NENTY - Evermore Global Value Fund Q1 2023 Portfolio Commentary

2023-06-14 02:51:00 ET

Summary

- Evermore is a New Jersey based investment adviser, providing "special situations" investing across three geographies; Global, European and International.

- The Fund was up 8.27% vs. 6.87% for the MSCI All Country ex U.S. Index.

- EVGIX’s performance in the first quarter outperformed its benchmark indices and peer group.

Dear Shareholder,

With rising interest rates and global fears of recession, investors were bracing for a tough start to the year. Then, the banking sector started to crack and fall apart. In quick succession, three large banks in the U.S. failed. In Europe, Credit Suisse ( CS ), once a stalwart and a European powerhouse, teetered and then, on the cusp of failure, was forced by the Swiss Government into the arms of former rival UBS ( UBS ) with substantial support from the government. We have historically avoided investing in banks, especially in Europe, where the accounting can often be opaque.

As we have seen over and over, crisis creates opportunity. It always has, and it always will. Given how banking is the heartbeat of any well-functioning economy, we expect that the banking issues in the U.S. and Europe will have ramifications for other sectors. The opportunities may not be the banks themselves but other types of businesses. We will know more over time but stand ready to take advantage of these special situations. We saw this play out after the financial crisis of 2008/09. Back then, we were finding incredible investment cases across the financials sector in both equities and the fixed income side.

The first quarter of 2023 was extremely robust for the Evermore Global Value Fund and for the firm as a whole. The Fund was up 8.27% vs. 6.87% for the MSCI All Country ex U.S. Index.

Portfolio Review - Investment Performance

Institutional Class shares of the Evermore Global Value Fund ("[[EVGIX]]" or the "Fund") were up 8.27% for the quarter that ended March 31, 2023. As shown in the chart below, the Fund's performance in the first quarter outperformed its benchmark indices and peer group.

The performance data quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data current to the most recent month end may be obtained by calling 866-EVERMORE (866383-7667). The Fund imposes a 2% redemption fee on shares redeemed within 90 days. Performance data quoted does not reflect the redemption fee. If reflected, total returns would be reduced. Please click here for standardized performance of the Evermore Global Value Fund.

Quarter Ending March 31, 2023

Morningstar Global Stock Category Average represents the average of all funds in the Morningstar Global Stock Category.

Portfolio Review - Characteristics

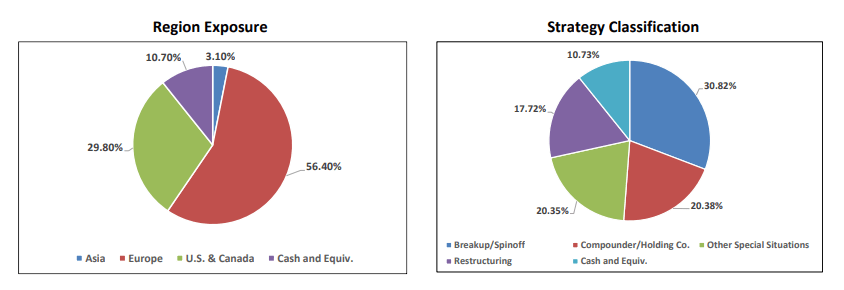

The Fund ended the quarter with $109.0 million in net assets and 23 issuer positions. As of quarter end, 46.6% of the Fund's net assets were in micro- and small-capitalization (up to $2 billion) companies; 17.2% were in mid-capitalization (between $2 billion and $10 billion) companies; and 25.5% were in large- capitalization (> $10 billion) companies. Set forth below please find the following geographic and strategy classification breakdowns (shown as a % of Fund net assets) as of the quarter end.

{kind=link}

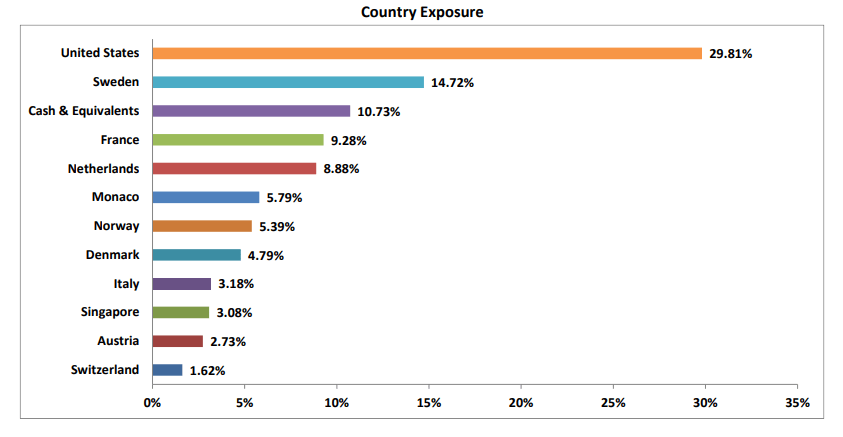

Country Exposure

{kind=link}

Over the last few years, you may have heard or read about how we have refocused the portfolio with a greater emphasis on family-controlled companies ("FCC"). Excluding the impact of cash, hedges, options, and warrants, our investments in FCCs have grown from about 42% of the portfolio in March 2020 (onset of the pandemic) to approximately 72% of the portfolio at the end of the first quarter.

Portfolio Review - New Investments

The Fund ended the quarter with two new positions - DHT Holdings, Inc. (( DHT ) US; Marshall Islands) and Stainless Tankers ASA (STST NO; Norway). Below please find a summary of our investment in DHT Holdings.

Starting this past January, we initiated our investment in DHT Holdings, Inc. (DHT US) , a $1.7 billion market cap, crude tanker operator primarily focused on the larger sized tanker vessels called Very Large Crude Carriers ("VLCC"). Founded in 2005, DHT is one of the leading global crude tanker operators with a fleet of 23 VLCCs which has a total carrying capacity of 7.2 million DWT.

We have been closely monitoring DHT since the Fund's first in-depth foray into the shipping sector in late 2015 / early 2016. Over the years, we have observed DHT's various milestones including Frontline's all-share offer for DHT in 2016 (the Fund previously owned Frontline). DHT ultimately rejected Frontline's offer and instead DHT acquired 11 VLCCs from BW Group in 2017. As part of the transaction, BW Group became a significant holder with a 33.5% stake at that time and BW Group continues to own almost 16% of DHT today. BW Group is the family-controlled holding company for the Sohmen-Pao family, which is a well-regarded operator and savvy investor in the maritime industry. It should be noted that the BW Group is also an anchor shareholder in another Fund investment, Cadeler, the offshore wind installation vessel operator.

The impetus for the Fund to get involved in DHT was the increasing demands for the U.S. to replace Russian barrels that were banned as a consequence of the Ukraine conflict. Favorably shifting trade flows and longer distances have already positioned VLCCs to become the biggest player in the US-to-Europe route in the first quarter of 2023. U.S. exports to Europe have reached the highest level in the last three years with VLCCs taking the lion share of the business from the smaller aframax vessels. In addition, the VLCC orderbook is effectively de minimis with only 11 ships left to deliver in 2023. With no new ordering of VLCCs taking place, this bodes well for a favorably skewed supply/demand setup for VLCC operators, which are the true workhorse for the crude oil trade transporting approximately 50% of seaborne crude. At the time of our investment, DHT was trading at 0.70x Price/NAV, an unwarranted discount to its comparable peers that were, on average, trading closer to NAV. Given the strong balance sheet and liquidity, management's track record and fleet composition of VLCCs (high leverage effect, i.e. "coiled spring"), we believe DHT is extremely well positioned in the current landscape.

Portfolio Review - Exited Investments

The Fund exited the following two positions during the first quarter:

- Atlantic Sapphire (ASA NO) ( AASZF ) : The Fund exited its long-term holding in Atlantic Sapphire ("Sapphire) at a loss. Sapphire, the Norwegian land-based salmon farmer with operations in Homestead, Florida was the biggest detractor from Fund performance in 2022 and, unfortunately, the drawdown continued in the first quarter. As we discussed in last year's commentaries, the Fund participated in the $125 million capital raise at the end of June last year for the company's buildout of Phase 2. Since the equity placement, the company reported good monthly performance reports last July and August. However, Sapphire experienced an operational setback in September and October which resulted in forced early harvesting due to an unexpected higher mortality event in some of the tank systems. The company has implemented the necessary improvements including light enhancements (to improve appetite), food reformulation, and modified biofilters to mitigate future mortality events. As expected, the share price reacted negatively to this event reflecting concerns about restricted access to Sapphire's debt facility that would impede the Phase 2 buildout.

During the first quarter, we heavily debated our position in Sapphire and ultimately decided to exit the investment. We were concerned about a potential equity raise if the company did not have access to the Phase 2 debt facility due to slippage in management's Q2 2023 target for steady-state production or the occurrence of another unintended, exogenous mortality event. While we believe management will eventually get to operational stability, we believe the growing level of skepticism from investors may cause the stock to go lower from here, especially with each subsequent incident. We will continue to watch closely from the sidelines. We believe Sapphire still has the ability to be a game-changer in the industry, but perhaps as part of a larger protein producer.

- Aker Horizons (AKH NO) ( AKHOF ) : The Fund exited its position in Aker Horizon in the quarter at a loss. Please refer to the Portfolio Review - Top Contributors & Detractors section below.

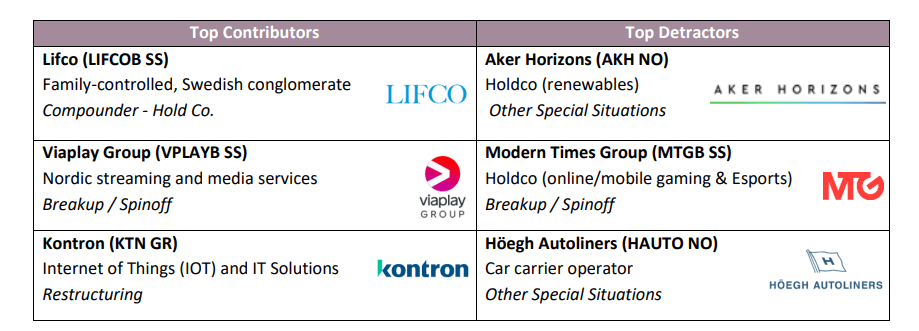

Portfolio Review - Top Contributors & Detractors

The top three contributors to and detractors from Fund performance in the first quarter and summaries for two of the most impactful contributors and detractors can be found below.

{kind=link}

Lifco AB (LIFCOB SS) ( LFABF ) ( LFCBY ) is a $9.7 billion market cap, Sweden-based, family-controlled holding company involved in market-leading niche segments including dental, demolition & tools, and systems solutions. Value creator and billionaire Swedish investor, Carl Bennet, is the chairman and the largest shareholder controlling 50% of the capital and 69% of voting rights. As a reminder, we have been shareholders since the IPO in November 2014. The share price has appreciated almost 12 times over the IPO price (SEK 18.60 adjusted for a 5-for-1 stock split effective May 2021).

Lifco was the largest contributor to Fund performance with the share price appreciating just over 28% in the first quarter. The company's two core segments, dental and demolition & tools, have realized strong organic growth in their respective markets which was further bolstered by price increases that were successfully pushed through to customers. The two core segments, in aggregate, account for 55% of total revenues and represent 55% of EBITDA contribution. In addition, Lifco completed eight acquisitions during the first quarter, of which two companies in dental, two companies in demolition & tools, and four companies in systems solutions. Accretive acquisitions made through the lens of management's disciplined approach continue to be a cornerstone of Lifco's DNA. Despite the modest pace of acquisitions year to date, Lifco continues to have a strong balance sheet with current leverage levels at 1.2x net debt to EBITDA, which is below the low end of their guidance range (2-3x net debt/EBITDA).

The systems solutions segment has always been characterized as the "catch-all" bucket for businesses that were outside the two core segments. In order to increase transparency, the company has reorganized the reporting divisions within the system solutions segment as follows: (1) service and distribution has been further divided into transportation products and special products divisions, (2) the construction materials division has been renamed to infrastructure products to clarify the future direction, and (3) the remaining assets within the forest division has been allocated to special products. While we ascribe a low probability to a potential breakup of Lifco's disparate segments, we believe the improved visibility within systems solutions could be a precursor to the disposal of non-core assets over time.

We had the pleasure of meeting with Carl Bennet and Dan Frohm (Board member and son-in-law) when they were in New York a few months ago. Based on our discussions with management and assessment of the underlying fundamentals of Lifco's businesses, we continue to have high conviction in our position in Lifco even at the current share price. Lifco has been an incredible compounder for the Fund.

Formerly known as Nordic Entertainment Group, Viaplay (VPLAYB SS) ( NENTF ) ( NENTY ) is a $2.0 billion market cap, Nordic broadcasting and media company comprised of free TV, Pay TV, distribution platforms (satellite, IPTV, cable networks, streaming) and a leading content portfolio. It was spun out from the former parent, Modern Times Group, in April 2019. Viaplay was the second largest contributor to performance in the first quarter, where the share price appreciated 33% during the period.

Viaplay embarked on a strategic expansion plan in 2021 to become the preeminent European streaming champion. Specifically, the company had announced it would expand its Viaplay streaming service to 10 new markets over the next three years. To date, Viaplay has successfully expanded as scheduled into the Baltics, Iceland, the Netherlands, and the U.S. (via Comcast (CMCSA) partnership). To put this into perspective, Viaplay had 3 million Viaplay subscribers at the end of 2020 before the start of the expansion initiative. In 2021, Viaplay added about 1 million subscribers, surpassing the milestone of 4 million subscribers. For 2022, total subscribers grew to over 7.3 million, (vs. 6.5 million target), of which the Nordic markets added 1.2 million subscribers to 4.6 million and the international markets added 2.1 million and reached 2.7 million total subscribers. Viaplay has a target of reaching 9 million subscribers (5 million from the Nordic market and 4 million from the international market) in 2023, which is currently on track through the first quarter. Viaplay has an aggressive goal to reach 12 million Viaplay subscribers by the end of 2025, which we believe is achievable based on the current track record.

The last two years (2021 and 2022) have been characterized as subscriber growth mode, whereas 2023 can be viewed through a similar growth lens but with the added focus on increasing average revenue per user (ARPU) across all markets. To that end, Viaplay has started to methodically implement its planned price increases across various regions. In 2022, Viaplay premiered 126 scripted and non-scripted Viaplay originals and expects to target more than 130 originals for 2023 given the overall popularity of Viaplay's content.

Modern Times Group AB (MTGB SS) ("MTG") underperformed during the first quarter with the share price declining 15.5% in the period. MTG is a $970 million market cap, Sweden-based online and mobile gaming company. The share price performance in the first quarter has clearly been frustrating for us, especially on the back of MTG's strong continued underlying growth from the acquisitions of PlaySimple (global leader in mobile word and casual games) and Ninja Kiwi (tower defense strategy games). PlaySimple continued its strong performance in the first quarter, resulting in the Word Games franchise accounting for the largest contributor to overall revenues over the last five quarters. MTG also realized impressive growth and strong interest in the new titles - Crossword Explorer and Word Search during the first quarter. Ninja Kiwi's flagship title, Boons TD6, continued to perform well and is on track to launch the game on Netflix later in the year.

Within Innogames, MTG's strategy and simulation segment, there was an inflection during the latter half of the first quarter. It appears that Innogames' softer performance from the prior quarter, which was driven by ongoing challenges from Apple's IDFA changes and post-pandemic normalization, has largely subsided with early signs of improvement. Innogames continued to deliver meaningful updates and additional content to its marquee title, Forge of Empires, which was well received as underscored by the strong reception from in-game events held in February and March. In April, Innogames announced plans to further realign the studio and accelerate new game development.

We believe investors generally have a greater level of uncertainty towards the overall gaming and mobile gaming sectors. Many have simply bought into the perspectives outlined by industry analytics providers, like Newzoo, that believe the overall gaming market will be down by upwards of 10% next year and hindered by a slower recovery. In the first quarter, MTG provided 2023 guidance of -3% to +2% for full-year revenues and adjusted EBITDA margin to range from 23-25% which we believe is achievable given the steady operational focus, a strong pipeline of new games, and transformative acquisitions consummated during a challenging market landscape. As we recently discussed with the CEO, Maria Redin, when she was visiting us in our office this past March, we believe MTG is a potential acquisition target with an ever-growing bullseye. To be clear, our view that MTG could be a potential takeout target is one of the scenarios that formed our initial investment thesis, but certainly not the central part of our assessment. With the transformative acquisitions (and integration) now in the rearview mirror and coupled with a strong balance sheet sitting on SEK 4 billion of net cash at the end of the first quarter (proceeds from divesting ESL Gaming to Savvy Gaming Group in April 2022), we believe MTG continues to be extremely well positioned with significant firepower for future acquisitions.

The Fund's position in Aker Horizons ASA (AKH NO) was the second largest detractor in the first quarter. Aker Horizons is a $615 million market cap, holding vehicle that was created as the dedicated platform for renewable and green-related investments for the Aker Group, a listed, family-controlled holding company (ticker: AKER NO) for the Røkke family. The company was founded in 2020 and listed on the Euronext Growth Oslo in February 2021. The Aker Group has stated its goal to invest in excess of NOK 100 billion (over $9.5 billion) in renewable investments by 2025, largely through Aker Horizons.

At the time of our initial investment, Aker Horizons had already cast numerous irons in the fire with diverse exposure to various green initiatives. The portfolio consisted of both listed and unlisted companies: (1) Mainstream Renewable Power (privately held): offshore and onshore wind and solar power plants with 1.4 GW net capacity in operation with a pipeline of development projects of ~10 GW, of which 5 GW is slated to become operational within three years; it is also the largest developer of renewable energy in Chile and the second largest producer in South Africa, (2) Aker Carbon Capture (listed, 51% stake): carbon capture, utilization, and storage technology, (3) Aker Offshore Wind (listed, 51% stake, subsequently taken private by Aker): pure-play offshore wind projects with a focus on deepwater, and (4) Aker Clean Hydrogen (listed, subsequently taken private by Aker Horizons): producer of clean hydrogen. Putting it all together, we believe the portfolio of market-leading renewable assets is worth significantly more than the prevailing share price.

Even though we recognize the impressive backlog amassed across the various green initiatives, Aker Horizons' early mover advantage, and the overall necessity of the structural shift towards renewables in the long term, we have ultimately decided to exit this investment at this juncture. In a rising interest rate environment and global fears of inflation, we underappreciated the reality that longer-duration assets (like renewables) will be subject to greater volatility and swift investor capitulation irrespective of the value proposition of the underlying assets. Without further belaboring the point, we were simply too early in this investment in a sector that is still in its formative years. We will continue to track this name and closely monitor the renewables sector.

Closing Thoughts

As the first quarter of 2023 ended, so did the first chapter in the life of the Evermore Global Value Fund. As noted in previous announcements and our recent proxy, there have been a number of significant events for the firm and our clients.

From January 2010 through March 2023, the Fund was managed by Evermore Global Advisors, LLC, a registered investment adviser founded by David Marcus and Eric LeGoff. David and Eric both worked for many years for renowned value investor Michael F. Price at Heine Securities Corp., the investment adviser to the Mutual Series family of mutual funds. As of April 1, 2023, Evermore Global Advisors was no longer an investment adviser to the Fund. Going forward, F/m Investments, LLC, a registered investment adviser that as of December 31, 2022, had over $1.4 billion in assets under management, is the investment adviser to the Fund and MFP Investors is the sub-adviser to the Fund.

The Evermore Global Value Fund will continue to be managed by Thomas O as co-portfolio manager and with me as the lead portfolio manager. The Price Family Office is a newly formed entity that provides personal services for the heirs and family members of the late Michael Price, of which I am the CEO. In my role as CEO, I also have oversight responsibility and serve on the Advisory Board of MFP Investors LLC, a limited partnership primarily owned by the Price family.

Our Head of Operations from Evermore, Beijing He, is now Director, Operations for MFP Investors, managing all operations for the combined asset management group.

It was a strong team effort to effect this transition. With our access to all the resources of MFP Investors, expanded investment team, legal, operations, etc., and the cross dialog and investment debate we have developed with their portfolio managers and investment team, I believe we are off to a strong start.

Just as we are embarking on the next chapter for the Fund and ourselves, our Vice President, Business Development, Adam Ermanis, will also be forging ahead on his next chapter. Adam has been a key contributor, partner, sounding board, and most importantly, friend, to the firm and to me personally. We wish him incredible success as he moves forward.

Please feel free to contact me (dmarcus@mfpllc.com) or Thomas O (to@mfpllc.com) with any questions.

Sincerely,

David E. Marcus

Portfolio Manager

Opinions expressed are those of MFP Investors LLC and are subject to change, are not guaranteed, and should not be considered investment advice.

Fund holdings and sector allocations are subject to change at any time and should not be considered recommendations to buy or sell any security. Current and future portfolio holdings are subject to risk.

S&P 500 is a stock market index that tracks the stocks of 500 large-cap U.S. companies.

The MSCI ACWI ex USA Index captures large and mid-cap representation across 22 Developed Markets countries.

The HFRX Event Driven index utilizes a UCITSIII-compliant methodology to construct the HFRX Hedge Fund Indices. The methodology is based on defined and predetermined rules and objective criteria to select and rebalance components to maximize the representation of the Hedge fund Universe.

EV/EBITDA -Enterprise Value/Earning Before Interest, Taxes, Depreciation, and Amortization is the most widely used valuation multiple based on enterprise value and is often used in conjunction with, or as an alternative to the price-to-earnings ratio to determine the fair market value of a company.

Free cash flow represents the cash a company generates after cash outflows to support operations and maintains its capital assets.

EBIT means earnings before interest and taxes and is an indicator of a company's profitability.

Please click here for the most recent holdings of the Evermore Global Value Fund.

Mutual fund investing involves risk. Principal loss is possible. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. This risk is greater for investments in Emerging Markets. Investing in smaller companies involves additional risks such as limited liquidity and greater volatility than larger companies. The Fund may make short sales of securities, which involve the risk that losses may exceed the original amount invested in the securities. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment in lower-rated, non-rated and distressed securities presents a greater risk of loss to principal and interest than higher-rated securities. Due to the focused portfolio, the fund may have more volatility and more risk than a fund that invests in a greater number of securities. Additional special risks relevant to the fund involve liquidity, currency, derivatives and hedging. Please refer to the prospectus for further details.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before investing. This and other important information is contained in the Fund's statutory and summary prospectus, which may be obtained by contacting your financial advisor, by calling MFP Investors at 866-EVERMORE (866383-7667) or on www.evermoreglobal.com . Please read the prospectus carefully before investing.

You cannot invest directly in an index.

MFP Investors LLC is the sub-advisor to the Evermore Global Value Fund, which is distributed by Quasar Distributors, LLC.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Evermore Global Value Fund Q1 2023 Portfolio Commentary