ES - Eversource Energy: Upgrading To Hold But Fundamental Challenges Remain

2024-01-16 12:53:00 ET

Summary

- The renewable energy market faces challenges due to last year's rising interest rate environment and shifting sentiment away from the ESG movement.

- I am upgrading Eversource Energy from a sell to a hold, but fundamental issues remain.

- ES faces challenges with offshore wind projects, potential impact from regulatory and political changes, and weakness in the renewable power market.

- I outline key price levels to monitor on the chart.

The renewable energy market took a sharp turn for the worse over the last several quarters amid steeply rising interest rates and an overall sentiment shift away from the ESG movement. Solar and wind projects are now being called into question given steeper costs to borrow while higher rates have broadly hurt the yield-sensitive Utilities sector.

I have a hold rating on Eversource Energy ( ES ). That is an upgrade from my sell rating issued in 2022 , but I continue to see fundamental challenges. The good news is that while the technical chart is soft, ES’s valuation has discounted a sizable portion of the bad news.

ESG Losing Favor

{kind=link}

According to Bank of America Global Research, ES is a regulated utility company providing electric and gas distribution as well as electric transmission services to customers in CT, MA, and NH. It also owns a water utility (Aquarion) which serves the same three states. ES has invested in offshore wind and announced a strategic review of the business in 2022.

The Massachusetts-based $19.9 billion market cap Electric Utilities industry company within the Utilities sector trades at a low 13.1 forward non-GAAP price-to-earnings ratio and pays a high 4.8% dividend yield as of January 12, 2024. Ahead of earnings due out next month, shares trade with a moderate implied volatility percentage of 25% while short interest on the stock is modest at just 1.3%.

ES faces significant challenges following a major $1.4 to $1.6 billion after-tax impairment charge to its offshore wind projects announced earlier this month. The stock plunged in the wake of that announcement after having rebounded in Q4 2023. The headline came after an impairment warning issued in May last year, and the total $1.9 billion impairment amount (pre-tax) was larger than was previously disclosed.

The major charge came after an EPS miss reported in November 2023; Q3 non-GAAP EPS of $0.97 was a penny worse than expected while quarterly revenue of $2.8 billion, down 13% from year-ago levels, was a substantial $620 million miss. Its earnings outlook is now at risk after the impairment announcement, so the long-term EPS growth rate of 5% to 7% may not materialize given the ongoing weakness in offshore wind. Key risks include regulatory and political changes that could adversely impact the business along with further weakness in the renewable power market.

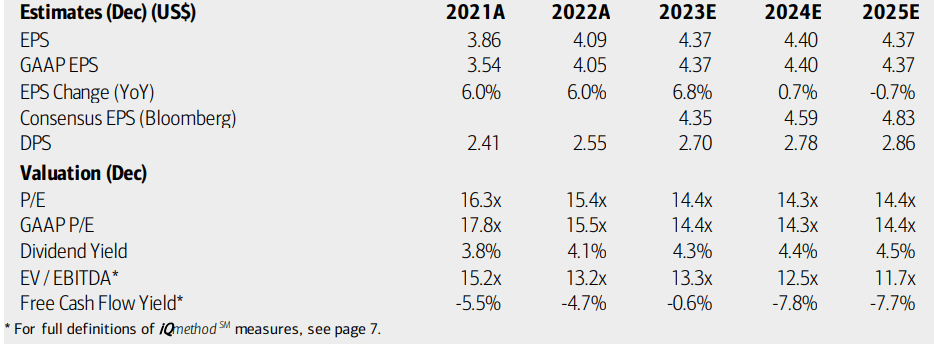

On valuation , analysts at BofA see earnings having risen by a solid 7% in 2023 but per-share profit growth is expected to stagnate over the next two years. EPS may hover around $4.40 on an annual basis, though the current consensus outlook, per Seeking Alpha, shows decent bottom-line growth in the mid-single digits through 2025. Revenue growth is forecast to range between 3% and 5%.

Dividends, meanwhile, are forecast to rise at a steady pace over the coming quarters, potentially making for a high yield. Free cash flow is negative, but that is common among Utilities sector companies that often have high capital expenditures. With an operating P/E now in the low teens and a high yield, the valuation has baked in a decent amount of negativity.

ES: Earnings, Valuation, Dividend Yield Forecasts

{kind=link}

If we assume $4.55 of normalized earnings over the next 12 months and apply a 13 P/E, below the sector median and ES’s 5-year historical norm due to its fundamental challenges, then shares should trade near $59. That is slightly undervalued, but amid uncertainties with its offshore wind assets and tepid profit growth ahead, a valuation discount is warranted. Overall, the valuation situation appears fair to me.

ES: Compelling Valuation Metrics, But Growth At Risk

{kind=link}

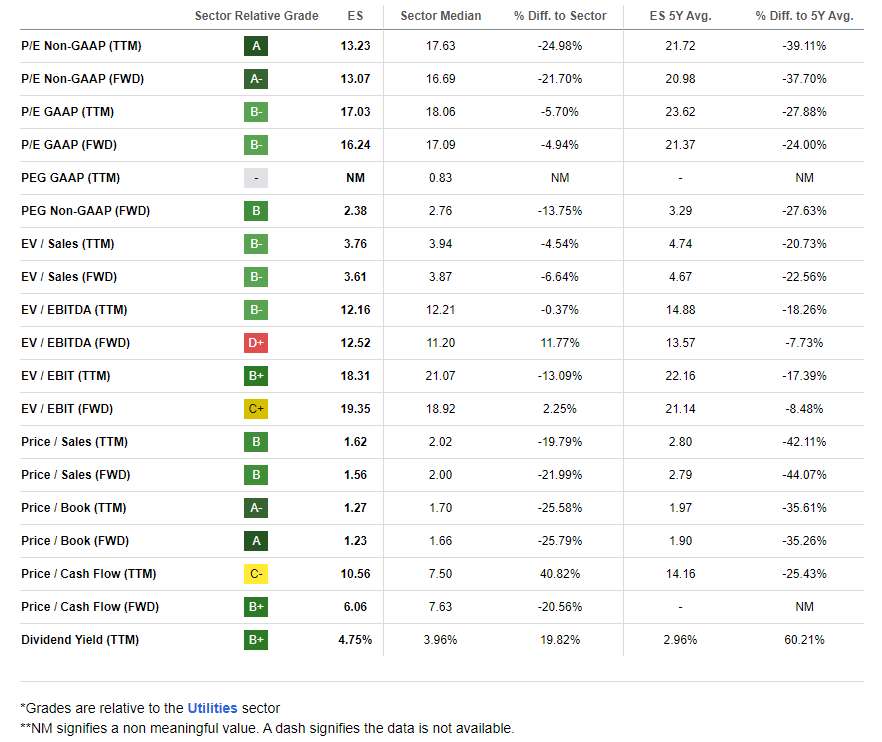

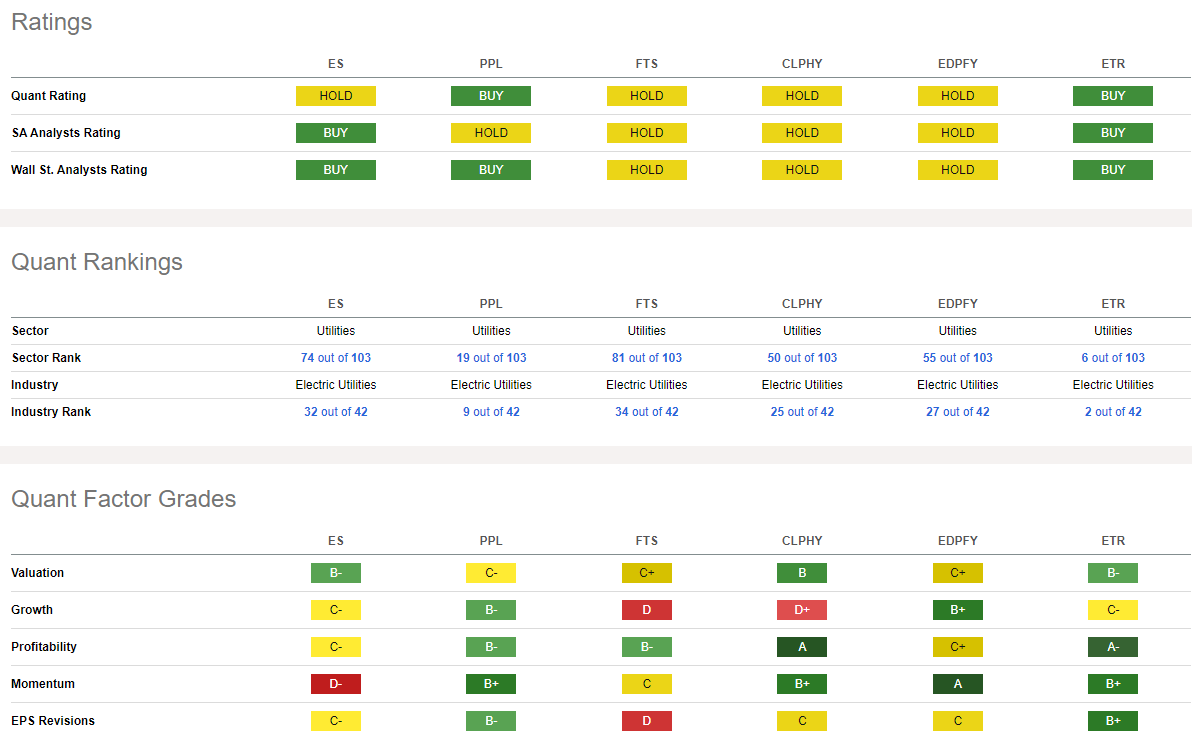

Compared to its peers , ES features a low set of valuation multiples while its growth trajectory is generally weaker than its domestic competitors. Profitability metrics are likewise soft and momentum has been extremely poor of late. EPS revisions , not surprisingly, are on the negative side (8 negative, 5 positive over the last 90 days).

Competitor Analysis

{kind=link}

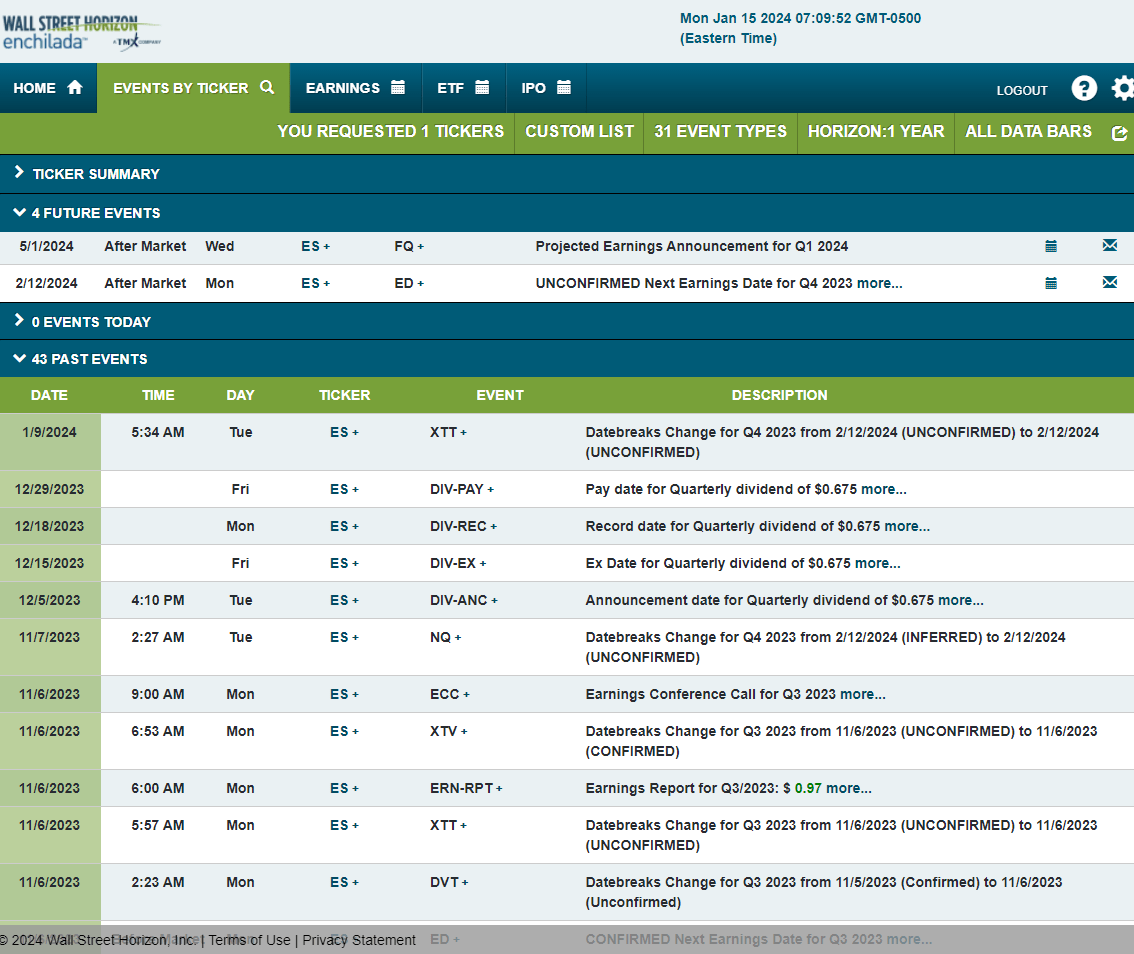

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2023 earnings date of Monday, February 12, after the close. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

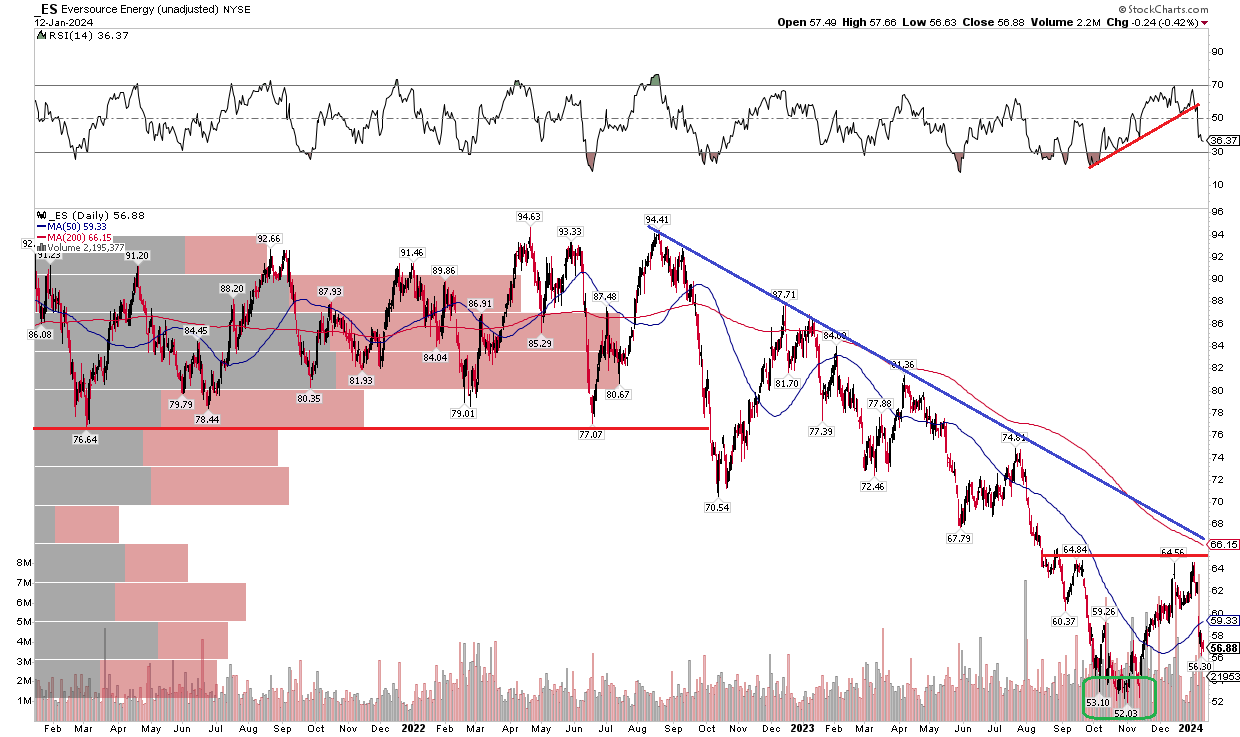

With a troubled fundamental backdrop and a fair valuation, the chart is quite weak. Notice in the graph below that ES has been mired in a steep downtrend off a double-top high notched in Q2 and Q3 of 2022. For about a year and a half, the bears have been in control, and it’s hard to suggest that has changed. The long-term 200-day moving average remains negatively sloped and there has been a bearish breakdown in the RSI momentum oscillator’s trend, indicated at the top of the chart.

Also take a look at how the $76 to $77 range was key support back when I first wrote on the stock in the middle of last year – while ES wavered around that mark, it ultimately broke down. The stock bottomed out at $52 last November, and shares appear ready to retest that mark in the weeks ahead. I see near-term resistance just above $64 – the September 2023 and early 2024 rebound highs. There is possible support at $52 – if we were to stretch out the chart’s zoom to 2018, we would find that ES bottomed there during the middle part of that year, so there could be some dip-buyers there.

Overall, the technical trend is bearish, though key support is seen at $52. Near-term resistance is in the mid-$60s with longer-term resistance starting at $76.

ES: Bearish Downtrend, RSI Breakdown as Price Approaches $52 Support Again

{kind=link}

The Bottom Line

I have a hold rating on ES. It is an upgrade from a sell rating issued 18 months ago, but the fundamental backdrop remains murky. The valuation has discounted a hefty amount of bad news while technicals suggest significant price-action risk.

For further details see:

Eversource Energy: Upgrading To Hold, But Fundamental Challenges Remain