EVRI - Everi: Acquisitions Loading And Clearly Cheap Digital Entertainment Play

2023-10-28 02:58:32 ET

Summary

- Everi Holdings is undervalued despite recent acquisitions in the digital entertainment industry.

- The company operates in two segments: financial solutions within video games and management, design, and marketing of video games.

- Everi has potential for net sales growth through developments in the video lottery terminal market and the horse racing market.

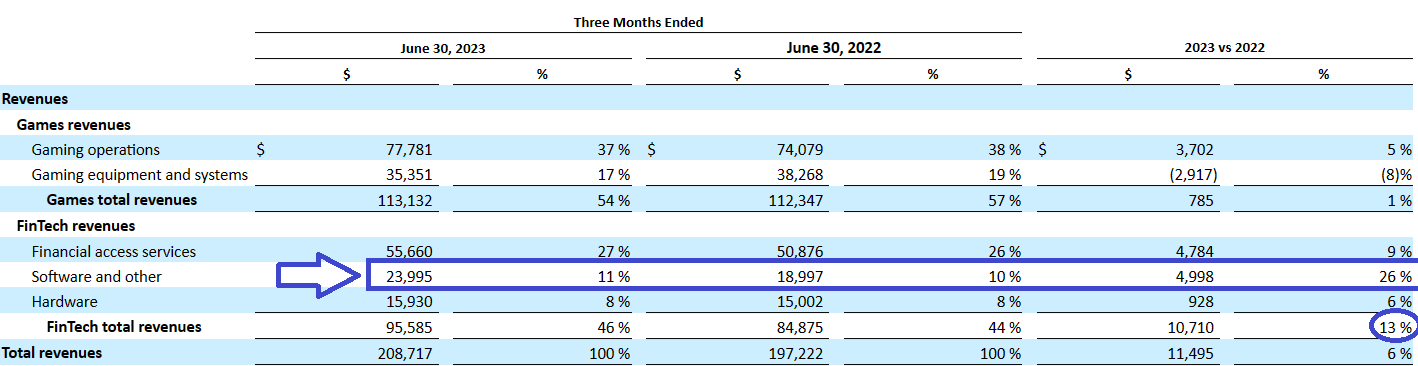

Everi Holdings ( EVRI ) appears to be trading quite undervalued even after executing a list of acquisitions in growing target markets in the digital entertainment industry. In my view, sufficient new development in the video lottery terminal market and the horse racing market could bring substantial net sales growth. Taking into account the FinTech quarterly revenue growth reported worth close to 13% y/y in the last quarter, I can imagine that many traders will most likely be looking at the new numbers to be released in November. In any case, considering the recent declines in the stock and conservative FCFs forecasting, Everi Holdings does look undervalued.

Everi Holdings

Everi is a company that develops and offers video game products, and actively participates in the digital entertainment industry internationally. In addition to developing its own entertainment offering, the company offers management services for casinos, and has an exclusive segment for financial solutions within the field of video games. This includes, along with gaming machines, b2b solutions within the named platforms.

{kind=link}

The operations of the company are divided into two segments. One segment corresponds to financial solutions within video games called Fintech, and the other segment corresponds to the management, design, and marketing activity of video games developed under its own platform as well as related services, under the Games name. The latter groups together the aforementioned operations, machine installation, machine management, and related activities, while the fintech segment is licensed by the company, and offers payment solutions within video games, the transaction of digital money, debit/credit card application, and all types of capital movement that are carried out within the platform.

Everi’s current operations include the registration of customers in more than 3,000 casinos located in the United States and Canada, Australia, Europe, and some areas of Asia. Sales in all cases are made through the company's own channel both nationally and internationally. It is good to note that of the 20% growth mentioned above for the Fintech segment, 17% came from the organic growth of the company's business, while the other 5% in this case was received from the acquisitions made by the company.

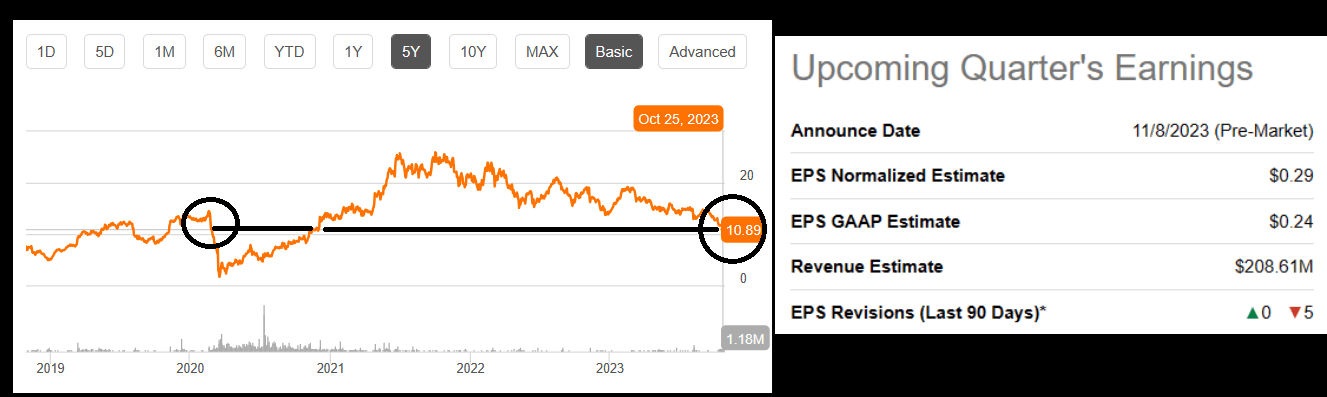

With that, I believe that it is a great time for reviewing Everi, considering the incoming quarterly earnings that will be released in November. Analysts out there are expecting to see EPS GAAP of close to $0.24 per share and quarterly revenue of about $208 million. Additionally, I wondered whether the current valuation of around $10-$11 per share really represents the true value of the stock. It is trading at levels seen in 2020 and 2021. In this regard, I ran a DCF model to understand the valuation of Everi.

{kind=link}

The Balance Sheet Includes A Lot Of Goodwill Derived From A Large Number Of Acquisitions

As of June 30, 2023, the company reported cash of about $210 million, settlement receivables worth $83 million, and trade and other receivables of about $117 million. With prepaid expenses and other current assets worth $43 million, the current ratio appears to be over 1x, so I think that Everi does not report liquidity issues.

With property and equipment worth $133 million, the largest asset is goodwill, which is worth $740 million. Total assets are equal to $1.712 billion. The company appears to be very active in the M&A markets. Recent acquisitions are ecash Holdings Pty Limited, Intuicode Gaming Corporation, Venuetize, and VKGS LLC.

The Company completed acquisitions for an aggregate purchase consideration of approximately $76.7 million during the year ended December 31, 2022. This resulted in the Company recording a significant amount of identified intangible assets and goodwill for the acquisitions of ecash Holdings Pty Limited, Intuicode Gaming Corporation, and Venuetize, Inc. Source: 10-k

On May 1, 2023, the Company acquired certain strategic assets of VKGS LLC, a privately owned leading provider of integrated electronic bingo gaming tablets, video gaming content, instant win games and systems. Under the terms of the purchase agreement, we paid the seller approximately $61.0 million. Source: 10-Q

Source: 10-Q Source: 10-Q

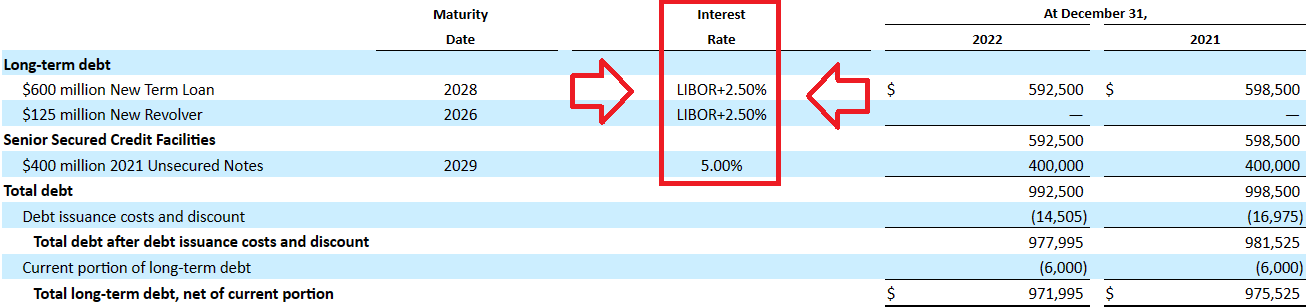

Everi uses debt to pay for acquisitions. With the current portion of long-term debt of about $3 million, long-term debt stands at about $970 million, with total liabilities close to $1.469 billion.

Source: 10-Q

The list of debt obligations includes $400 million 2021 Unsecured Notes with an interest rate of 5%. The company also noted long term debt with an interest rate of about LIBOR+2.5%. I did take into account these figures for the assessment of the cost of capital and the execution of my DCF model.

{kind=link}

Revenue Growth From Acquisitions Will Most Likely Continue To Bring Net Sales Growth In The Coming Years

The company recently launched products such as a new gaming cabin that provides new functionalities to the user community or the expansion of payment methods within digital casino platforms. Additionally, the company will most likely see revenue growth thanks to bingo related solutions, the acquisition of VKGS LLC, and revenue from the HHR business. Further acquisition of gaming companies and new products may bring further net sales growth.

I also took into account the recent FinTech revenue increase of about 13% y/y in my future assumptions. In my view, higher software sales and support related services attributable to loyalty, kiosk, and compliance solutions will most likely bring further business growth in the coming years. Besides, results from acquired businesses will most likely continue to have an impact on future software revenues.

{kind=link}

Entering New Markets Or Strengthening Its Position Could Also Bring Significant Business Growth: The Video Lottery Terminal Market, And The Horse Racing Market

Everi has completed acquisitions that serve both segments of the business model, such as Intuicode which promises a potential insertion into the traditional horse racing market. Given the expected growth of the horse racing market, I believe that future net sales growth may see some traction in the coming years.

Horse Racing Market size is valued at USD 396.21 Billion in the year 2022 and it is expected to reach USD 812.48 Billion in 2030, at a CAGR of 8.93% from 2024 to 2030. Source: Global Horse Racing Market Size, Exploring Share, Trends, and Growth Prospects from 2023-2030

Another of Everi's short-term objectives is to further develop products in the video lottery terminal market, which is expected to grow at close to 7.31% CAGR from 2022 to 2028. The following lines were obtained from an expert in market assessment.

The global video gaming terminals market size was valued at USD 4845.89 million in 2022 and is expected to reach USD 7399.71 million by 2028, at CAGR 7.31%. Source: Video Gaming Terminals Market

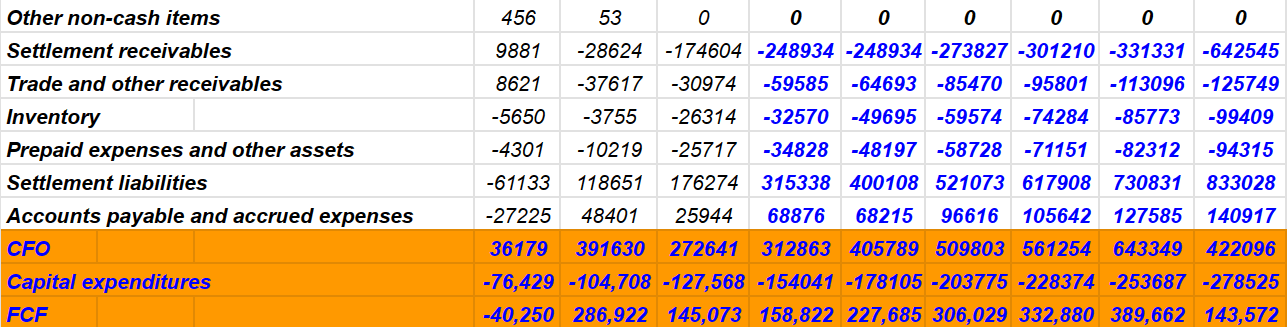

Cash Flow Statement Model

My cash flow model includes 2028 net income close to $87 million, depreciation of about $69 million, 2028 amortization of about $20 million, and non-cash lease expense worth $5 million. I believe that my figures are quite conservative, much more than those offered by other analysts out there.

According to S&P, most analysts are expecting net income growth, net sales growth, and positive free cash flow in 2023, 2024, and 2025. In particular, 2025 net sales are expected to be close to $897 million, with 2025 EBITDA of about $413 million, 2025 net income of close to $117 million, EPS of $1.35 per share, and free cash flow close to $101 million.

Source: Market Screener

I also assumed 2028 amortization of financing costs and discounts worth -$2 million, with loss on sale or disposal of assets worth -$1 million, accretion of contract rights of about $14 million, and provision for credit losses worth $17 million. My numbers are pretty much in line with the figures reported in previous cash flow statements reported in 2021 and 2022.

I did not take into consideration reserves for inventory obsolescence, write-down of assets, or other non-cash items because I believe they are not part of the regular business model of Everi. I also took into account inventory worth -$100 million, prepaid expenses and other assets of about -$95 million, and 2028 accounts payable and accrued expenses worth $140 million.

Source: My Cash Flow Statement Expectations

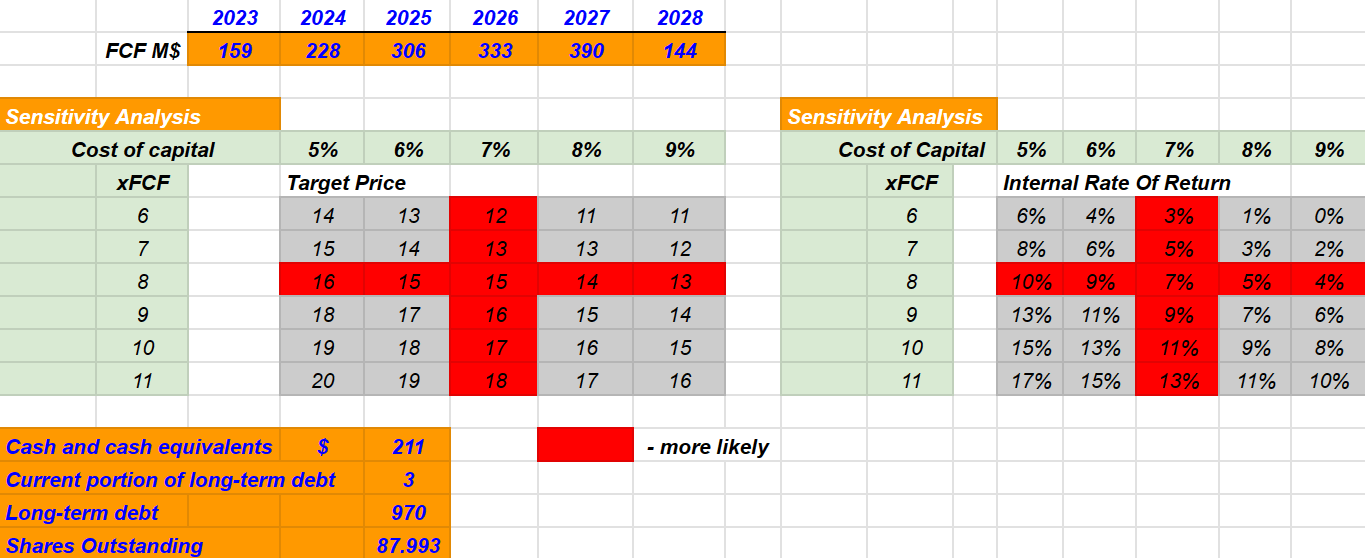

My results for the year 2028 would include CFO of about $422 million, capital expenditures close to -$279 million, and 2028 FCF of $143 million. Note that my FCF results are really not far from the figures obtained in the past.

Source: Ycharts

{kind=link}

If we also take into account cost of capital of about 5%-9% and an enterprise value/FCF multiple between 6x and 11x, the implied target price would be close to $20-$11 per share. Besides, the internal rate of return would be close to 17%-1% with a median IRR of 7%.

{kind=link}

Let's note that the company appears overall undervalued as compared to other peers in the sector. In particular, the Price/Cash Flow multiple stands, according to SA, at close to 3x, and the sector median is equal to 7x. The EV/EBITDA in the sector is close to 8x. In any case, I believe that my terminal EV/FCF multiple at around 6x-11x is not far from the reality seen in the sector.

Source: SA

Competitors, And Business Risks

Competition is intense and highly consolidated for both segments. On the one hand, the Fintech segment competes with a large number of other companies that offer the same service, and some of them have created alliances to capture larger portions of the market. In some cases, they have greater resources than Everi. In the case of this segment, the industry participants are not so numerous. On the other hand, with regard to the traditional gaming industry, competition is more varied and broader, and also changes depending on the region of activity, in addition to being crossed by other forms of entertainment and consumer services related to stays and services of tourism activities.

Among the risks that we find highlighted in the company’s reports, we must mention that the majority of commercial relationships with their clients are based on short-term contracts, and the inability to retain these customers or order contracts will generate complications in the company's operating margins. Likewise, within the risk section, we find that a large number of the machines enabled for gaming under the ownership of Everi are located in tribal territories that respond to particular legislation, and any alteration in this sense could minimize the margin of presence of this type of activities.

It must also be considered that the digital payments segment is highly conditioned by a series of legal regulations, and any change or alteration in the payment method can directly affect the activity of this segment.

Conclusion

In the most recent quarter, Everi Holdings reported FinTech revenue increase of about 13% q/q. I cannot really say whether the company will repeat the same quarterly net sales growth in the incoming quarterly release, however I firmly believe that traders out there are not really paying attention to the recent financial figures and current valuation. In my view, sufficient new developments in the growing video lottery terminal market and the horse racing market, new acquisitions, and correct integration of targets could bring significant net sales growth. Yes, there are risks out there coming from short-term contracts, competition, or the total amount of debt, however the price could be higher.

For further details see:

Everi: Acquisitions Loading, And Clearly Cheap Digital Entertainment Play