MRAM - Everspin Technologies: Fair Price Point With An Exciting Market Opportunity

2024-01-15 01:50:28 ET

Summary

- Everspin Technologies is a small-cap company in the semiconductor space focusing on spintronics and related products.

- Everspin offers a diverse range of MRAM solutions for various industries, including industrial, medical, automotive, aerospace, and data centers.

- Despite a slight decrease in sales, MRAM has achieved a positive bottom line and is positioned for growth, with a price target of $11.7.

Investment Rundown

The semiconductor space is broad and covers a lot of various markets right now. One of the most exciting markets to be a part of I think quite honestly. One of the companies that I have recently stumbled upon is Everspin Technologies ( MRAM ). This company is focusing on spintronics and various products related to that. It's a young market that is experiencing quite a lot of demand, mostly from increased demand from factories and production facilities where machines are getting more and more advanced to further efficiencies various processes. It's quite broadly and briefly explained, but I think MRAM along with other companies in this sector is a good bet on increased spending in production outputs, but also more domestic production capabilities.

The market cap of MRAM is quite small, just under $200 million which certainly puts it in the small-caps category, but I think this is where you want to be looking in 2024. With the market MRAM operating is expected to rapidly grow, making the company a small position in a portfolio I think is a worthwhile thing to do, to not miss out on this opportunity. I am covering Everspin stock for the first time and I will be doing so by rating it a buy.

Company Segments

MRAM is a manufacturer and supplier of magnetoresistive random access memory products. With a global presence spanning across important markers like the US, but also in China and Germany for instance. The company offers a very diverse range of MRAM solutions. These include Toggle MRAM products, spin-transfer torque MRAM, and tunnel magneto resistance sensor products, catering to various applications across industrial, medical, automotive/transportation, aerospace, and data center markets. A large portion of these markets are expected to continue to grow at very solid rates over the next several years. One worth highlighting for example is the data center market, expected to reach a CAGR of 10.9% until 2030. The primary tailwinds for this are increased company spending in cloud capacity and computing power.

{kind=link}

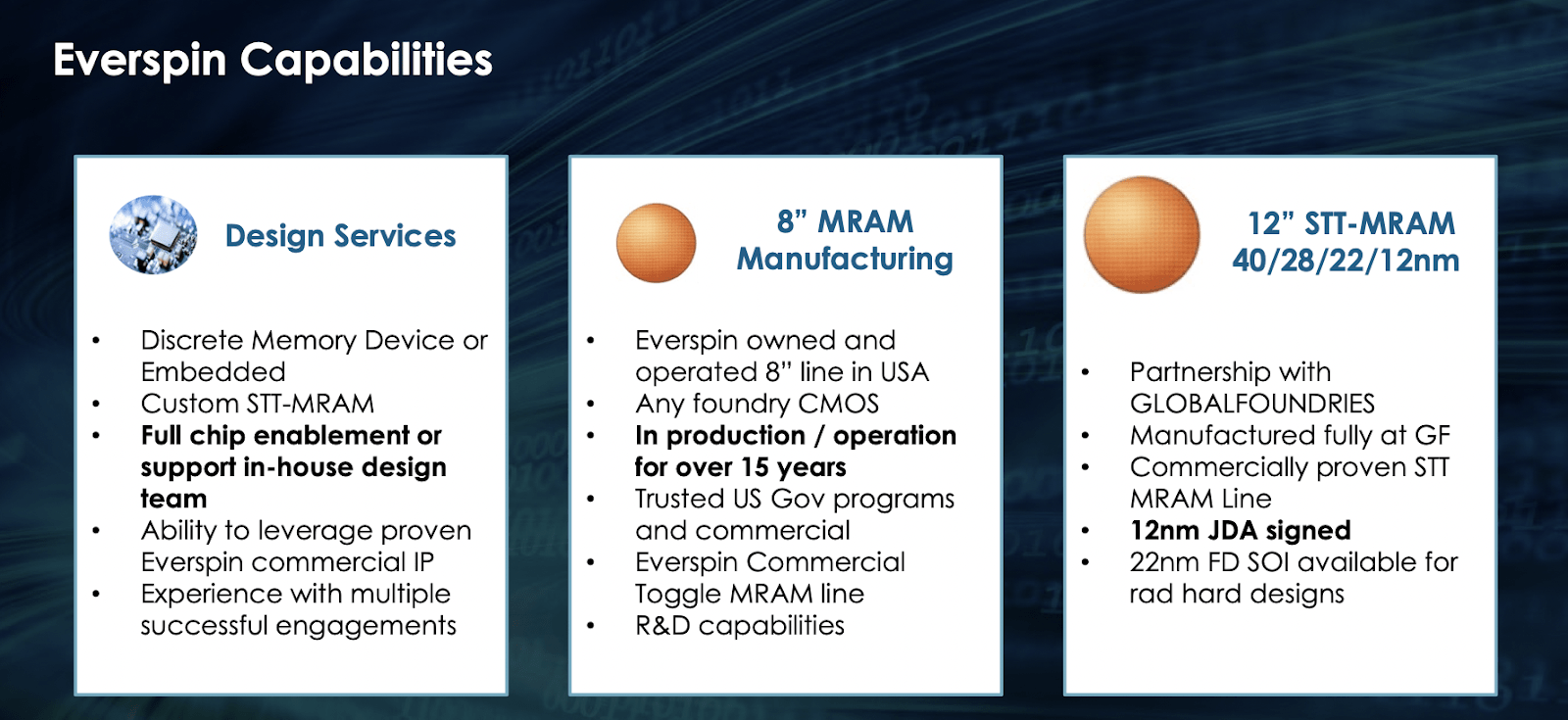

STT-MRAM specializes in both Discrete Memory Devices and Embedded solutions. They offer custom Spin-Transfer Torque Magnetoresistive RAM, providing full chip enablement and support through an in-house design team. Everspin's ability to leverage proven commercial IP is exemplified by its successful engagements in this field. The company owns and operates an 8-inch MRAM manufacturing line in the USA, utilizing any foundry CMOS. With over 15 years of production experience, Everspin's 8-inch line is trusted by U.S. Government programs and commercial entities.

{kind=link}

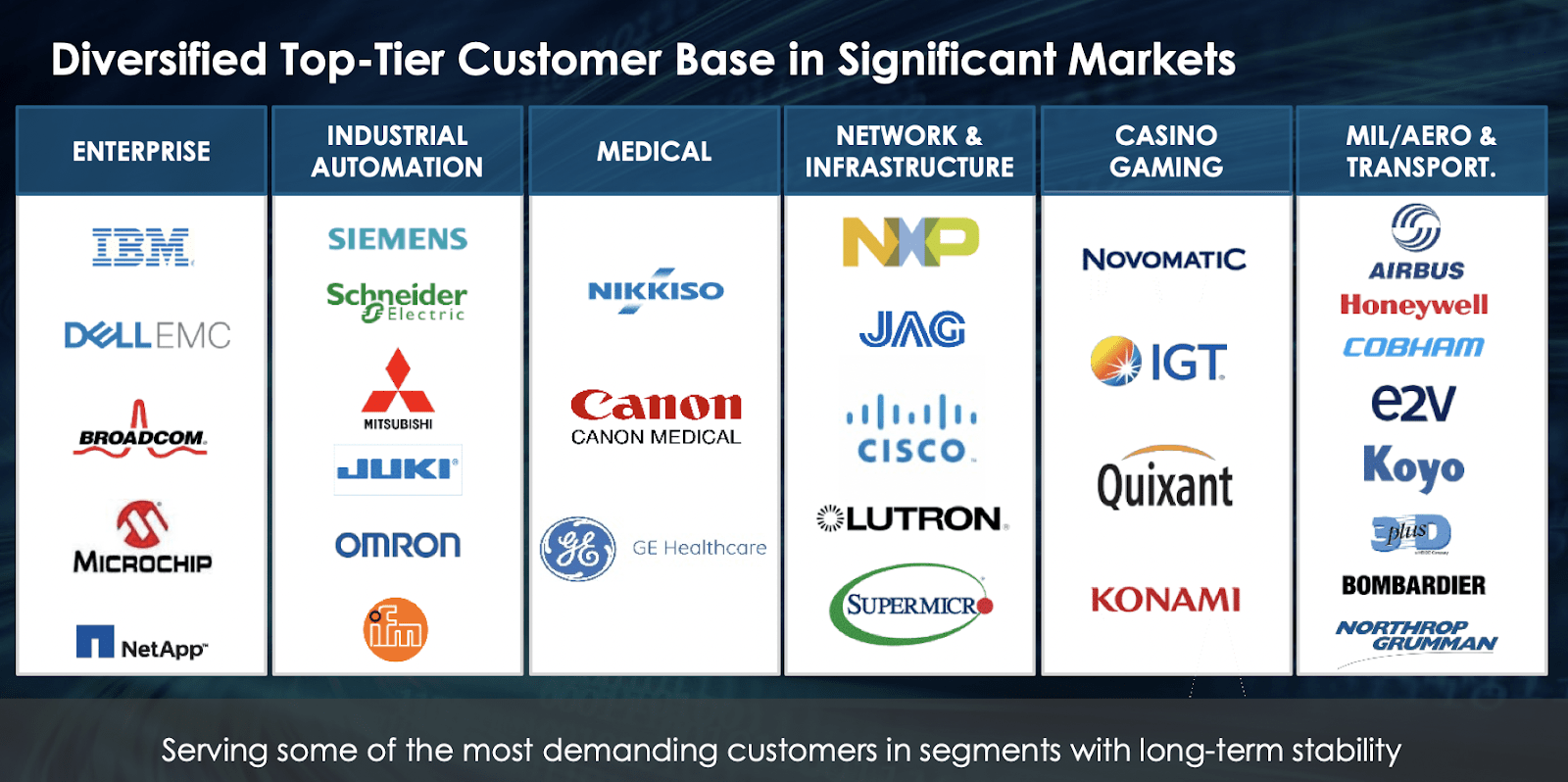

Being included in government programs I think offers MRAM an exciting opportunity to take on more contracts from this side. Being a supplier to the US government would bring about a steady stream of revenues in my opinion. But apart from government programs, MRAM has been very active in partnering up and collecting very large customers like Siemens (SIEGY) and Airbus ( OTCPK:EADSF ) for example.

Earnings Highlights

{kind=link}

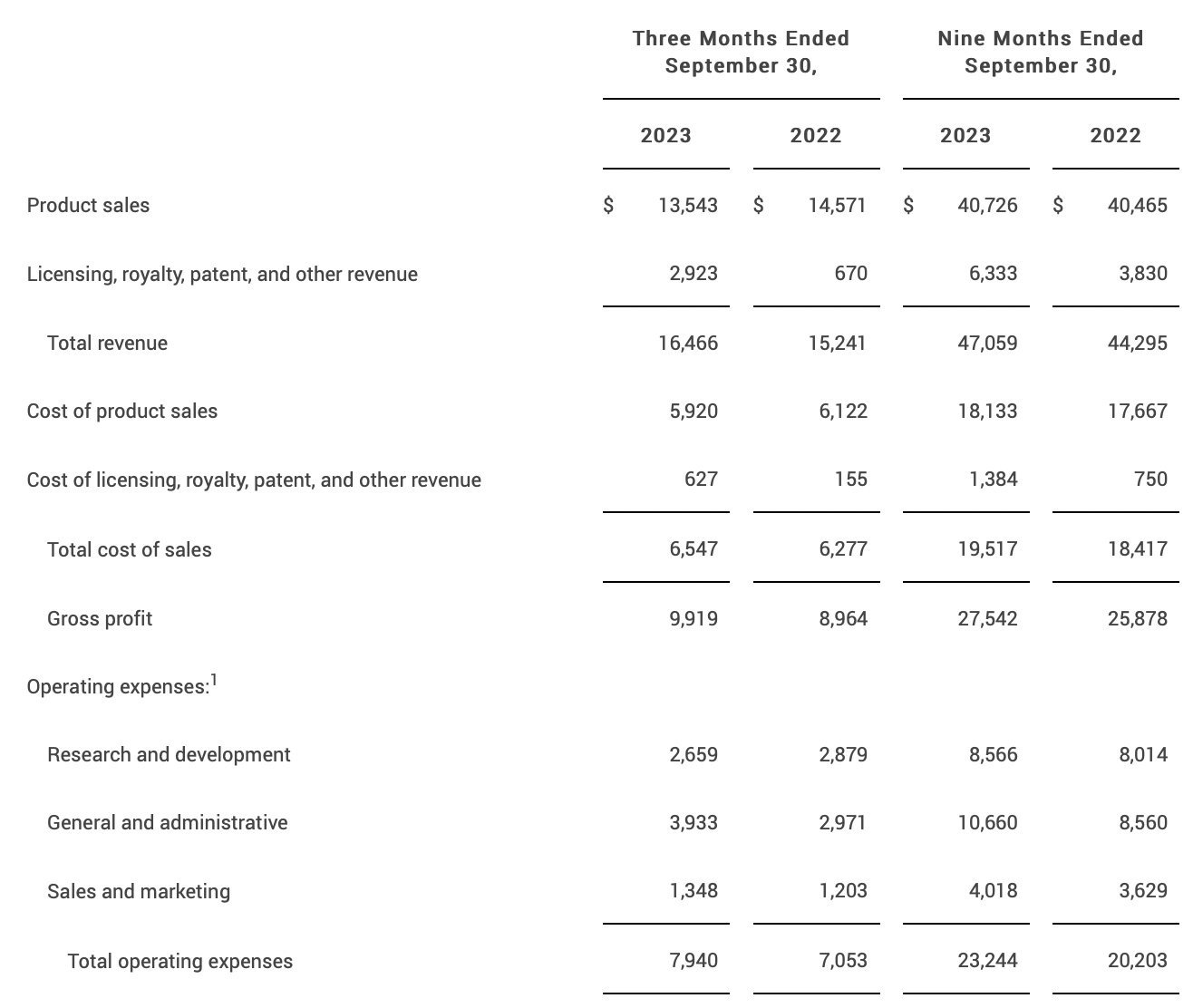

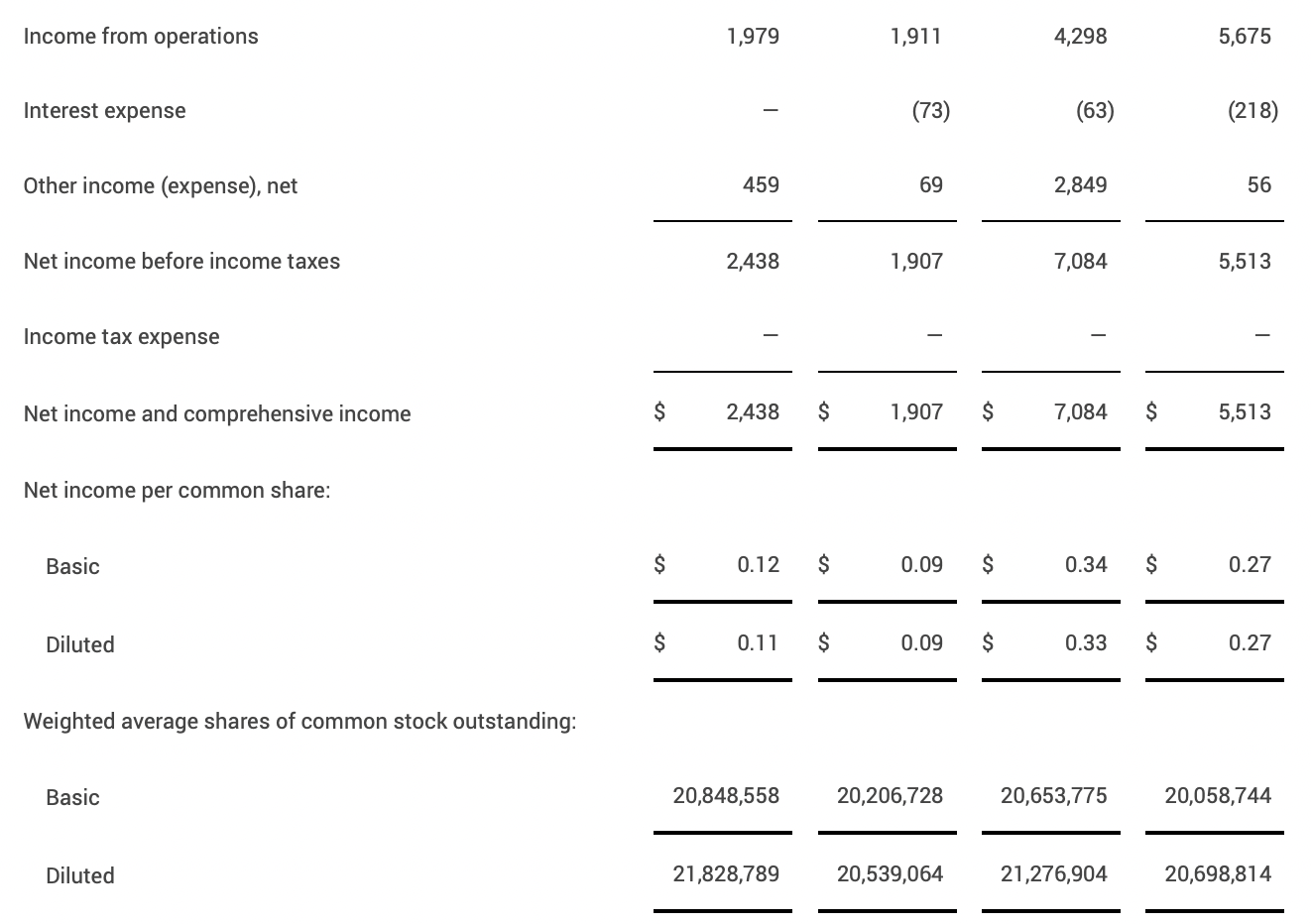

On November 1 MRAM released their last earnings report and the results did showcase as I think common with a lot of tech companies, a slowdown in the sales. The product sales went from $14.5 million in Q3 FY2022 to $13.5 million, a 7% decrease. Using the nine months through for the year MRAM is up by $300 000. I think that FY2023 will show a slightly low single-digit improvement YoY, which compared to many other tech companies is a very strong achievement. A primary cause for the lower demand I think comes from higher interest rates which is putting pressure on company spending. Operating expenses did remain high as a large increase came from the general and administrative section, growing over $2 million YoY for the last 9 months. I think that marinating a strong growth plan along with proper management of hiring will be key to maintaining a positive bottom line for MRAM.

{kind=link}

When it came to the bottom line for MRAM they saw a YoY EPS growth of roughly 30%, which was helped by an increase in their incomes, up from $69 000 last year, to nearly half a million instead. Dilution has continued but is now at a much slower rate than some years ago, although still something that I am monitoring. If it stops I think the valuation of the company could rise as investors are getting more value over the long term.

{kind=link}

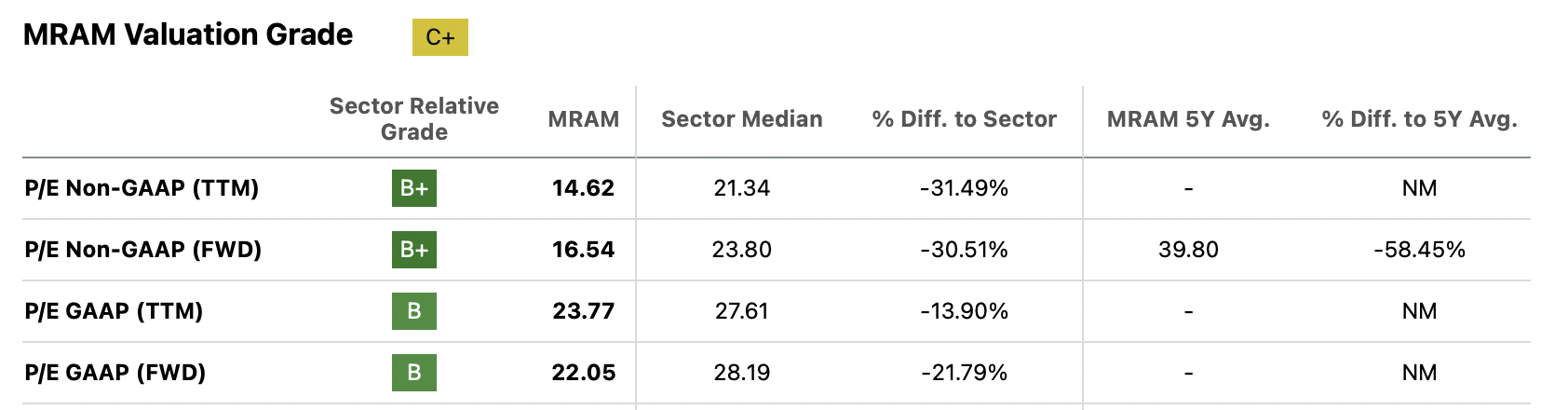

On the valuation part of MRAM, I think it offers some pretty good upside right now. In the last few months, the stock price has consolidated after running up very quickly between March and July. I think the markets are looking toward how the interest rates might land this year and for 2025 as well. My bet is on a slight cut in the second half of the year, with more aggressive cuts coming in 2025. With the p/e at an FWD multiple of 16, I think given the market opportunities and improvements that MRAM has made in recent years a 21x multiple is more fair right now. The multiple of 39 I think is too high, and frankly a multiple I would extremely rarely pay for a business. I think that FY2023 will end with an EPS of around $0.51, and 2024 to show a 10% YoY growth rate. This leaves an EPS of $0.56 for FY2024, and a 21x multiple leaves a price target of $11.7 for MRAM. With an upside of 32%, I am rating the business a buy. On a 12-month basis that is a solid return to potentially get. I think the results will be heavily dedicated to market conditions, and for them to be a favorable focus for MRAM. A more positive market environment would come from rate cuts as it frees up capital for business and investments will likely increase as a result.

Risks

MRAM currently grapples with the competitive nature of its markets, which pose a significant challenge. Operating in this sector demands substantial capital, with a considerable portion allocated to R&D activities. The risk emerges if larger players, such as Intel Corporation ( INTC ), decide to intensify their investments in this field, potentially creating headwinds for MRAM. INTC already has a small presence in this market, which also opens up the potential of a buyout too, which would be a positive perhaps. INTC is a far larger company with a market cap of nearly $200 billion. MRAM is a drop in the ocean compared to that, and therefore a potential buyout target as well. I won't dig any deeper into that since I partly also think the markets that MRAM operates in have to develop a little more until M&A activity starts to happen.

{kind=link}

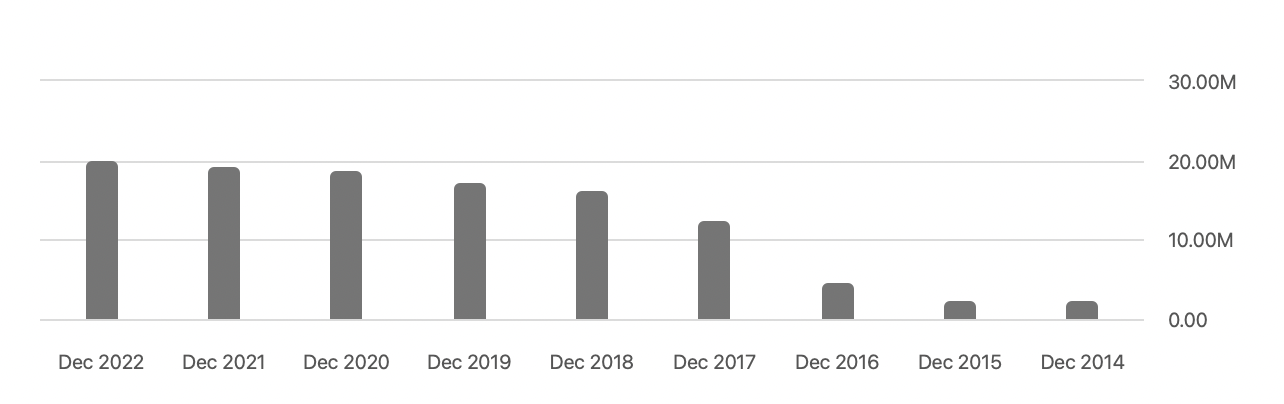

Fueling the growth that MRAM has had over the last several years seems to have been the dilution of shares. The company quite rapidly diluted shareholders between 2015 and 2018 as seen above here. It seems to have paid off as the bottom line has become constantly positive over the past few years, likely fueled as well by higher demand. But I want to highlight that dilution is a risk. If MRAM can't organically grow its top and bottom line without investments from dilution then there might be less value here than I initially thought, posing a risk ultimately.

Final Words

I am covering MRAM for the first time and I am excited to be doing so by rating it a buy as well. The company has over the past few years managed to achieve a positive bottom line, and with no debt, is in a great position to continue growing. The market they are in is beginning to be more competitive and I think proper expense control will be the factor that leads to a higher valuation for MRAM. I set out a PT of $11.7 for next year and with an over 30% upside it means I am rating the company a buy now as I initiative converge on the stock.

For further details see:

Everspin Technologies: Fair Price Point With An Exciting Market Opportunity