MRAM - Everspin Technologies Should Benefit From The Fast-Growing MRAM Market

2023-05-12 17:39:09 ET

Summary

- MRAM chips are becoming more attractive than the projections suggest, and the company should benefit from that.

- The market is set to grow at high rates for the next decade.

- The company is very strong financially and is one of the leading players in the MRAM space.

- The company is fairly priced right now and a good buy for the long run.

Investment Thesis

In this article, I will explore the potential of Everspin Technologies' ( MRAM ) growth potential and wider adoption of MRAM technology in the market. I believe that MRAM technology will have a good growth trajectory in the future, with many different large players looking into adopting it for their products. I argue that the company is a good buy at these levels to reward shareholders handsomely in the future, however, I would expect further headwinds in the short term due to the lack of love for the semiconductor sector and overall negative macroeconomic outlook.

Briefly on the Company and Q1 Results

Everspin develops and is a pioneer of Magnetoresistive Random Access Memory ('MRAM') technology. MRAM is non-volatile, which means that the content is not lost with loss of power. MRAM is the same as DRAM or SRAM which loses no data and MRAM uses magnetic states instead of electrical charges that DRAM uses. MRAM combines the high speed of SRAM and the high density of DRAM. The company provides many different customers in different markets such as industrial, medical, automotive, and data centers.

Their portfolio consists of mainly two products, Toggle MRAM and Spin-transfer Torque MRAM (STT-MRAM).

The company recently reported Q1 results, which beat consensus estimates on revenues and EPS. The company has managed to turn itself around and has been profitable for the last 8 quarters now, which seems like the company has managed to turn the ship around and is looking to continue this going forward.

Gross margins also saw an expansion compared to the previous quarter by around 540bps, while on a y-o-y basis, the margins are slightly lower by 120bps.

MRAM Adoption and Outlook

One of the big reasons that MRAM tech hasn't exploded in popularity is that it was still very expensive to produce, and the memory density wasn't good enough compared to other products like DRAM and Flash. Cloud-based data servers require 1 Gb of storage to store data, and for the longest time, the largest MRAM chip was 256Mb. That has changed over time and Everspin launched the world's first 1 Gb STT-MRAM product .

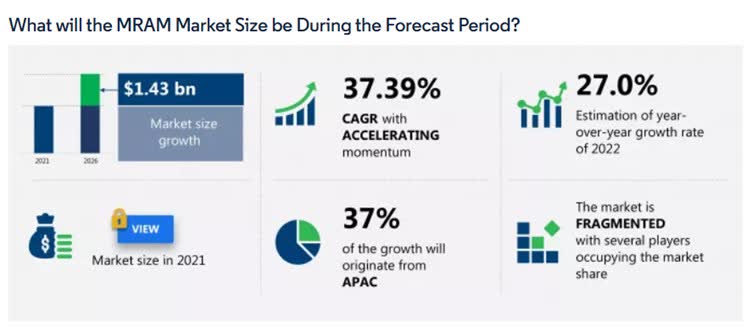

The growth of this market seems to be outstanding in the coming years. It is projected to grow at around 37% CAGR from '21 to '26 . It seems like MRAM is becoming more widely accepted as the benefits of using 50% less power to run may be starting to outweigh the costs. In the same report, it says that Apple ( AAPL ) is interested in MRAM technology for their future phones. Mobile phones are a huge market worldwide, and even though the company may not be specializing in that industry yet, it still may expand later on.

In the latest quarter, the primary region that the company receives the most revenue from is APAC, which is predicted to have around 37% growth of the total projected growth of MRAM, so this is very positive for the company. It's also noteworthy that the EMEA region's revenues doubled from the same time last year, which suggests the demand is strong worldwide.

{kind=link}

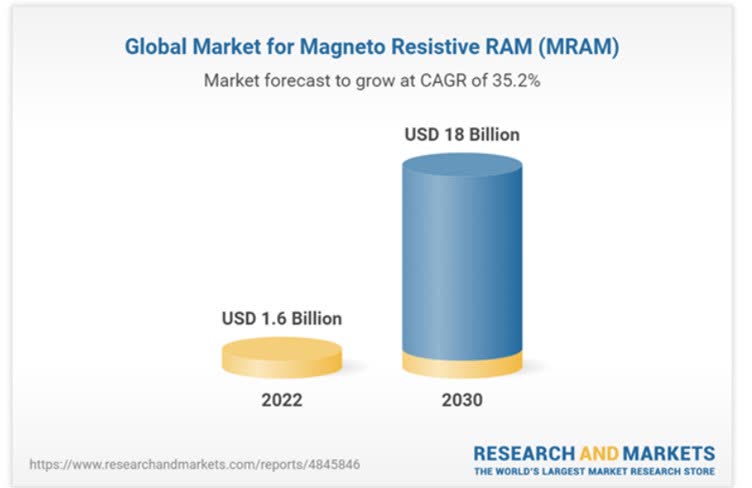

Another analysis puts MRAM CAGR for the next 8 years at 35.2% . Needless to say, many experts are predicting outstanding growth of MRAM technology adoption in the products, and Everspin Technologies is always cited as one of the key players that will benefit greatly in the future.

{kind=link}

In the short term, however, there will be some negative sentiment floating around in the semiconductor sector. The inventory build-up will be a challenge for the remainder of the year and early '24. I don't focus on short-term noise as I am looking for a company that will deliver outstanding results over the long haul, and I believe Everspin is one of them.

Financials

It seems like there is a bright future for Everspin, now let's look at the company itself.

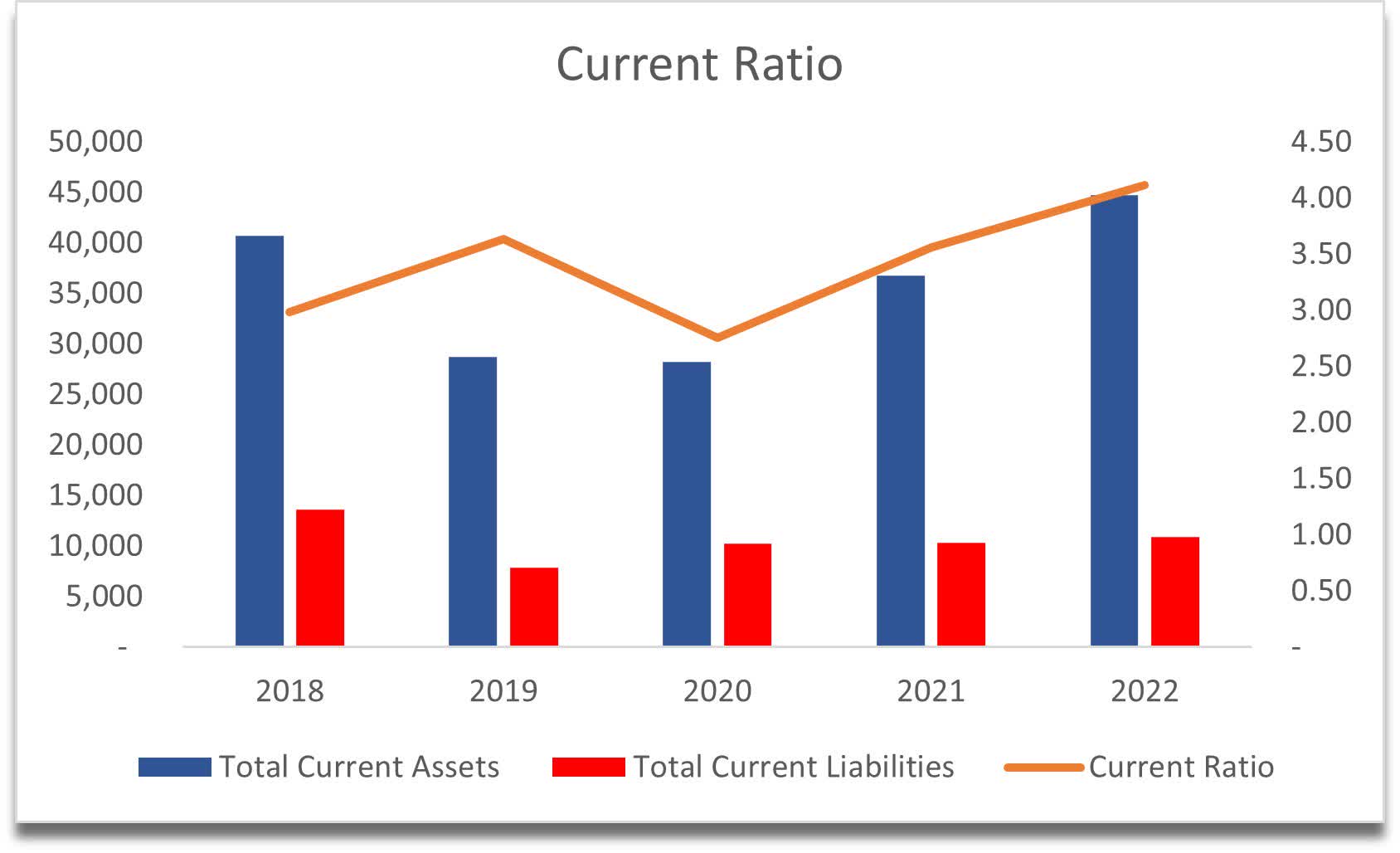

The company has seen quite a turnaround in recent years in terms of liquidity, profitability, and efficiency. The company had around $27m in cash at the end of FY22 and around $2.6m in short-term debt, while having no more long-term debt as of the first quarter of '23, the management was very pleased that the company became completely debt-free. It's very admirable that the management prioritized paying off their debt, which puts the company in a much stronger position to weather any sort of economic downturn that we are going to experience in the next 6 to who knows how many months.

The company is much more flexible without the debt weighing it down. The company's current ratio is very healthy too, standing at around 4 at the end of FY22, and 6.7 at the end of Q1 '23. The company is able to pay off its short-term obligations 6 times over. It is safe to say the company has no liquidity issues.

{kind=link}

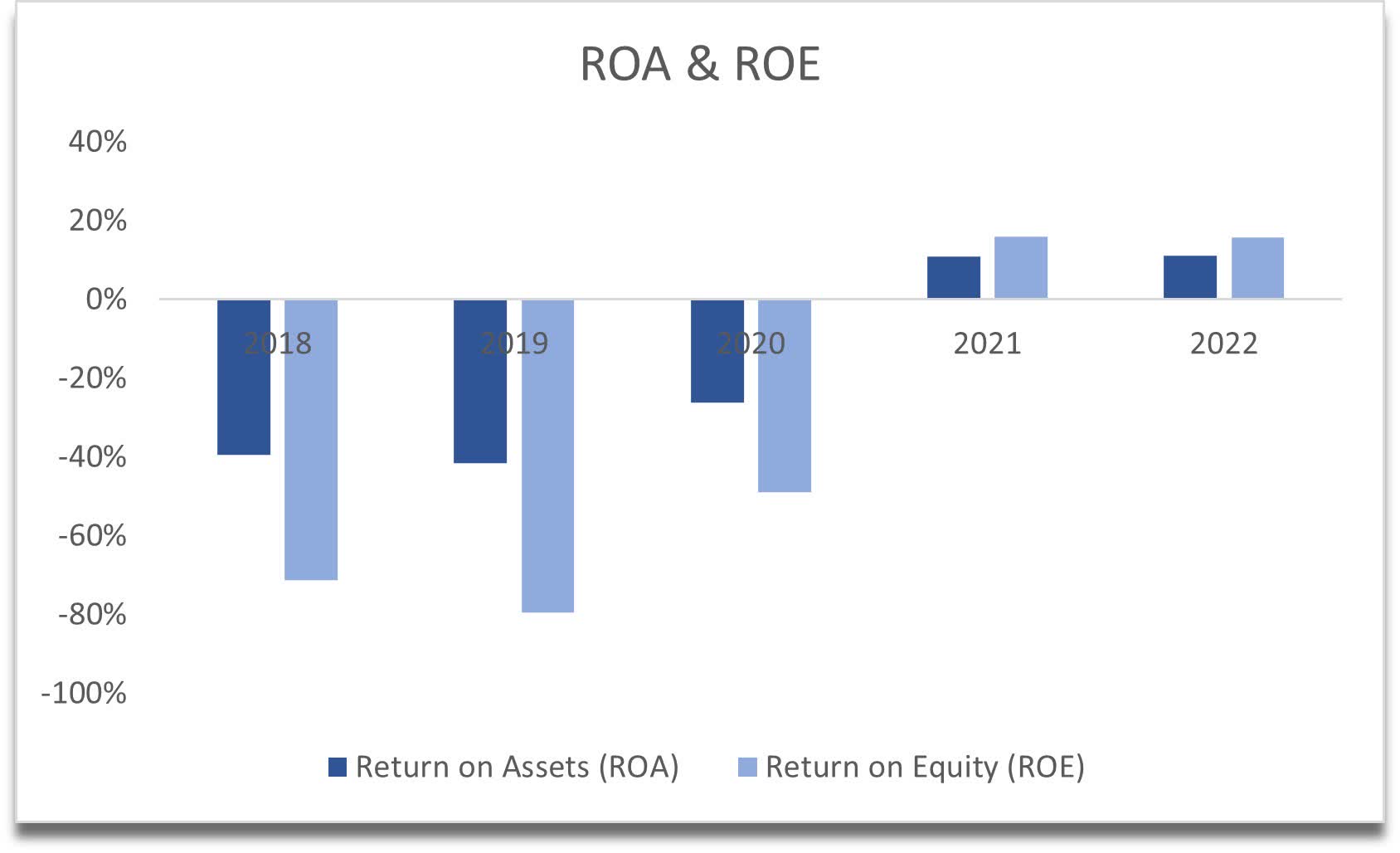

In terms of profitability and efficiency, the company has shown a nice turnaround story in recent years. The company has become much more efficient and profitable, which will reward shareholders in the future if they can keep it up. ROA and ROE have well turned into positives and are well above my minimum thresholds of 5% for ROA and 10% for ROE. ROA is 11% while ROE is 16% at the end of FY22.

{kind=link}

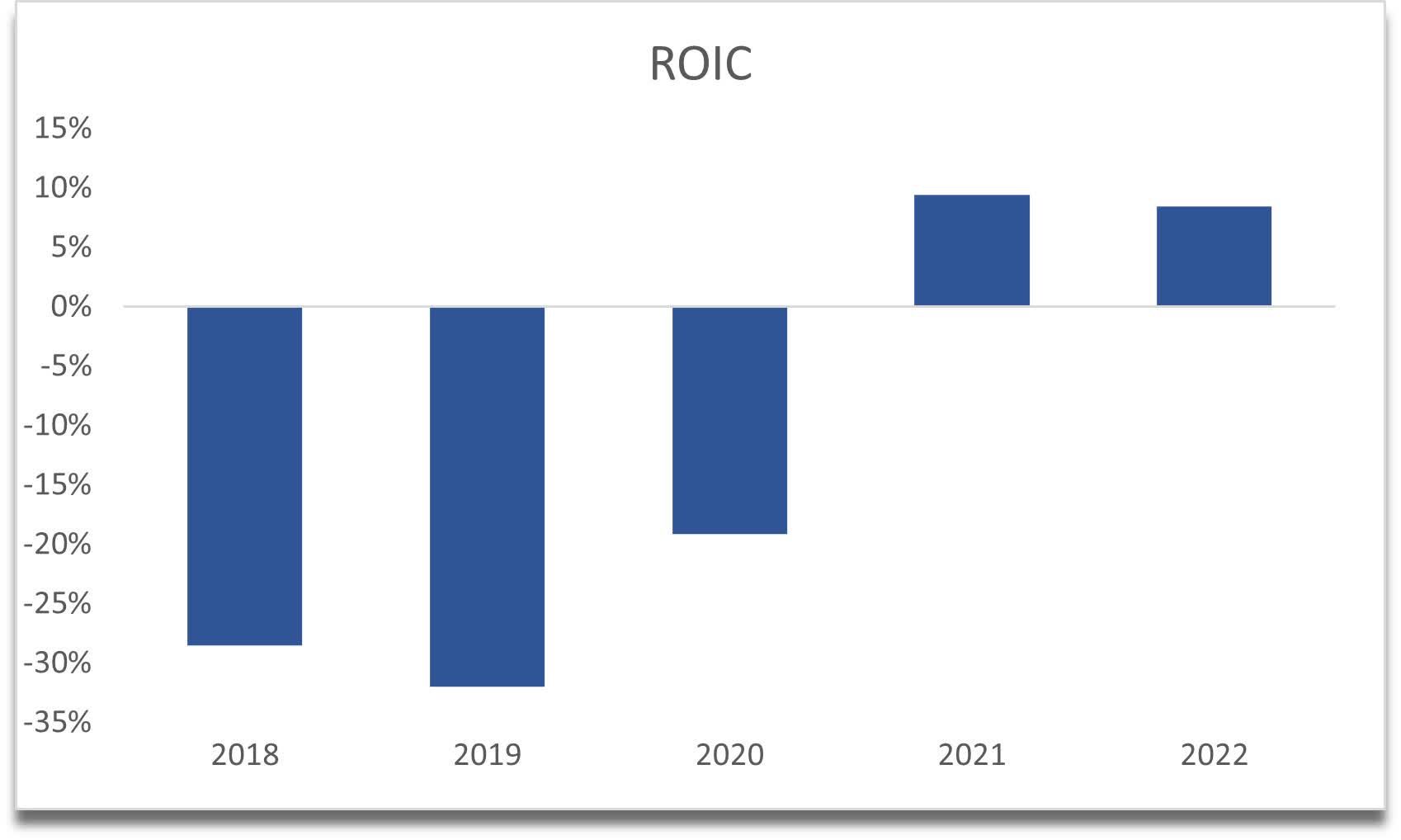

The same story can be said of ROIC. It's not the greatest return, but when looking back at where the company used to be, it is quite an improvement. I would expect that the company will achieve a better moat and competitive advantages with time as the industry grows more attractive and technology becomes more cost-efficient, which will drive up future profit margins.

{kind=link}

Overall, the financials have been very good in recent years. If I was covering the company in 2020, I would have stopped right there and not gone any further, as I like to invest in companies that have turned around or have been operating profitably for years. The balance sheet of Everspin is very strong and that will play a huge role in the company's success in the future.

Valuation

I decided not to be too overly optimistic about MRAM's growth in the future, as I would rather be on the safer side by being more conservative, yet still reasonable.

For the base case, for '23 I went with -5% revenue growth because of the negative sentiment towards the sector and macroeconomic outlook. For '24 I assumed the company would see a good bounce in demand of around 22% which I will linearly grow down to 5% by '32, giving me a growth in revenues from around $57m in '23 to $176m by '32, which is around 12% CAGR for the next 10 years.

For the optimistic case, CAGR is around 14%, while for the conservative case, it is around 10%. I believe these numbers are achievable for such a small company as Everspin which is one of the key players in MRAM production.

In terms of margins, I also implemented improvements of 200bps in gross and operating margins, which I believe is still very conservative, because the company managed to go from very negative numbers in the past to acceptable margins right now in just two years.

On top of my assumptions, I will also add a 25% margin of safety, which is the lowest I add to any company that has a really strong balance sheet.

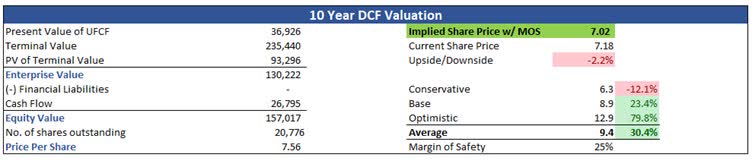

With that said, the company's intrinsic value is $7.02 a share, implying the company is trading at a fair price right now.

{kind=link}

Closing Comments

I believe my assumptions are on the conservative side still and the company is a good buy at this price and will deliver good returns for shareholders. What I will do in this situation is be a little bit more patient before jumping into an investment because of the aforementioned lack of love for the semiconductor sector and negative macroeconomic sentiment, which will bring further volatility to the markets and may present an even better risk/reward ratio for the patient investor.

The company already presents a good risk/reward ratio in my opinion, and I wouldn't be opposed to starting a small position right now and dollar cost average when and if it drops further. The future seems to be bright for MRAM technology and if it does come true the company will be in the forefront and will manage to capture a big piece of the market share in my view.

For further details see:

Everspin Technologies Should Benefit From The Fast-Growing MRAM Market