OGE - Eversource Energy: Strong Renewable Credentials Make For A Somewhat Pricey Stock

Summary

- Eversource Energy is a large electric utility serving the heavily populated New England region.

- The company is positioned to provide investors with an 8% to 10% total return over the next three years.

- The company is heavily focused on sustainability, which may ultimately begin attracting money from the wealthy mutual funds that focus on this area.

- Eversource Energy has a reasonable debt load and will almost certainly increase its dividend over the next few weeks.

- Eversource stock looks a bit pricey compared to a few of its peers, which could give some credence to the ESG thesis.

Eversource Energy ( ES ) is a major regulated electric and natural gas utility serving customers throughout much of New England. The utility sector has long been among the favorite ones for conservative investors due to its relative stability and very high dividend yields. Eversource Energy is something of an exception to this rule, as its 2.97% current yield is a bit low for a utility company, although it does enjoy stable cash flows.

Fortunately, Eversource Energy has a long history of steadily raising its dividend and producing fairly strong earnings per share growth, so anyone investing today will see a significantly higher yield-on-cost in only a few years. It is not too difficult to justify an investment in Eversource Energy today, either, as the stock is fairly cheap, although not quite as cheap as it was the last time that we discussed this company. Admittedly, our overall thesis has not changed too much since the time of that last article, but the company’s most recent earnings report provides evidence that it is playing out as planned, and Eversource is likely to boost its dividend within the next few months, so there might still be some reasons to purchase the stock today.

About Eversource Energy

As stated in the introduction, Eversource Energy is a fairly large regulated electric and natural gas utility that serves approximately four million customers in the New England states of New Hampshire, Massachusetts, and Connecticut:

Eversource Energy

Despite being one of the more progressive regions in the United States, New England’s primary source of heat for homes and business is crude oil. In fact, the region consumes approximately 85% of all of the heating oil in the United States. As such, we might expect that Eversource Energy serves many more electric customers than natural gas ones. This is certainly correct, as the company has approximately 3.26 million electric customers but only 886,000 natural gas customers. This is something that some investors may find attractive. After all, politicians and activists have been promoting the idea that we will soon abandon fossil fuels for electricity as a source of power for space heating.

As I have pointed out in various previous articles, including my previous one on Eversource Energy, this is highly unlikely to happen. Electric utilities do have one major advantage over natural gas ones in terms of stability, though. Natural gas is mostly consumed in the winter, so nearly all natural gas companies see their cash flows and earnings spike during the fourth and first quarters of the year. Electricity, meanwhile, is consumed all year long so electric utilities tend to enjoy somewhat more consistent earnings from quarter to quarter. We can see this quite clearly by looking at Eversource Energy’s operating cash flows over time. This chart shows the company’s figures over the past eleven quarters:

{kind=link}

We do still see a cash flow increase during the third quarter of each year. This is, while electric consumption does tend to be somewhat steady over the course of the year, there is higher consumption during the third quarter in most areas due to the extensive use of air conditioning. As electric consumption is higher during these months, we can expect to see an electric utility bringing in more money during that time.

The biggest draw of utilities for conservative investors, though, is that they are fairly recession-resistant. This is because electricity and natural gas are generally considered to be a necessity for our modern way of life. After all, who does not have electricity or heating in their homes and businesses? In fact, the government typically provides money for assistance with paying heating bills to people that cannot afford it on their own. As a result of being considered a necessity, most people will prioritize paying their natural gas and electric bills ahead of discretionary expenses during times when money gets tight. This is something that is quite important today, because nearly everybody expects that the economy will enter into a recession in 2023. Many people of limited means have to cut back on their spending during a recession, so it might be a good idea to invest in a company that will be able to weather the conditions effectively.

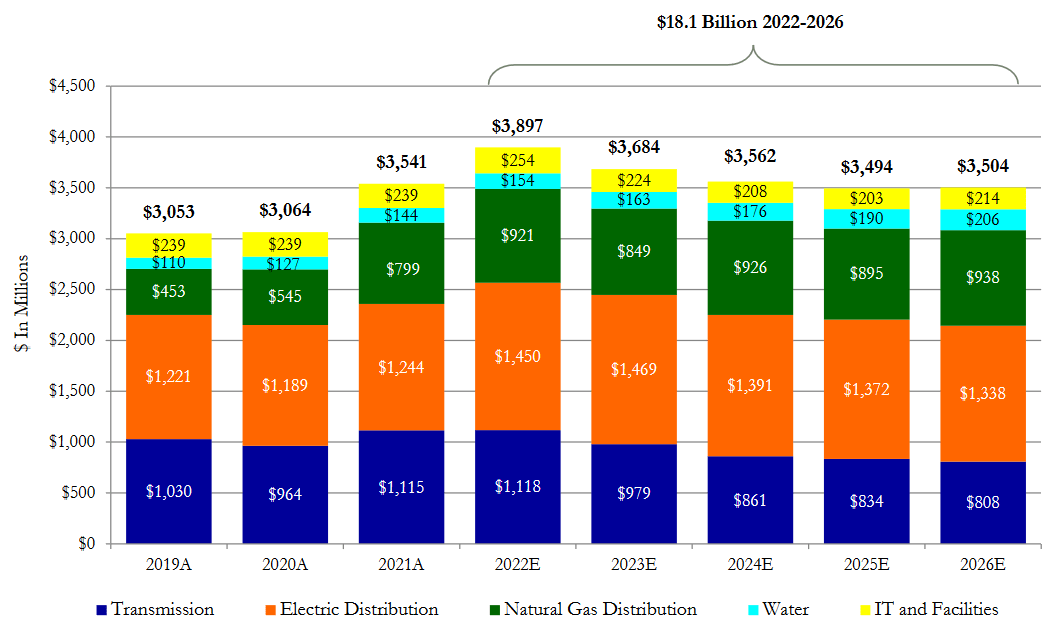

Naturally, as investors, we want to see more than simple stability. We like to see growth, which is especially important with a company like Eversource Energy that increases its dividend annually. Fortunately, Eversource Energy is well-positioned to accomplish this. The primary way through which it will accomplish this is by expanding its rate base. The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base thus allows the company to increase the price that it charges its customers in order to earn that specified rate of return. The usual way through which a company grows its rate base is by spending money to upgrade, modernize, and possibly even expand its utility infrastructure. Eversource Energy is planning to do this as the company has unveiled an $18.1 billion investment plan over the 2022 to 2026 period:

{kind=link}

I will admit that I would like to see a bit longer of an outlook than this considering that we are now in the second week of 2023 but Eversource Energy has not publicly released one. The company has stated that it will present this information during its year-end conference call, which will likely be in early February. Still, it appears that the company is planning to spend $14.203 billion under this capital spending plan over the 2023 to 2026 period. This is the best information that we have until it releases its estimates for 2027. We can anticipate that its spending in 2027 will likely be around $3.5 billion, just as it is during every other year in the projection period. One reason for this is that the company has to spend that much simply to overcome the impact that depreciation will have on its asset base if it intends to continue to generate growth. This growth program as provided should allow the company to grow its earnings per share at a 5% to 7% rate, which works out to a total estimated return of 8% to 10% when we consider the dividend. This is quite reasonable for a conservative dividend stock, although it is not quite as high as some of the company’s peers possess.

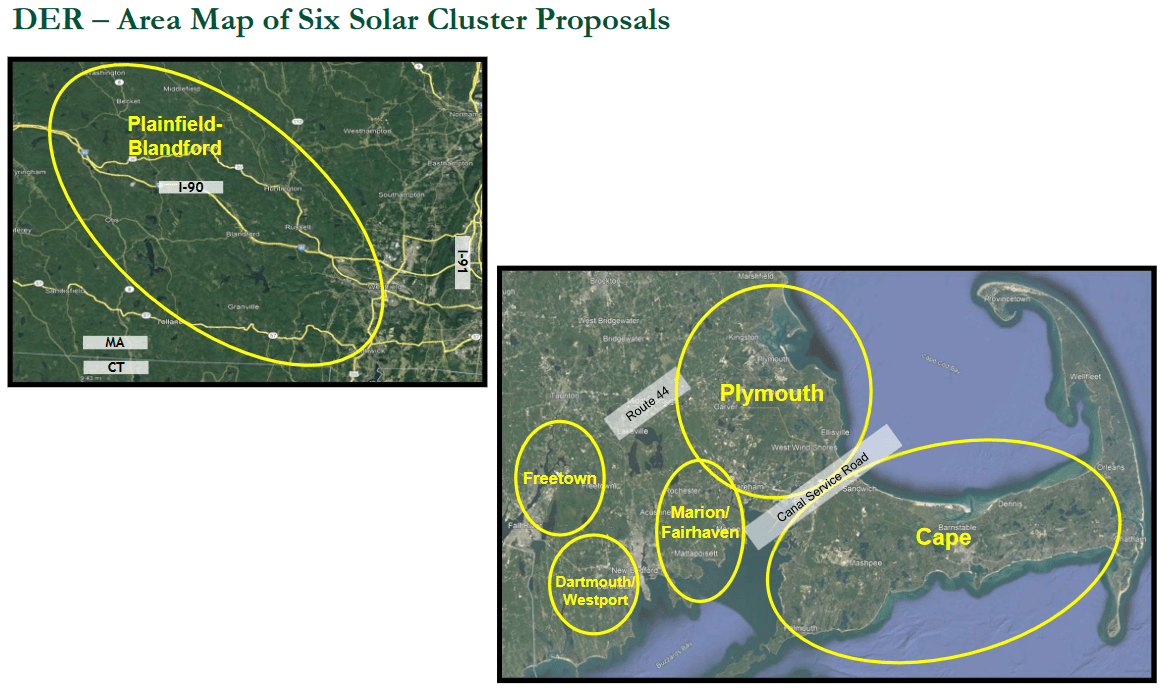

One area in which Eversource Energy is planning to invest heavily is renewable generation capacity. This is hardly surprising considering that the company is based in New England, which is one of the most progressive areas of the country. Massachusetts, for example, unveiled a program back in 2020 intended to incentivize the deployment of both rooftop solar and utility-scale solar generation facilities. It will be rather interesting to see if this program works due to the fact that Massachusetts only receives a fairly limited amount of sunlight, but the state is committed to it. Eversource Energy has proposed a series of facilities with a total output capacity of 1 gigawatt intended to be deployed around the state over the next four to five years as part of this initiative. The projects will be deployed around the Cape and Plainfield areas:

{kind=link}

The company has revealed little about these projects beyond their total capacity and total estimated cost of $902 million. Frankly, the company would be better off with its offshore wind projects given the climate and geography of this area but it is committed to achieving the solar goals that were dictated by the Massachusetts Department of Energy Resources. I suppose that makes sense for a utility, although it seems unlikely that these projects will really have a significant impact on the company’s financial performance.

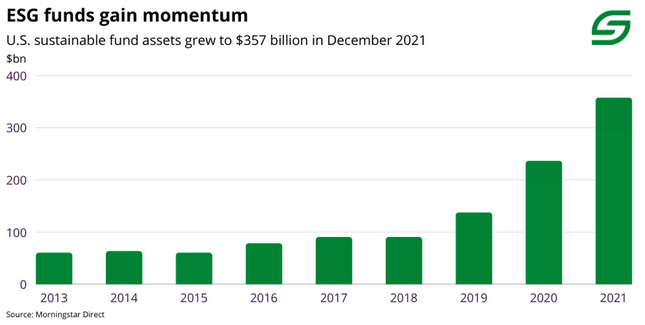

The company might derive another benefit from its intense focus on renewable energy capacity, however. As I pointed out in a previous article , American environmental, social, and governance funds held $357 billion as of December 2021. This represents a substantial increase over previous years:

{kind=link}

Unfortunately, a figure for December 2022 has yet to be released. However, Bloomberg has previously estimated that environmental, social, and governance funds will contain about one-third of all investable assets by 2025. While the market volatility of 2022 may have tempered that expectation, nobody can deny that the various funds that have sprung up around this theme have an incredible amount of assets. This is important because one of the things that these funds invest in is renewable energy and those companies that promote “green energy conversion.” This would include Eversource Energy given its solar projects in Massachusetts and its offshore wind projects, whose fate the company has not determined yet. The size of these funds is sufficient to drive up the company’s stock price should they begin purchasing its shares or to put a floor under the stock price should the shares begin to decline in a market correction. Thus, investors may have an opportunity to front-run the funds by purchasing shares of Eversource Energy today before its renewable ambitions become more widely known.

Financial Considerations

It is always important to have a look at the way that a company is financing its operations before making an investment in its shares. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt to repay the maturing debt, which can result in a company’s interest expenses increasing depending on the conditions in the market at the time that it performs the rollover. In addition to this, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. Although electric utilities like Eversource Energy tend to have remarkably stable cash flows, as we saw earlier, bankruptcies have occurred in the sector so this is still a risk that we should not ignore.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company’s equity can repay its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of September 30, 2022, Eversource Energy had a net debt of $21.8119 billion compared to shareholders’ equity of $15.4347 billion. This gives the company a net debt-to-equity ratio of 1.41, which is in line with the ratio that the company had following the second quarter. Here is how that compares to the firm’s peers:

| Company |

| Net Debt-to-Equity Ratio |

| Eversource Energy |

| 1.41 |

| DTE Energy ( DTE ) |

| 2.22 |

| Entergy Corporation ( ETR ) |

| 2.14 |

| NextEra Energy ( NEE ) |

| 1.33 |

| OGE Energy ( OGE ) |

| 0.92 |

With the notable exception of OGE Energy, we can clearly see here that Eversource Energy is generally in line with or better positioned than its peers. This is a very good sign and serves as a clear indication that Eversource Energy is not relying too heavily on debt in order to finance its operations. Thus, there should be no real need to worry about the company’s debt level as it does not represent an outsized risk.

Dividend Analysis

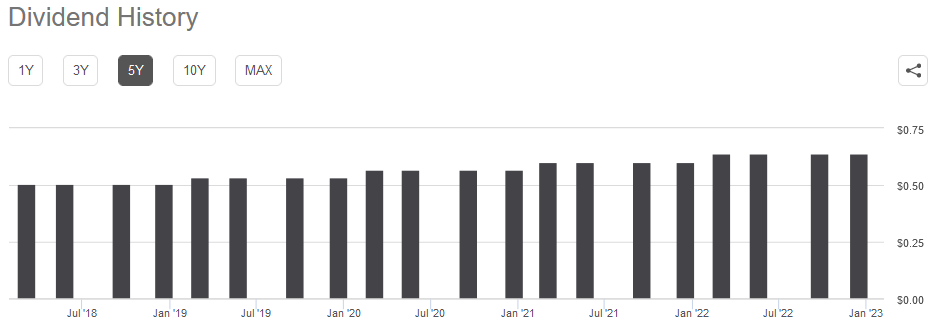

As stated in the introduction, utility companies tend to have fairly high dividend yields. This is one reason why these utilities are often attractive to conservative investors such as retirees. Unfortunately, Eversource Energy disappoints a bit here as its 2.97% yield is a bit low for the sector. However, it is still much higher than the 1.63% yield of the S&P 500 Index (SP500). Eversource Energy does have a long history of raising its dividend annually, as we can see here:

{kind=link}

The fact that the company steadily increases its dividend annually means that anyone purchasing the stock today will have a significantly higher yield-on-cost in a few years. In addition, the fact that the company is steadily increasing its dividend is something that is quite nice to see during inflationary periods such as the one that we are in today. This is because inflation is constantly reducing the number of things that can be purchased with the dividend that the company pays out. Thus, an investor may feel as if they are steadily getting poorer and poorer over time. The annual increase in the dividend helps to overcome this effect and maintains the purchasing power of the dividend. As is always the case, though, we want to make sure that the company can actually afford the dividend that it pays out. After all, we do not want it to have to reverse course and cut the payout since that would reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we evaluate a company’s ability to finance its dividend is by looking at its free cash flow. A company’s free cash flow is the amount of cash that was generated by its ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the amount that is available to do things that benefit the shareholders such as reducing debt, buying back stock, or paying a dividend. During the third quarter of 2022, Eversource Energy reported a levered free cash flow of $264.8 million but only paid out $215.7 million in dividends. Thus, the company did manage to cover its dividend out of free cash flow, which is nice to see.

It is fairly rare for a utility to be able to accomplish this, though, as they usually have a negative free cash flow due to the high cost of constructing and maintaining utility-grade infrastructure over a wide geographic area. Indeed, Eversource Energy does usually have a negative free cash flow, as we can see here:

| Q3 2022 |

| Q2 2022 |

| Q1 2022 |

| Q4 2022 |

| Levered Free Cash Flow |

| $264.8 |

| -$231.0 |

| -$129.1 |

| -$199.6 |

(All data in millions of U.S. dollars.)

Thus, the usual practice is for the company to finance its capital expenditures through the issuance of debt and equity, then pay the dividend out of its operating cash flow. During the third quarter of 2022, Eversource Energy reported an operating cash flow of $847.1 million, which was more than sufficient to cover its $215.7 million dividend and leave the company with a great deal of money left over that it can use for other purposes. Overall, the dividend appears to be very safe here. Investors should not have to worry much about a dividend cut in the near future.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like Eversource Energy, we can value it by looking at the price-to-earnings growth ratio. This ratio is a modified version of the familiar price-to-earnings ratio that takes a company’s earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share and vice versa. However, there are very few stocks that have such a low ratio in today’s richly valued market. Thus, it makes the most sense to compare the company’s price-to-earnings growth ratio to that of its peers in order to determine which stock offers the most attractive relative valuation.

According to Zacks Investment Research , Eversource Energy will grow its earnings per share at a 6.51% rate over the next three to five years. That is relatively in line with the 5% to 7% figure that we projected earlier based on the company’s rate base growth so the Zacks estimate seems pretty solid. This gives Eversource Energy a price-to-earnings growth ratio of 3.01 at the current share price. Here is how that compares to the company’s peers:

| Company |

| PEG Ratio |

| Eversource Energy |

| 3.01 |

| DTE Energy |

| 3.18 |

| Entergy Corporation |

| 2.66 |

| NextEra Energy |

| 2.77 |

| OGE Energy |

| 3.79 |

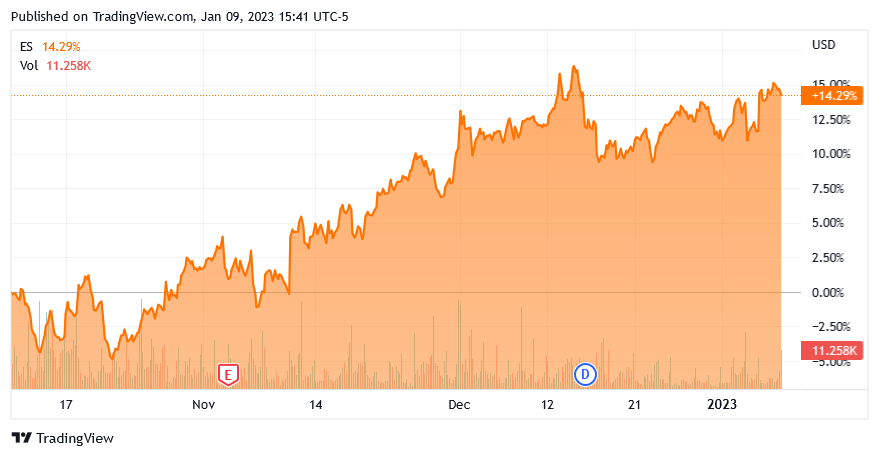

This is somewhat disappointing to see. As shown here, Eversource Energy looks rather expensive compared to several of its peers, although it is not the most expensive company here. Eversource Energy is also looking considerably more expensive than it was the last time that we looked at the company back in October, which is probably because the stock is up 14.29% in the past three months:

{kind=link}

Admittedly, it may be best to wait for a market correction before buying shares of the company. This strong recent performance and valuation do somewhat support my statements about the potential effects of the company’s environmental credentials, however.

Conclusion

In conclusion, Eversource Energy continues to be a respectable utility company with strong green ambitions. This may be reflected in the stock price, as Eversource Energy seems a bit expensive compared to some of its peers, although it is certainly not the most expensive company in the utility sector. Eversource Energy is a reasonable play today though as it has a strong balance sheet and is likely to increase its dividend in the very near future. I would recommend waiting for the stock price to decline in a market correction before buying in, though.

For further details see:

Eversource Energy: Strong Renewable Credentials Make For A Somewhat Pricey Stock