TSM - Everspin Technologies: A Bargain Semiconductor Play

Summary

- Everspin's valuation keeps compressing in a positive fashion on a flat stock quote in 2022-23.

- An upside breakout may be about to take place, if Q4 EPS surprises analysts and investors again in coming days.

- A solid price gain on limited volume interest since December may be shouting a lack of overhead share supply exists.

- Price to trailing sales around 2x is incredibly cheap for a growing and profitable semiconductor business.

I have written about Everspin Technologies ( MRAM ) several times since 2021 as a bullish growth and value pick in the U.S. semiconductor space. And, the positive setup appears to be getting cheaper, as underlying sales and income continue to ramp with higher results than expected, at the same time as the stock quote has stagnated. My last article in May 2022 linked here provides a good overview of the business model and products offered. Since this effort, price has risen about +5% vs. a flat total return from the S&P 500 index.

Seeking Alpha - Paul Franke, Everspin Article, May 6th, 2022

{kind=link}

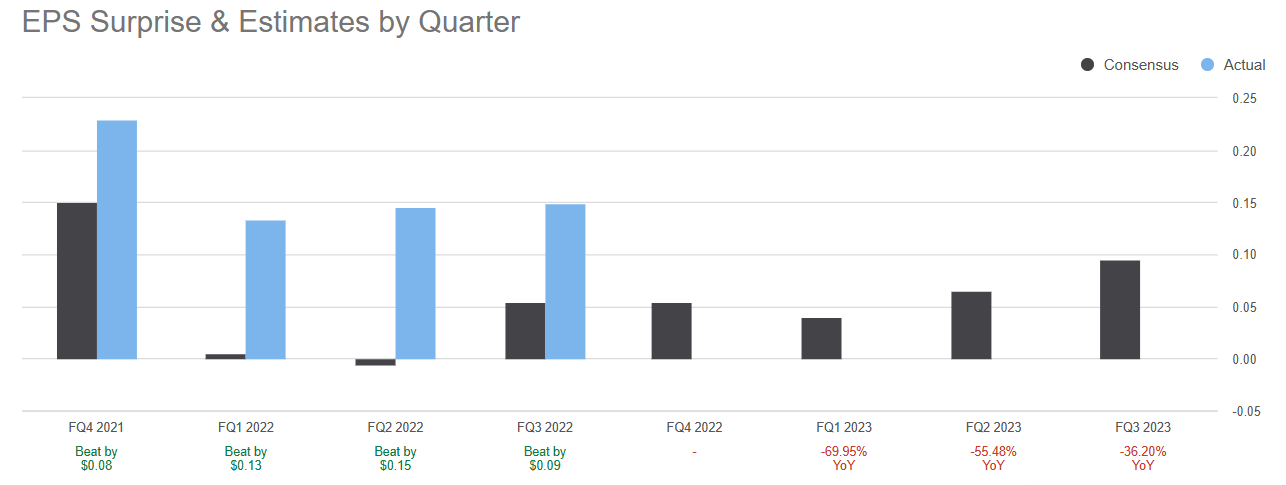

Earnings and sales continue to impress with reports in 2022 far exceeding tempered Wall Street analyst expectations. In fact, I would rank Everspin's history of beats near a leading position vs. the semiconductor industry trying to rebalance supply/demand after once-in-a-lifetime pandemic disruptions.

Seeking Alpha Table - Everspin, EPS since Q4 2021, Forward Analyst Forecasts, February 14th, 2023

{kind=link}

You can review below the wicked progress MRAM has made toward serious profitability in 2022 vs. large operating losses just a few years ago. This 5-year net income margin improvement is measured against more successful semiconductor and memory chip peers and competitors NVE Corp. ( NVEC ), Intel ( INTC ), NVIDIA ( NVDA ), Advanced Micro Devices ( AMD ), Micron ( MU ), Taiwan Semiconductor ( TSM ), Texas Instruments ( TXN ), Qualcomm ( QCOM ), and Rambus ( RMBS ).

YCharts - Memory Chip Makers, Final Income Margins, 5 Years

Undervaluation Story

In my opinion, Wall Street still incorrectly believes Everspin is a money losing outfit, not an increasingly profit-driven enterprise. On basic ratio analysis of price to trailing earnings, sales, cash flow, and tangible book value, the company can be argued as having its lowest valuation ever in early 2023. Being able to purchase a profitable and growing semiconductor concern (with an extensive list of patents on spintronics memory chips) for just 2.3x sales is a difficult find.

YCharts - Everspin, Price to Trailing Fundamentals, 5 Years

Even better news is the balance sheet is full of cash with only minor liabilities and IOUs. $23 million in cash and $44 million in current assets were held at the end of September vs. just $17 million in total liabilities (about half of liabilities revolved around debt and long-term building leases) This means enterprise value calculations actually reduce the $140 million market cap for an upfront number using price alone. The $120 million for EV today is more appropriate in determining the operating business worth for investors (or as a basis for takeover bids).

EV to revenues is trading under 2x, which is the lowest ratio vs. the peer group of leading semiconductor names, somewhat lower than the depressed and problematic operating businesses of Intel (product issues) and Micron (chip cycle issues). This simple EV/sales comparison is a good 65% discount to the median average of 5.5x for the group.

YCharts - Memory Chip Makers, EV to Trailing Revenues, 1 Year

On EV to cash EBITDA readings, Everspin is also sliding into the lower tier for a valuation, assuming earnings and sales continue to impress on the upside in 2023. Over the past 12 months, this ratio has declined from 35x to 12x, which is now close to the peer median average. Very quickly, the argument that Everspin is not profitable enough to consider for investment may disappear for bears and sideline watchers. A transition in sentiment toward a buy decision could be the catalyst for far stronger share pricing.

YCharts - Memory Chip Makers, EV to Trailing EBITDA, 1 Year

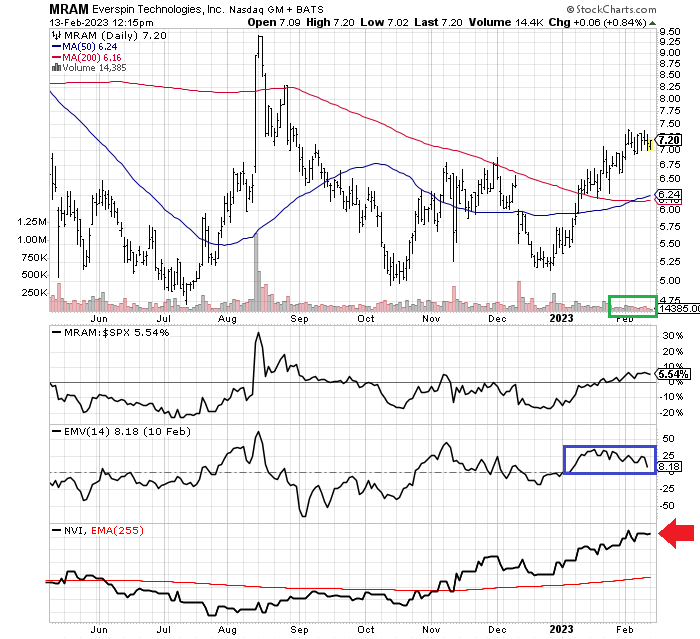

Technical Trading Chart

Rising price on low volume, combined with several momentum indicators moving in a positive direction, has me a little excited for 2023.

Below is a chart drawn from my last MRAM article, posted roughly 9 months ago, of daily changes in price and volume trading. The first thing to notice is price has jumped since December and now sits comfortably above both its 50-day and 200-day moving averages (with trending higher MAs since last week).

Secondly, and completely out of character with 2022 trading, ultra-low volume has been part of the rising price trend in early 2023 (boxed in green). Sure, climbing price on high volume is great, but often low volume increases in the quote are even better signals of future big gains (especially in short squeeze situations).

Everspin has outperformed the S&P 500 by +5% over 9 months, but almost +25% over the latest 8 weeks! The solid price gain on low volume is the main reason the Ease of Movement indicator has been in a steady bullish pattern in early 2023 (boxed in blue). The 14-day EMV indicator is more of a coincidental readout vs. a predictive one. Nevertheless, prolonged bull advances usually have steady EMV trends vs. spikes on high volume. I really like the EMV pattern for MRAM of late.

The Negative Volume Index has also reversed a regular downtrend in 2022 into a very bullish and consistent rising trend (marked with a red arrow). Since October, the advancing NVI may be signaling a lack of overhead share supply, as plenty of buyers exist on slow-volume trading sessions, while price is zigzagging to new highs each week or two.

StockCharts.com - Everspin, 9 Months of Daily Price & Volume Changes, Author Reference Points

{kind=link}

Final Thoughts

After stagnating in price with the semiconductor investment group and having to fight weakness in the overall market (represented by the S&P 500 index) last year, the long-term value proposition in February is getting harder to ignore.

I own a small stake in Everspin, and am considering buying additional shares. The technical setup for a material turnaround and sharp quote gain is close to ideal. Of course, such will depend on the Q4 earnings release in a couple of weeks. If MRAM is able eclipse Wall Street analyst expectations AGAIN, larger asset managers like hedge funds and actively managed mutual funds could push price straight up. It would be an admission they don't want to miss the boat on this growing semiconductor concern. On the flip side, EPS around the unchanged level that meets current estimates will likely hold the stock quote in the $6 to $8 range during the first half of the year.

With sizable cash holdings and at least breakeven numbers for income, I don't see much downside beyond $5 a share, as my worst-case scenario over the next 12 months. Yet, given EPS above $0.50 for 2023, a share price of $10-12 looks entirely appropriate to me. So, a range of possibilities from -30% for a total return from $7 currently, to +65% in a best-case scenario argue for ownership.

The odds of a takeover bid above $12 or a strong cyclical uptick in demand for Everspin's rugged and unique memory inventions could bring outlier gains. Since I am not expecting the S&P 500 to advance much or even decline the rest of the year, finding equities with the honest potential to jump +50% or greater will be key to investment portfolio success. MRAM fits this description for me. I rate the stock a Buy.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Everspin Technologies: A Bargain Semiconductor Play