite of its relative outperformance, I believe there is room to grow, considering operational excellence and a level of undervaluation.

Comparable Companies

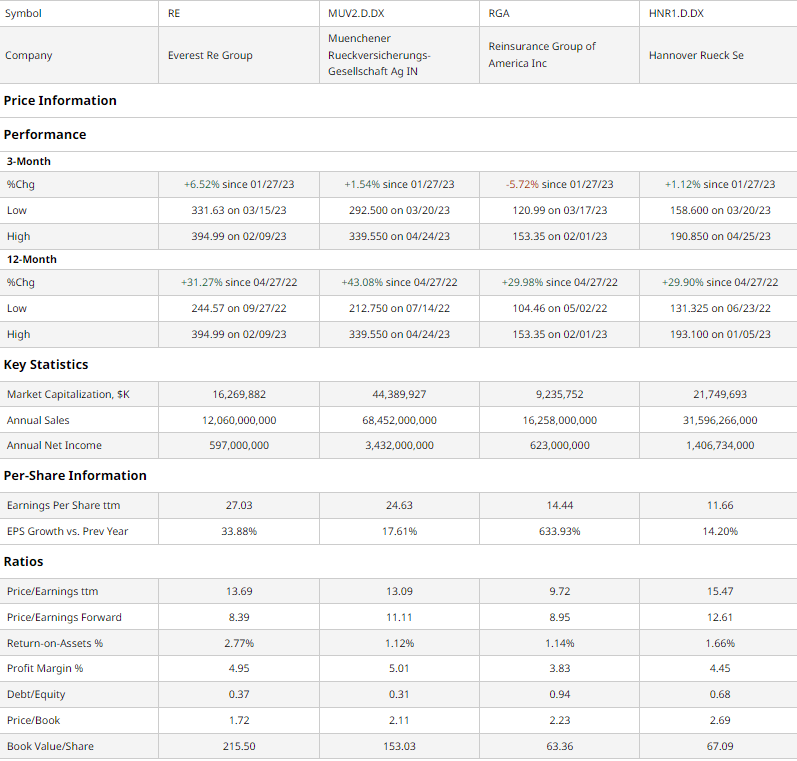

The inherently global and mutual nature of reinsurance products leads to a complex dynamic of competitors; many are state-owned, co-owned, and- even if public- a low amount of information on them. Among reinsurance companies, Munich Re (MURGY) is the largest, while the Reinsurance Group of America ( RGA ) and Hannover Ruck SE (HVRRF) are prominent groups operating as peers to Everest Re.

{kind=link}

Although, as previously discussed, Everest Re has materially outperformed the market and industry, its performance is in line with other major reinsurance firms.

Even when concerned with P/E, profit margin, etc. Everest stays consistent with its peers.

In addition, the superior P/E forward ratio, ROA, and BV/Share demonstrate why I believe Everest Re has space to grow despite its recent rally.

Valuation

According to my discounted cash flow model, Everest Re, at its base case, is undervalued by ~46%, with its fair value being ~$691.90, rather than its current price of $373.87.

The model assumes a discount rate of 10%, given both volatile macro circumstances and the inverse convexity of insurance products with interest rates.

{kind=link}

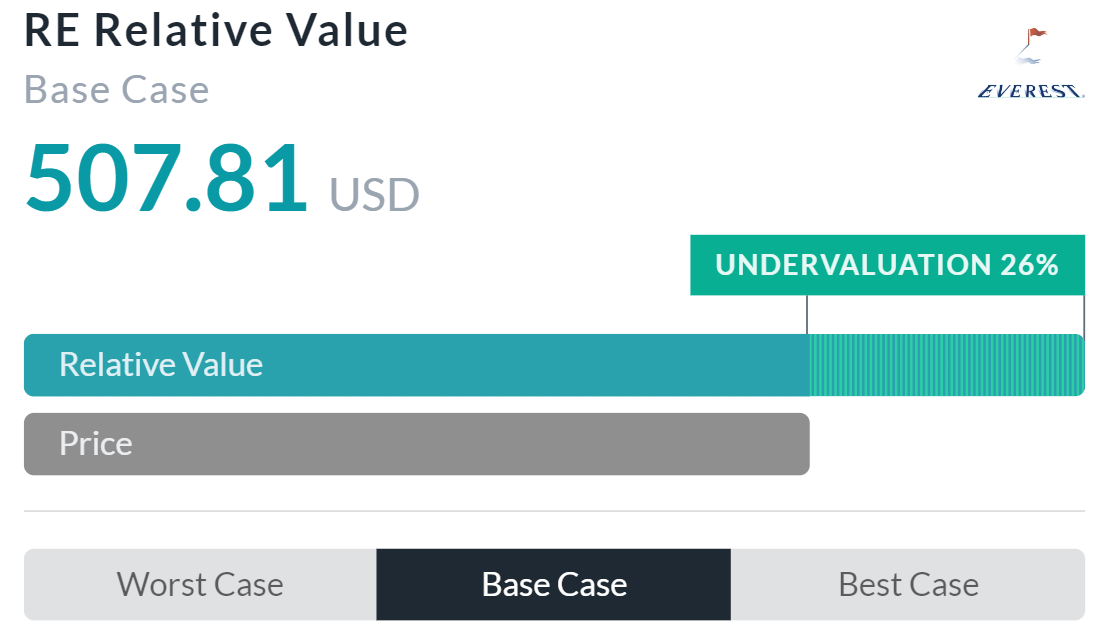

AlphaSpread's relative valuation tool reiterates this theory of undervaluation, with, at its base case, its real value projected to be 26% higher, at $507.81. This reflects superior book value multiples as well as solid earnings and cash flow multiples.

Using a mean-based approach, Everest's fair value is thus $599.86, or 36% greater than its current price.

Foray into Specialty Insurance Complements Reinsurance Presence

The dual mandate of insurance and reinsurance warrants a blend of diversification, stable income and strengthened total returns.

{kind=link}

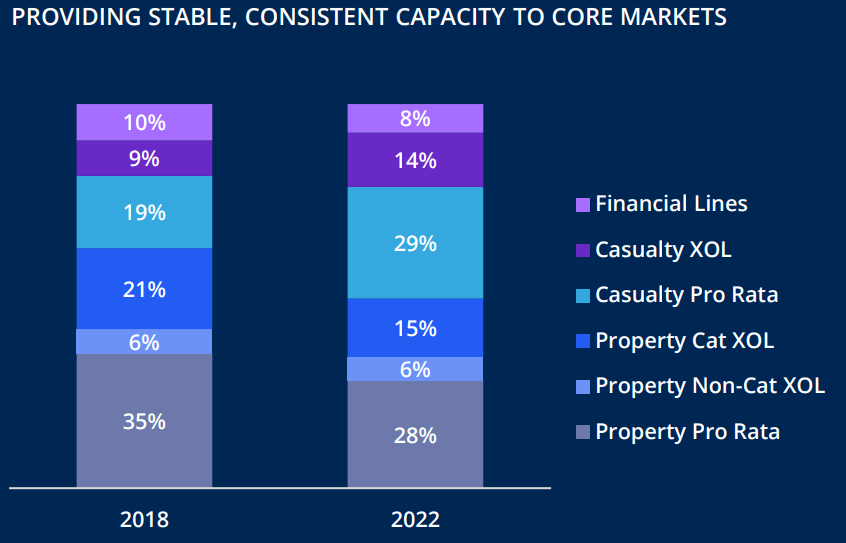

Focusing on its reinsurance platform, Everest maintains a stable attritional combined ratio at 84-86%. The company's breadth of relationships- geographic or sub-segmentation- ensures a consistently large revenue base, with an industry-leading expense ratio and constant income.

Specialty Insurance Sub-Segments (Everest Re Annual Presentation)

{kind=link}

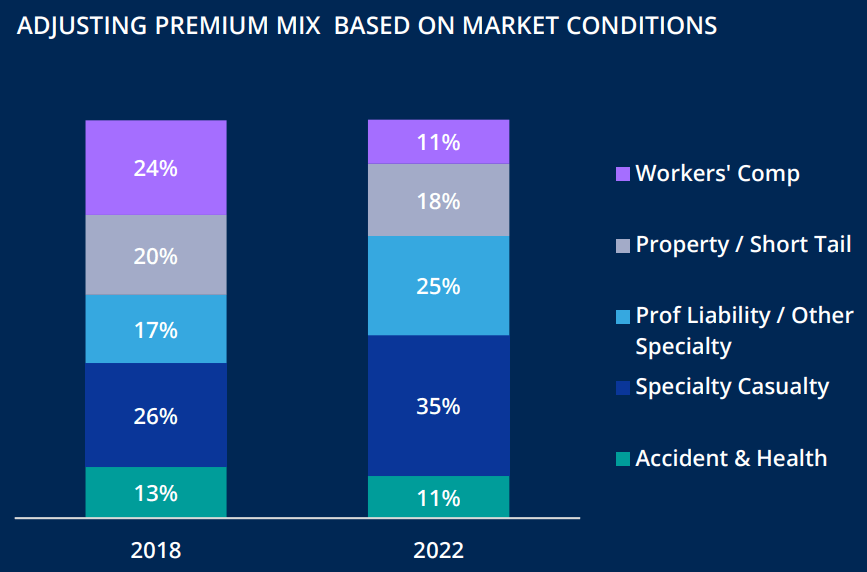

On the flip side, the company's more novel insurance segment concentrates on traditionally undercovered niches, such as workers' comp or specialty casualty. This deep-rooted underwriting in niches can help support an expanded global footprint while leveraging pre-existing reinsurance relationships.

{kind=link}

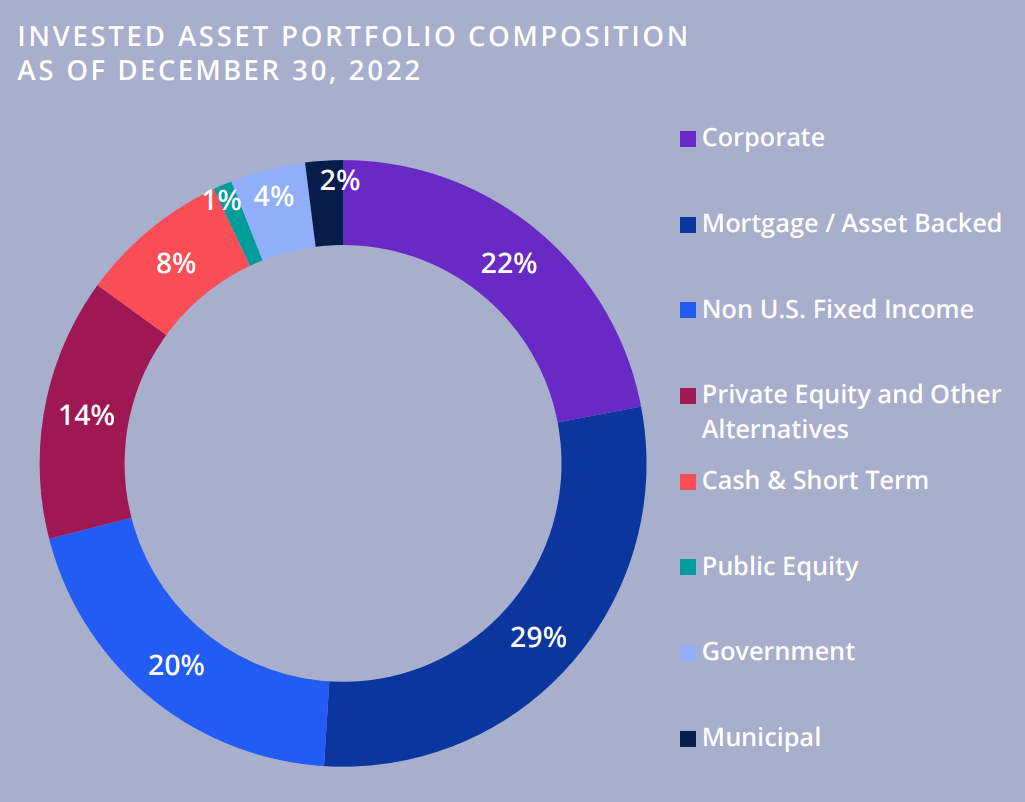

Sustaining this virtuous cycle of stable growth through reinsurance and aggressive expansion via specialty insurance, the company has committed itself to high liquidity, diversification, credit quality, and optimized risk and return portfolios.

Wall Street Consensus

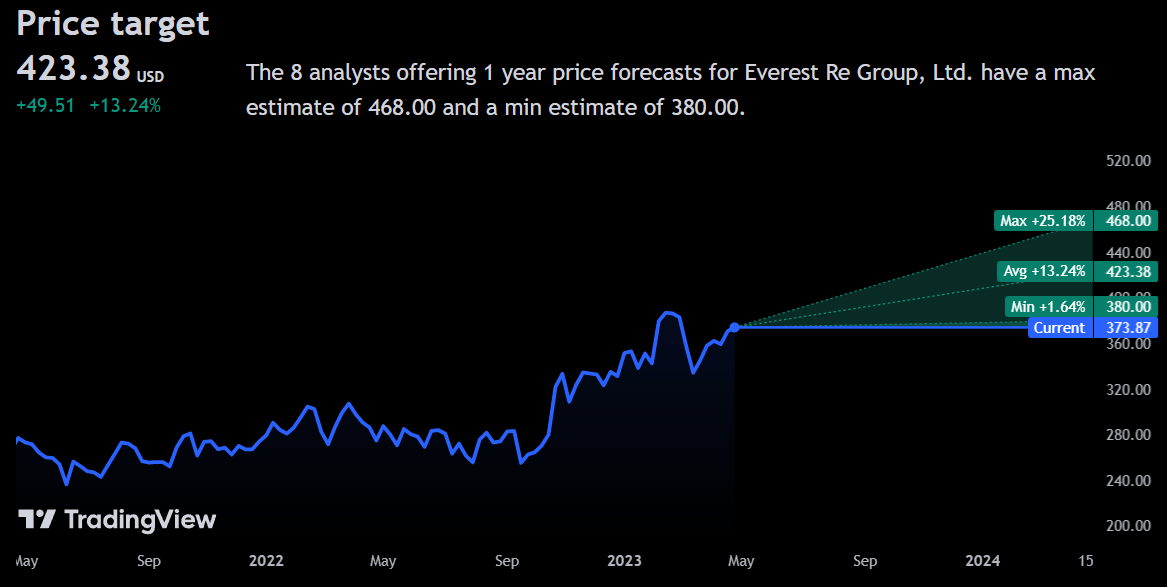

Analysts repeat my highly favourable view of the company, projecting an average price increase of 13.24% to $423.38, up from $373.87 today.

{kind=link}

And thanks to their undervaluation and consistent, baked-in growth, analysts project an absolute minimum price increase of 1.64% to $380.00.

Risks

'Act of God' Events Could Adversely Affect Results

As COVID-19 and the rise of extreme weather events due to climate change demonstrate, an increase in black swan events put downward pressure on profit margins - from 2021 to 2022, profit margins fell from 11.47% to 4.88%, for instance. Continued pressure from such an impact can heavily reduce competition. By working within the bounds of specialty insurance, Everest is attempting to dampen the effect of market and macrocycles, though it is unknown how well this will work with sustained pressures.

Continued Complexity in Assessing Underwriting Risk

Especially as the company moves in the direction of providing specialty insurance, it has become increasingly difficult to adequately understand the risks and rewards prevalent in certain insurance policies. A constant failure to do so can risk long-term financial and operational success.

Regulatory Pressures Can Put Downward Pressure on Prices

Concerning their P&C reinsurance and insurance products, the increased costs borne by climate events among other macro effects have led to consumer dissatisfaction and increased regulatory scrutiny. Any government and regulatory acts limiting price increases or risk assessment can thus lead to financial loss or reduced scale.

Conclusion

In the short term, I believe that Everest's undervaluation and strength in its traditional reinsurance business will support a rally.

In the long term, operational success in specialty insurance alongside portfolio optimization will support a long-term upwards trajectory.

For further details see:

Everest Re: Diversified Written Premiums Drive P&C Scale