RE - Everest Re: P&C Strategy And Localized Growth Support A Reversion Theme

2023-07-09 10:00:44 ET

Summary

- Everest Re, a multinational provider of reinsurance and insurance products, is rebranding as 'Everest Group' and changing its ticker to 'EG' to reflect its dual focus on reinsurance and primary insurance products.

- The company's Q1 revenues were $3.29bn, a 13.45% YoY increase, with a net income of $360.00mn, up 22.54% YoY, and a free cash flow of $1.20bn, up 19.01% since Q1'22.

- Combined with operational growth driven by macro tailwinds for reinsurance, segmented diversification, and geographic growth, this leads me to rate Everest a 'buy'

Everest Re ( RE ) is a Warren, New Jersey-based multinational provider of reinsurance and insurance products, with operations across financial, casualty, and property reinsurance and workers comp, property, liability, specialty casualty, and accident and health insurance products.

The latter dual focus on reinsurance and primary insurance products has led to a significant corporate rebrand, de-emphasizing reinsurance by renaming the company 'Everest Group' and changing its ticker to 'EG'. This rebrand is set to be completed on July 10.

{kind=link}

The firm's activities have supported Q1 revenues of $3.29bn- a 13.45% YoY increase-alongside a net income of $360.00mn- up 22.54% YoY- and a free cash flow of $1.20bn-up 19.01% since Q1'22.

Introduction

In light of its pivot toward primary insurance, Everest has developed a sixfold macro strategy, focused on the use of Everest's market leadership for optimal pricing, the scalability of global franchises through localized approaches, financial resilience through strong liquidity and coverage rations, the retention of high quality and integrated talent to support a disciplined underwriting strategy, all culminating in the pursuit of operational excellence throughout the firm's business verticals.

{kind=link}

On a tactical level, Everest has manifested this strategy through a trifold operational plan, with geographic and segmented franchises leading Everest's growth, supported by talent-oriented and culture-supporting behaviours and operational excellence driven by capital allocation and a strong combined ratio.

{kind=link}

Since I previously rated Everest, the stock has experienced a >7% price decline, though, operationally, little has changed.

As such, the combined accretive effect of Everest's geographic growth strategy, leadership in primary insurance and reinsurance scalability, alongside a moderate undervaluation leads me to rate the company a 'buy'- in line with my previous evaluation.

Valuation & Financials

General Overview

In the TTM period, Everest-up 22.97%- has experienced superior price action to both TradingView's Insurance Index-up 3.09%- and the broad market, represented by the S&P 500 ( SPY )- up 12.74%.

{kind=link}

The relative underperformance of insurance companies is likely a product of rising interest rates, which have diminished portfolio values and downstream demand for insurance products.

Everest, however, runs with more inelastic demand between its reinsurance and specialized insurance capabilities and has thus been able to develop superior pricing capabilities.

As such, going forward, I believe Everest will continue to rally despite macro uncertainties.

Comparable Companies

The reinsurance industry and primary insurance industries have become increasingly integrated over the years, with high levels of forward and backward integration to support risk management and cash flow generation. As such, Everest is most comparable to similarly sized reinsurance companies, who oftentimes maintain similar dealings in primary insurance. These include firms such as RenaissanceRe ( RNR ), Chesterfield, Missouri-based Reinsurance Group of America ( RGA ), and the German HannoverRe ( HVRRY ).

{kind=link}

As demonstrated above, Everest's stock has experienced the poorest YoY performance alongside the second-poorest quarterly price action. Although Everest, alongside other major reinsurance companies, has experienced positive yearly price action, I believe the firm's underperformance reflects investor anxieties about erratic YoY revenue and net income growth.

Despite this, Everest maintains strong multiples-based value and outsized growth and reinvestment capabilities.

For instance, Everest retains the second-lowest trailing P/E, alongside the lowest forward P/E ratio, and the highest book value per share, representing a strong income statement and balance sheet.

Additionally, with peerless 5Y earnings growth, best-in-class ROA, and the second-lowest debt-equity in the comparable group, Everest sustains reinvestment and capex capabilities alongside proven return capabilities on investments.

All this is topped off by Everest's second-best dividend, which works alongside opportunistic share repurchases for a balanced shareholder return.

Valuation

According to my discounted cash flow model, at its base case, Everest's fair value is $432.92, which means, at its current price of $351.28, the stock is currently undervalued by 19%.

My model, calculated over 5 years without perpetual growth built-in, assumes a discount rate of 8%, addressing Everest's overall debt-light capital structure and a low equity risk premium. Additionally, for a more conservative projection, despite an average 5Y revenue growth rate of 16.27%, I project a revenue growth rate of 8% and declining, expecting downstream demand pressures to reduce scalability.

{kind=link}

Alpha Spread's multiples-based relative valuation tool more than validates my thesis on undervaluation, estimating an undervaluation of 42%, meaning the stock's relative value is $607.53.

Therefore, taking an average of my analysis and Alpha Spread's relative valuation, the fair value of Everest should be $520.23, leading to an undervaluation of 30.5%.

Streamlined Growth Strategy Couples With Resilient Financials For Accretive Growth

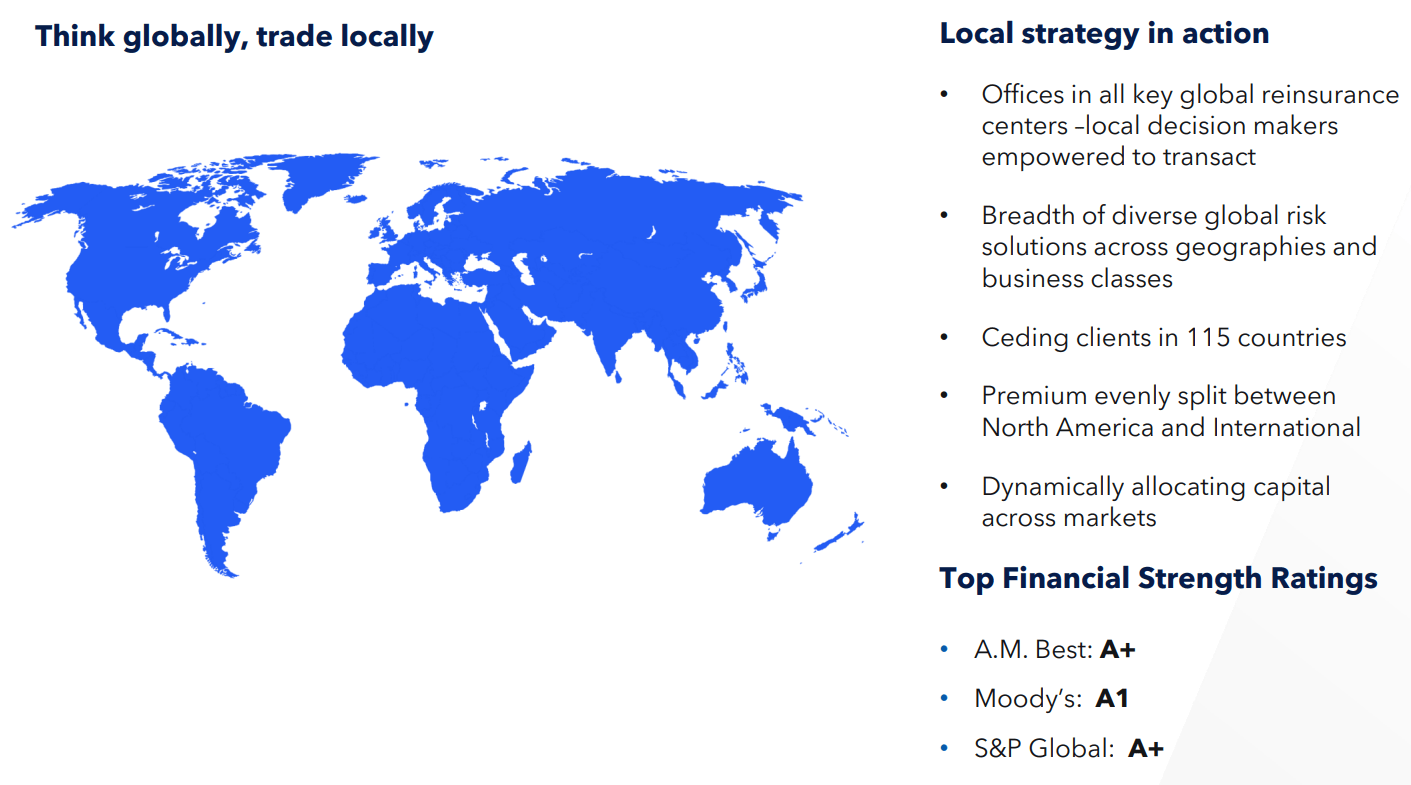

The chief advantage Everest has been able to operate with has been scale, being a top 10 major reinsurer. To promote integrated growth and long-run margin growth, Everest is looking towards international growth, driven by its reputational premium and strong financial position. To capture client growth and upsell between its reinsurance and primary insurance products, Everest has adopted a strategy of localized franchise growth, enabling largely independent operations supported by Everest's international presence and financial capabilities.

{kind=link}

At the core of Everest's business, however, remains reinsurance. To carve a niche for themselves, Everest has focused on P&C reinsurance on the basis of bilateral relationships with insurers. With favourable macroeconomic conditions-including rising insurance losses, inflation, and catastrophic risks, Everest, alongside other P&C reinsurance majors, has been able to support optimized pricing models, supporting elevated profitability and leading to bullish sentiment from Wall Street. The firm has seen upgrades from Morgan Stanley ( MS ) and Citigroup ( C ) in the past 20 days. This anticipated growth has supported Everest's decision to initiate a $1.65 dividend.

{kind=link}

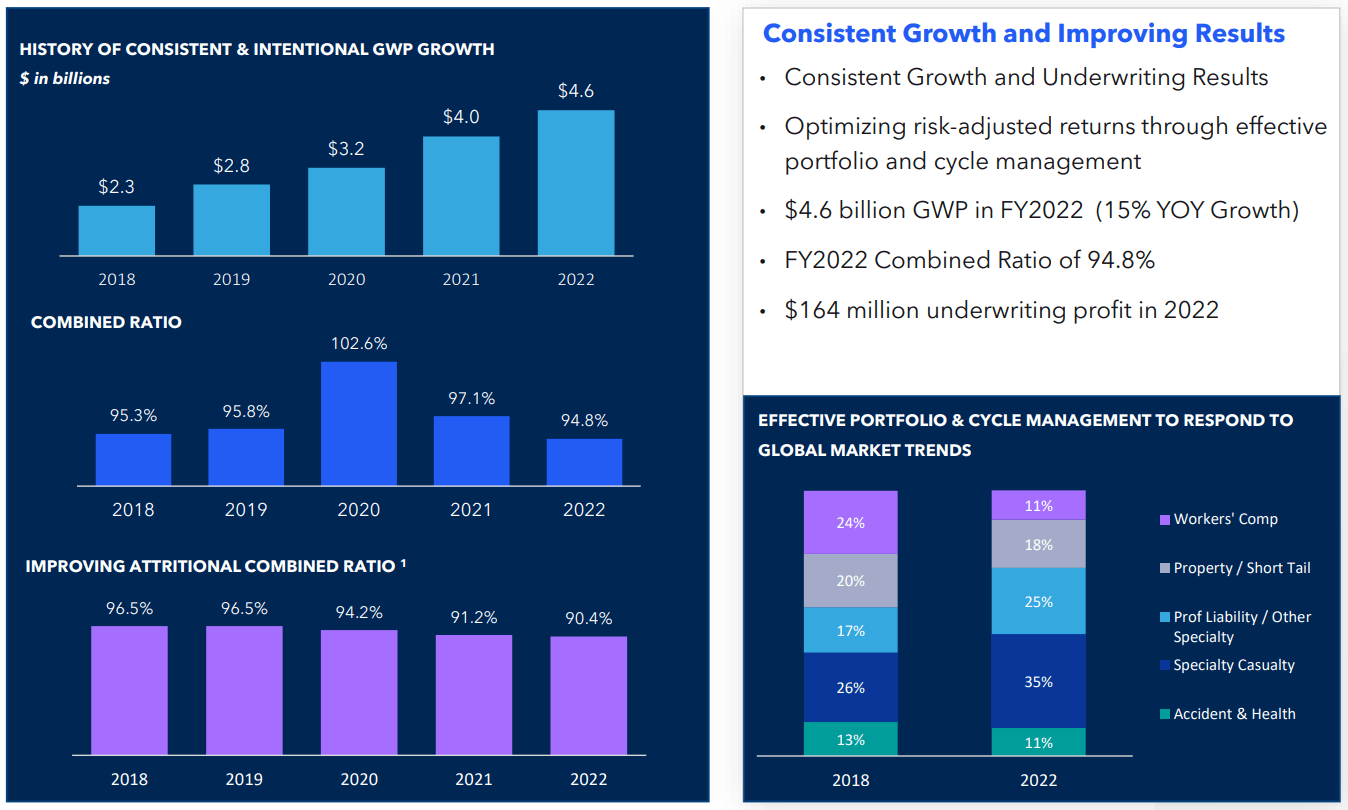

Regardless of reinsurance tailwinds, Everest has zeroed in on specialty primary insurance as a means of scale and margin expansion. The said strategy has seen Everest involved in a diverse array of insurance practices and building a competitive moat. Through this, the firm has experienced 15% YoY growth in GWP, supporting accretive revenue and profit growth.

{kind=link}

Wall Street Consensus

Analysts largely echo my positive opinion of the stock, estimating an average 1Y price increase of 22.21% to a price of $429.30.

{kind=link}

Even at the minimum projected 1Y price target of $390.00, analysts expect Everest to go up by 11.02%, reflecting Wall Street's opinion that the market has underpriced Everest's market position and operational capabilities.

Risks & Challenges

Expansion Into Primary Insurance Invites Complexity

Although Everest has professed strong capabilities across specialized primary insurance products, seeing outsized growth and client retention, Everest nonetheless must contend with increased regulatory and financial complexity as a result of segmented and geographic complexity. As such, any increased stressors may reduce Everest's operational flexibility, leading to potential reductions in long-run scale growth and cash flow generation capabilities.

Rising Interest Rates Continue to Drive Uncertainty

A key reason why the insurance industry, as demonstrated in the 'General Overview' section, has underperformed the general market has been its exposure to fixed-rate bonds, which demonstrate an inverse convexity to interest rates. As such, regardless of Everest's expansion into primary insurance, Everest's reinsurance market is exposed to reductions in demand as a result of rising interest rates harming the net incomes of insurers, thus reducing scale growth.

Conclusion

Looking forward, Everest's macro-supported pricing capabilities, alongside growth across specialty primary insurance and geographies, will enable scale and margin growth for years to come.

For further details see:

Everest Re: P&C Strategy And Localized Growth Support A Reversion Theme