EVRG - Evergy: A Solid Choice As Recession Seems Imminent

2023-10-16 16:58:57 ET

Summary

- Evergy, Inc. is a regulated electric utility serving customers in Kansas and Missouri, with a service territory that includes multiple large cities.

- The company is well-positioned to handle an economic downturn and offers stability in the face of a recession.

- Evergy's growth prospects rely on population growth in its service territory and expanding its rate base through investments in infrastructure.

- The company's interest expenses are rising, which is increasingly a concern. However, it remains in a stronger financial position than many of its peers.

- The company's 4.90% yield appears to be sustainable, and its current valuation appears reasonable.

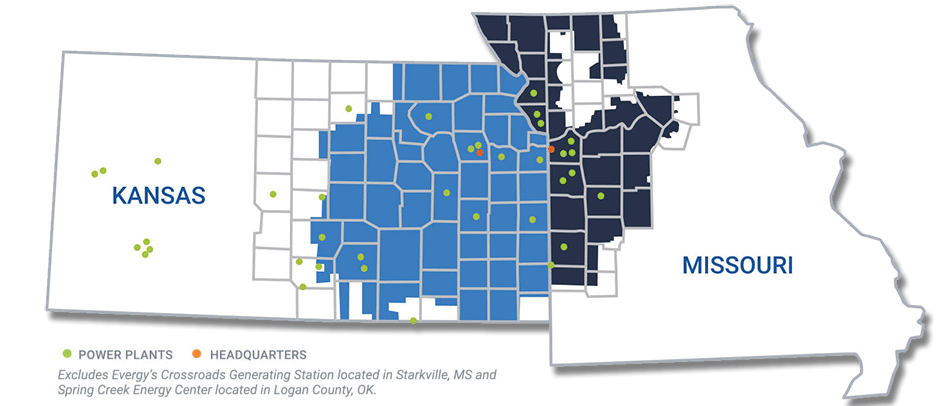

Evergy, Inc. ( EVRG ) is a regulated electric utility that serves customers in Kansas and Missouri. Admittedly, neither of these states is particularly well known for its high population, but the states do contain a few very large cities. Evergy’s service territory includes these cities, as we can see here:

{kind=link}

The company enjoys many other characteristics that have long made utility companies popular holdings among retirees and other conservative investors. In particular, the company should prove highly resilient in the face of any economic weakness. We are starting to see signs that this economic weakness may be rapidly approaching, as a few retailers recently have started to warn about a decline in consumer spending. Citibank ( C ) has noted a similar trend in the credit card spending data. Evergy should be well positioned to handle a weakening economy with ease, however, which could mean that it could be a good holding for an investor who is seeking to ride through a recession with a certain amount of ease.

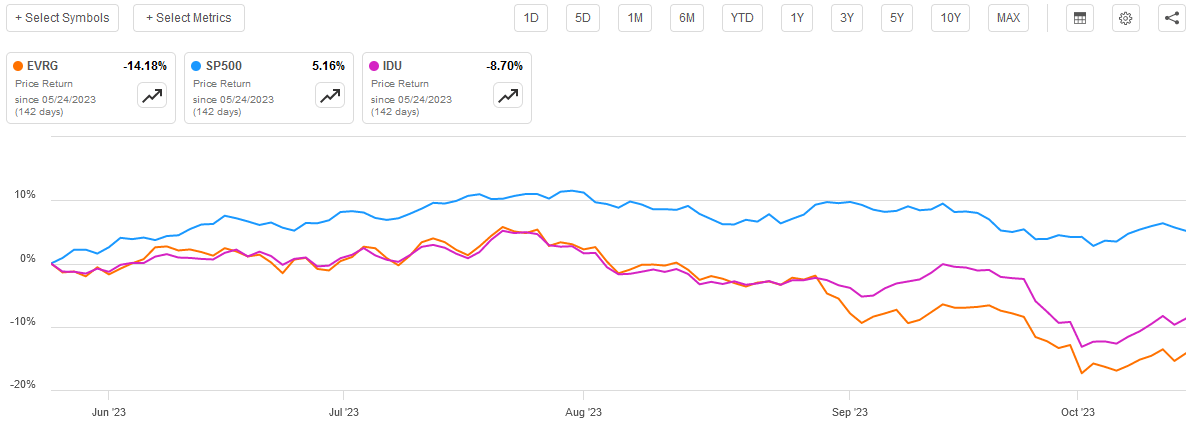

As regular readers can likely recall, we last discussed Evergy in late May of this year. Unfortunately, the stock has not performed particularly well since that time. As we can see here, shares of Evergy are down 14.18% since my previous article on the company was published. This is worse than either the S&P 500 Index ( SP500 ) or the U.S. Utilities Index ( IDU ) has delivered since that date:

{kind=link}

We will discuss the reasons for this decline in this article, but in short Evergy trades much like a bond due to its low growth rate and high dividend yield. Indeed, as of right now, the stock has a 4.90% dividend yield. That is quite a bit better than many of its peers offer, and it is high enough to draw the attention of income-focused investors. However, the stock’s yield is still slightly lower than a good money market fund is offering. The stock’s decline has also caused the company to boast the most attractive valuation that it has had in years, so now could be a good time to buy into the company. Let us investigate.

About Evergy, Inc. And Its Growth Prospects

As stated in the introduction, Evergy is a regulated electric utility that serves customers in Western Missouri and Eastern Kansas. The company’s service territory makes a great deal of sense because it was formed through a 2018 merger between Great Plains Energy in Missouri and Westar Energy in Kansas. The company’s service territory includes the largest city in Missouri (Kansas City), as well as the state capital of Kansas (Topeka). Thus, despite the reputation that much of the Great Plains region possesses, the company serves approximately 1.7 million customers, so it is certainly not a small utility company.

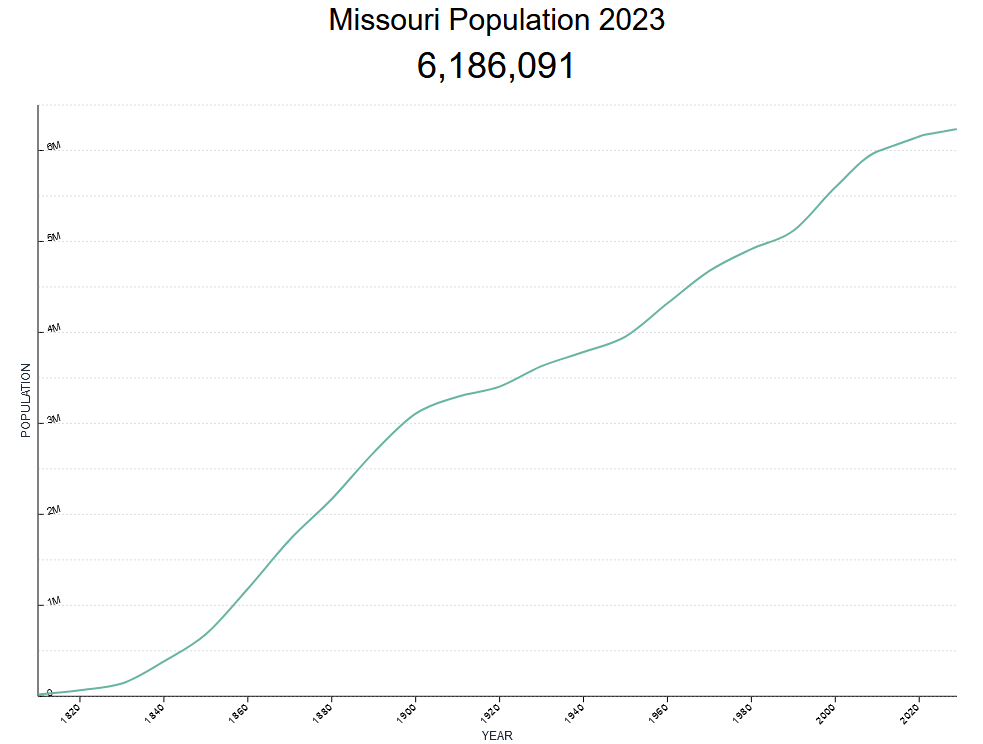

One of the nice things about the company’s service territory is that it is experiencing population growth. This is particularly true in Missouri, which the U.S. Census Bureau projects is growing at a 0.18% annual rate:

{kind=link}

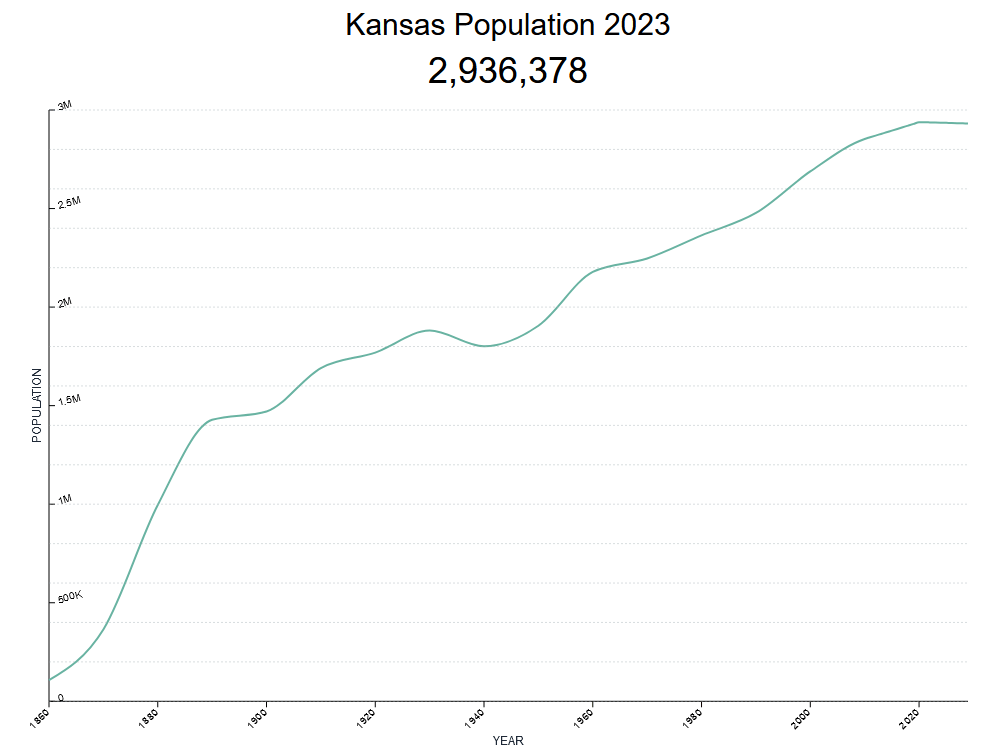

Kansas is not benefiting from growth to the same degree, although it is not suffering from a declining population to nearly the same degree as some other states are:

{kind=link}

As we can see above, the state’s population is expected to be relatively stable through the end of the decade. Officially, the U.S. Census Bureau puts the state’s population growth rate at -0.03%, but that only represents 772 people annually, which is negligible. There are numerous states whose population is declining much more rapidly than Kansas. For its part, Evergy is easily able to adjust for the very slight decline in the Kansas population through growth in Missouri. Overall, the demographics for the company are favorable.

The reason that this is important for Evergy is that population growth in its service territory is one of the only ways that the company can generate growth. After all, the more customers that it has paying their monthly bills, the more revenue the company will bring in all else being equal. That means that it has more money available that it can use to cover its expenses and ultimately make its way down to net income. Unfortunately, the demographics of the company’s service territory are completely out of the company’s control, so it is nice to see that Evergy has some tailwinds here.

As we can see though, the population of the company’s service territory is almost certainly going to grow at an incredibly slow pace. If the company was entirely dependent on adding new customers, it would be unlikely that it could deliver a growth rate that is at all acceptable to the typical common stock investor. Fortunately, Evergy has another method through which it can grow its earnings. This is by expanding its rate base. I explained how this works in my previous article on the company:

One of the ways in which Evergy will achieve earnings growth is by expanding its rate base. The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the amount that it charges its customers in order to earn that specified rate of return. The usual way that a utility company expands its rate base is by investing money into upgrading, modernizing, or possibly expanding its utility-grade infrastructure.

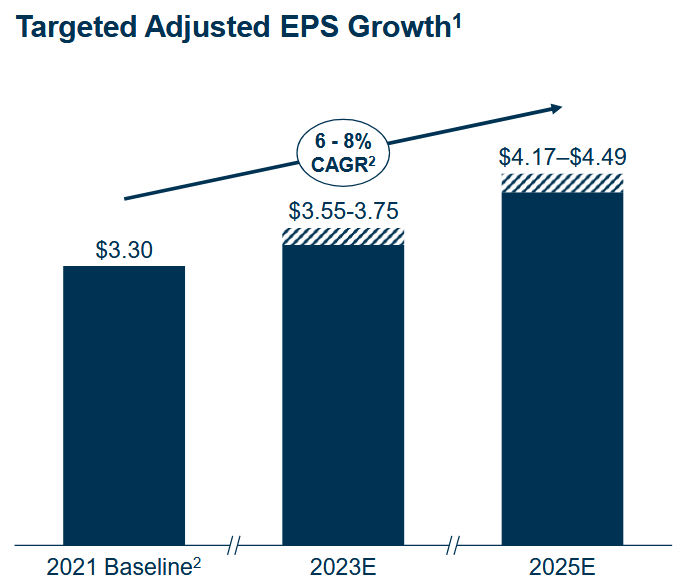

In the company’s second-quarter earnings conference call , Evergy stated that it intends to invest $11.6 billion into expanding its rate base over the 2023 to 2027 period. The company projects that this will expand its rate base at a 6% compound annual growth rate over the period. This is reasonable and it is in line with what many of the company’s peers are likely to deliver over the same period. Curiously, though, the company gave no guidance with respect to the impact that this would have on its earnings per share growth over the period. The company only stated that it expects to achieve a 6% to 8% earnings per share growth rate over the 2021 to 2025 period:

{kind=link}

It would be somewhat reasonable to assume that the company should be able to continue to grow its earnings per share at this growth rate through 2027, but it depends on how it intends to finance its spending. If it issues equity to fund its capital spending, then obviously the earnings per share growth rate will be reduced because of the resulting stock dilution. It could partially, or fully, fund its capital spending with debt as well. That is the usual way through which these companies fund their capital spending, but of course, that results in the company’s interest expenses going up with the passage of time. Evergy has already seen its interest expenses increase significantly over the past few years:

{kind=link}

(All figures in millions of U.S. dollars.)

Thus, borrowing more money to fund rate base expansion will drive interest rates up more than the company has already seen. This is true now more than ever since it seems likely that high interest rates will be with us for quite some time. The fact that the company’s interest expenses will be going up is not necessarily a problem as long as it can increase its rates rapidly enough to keep up with the rising interest expenses, but it is uncertain that this will be the case as regulators might try and keep rate hikes at a minimum for political reasons. Thus, it seems likely that trying to fund its capital expenditures solely through debt issuance will almost certainly be a drag on earnings per share growth.

If we assume that the company will manage to grow its earnings per share at the same rate as its rate base growth, then Evergy should be able to give investors an 11% to 13% total average annual return. That is quite a bit above what the company’s peers are likely to deliver over the same period, so it may be unlikely that we will actually get a total return this high. Analysts are projecting a 4.82% earnings per share growth rate, which reduces the company’s total return to about 10% annually, which is in line with peers. It appears that the market may agree with analysts here, and that could be one big reason why the stock has declined over the past five months.

Stability In The Face Of A Recession

As I mentioned earlier in this article, one of the nice things about Evergy is that the company’s revenue and earnings should prove to be reasonably stable regardless of the conditions in the broader economy. This has been the case over the past few years, which we can see in this chart. Here are the company’s total revenues during each of the past eleven twelve-month periods:

{kind=link}

As we can see, there have been relatively few fluctuations in the company’s revenues despite the fact that there were some changes in economic conditions over this period. For example, earlier periods will still include the effects of the pandemic lockdowns and the economic struggles associated with people voluntarily taking action to avoid contact with others out of fear of contracting the disease. Later periods include both the economic recovery and the surging inflation rate that started to pressure household budgets. We can see that none of these things had any real effect on the company’s revenues.

We see much the same thing when we look at the company’s operating income. This chart shows the company’s operating income during the same periods:

{kind=link}

This chart shows the company’s net income over the same periods:

{kind=link}

We do see some pressure on the company’s net income in more recent periods (mid-2022 and later) as net income declined a bit compared to earlier periods. This does not defeat our overall thesis regarding the company’s financial stability, however. Rather, it reinforces my earlier point about rising interest rates beginning to be a drag on financial performance. The fact that operating income remained stable alongside revenue, but net income started to weaken strongly suggests that the company’s rising interest expenses are a drag on net income. After all, its operations are clearly fine despite the inflation and steep decline in real wages that its customer base has been suffering from.

In my last article on the company, I explained why Evergy’s operating performance tends to be reasonably consistent:

The reason for this general stability is that Evergy provides a product that is generally considered to be a necessity for our modern way of life. After all, how many people today do not have electric service to their homes and businesses? While there are still a surprising number of senior citizens that do not have Internet access, which many people would likewise classify as a necessity today, these individuals still have electricity. As such, most people will prioritize paying their electric bills ahead of any discretionary expenses during times when money gets tight.

As mentioned in the introduction, there are signs that consumers may be starting to get tapped out as inflation continues to reduce the purchasing power of the U.S. dollar. For example, U.S. spending on luxury goods is now right about in line with pre-COVID levels, following a surge in 2021:

{kind=link}

The signs of consumer weakness are not simply in luxury goods spending, however. Earlier this month, Bill Simon, former CEO of Walmart ( WMT ), told CNBC that consumers are starting to buckle for the first time in a decade. The CNBC news release stated:

He’s blaming a list of headwinds weighing on consumers including inflation, higher interest rates, federal budget wrangling, polarized politics and student loan repayments – and now new global tensions connected to violence in Israel.

The market appears to agree with this assessment, as shares of Amazon.com ( AMZN ), Target ( TGT ), and Walmart are all down over the past two months.

Consumer spending has been perhaps the only thing holding up this economy, as the Leading Economic Indicators have all been pointing negative for quite a while. Thus, if the consumer really has reached their breaking point, as Mr. Simon suggests, that could be the final factor that officially tips the United States into a recession.

As we have already seen though, Evergy should be better positioned to weather such an economic downturn than many other companies. After all, the product that it provides is a necessity and it seems likely that people will continue to pay their electric bills even if they do not want to go shopping. Thus, the company might be able to provide something of a safe haven for investors.

Financial Considerations

As I pointed out in my previous article on Evergy:

It is always important that we investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is normally accomplished by issuing new debt and using the proceeds to repay the existing debt. This can cause a company’s interest expenses to increase in certain market conditions.

As we have already seen, Evergy has been seeing its interest expenses go up due to the fact that interest rates are now at the highest levels that we have seen since early 2001. There is still a risk that they may increase further, so we need to be prepared for this and ensure that the company is not overly leveraged.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. As of June 30, 2023, Evergy had a net debt of $12.8732 billion compared to $9.5507 billion in shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.35 today. This is quite a bit above the 1.30 ratio that the company had the last time that we discussed it, which is rather concerning. After all, this implies that the company is increasing its leverage and thus its overall reliance on debt specifically at a time when we do not want it to be doing that.

However, the most important thing is whether it is relying too much on debt. The best way to determine that is to compare its ratio to its peers:

| Company |

| Net Debt-to-Equity |

| Evergy, Inc. |

| 1.35 |

| DTE Energy ( DTE ) |

| 1.89 |

| Public Service Enterprise Group ( PEG ) |

| 1.28 |

| Eversource Energy ( ES ) |

| 1.58 |

| The AES Corporation ( AES ) |

| 4.05 |

| Entergy Corporation ( ETR ) |

| 1.92 |

Evergy is not the only company on this list that has increased its net debt-to-equity ratio since the last time that we discussed it. In fact, quite a few of these companies have seen their ratios go up. However, that does not mean that we can ignore the increasing leverage. Fortunately, for now, Evergy appears to be less reliant on debt to finance its operations than many of its peers, so it does not appear that the company is too highly leveraged. We just want to keep an eye on its finances as debt poses more risks in today’s high-interest rate environment than it used to.

Dividend Analysis

One of the biggest reasons why investors purchase shares of utility companies is that these firms tend to have higher dividend yields than many other things in the market. Evergy is certainly no exception to this, as the company’s current 4.90% yield is substantially higher than the 1.51% yield of the S&P 500 Index ( SPY ) as well as the 2.97% yield of the U.S. Utilities Index. Evergy’s dividend yield also compares quite well to that of its peers:

| Company |

| Dividend Yield |

| Evergy, Inc. |

| 4.90% |

| DTE Energy |

| 3.89% |

| Public Service Enterprise Group |

| 3.75% |

| Eversource Energy |

| 4.91% |

| The AES Corporation |

| 5.04% |

| Entergy Corporation |

| 4.58% |

We can see that Evergy’s dividend yield is higher than all of its peers except for Eversource Energy and The AES Corporation. These companies have both been under a great deal of pressure due to their debt loads and rising interest expenses, so it makes sense that their yields would be pushed up just like Evergy’s. However, all of the companies on this list currently boast much higher yields than they did at the start of this year.

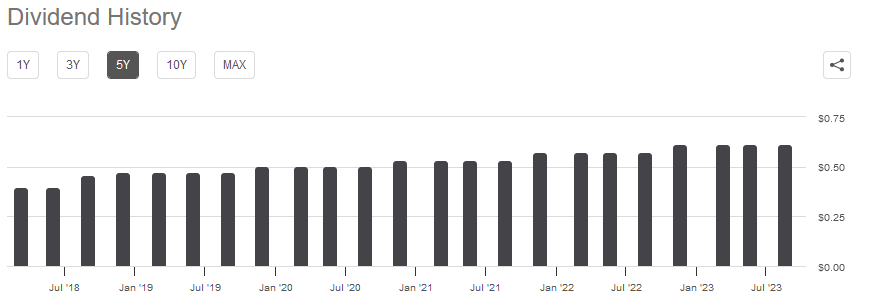

Evergy has a long track record of boosting its dividend on an annual basis, which we can clearly see here:

{kind=link}

This is something that is very nice to see in today’s inflationary environment because it helps to offset the decline in purchasing power that the dividend would otherwise suffer over time. That is something that could be a very big problem for anyone who is dependent on their portfolio for income, such as most retirees.

As is always the case, however, we want to ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut that reduces our incomes and almost certainly causes the company’s share price to decline.

The usual way that we judge a company’s ability to pay its dividends is by looking at its free cash flow. During the twelve-month period that ended on June 30, 2023, Evergy reported a negative levered free cash flow of $1.3539 billion. That was obviously not enough to pay any dividends, but the company still paid out $883.7 million to its shareholders. At first glance, this is likely to be concerning as the company is not generating enough cash internally to cover both its capital expenditures and its dividends.

As I have pointed out in the past, it is common for utilities to finance their capital expenditures through the issuance of debt and equity, while paying their dividends out of operating cash flow. This is done because of the extremely high costs involved in constructing and maintaining a utility-grade infrastructure network over a wide geographic area. During the most recent twelve-month period, Evergy reported an operating cash flow of $3.5955 billion. This was more than sufficient to cover the $883.7 million that the company paid out in dividends with a substantial amount of money left over for other purposes. Overall, the company’s dividend appears to be reasonably safe here.

Valuation

According to Zacks Investment Research , Evergy will grow its earnings per share at a 4.82% rate over the next three to five years. This gives the stock a price-to-earnings growth ratio of 2.89 at the current price. That is substantially less than the 3.14 ratio that the stock had the last time that we discussed it, which makes sense considering the decline in the share price that the stock suffered over the past few months. Here is how Evergy’s valuation compares to its peers:

| Company |

| PEG Ratio |

| Evergy, Inc. |

| 2.89 |

| DTE Energy |

| 2.63 |

| Public Service Enterprise Group |

| 3.23 |

| Eversource Energy |

| 2.53 |

| The AES Corporation |

| 1.22 |

| Entergy Corporation |

| 2.39 |

Admittedly, Evergy does not appear to be especially cheap compared to some of its peers, although it is not the most expensive company on the list. However, it does compare reasonably well when we consider that the company’s finances are a bit stronger than some of the other companies on this list. As such, it may be worth considering, especially considering that its lower level of leverage than the companies with a more attractive price-to-earnings growth ratio makes it less risky going forward.

Conclusion

In conclusion, Evergy is an electric utility serving the Great Plains region that may be worth considering as the United States teeters on the verge of a recession. The company’s finances are remarkably stable over time, and it boasts a more attractive balance sheet than many of its peers. There is, admittedly, a certain amount of risk with respect to the company’s debt, but it is in a better financial position than many of its peers. The high dividend yield is a bonus as that provides a respectable investment return while we wait for conditions in the economy to improve.

For further details see:

Evergy: A Solid Choice As Recession Seems Imminent