EVER - EverQuote Approaches Operating Breakeven As It Diversifies

2023-06-02 13:45:45 ET

Summary

- EverQuote reported its Q1 2023 financial results on May 8, 2023.

- The firm operates an online insurance shopping service and related lead generation services for insurance carriers and agents in the U.S.

- EVER is diversifying from its focus on the volatile auto insurance sector, approaching operating breakeven and a low current valuation.

- For patient investors, my outlook on EVER is a Buy at around $9.60 per share.

A Quick Take On EverQuote

EverQuote ( EVER ) reported its Q1 2023 financial results on May 8, 2023, beating both revenue and EPS consensus estimates.

The firm provides online insurance shopping in the United States for consumers and lead generation for insurance carriers and agents.

Given management's focus on diversifying into more stable markets, a meaningful move toward operating breakeven, and a low current valuation multiple, for investors with a patient time frame, my outlook on EVER is a Buy at around $9.60 per share.

EverQuote Overview

Cambridge, MA-based EverQuote was founded in 2008 to make "insurance shopping easy, efficient and personal, and to save consumers and insurance providers time and money."

Management is headed by Chief Executive Officer, Jayme Mendal, who has been with the company since 2017 and was Vice President of Sales at PowerAdvocate.

The firm connects insurance shoppers with insurance providers for the following types of insurance:

-

Auto

-

Home

-

Renters

-

Life

-

Health

According to management, finding the right insurance product can be difficult for consumers due to limited online options, pricing, and a large number of confusing coverage options.

EverQuote provides a platform for cost-effective insurance shopping in the U.S.

EverQuote's Market & Competition

As EverQuote attracts consumers, the company also collects more data which improves personalization, conversion rates, and consumer satisfaction. More providers help attract more consumers, which also assists with data collection.

The company advertises through hundreds of online channels including internet search, email, social media, and display advertising.

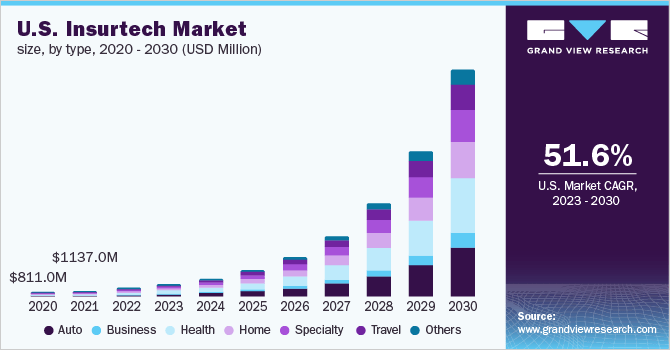

According to a 2023 market research report by Grand View Research, the global Insurtech market was an estimated $5.45 billion in 2022 and is forecasted to reach $161 billion by 2030. It is expected to grow at a whopping CAGR of 52.7% during the forecast period from 2023 to 2030.

The main factor driving market growth is the increasing phenomenon of revamping the insurance industry to connect with a wider customer base consisting of High Net Worth individuals (HNWI), upper-middle-income groups, and lower-middle-income groups.

Top banks and insurance companies are expected to enhance their offerings or develop strategic partnerships with financial technology innovators to provide innovative payment solutions to customers.

The U.S. Insurtech market's historical and projected future growth trajectory through 2030 is shown below:

{kind=link}

Major competitive vendors that are developing insurance industry technology include:

-

SelectQuote

-

Insurify

-

The Zebra

-

Policygenius

-

TrueMotion

-

Esurance

-

CoverHound

-

Insure.com

EverQuote's Recent Financial Trends

-

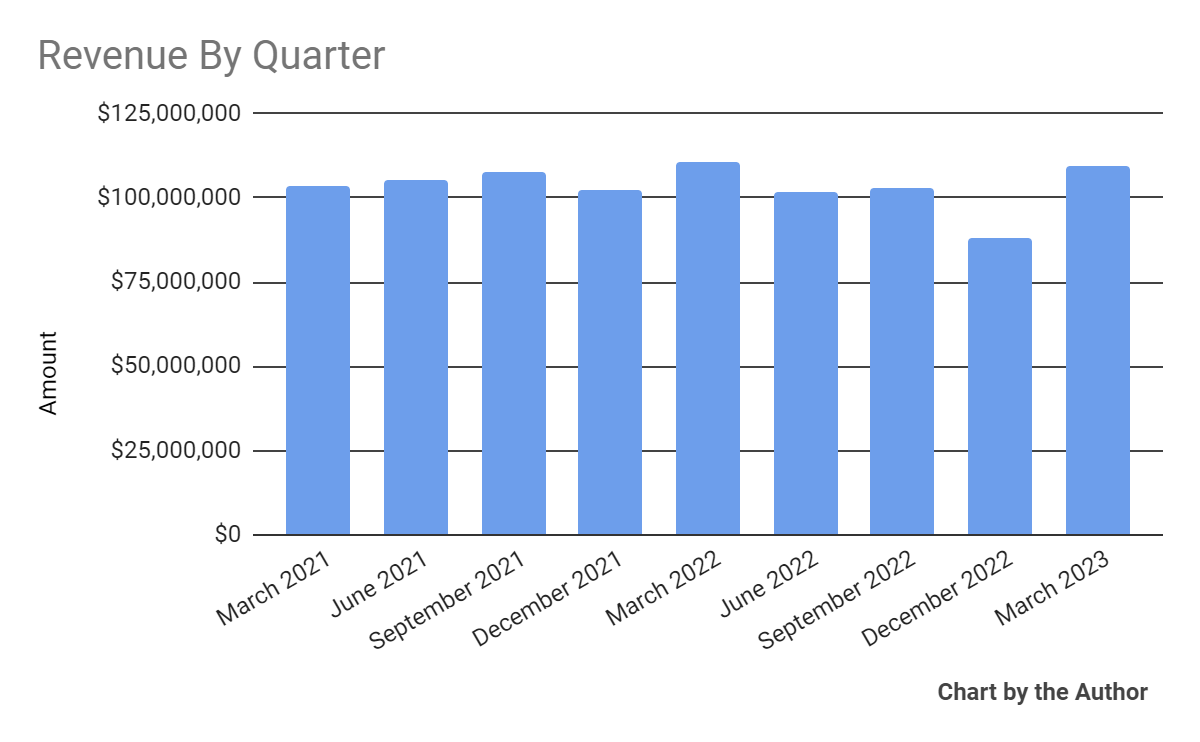

Total revenue by quarter has proceeded unevenly in recent quarters:

{kind=link}

-

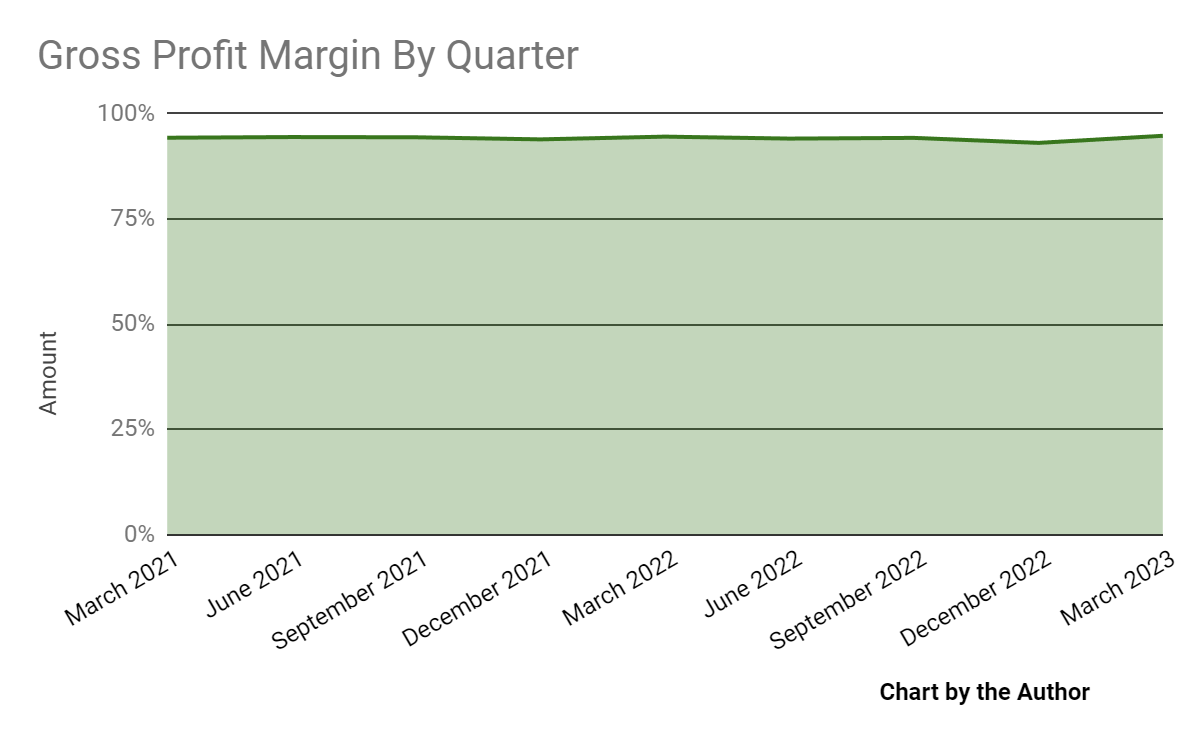

Gross profit margin by quarter has been largely flat:

{kind=link}

-

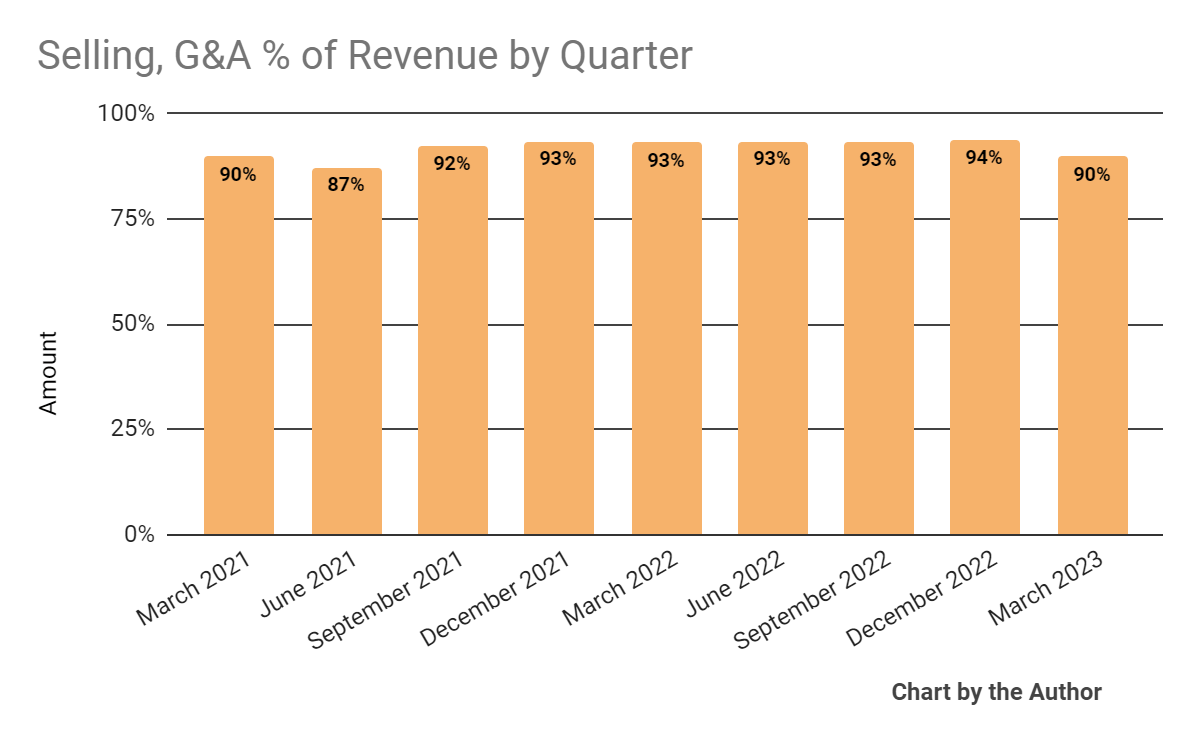

Selling, G&A expenses as a percentage of total revenue by quarter dropped in the most recent quarter, YoY:

{kind=link}

-

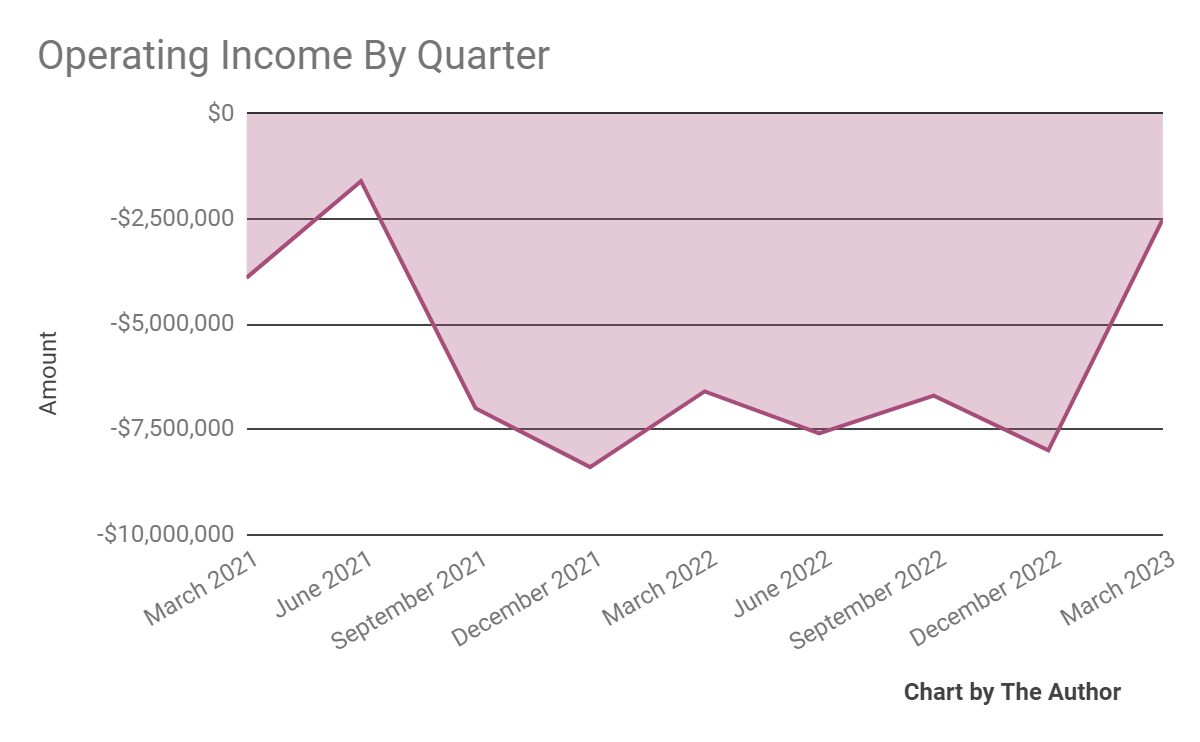

Operating income by quarter has remained negative but has more recently made substantial progress towards breakeven:

{kind=link}

-

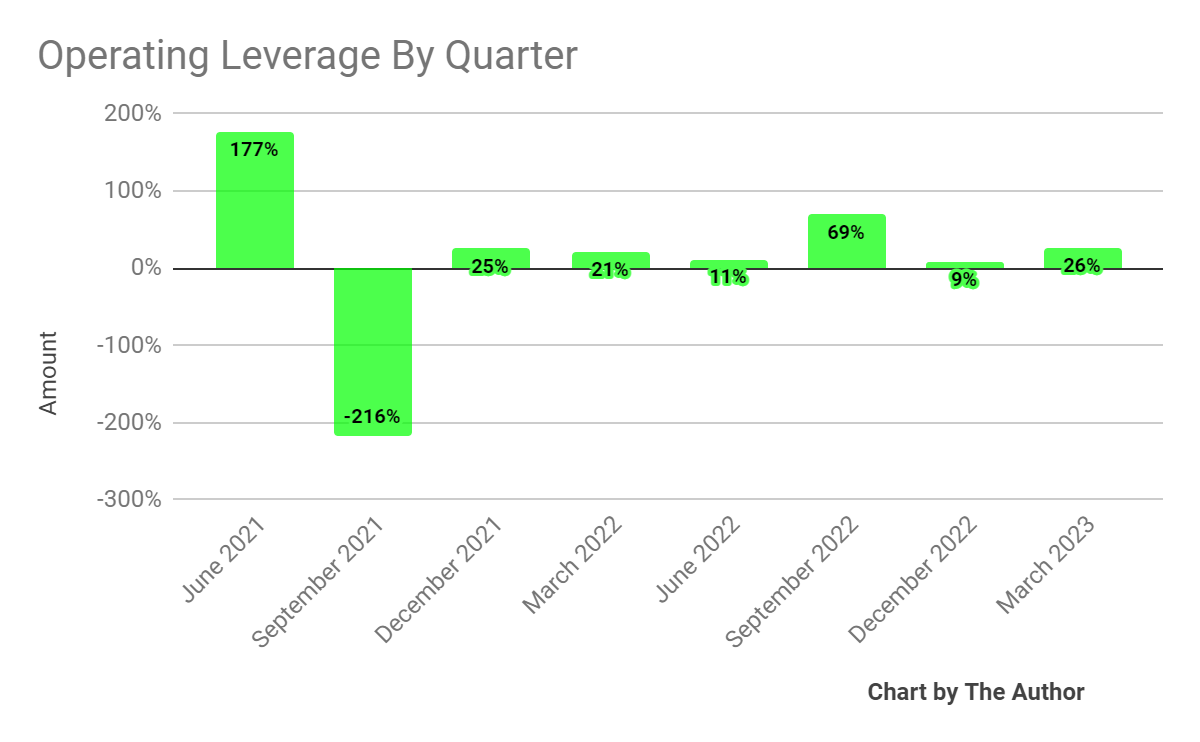

Operating leverage by quarter has generally been positive in recent quarters:

{kind=link}

-

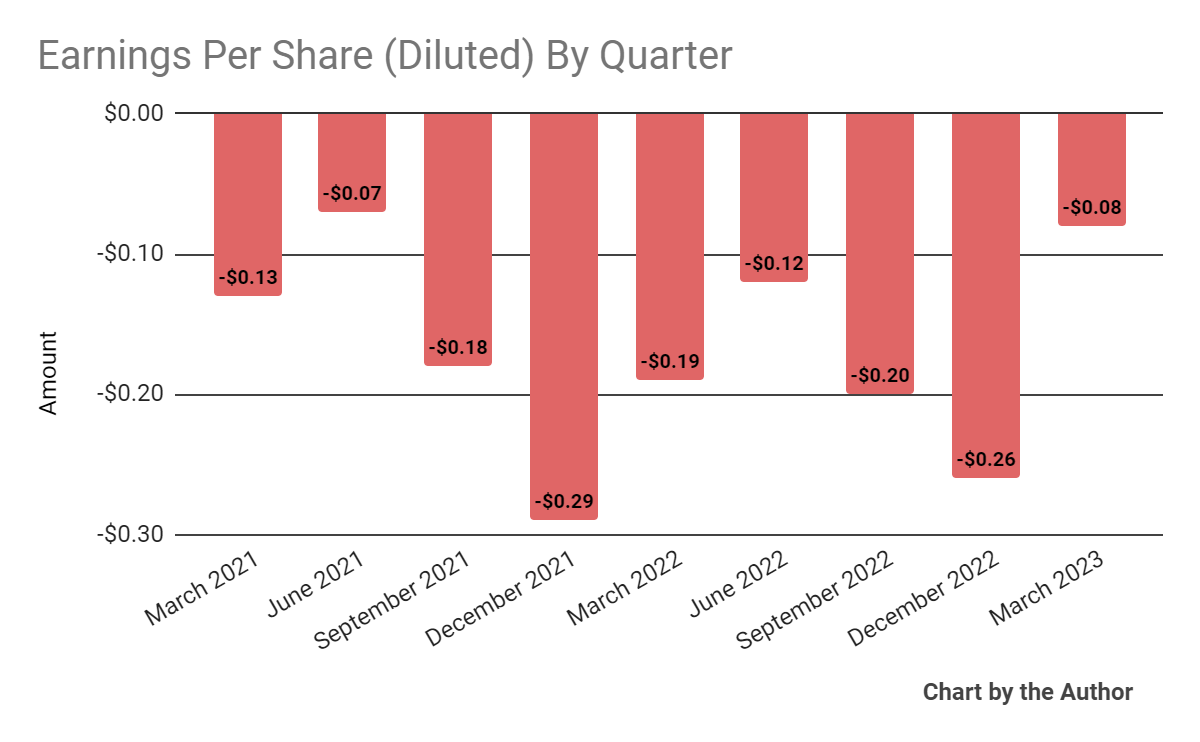

Earnings per share (Diluted) have remained negative but Q1 2023's result was encouraging:

{kind=link}

(All data in the above charts is GAAP)

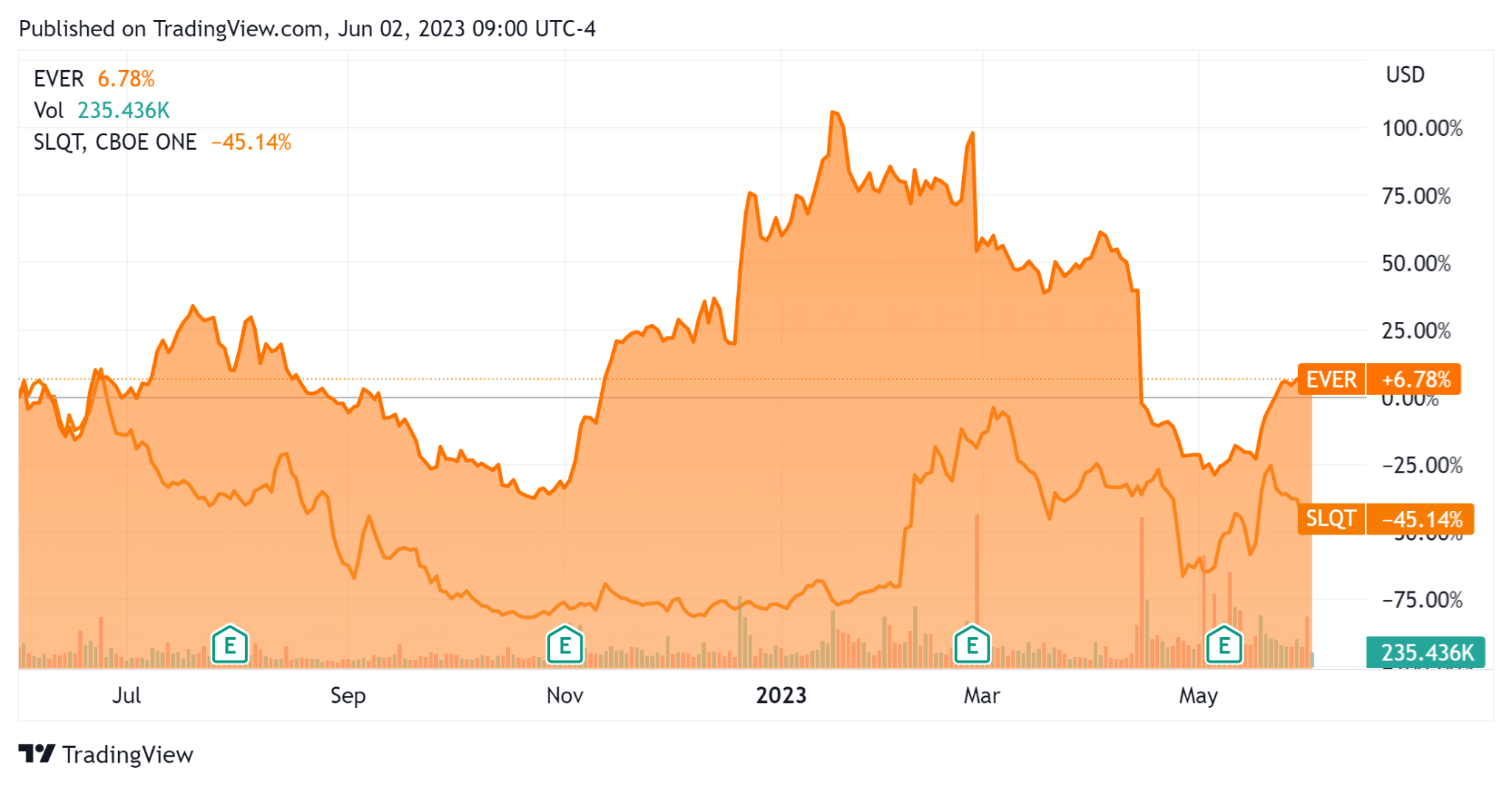

In the past 12 months, EVER's stock price has risen 6.78% vs. that of SelectQuote's ( SLQT ) fall of 45.14%, as the chart indicates below:

{kind=link}

For the balance sheet, the firm ended the quarter with $28.8 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash flow was $8.6 million, of which capital expenditures accounted for $4.6 million. The company paid $28.0 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For EverQuote

Below is a table of relevant capitalization and valuation figures for the company:

| Measure ((TTM)) |

| Amount |

| Enterprise Value/Sales |

| 0.7 |

| Enterprise Value/EBITDA |

| NM |

| Price/Sales |

| 0.7 |

| Revenue Growth Rate |

| -5.3% |

| Net Income Margin |

| -5.3% |

| EBITDA % |

| -5.4% |

| Net Debt To Annual EBITDA |

| 1.3 |

| Market Capitalization |

| $309,930,000 |

| Enterprise Value |

| $286,540,000 |

| Operating Cash Flow |

| -$13,180,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.66 |

(Source - Seeking Alpha)

As a reference, a relevant partial public comparable would be SelectQuote, although SLQT's focus is on Medicare Advantage health insurance; shown below is a comparison of their primary valuation metrics:

| Metric ((TTM)) |

| SelectQuote |

| EverQuote |

| Enterprise Value/Sales |

| 1.0 |

| 0.7 |

| Enterprise Value/EBITDA |

| NM |

| NM |

| Revenue Growth Rate |

| 13.8% |

| -5.3% |

| Net Income Margin |

| -12.5% |

| -5.3% |

| Operating Cash Flow |

| -$66,790,000 |

| -$13,180,000 |

(Source - Seeking Alpha)

Commentary On EverQuote

In its last earnings call (Source - Seeking Alpha), covering Q1 2023's results, management highlighted its 'broad-based' progress despite automobile insurance carrier spending headwinds.

As a result, management has shifted its efforts to home insurance markets 'as carrier budgets and agents demand shifts from auto into homeowners' products.'

Leadership is also focused on expanding its use of AI and machine learning technologies in producing 'greater productivity (internally) and/or enable entirely new products, services or ways of doing things.'

Management didn't disclose any company or customer retention rate metrics.

Total revenue for Q1 2023 fell by 1.4% YoY and gross profit margin increased by 0.2 percentage points.

Selling, G&A expenses as a percentage of revenue decreased by 3.3 percentage points, a positive trend indicating increasing operating efficiency. Operating losses dropped by 62.5% YoY, also a positive sign.

Looking ahead, management withdrew its previous guidance for 2023 and said it will focus on increasing its operational efficiencies and diversifying into 'stable parts of the business.'

The company's financial position is reasonably solid for its size, with nearly $29 million in cash, no debt, and positive free cash flow.

Regarding valuation, the market is valuing EVER at an EV/Sales multiple of around 0.7x.

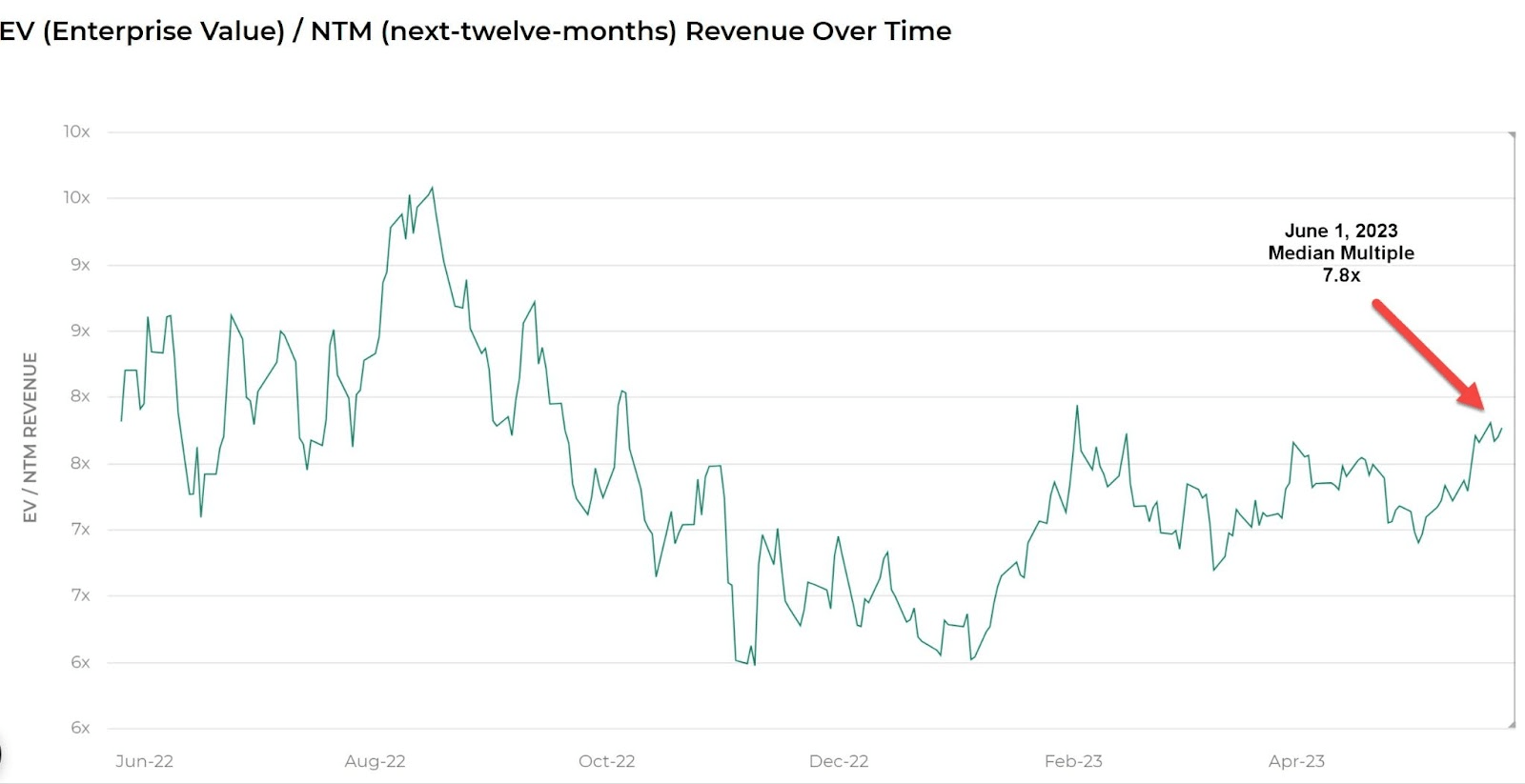

The Meritech Capital Index of publicly held SaaS application software companies showed an average forward EV/Revenue multiple of around 7.8x on June 1, 2023, as the chart shows here:

{kind=link}

So, by comparison, EVER is currently valued by the market at a substantial discount to the broader Meritech Capital SaaS Index, at least as of June 1, 2023.

Risks to the company's outlook include an economic slowdown that may be underway, reduced credit availability which may affect customer/prospect spending plans, and lengthening sales cycles which may reduce its revenue growth potential in the near term.

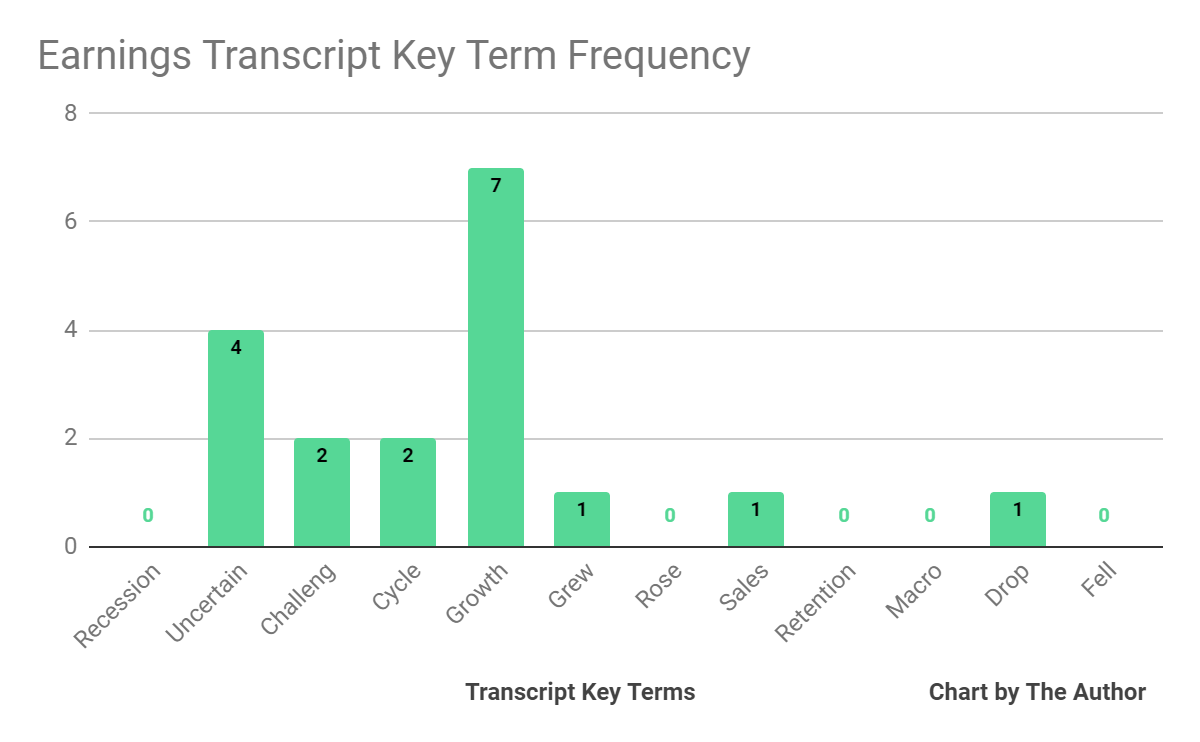

From management's most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

{kind=link}

I'm most interested in the frequency of potentially negative terms, so management or analyst questions cited 'Uncertain' four times, 'Challeng(es)(ing)' two times, and 'Drop' once.

The negative terms refer to a current downturn in the auto insurance sector and the resulting impact of a drop in insurance carrier lead spend.

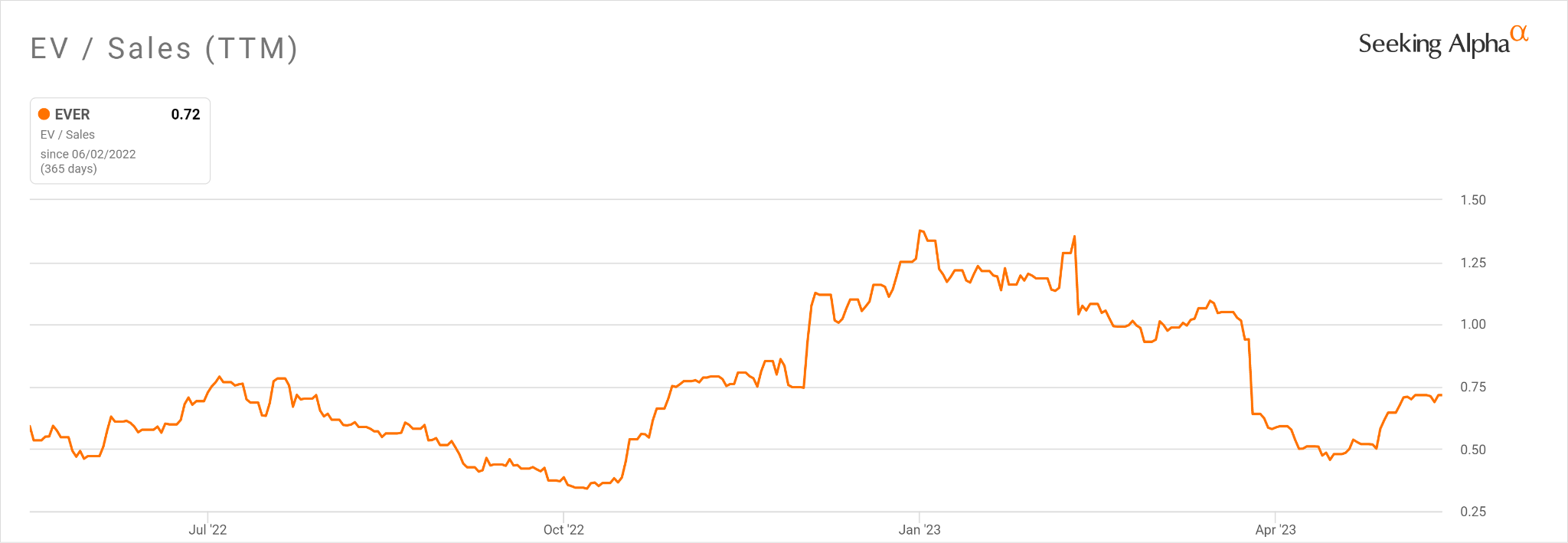

In the past twelve months, the firm's EV/Sales valuation multiple has risen by 22%, as the chart from Seeking Alpha shows below:

{kind=link}

A potential upside catalyst to the stock could include a continued increase in its variable marketing margin from its recent record high of 32.6% in Q1.

This margin success has likely been a factor in driving the stock higher over the past twelve months, despite an auto industry insurance carrier slowdown.

However, the stock has been highly volatile over the past year, so it isn't for the faint-hearted.

Given management's focus on diversifying into more stable markets, a meaningful move toward operating breakeven, and a low current valuation multiple, for investors with a patient time frame, my outlook on EVER is a Buy at around $9.60 per share.

For further details see:

EverQuote Approaches Operating Breakeven As It Diversifies