DTB - Eversource Energy: Debt Concerns Result In A Good Entry Point For This 3.67%-Yielder

2023-03-23 16:24:08 ET

Summary

- Eversource Energy is a major utility serving most of New England.

- The company enjoys remarkably stable cash flows, which can be a real advantage today.

- The company is positioned to deliver a 9% to 11% total average annual return, which is reasonable for a conservative utility.

- The company has a substantial amount of debt maturing this year, which will cause its interest expenses to increase and pressure EPS and OCF.

- The company is trading at a reasonable valuation right now.

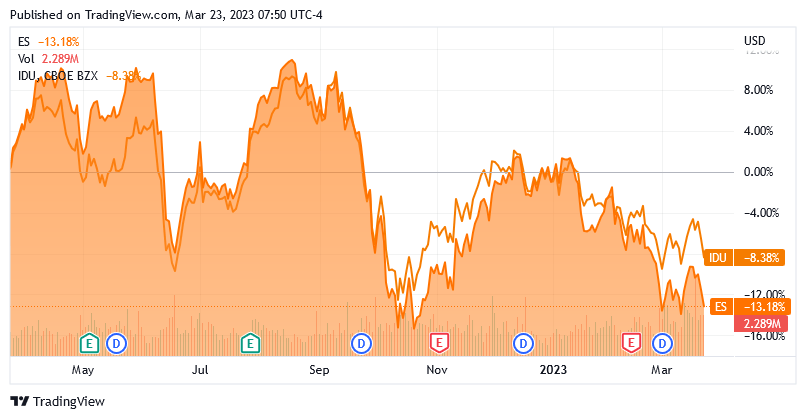

Eversource Energy ( ES ) is a regulated natural gas and electric utility that serves much of the New England region of the United States. While this is a fairly small area in terms of geography, it's one of the most densely populated regions of the United States and, as such, causes Eversource Energy to be one of the largest utilities in the United States. However, size does not really matter since most people buying shares of a utility like Eversource Energy value these companies for their overall stability and high yields. Indeed, Eversource Energy’s 3.67% current yield is substantially higher than most other things in the market right now, although its yield is below that of a money market fund, which is disappointing. Unfortunately, the stock’s performance over the past year has been nothing short of disappointing as Eversource Energy has declined 13.18% over the past year compared to 8.38% for the U.S. utility sector index ( IDU ):

{kind=link}

There was little news that could have caused the company to underperform so severely, although Eversource Energy’s attempt to back away from its offshore wind ambitions likely disappointed investors that favor environmental, social, and governance policies. I discussed this in a previous article on the company. The company also has a significant amount of debt maturing this year, so the rising rate environment could be a concern as that would increase its costs significantly following the rollover. However, the stock is not particularly expensive today so it might still be worth taking a risk on.

About Eversource Energy

As stated in the introduction, Eversource Energy is a regulated natural gas and electric utility that serves much of the New England region of the United States. This includes the states of New Hampshire, Massachusetts, and Connecticut:

Eversource Energy

This is a pretty small service area in terms of geography, particularly when we compare it to some of the utilities operating in the Western states. However, it's a very densely populated area as Eversource Energy serves more than four million customers in total. The company’s size is largely irrelevant in terms of its characteristics, though. The most important of these for investors today is the fact that the company’s cash flows are remarkably stable with time. We can see this quite clearly by looking at the company’s operating cash flow. Here are the figures for each of the past 10 years, including the most recent quarter:

{kind=link}

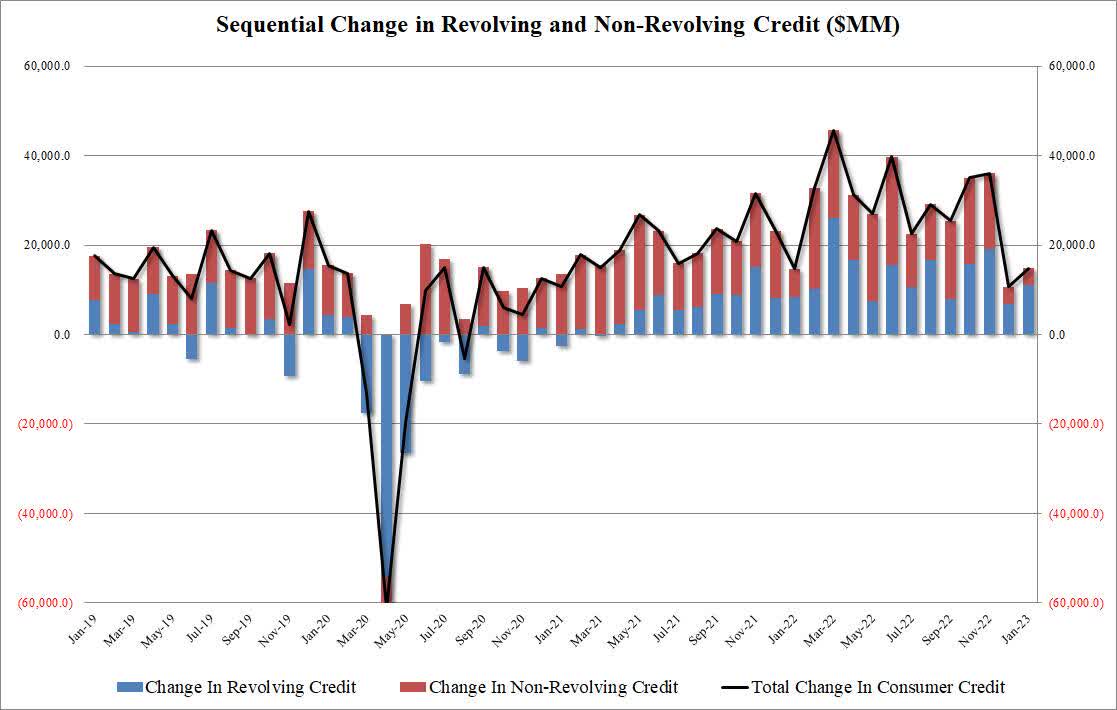

As we can clearly see, Eversource Energy’s cash flow has not varied too much over the past decade, although it has increased over time. The reason for this general stability is the fact that the product that the company provides is considered a necessity by most people. After all, how many people do not have electric service to their homes and businesses? Thus, they will typically prioritize paying their electric bills ahead of making discretionary expenses. That's something that could be important today, since we have started to see money getting tight for many households around the country. This is evident in the fact that credit growth has slipped significantly over the past few months:

{kind=link}

That's in stark contrast to the historical average of total outstanding consumer credit increasing by $20 billion to $30 billion monthly. This shows that households are clearly starting to hurt financially and are slowing down their credit-fueled discretionary spending. This is bad news for any company that's heavily dependent on consumer spending, but it's not likely to hurt Eversource Energy since consumers will continue to pay to keep the lights on in their homes (and there's government assistance available to help those who are having difficulty with this). This is exactly the kind of company that we want to have in our portfolios today.

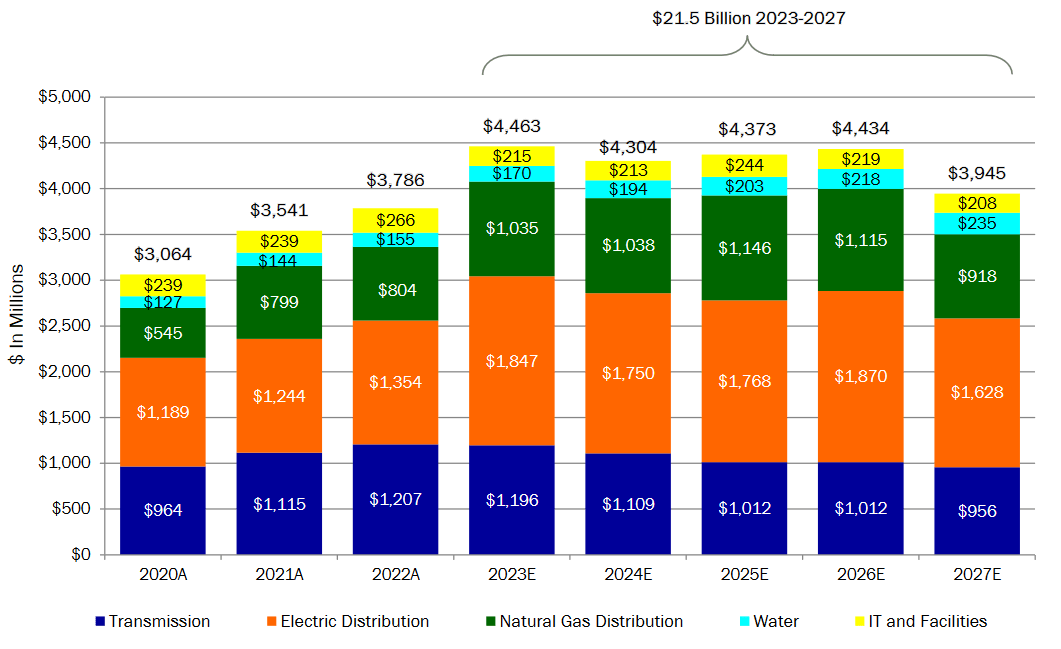

Naturally, as investors, we are unlikely to be satisfied with mere stability. We like to see a company that we're invested in grow and prosper over time. As we can see above from the company’s operating cash flow, Eversource Energy has generally been able to accomplish that over the past decade. Fortunately, the company appears to be positioned to continue that trend. The primary way that it will do this is by growing its rate base. A utility’s rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. Since this rate of return is a percentage, any increase in the rate base allows the company to positively adjust the prices that it charges its customers in order to earn that specified rate of return. The usual way that a utility increases the size of its rate base is by investing capital into upgrading, modernizing, or possibly even expanding its utility-grade infrastructure. Eversource Energy is planning to do exactly that going forward. In its full-year 2022 earnings presentation , the company unveiled an updated capital program that calls for the firm to invest $21.5 billion into its infrastructure over the 2023 to 2027 period:

{kind=link}

This is nice because it provides us with much more visibility into the company’s forward plans than we have been provided with by some of the firm’s peers. Regular readers may recall me complaining about utilities only providing plans going out to 2025 in a few articles that I published over the past week, so it's nice to see that Eversource Energy is doing a better job in that respect. The company’s capital plan as detailed above should be able to grow its rate base at an impressive 7.5% compound annual growth rate over the period, but that does not necessarily mean that its earnings will grow at this rate. This is because the company needs to finance its capital program, which could mean equity issuance that dilutes the shareholders somewhat. However, Eversource Energy’s management is still projecting that earnings per share will grow at a 5% to 7% compound annual growth rate over the period, which seems quite reasonable. This positions the company pretty well to deliver a 9% to 11% total average annual return over the next five years given its current yield, which is a very acceptable return for a conservative utility stock.

Financial Considerations

It's always important that we investigate the way that a company is financing itself before making an investment in it. This is because debt is a riskier way to finance a business than equity because debt must be repaid at maturity. This is usually accomplished by issuing new stock and using the proceeds to repay the maturing debt. That can cause a company’s interest expenses to increase following the rollover, which may be an especially big concern today since interest rates are currently higher than they have been in years. In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company’s cash flow to decline could push it into financial distress if it has too much debt. Although utilities such as Eversource Energy tend to enjoy remarkably stable cash flows, this is still a risk that we should not ignore as bankruptcies have occurred in the sector.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio essentially tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. The ratio also tells us how well a company’s equity can cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of Dec. 31, 2022, Eversource Energy had net debt of $22.6803 billion compared to $15.6287 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.45 today. Here's how that compares to some of the company’s peers:

| Company |

| Net Debt-to-Equity |

| Eversource Energy |

| 1.45 |

| DTE Energy ( DTE ) |

| 1.85 |

| Entergy Corporation ( ETR ) |

| 2.02 |

| FirstEnergy Corporation ( FE ) |

| 2.05 |

| Exelon Corporation ( EXC ) |

| 1.61 |

Overall, we can clearly see here that Eversource Energy appears to have a very strong balance sheet relative to its peers and is less dependent on debt to finance itself. This is nice to see as it's a sign that the company should not really present investors with an outsized risk due to its debt.

With that said, Eversource Energy has a significant amount of debt maturing this year, as stated in the introduction. This is shown clearly here:

Eversource Energy

The biggest risk here comes from the fact that the company is unlikely to be able to obtain similar rates to these today. That's a direct effect of the Federal Reserve’s efforts to combat inflation, which has now driven interest rates to the highest levels that we have seen in more than 10 years. The company has conducted two raises this year, both of which carried substantially higher rates than the ones that the company needed to refinance:

Eversource Energy

For example, take a look at the $500 million issue by Connecticut Light & Power, which was intended to refinance the $400 million offering that matured back in January, as well as give the company a bit of extra money. The interest rate went from 2.50% prior to the refinance to 5.25% after it. Connecticut Light & Power is owned by Eversource Energy, so we can see that the company’s interest expenses have already started to go up because of debt refinancing. That will continue to be the case as the company has $850 million of fixed-rate debt at the parent company level maturing this year (the variable-rate debt that matures in August is not as big of a deal since the company has already been experiencing the effects of interest rate increases there). It will never be able to obtain the 2.80% to 3.80% interest rate that it's currently paying in today’s market. Thus, we can expect to see Eversource Energy’s interest expense increase fairly significantly over the next four quarters, which will be a drag on the company’s operating cash flow and net income. This is likely one reason for the company’s weak stock market performance lately.

Fortunately, Fitch, one of the major rating agencies, does not expect that the company will have difficulty rolling over its debt. The agency stated such back in June when it explained its reasons for a BBB+ rating on Eversource Energy:

“Long-term debt maturities over the next five years are manageable. At the parent level, Eversource has $450 million of 2.8% senior unsecured notes due May 1, 2023; $350 million of floating rate senior unsecured notes due August 15, 2023; $400 million of 3.8% senior unsecured notes due December 1, 2023; $450 million of 2.9% senior unsecured notes due October 1, 2024; $300 million of 3.15% senior unsecured notes due January 15, 2025; $300 million of 0.8% senior unsecured notes due August 15, 2025; $250 million of 3.35% senior unsecured notes due March 15, 2026 and $300 million of 1.4% senior unsecured notes due August 15, 2026.”

That's certainly a great deal of debt due over the next few years and it will cause the company’s interest expenses to increase over time, particularly if the Federal Reserve keeps rates around today’s levels for a while. However, the Federal Reserve removed its previous language about “a sustained period” during its rate announcement yesterday so it's possible that the recent turbulence in the banking sector is causing the central bank to consider pausing monetary tightening or even implementing the pivot that some investors have been hoping for. Thus, it's uncertain exactly what the impact will be on Eversource Energy over the next few years, but it does still seem likely that the company will see its interest expenses increase significantly from the 2023 maturities at the very least.

Dividend Analysis

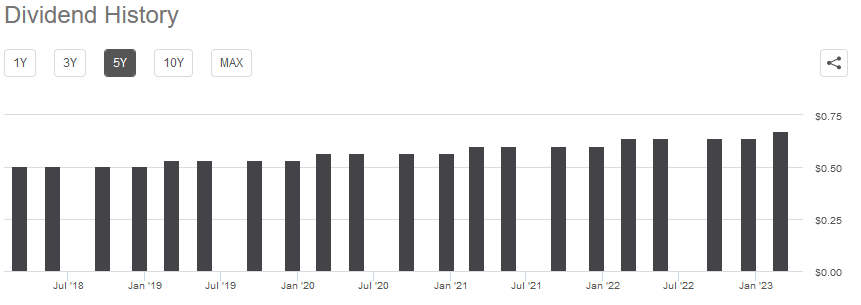

One of the primary reasons why investors purchase shares of utilities like Eversource Energy is that they frequently have higher dividend yields than most other things in the market. Eversource is certainly no exception to this as its 3.67% current yield is substantially higher than the 1.65% yield of the S&P 500 Index ( SPY ). As is the case with many utilities, Eversource Energy also has a long history of annual dividend increases. This is shown here:

{kind=link}

The fact that the company increases its dividend every year is something that we should be able to greatly appreciate as investors. This is especially true during inflationary times like we are experiencing today. The reason for this is that inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This fact makes it seem that we are getting poorer and poorer with the passage of time. The fact that the company increases its dividend each year helps to offset this effect and maintains the purchasing power of the dividend that we receive from the company.

As is always the case though, it's important that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut that reduces our incomes and almost certainly causes the company’s stock price to decline.

The usual way that we evaluate a company’s ability to maintain its dividend is by looking at its free cash flow. A company’s free cash flow is the amount of money that was generated by its ordinary operations and is left over after the company pays all its bills and makes all necessary capital expenditures. This is therefore the money that can be used for such purposes as reducing debt, buying back stock, or paying a dividend. During the 12-month period that ended on Dec. 31, 2022, Eversource Energy had a negative levered free cash flow of $433.7 million. That was obviously not enough to pay any dividends, but the company still paid out $860.0 million in dividends during the year. At first glance, this is quite concerning as the company is not generating enough free cash flow to cover its dividend.

However, it's quite common for a utility to finance its capital expenditures through the issuance of equity and debt, while paying its dividend out of operating cash flow. This is due to the incredibly high costs inherent in constructing and maintaining utility-grade infrastructure over a wide geographic area. These costs are so high that they usually exceed a company’s operating cash flow and would therefore prevent it from ever generating a positive free cash flow. During the full-year 2022 period, Eversource Energy reported an operating cash flow of $2.4013 billion, which was easily enough to cover the $860.0 million dividend that the company paid out with a great deal of money left over for other purposes. Thus, it appears that Eversource Energy can probably afford to sustain the dividend at the current level, so we do not really have too much to worry about here.

Valuation

It's always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a utility like Eversource Energy, we can value it by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company’s forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. However, there are very few stocks that have such low ratios in today’s richly valued market. As such, the best way to use this metric today is to compare Eversource Energy with its peers in order to determine which company offers the most attractive relative valuation.

According to Zacks Investment Research , Eversource Energy will grow its earnings per share at a 6.51% rate over the next three to five years. This is in line with the 5% to 7% growth rate that we used earlier to calculate the company’s projected total return and it's reasonable considering the company’s rate base growth so it seems like a pretty good estimate. This gives the company stock a price-to-earnings growth ratio of 2.59 at the current stock price. Here is how that compares to the company’s peers:

| Company |

| PEG Ratio |

| Eversource Energy |

| 2.59 |

| DTE Energy |

| 2.79 |

| Entergy Corporation |

| 2.50 |

| FirstEnergy Corporation |

| 2.40 |

| Exelon Corporation |

| 2.53 |

As we can see, Eversource Energy is not completely out of line with its peers, but it's also not the cheapest company in this group. Overall, the current price looks fair, although any market reversal would make the company cheaper.

Conclusion

In conclusion, Eversource Energy continues to look like a reasonable investment for a utility investor, although there's going to be some negative pressure on its cash flow over the next several months as the company is forced to roll over a significant amount of debt at much higher rates. Fitch believes that this is a manageable situation though, and considering the fact that utility service is a necessity in the modern world, I cannot see any reason to doubt this prediction. These concerns have driven down the company’s share price though, which has resulted in us having a nice entry point and a 3.67% dividend yield.

For further details see:

Eversource Energy: Debt Concerns Result In A Good Entry Point For This 3.67%-Yielder