CNLHO - Eversource Energy: Undervalued Utility With A Generous Yield Is A Buy

2023-10-26 16:05:32 ET

Summary

- Eversource is a utility holding company with 4.4 million customers in Connecticut, Massachusetts, and New Hampshire.

- The company's share price has declined significantly due to a second-quarter charge related to the sale of an offshore wind project.

- I believe the stock is undervalued by 15.0% at its current level, with the potential for significant upside when the offshore project is resolved.

- The current dividend of 5.0% will likely be increased in February, and there are several series of preferred shares offering yields up to 6.8%.

Eversource Energy ( ES ) is a utility holding company with 4.4 million customers. It sells electricity, natural gas and water in the States of Connecticut, Massachusetts and New Hampshire. Electricity transmission and distribution make up about two-thirds of the company's revenues. Eversource currently has 14 subsidiaries; the most recognizable of these are The Connecticut Light & Power Company, NSTAR Electric, Public Service Company of New Hampshire, Aquarion Water, Yankee Gas Service and Eversource Gas of Massachusetts. According to the Edison Electric Institute, it is the 13th largest utility in the US by market capitalization, currently at $18.8 billion. The company has a strong credit rating of A-, or upper medium investment grade, from Standard & Poor's.

Eversource Service Area (2022 investor Presentation)

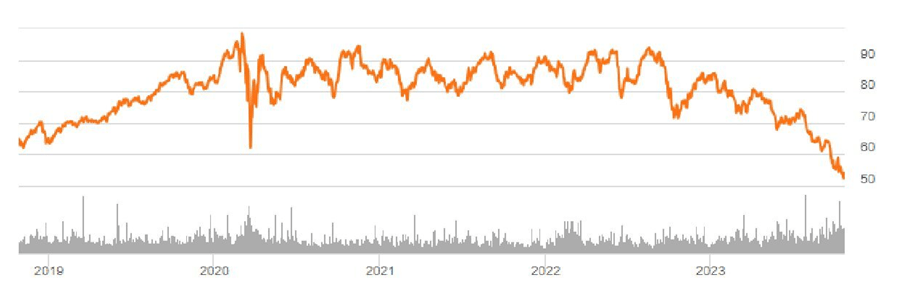

During the last year, the peak price for Eversource shares was $85.80 in January 2023. The current share price of $54.30 is down a remarkable 36.7% from that peak. Part of this decline is the market's reaction to a large charge-off in the second quarter of 2023, related to the sale of an offshore wind project. This charge lowered EPS from $0.99 to $0.04 for the quarter. When the news was announced, the company's share price was $67.24, 23.8% higher than it is today. The rest of the decline in the share price is due to utilities being out of favor in the market. According to Morningstar , the "median 16.0 P/E (for utilities) is at its lowest since exiting the 2008-09 recession," and the sector is down 13.0% since the beginning of 2023. Eversource's share price over the last five years is presented below.

Eversource Share Price Five Years (Seeking Alpha Charting)

{kind=link}

Earnings in 2022 and 2023

In 2022, total revenues were a healthy $12.29 billion , up 24.6% from $9.86 billion in 2021. GAAP earnings per share in 2022 (the company reports GAAP and non-GAAP) were $4.05, up 14.4% from $3.54 in 2021. The 2021 earnings per share would have been $3.86, except there were one-time charges of $0.32 per share paid by Connecticut Light & Power, as a credit to customers' bills in a rate settlement. In 2020, earnings per share were $3.55.

In the second quarter of 2023, the company reported earnings of $15.4 million, or $0.04 per share, versus $291.9 million, or $0.84 per share, in the prior year. In the first quarter of 2023, earnings per share were $1.41 compared with $1.28 in the first quarter 2022. Second quarter 2023 earnings would have been $0.99 per share and first half earnings would have been $2.40 but for a one-time charge-off. This was described as follows: "As a result of Eversource completing its Offshore Wind Strategic Review that included the sale of its interest in the undeveloped offshore lease area… Eversource has determined that the carrying value of its total offshore wind investment is impaired. Therefore, the results for the second quarter and first half of 2023 include an after-tax impairment charge of $331.0 million, or $0.95 per share." As a result, Eversource Energy reported earnings of $1.45 per share during the first half of 2023, compared to $2.13 per share during the first half of 2022. This issue is discussed further in a later section.

Regulatory Environment

Not all of Eversource's subsidiaries are regulated, but the ones that are include the majors Connecticut Light & Power, NSTAR Electric, Public Service Company of New Hampshire, Yankee Gas, Aquarion Water, NSTAR Gas and NSTAR Electric. Electric transmission is 41.0% of regulated earnings, electric distribution is 40.0%, natural gas distribution is 16.0% and water services are 3.0%.

The rate base of the company was $24.4 billion at the end of 2021, per the June 2023 Investor Presentation , and it is expected to grow to $37.7 billion by the end of 2027. There are a total of 12 state and federal regulatory agencies that oversee what Eversource can charge. Current allowed return on equity is in a range from 9.8% for NSTAR Electric to 11.14% for Connecticut Light & Power. Average return on equity for the company in 2022 was at a 10.57% base, with an incentive cap at 11.74%.

During the past year, an important rate decision in Eversource's favor came from the Massachusetts Department of Public Utilities, which approved a base distribution rate increase of $64 million effective January 1, 2023

Long-Term Debt

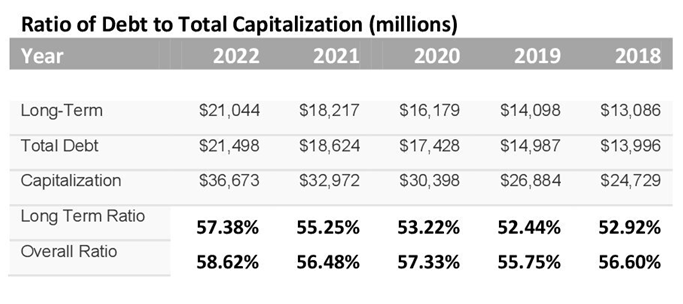

During 2022, Eversource had increases in short-term and long-term interest expenses due to higher interest costs after the Federal Reserve raised rates. This has been the case at many utilities the last two years. Interest expense increased by $95.9 million in 2022, or $0.27 per share, a not insignificant number. While the overall level of total debt has risen slightly over the last five years, from 56.6% to 58.6% of total capitalization, overall it is considered to be at manageable levels, as presented below.

Debt to Total Capitalization (Author Calculated)

{kind=link}

Capital Expenditures - Five Year Plan and Renewables

Eversource has earmarked a total of $21.5 billion to be invested in infrastructure between 2023 and 2027. A large portion of this money is for grid modernization, which is especially needed in Connecticut. In 2021, autumn storms knocked out power for several days there. The bulk of the money will be spent on "transmission line upgrades, the installation of new transmission interconnection facilities, substations and lines, and transmission substation enhancements." A portion of the funds are budgeted to help the company meet its carbon-neutral goal by 2030.

The push toward renewables is the result of two factors. The first is the Paris Climate Accord . The second is that the current US administration has set a goal of reducing greenhouse gas emissions 50.0 percent by 2030 , based on 2005 levels, and achieving net-zero emissions by 2050. Several states that are in Eversource's service territory also have their own carbon goals. In Connecticut there is legislation to achieve zero carbon by 2040 and in Massachusetts there is a net zero emissions target for 2050. New Hampshire has a Climate Action Plan calling for an 80.0% reduction in greenhouse gas emissions by 2050. Connecticut's Renewable Portfolio Standard requires increasing percentages of the electricity sold in the state to have a renewable source. That percentage was 33.0% in 2022. All the state regulatory agencies allow Eversource to recover capital costs for investments in renewables.

To date, most of Eversource's renewable projects have involved wind. There are three projects in development and another that was offshore land. From the 10-K: "Revolution Wind is a 704 MW offshore wind power project located approximately 15 miles south of the Rhode Island coast, and South Fork Wind is a 130 MW offshore wind power project located approximately 35 miles east of Long Island." Construction is nearing completion on South Fork Wind with service projected by late 2023. There is also the Sunrise Wind Project, which is off the coast of Long Island. The fourth location, which has now been sold for $625 million, was land off the coast of Massachusetts. This was sold to Eversource's development partner Orsted ( DNNGY ).

The three projects still underway are expected to be in operation by 2025. However, Eversource is considering selling its 50.0% interest in one or more of the remaining wind projects. Regulators recently denied a rate increase that would have made these projects more profitable. In total, Eversource has invested $1.95 billion in wind as of the end of 2022. The write-off was about 17.0% of this amount.

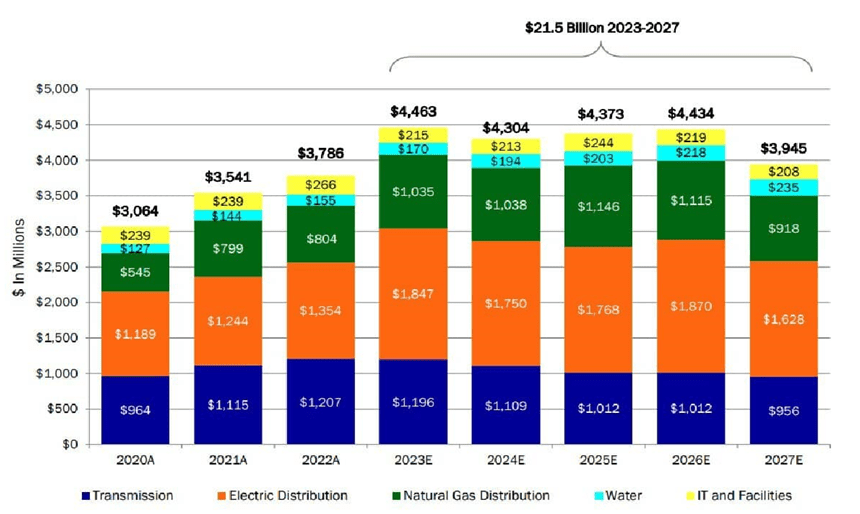

As for solar, the company has plans for six cluster areas in Massachusetts that could add one gigawatt of generation. Below is a schedule of Eversource's planned capital investments over the next five years.

Five-Year Capital Expenditures (2023 Investor Presentation)

{kind=link}

The Eversource Dividend

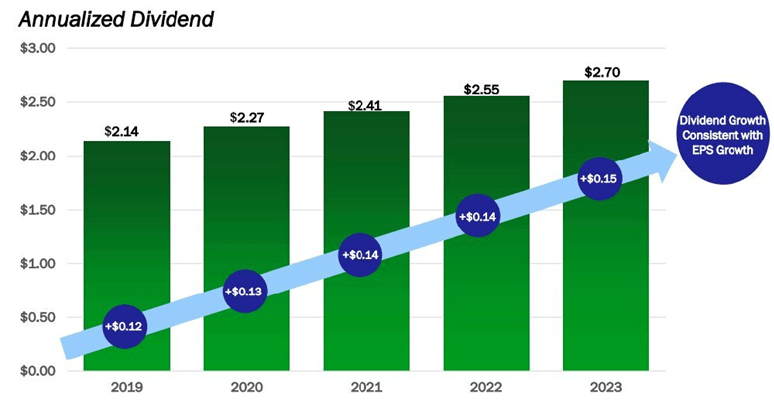

Eversource has increased its dividend every year since 2001, now a total of 23 years. In 2025, Eversource will most likely become a member of the Dividend Aristocrats, a Standard & Poor's list that requires the company to be a member of the S&P 500, have a market cap over $3.0 billion, and 25 consecutive years of raising the dividend.

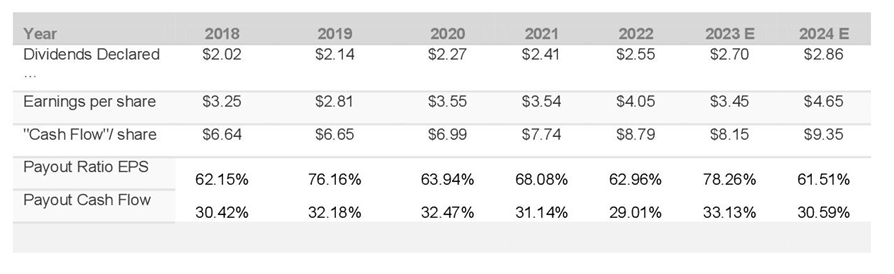

The current yield is 5.0%, with a quarterly payout of $0.675. The next increase will be for the March 2024 payment, typically announced by the board in February. The company expects to grow the dividend and earnings per share at 5.0-7.0% per year, per the 2022 Presentation . Right now the dividend at Eversource is quite attractive compared to many other large cap peer utilities like The Southern Company ( SO ) which has a yield of 4.18%, or Duke Energy ( DUK ) which has a yield of 4.63%, or American Electric Power ( AEP ) with a current yield of 4.64%. Below is a table of the dividend amount and payout ratio by year, using GAAP figures.

Eversource Payout Ratio (Author Calculated)

{kind=link}

The current payout ratio based on earnings per share is very reasonable and sustainable. Note the 2023 figures have been lowered by the $0.95 per share charge-off in the second quarter 2023. Even so, the payout ratio for the year looks acceptable. According to Edison Electric Institute, the average utility payout ratio in 2022 was 70.8%. By way of comparison, the average for Consumer Staples was 54.3%.

Dividend Growth (2023 Investor Presentation)

{kind=link}

Several Series of Preferred Shares

An Eversource subsidiary, The Connecticut Light & Power Company has 13 different series of preferred shares at present, with face yields ranging from 3.8% to 6.56%. Investors should note that these series are all yielding 6.4-6.8% today, based on their current price. These were issued between 1947 and 1968; they all have redemption premiums $0.50 to $2.50 per share and at this point it is unlikely that they will be redeemed. You can find all of these listed here at Quantum Online. These debuted before EDGAR, so I am seeing no prospectuses for these shares. These are trading OTC and have a very thin volume, but here are some of the tickers that have more activity: CNLPL , the 1963 Series at 4.5%; CNLTL the 1947 series at 3.8%; and CNLHO the 1956 Series at 4.5%. These all have a par value $50.00 per share, and are rated BBB+ by Standard & Poor's, or middle investment grade. These shares are all cumulative and eligible for preferential tax treatment.

NSTAR Electric also has two series of preferred stock, both with a par value $100.00 per share, and known as the 4.25% Series and the 4.78% Series. These were issued in 1956 and 1958, respectively. Investors should note that these series are all yielding 6.3-6.5% today. The tickers are NSARP and NSARO . These are cumulative and qualified. NSARP has a $3.63 per share redemption premium while NSARO has a $2.80 per share redemption premium. As with the Connecticut Light & Power Shares I believe it is unlikely they will be redeemed at this point. Both NSTAR Series are rated BBB+ by Standard & Poor's, or middle investment grade.

Valuation of Shares

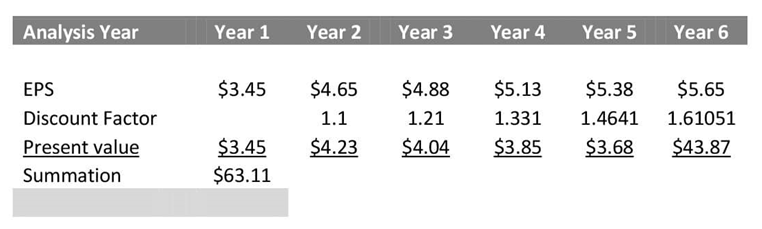

I estimate the current value of Eversource shares to be $63.11, so at today's price of $54.30, shares are about 15.0% undervalued. I used a discounted cash flow cash to value the stock, starting with the earnings per share estimate of $4.40, less the $0.95 per share impairment charge, so $3.45 per share beginning in 2023, and then projecting forward. In this case I have used a 5-year projection period. For the discount rate, I considered the average annual return of the S&P 500. The long-term average is about 9.8% , while over the last 10 years it has been higher at 12.4% . I have used a discount rate of 10.0% here, just above the lower end of the range, and discounting begins in the second year. I have used a reversion rate of 8.0%.

Below are Eversource's annual earnings since 2018. Note that these are the GAAP figures. Between 2018 and 2023 the compound annual growth rate in earnings per share was 6.2% (assuming the one-time charge didn't occur), so within the company's targeted range of 5-7.0% for its earnings per share. Morningstar forecasts a median 6.0% annual EPS and dividend growth across the overall utility sector. This is also supported by Institutional Investor , which has projected 6.0% per year growth for utilities over the next three years.

Earnings per Share (2022 Annual Report)

{kind=link}

To be on the conservative side in evaluating the company, I have used an annual growth rate of 5.0%. The resulting valuation per share as presented below.

Eversource Discounted Cash Flow (Author Calculated)

{kind=link}

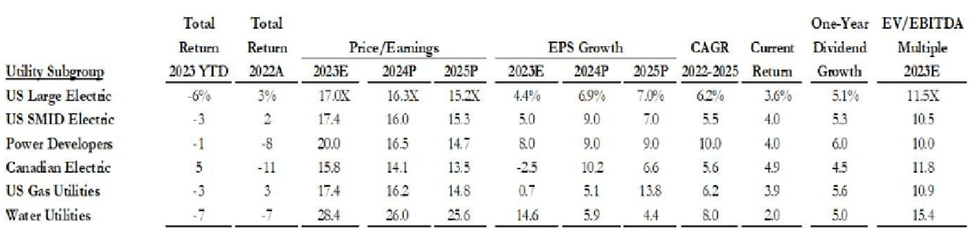

I have also looked at the shares through the lens of P/E Ratio valuations. According to Morningstar, the current "median 16.0 P/E (of utilities) is at its lowest since exiting the 2008-09 recession." Morningstar also estimates that the sector is 15.0% undervalued. I was able to locate two other source of P/E multiples including Yardeni Research , which estimates the forward P/E multiples of electric utilities as 14.7. Gabelli Funds tracks utility ratios and lists US large electric as 16.3 for the upcoming year and gas utilities as 16.2 times earnings.

Utility P/E Ratios (Gabelli Funds)

{kind=link}

Using the forward multiples and the earnings estimate for next year of $4.65 (to avoid dealing with the one-time charge-off), the value by P/E comparable is somewhere between 14.7 X $4.65 = $68.36 and 16.0 x $4.65 = $74.40. This would make the shares as much as 27.0% undervalued. I have chosen the more conservative and likely more accurate DCF estimate of $63.11 for my value conclusion.

Risks to Outlook

The primary risk with Eversource is the outcome of the sale of its offshore wind projects. Will they sell and for how much? I believe that Eversource's share price will be held back by this issue until it is resolved. Another risk that all utilities face right now is unseasonably warm weather. This has lowered electric demand and adversely impacted earnings per share.

Conclusion

The company's current forward P/E ratio of 11.7 (using the forward EPS estimate of $4.65) is well below the utility industry multiple of 16.0, and below the forward multiple of 14.7 for the industry. I think the discounted cash flow number of $63.11 is the right way to look at this company, so, generally shares are 15.0% undervalued. The dividend is already at 5.0% so a 5.0% increase next year would take it to 5.2% at the current price. The stock has an attractive valuation and an attractive yield, you just have to be comfortable with the possibility of more wind-related charge-offs in the future. It looks like this is mostly a thing of the past, but the market is certainly discounting for the possibility of more.

Of note, in 2022, Eversource issued 2,165,671 common shares, which generated revenue of $197.1 million. This equaled about 0.6% of the 349.1 million shares outstanding. The average price for these shares was $92.71.

For further details see:

Eversource Energy: Undervalued Utility With A Generous Yield Is A Buy