EVTC - Evertec: A Stock Worth Adding To My Watchlist

Summary

- Evertec's first-hand knowledge of the Latin American/ Caribbean markets gives it an inherent competitive advantage against its peers.

- Popular has been a significant part of Evertec's growth process.

- Evertec gave an EPS guidance of $2.53 to $2.64 for FY 2023 and revenue guidance range of $638 million to $647 million.

Evertec, Inc. (EVTC) reported Q4 2022 revenues of $161.79 million representing an increase of 4.22% (Y/Y) beating estimates by $6.74 million. It matched EPS estimates at $0.65 indicating a surge of 62.5% (QoQ). There was a 5% (Y/Y) increase in annual revenue at $618 million, results which the company intimated exceeded its expectations. These were strong earnings considering the market headwinds caused by the Federal Funds rate adjustments from the second half of 2022, inflation, higher price of gas, and natural catastrophes such as Hurricane Fiona.

Thesis

Evertec expects a strengthened partnership with Puerto Rican financial powerhouse, Popular, Inc. (BPOP) especially the Master Services Agreement ((MSA)) in 2023. This partnership will see the company grow its merchant-acquiring business into the greater Latin American region. The company also expects to limit operating expenses to a single-digit rate. This reduction will offset investments and support the high revenue/ earnings guidance set for 2023.

Popular-Evertec Partnership

First off, the relationship between Evertec and Popular has been a significant part of the company's growth process. In the year ending on December 31, 2022, Evertec attributed 39% of its revenue (about $240 million) from Popular through its subsidiary, Banco Popular de Puerto Rico. This revenue concentration in my view makes the Master Service Agreement a special client contract. Evertec's MSA contract with Popular is expected to end in 2028, and it is apparent that Evertec intends to capitalize on this agreement.

Under the MSA terms, Popular agreed on various services from Evertec including the Merchant Acquiring Service (A&R ISO Agreement) and ATH (Interbank) network whose 5-year extension was announced in Q4 2022.

Back in February 2022, Popular (through its subsidiary, Banco Popular) acquired about 4.6 million shares of Evertec for a total consideration of $196.6 million valued at $42.84 (at the time). The share price has since declined 14.24%. Popular's purchase at the time was not just to make Evertec, its subsidiary, but mainly to improve its in-house technology as well as its customers' experiences. This deal included strengthening Banco Popular's payments business by integrating a revenue-sharing structure of the bank. This incorporation involved Evertec's merchant acquiring service.

On August 15, 2022, Popular divested its Evertec shares at a reduced price of $169 million even as it realized a 40.4% (QoQ) growth in total revenue to $957.2 million as of Q3 2022. These were recorded earnings for Popular since it later realized a 30.16% (QoQ) revenue decrease in Q4 2022 to $668.5 million. What we can see here is that the fintech assets purchased by Popular had a direct impact on the company's revenue generation mechanism.

Popular's returning of Evertec's shares means that the latter is no longer a subsidiary. In that regard, Evertec will have increased flexibility in pursuing other acquisitions in the IT-fintech space. Recent years have seen consumers in the Americas and the world over, accelerate the shift to a cashless payments system. The heightened demand for omnichannel payment systems

Market Growth Opportunities

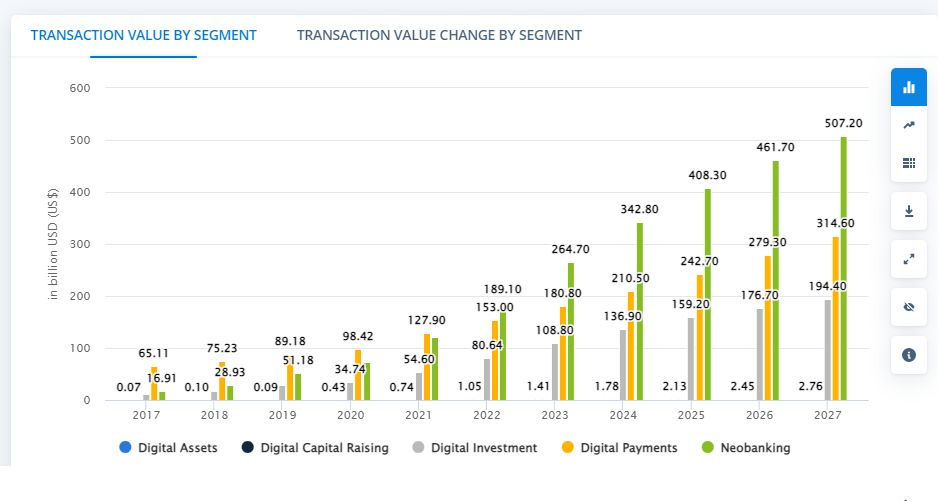

Neo-banking in Latin America is expected to take up the largest chunk of transactional value in 2023 at $264.70 billion and revenue growth of 29.4% by 2024. In turn, the number of digital/ cashless payment users in the region is forecast to reach 257.50 million by 2027. In 2020, more than $7 trillion was transacted by American citizens using cashless payment systems including debit cards. Transactions conducted through Automated clearing house (ACH) transfers such as paycheck direct deposits (PDDs), Zelle, and Venmo among others hit a high of $62 trillion.

{kind=link}

As seen above, the level of digital/ cashless payment adoption is on a rampant increase globally. Several reasons have been cited for this situation. They include and are not limited to card rewards, improved security, and peer-to-peer transactions. Additionally, the world is quickly adopting the use of alternative payment methods such as QR codes, digital wallets, and instant account-to-account payments. According to the World Payment Report of 2022, non-cash transaction volumes in Latin America from 2016 to 2021 grew 62% to 65.9 billion. From 2021 to 2026, a non-cash transaction in this region is expected to reach $31.6 billion growing at a CAGR of 12.8%.

Evertec's first-hand knowledge of the Latin American/ Caribbean markets gives it an inherent competitive advantage against its peers. I am looking at its financial technology background, geographical coverage, and ease of penetrating new markets. Evertec serves 26 countries from its headquarters in San Juan, Puerto Rico offering merchant acquiring, processing of payments, and other business solutions. Evertec has invested and is continually expanding its digital business solutions. It has an e-commerce gateway known as PlacetoPay, ATH Movil/ ATH Business (wallet) and its issuing and acquiring processing platform known as PayStudio.

Expected Growth in the future

In merchant acquiring, Evertec expects a mid-single-digit rate surge in 2023. The main drivers of this increase will be accommodative price initiatives, a balanced merchant spread, and the incorporation of high-volume merchants. The continued growth and adoption of ATH Movil, increased POS transactions, Popular's services CPI effect, and other business solutions.

Revenue from Payments Puerto Rico increased by 14% (YoY) due to the rise in POS transactions in FY 2022. Over 1.8 billion transactions are processed by Evertec annually and the company is not slowing down. Still, on annual basis, the company stated that it manages more than 4,100 automatic teller machines (ATMs), and more than 104,000 POS payment terminals in Latin America. According to me, this portfolio is attractive considering it only went public in 2013 at a valuation of $1.5 billion.

Risks to be considered

At the moment, Evertec relies on its relationship with Popular with the latter even contributing to more than a third of its revenues in FY 2022. This reliance may be detrimental to the company if Popular should terminate or pull out of the MSA contract or decline an extension. The company admitted that its adjusted EBITDA declined 9% (YoY) to $270 million due to the effect of Popular transaction loss. Revenue from business solutions also fell 9% (YoY) due to the sale of assets sold in 2022 from Popular's transaction.

As a payment processing company, Evertec is not immune to inflationary pressures. Puerto Rico's inflation rate as of December 2022 stood at 6%. A further increase in this rate will force the company to increase card processing costs as normal product/ service prices increase. While the company indicated that it wanted to lower its expenses to a single-digit rate, its cost of revenues is already at its quarterly record high of $77.4 million. In addition, Evertec's net income declined 79.17% (QoQ) from a high of $137.9 million in Q3 2022 to $28.7 million in Q4 2022.

On the bright side, Evertec gave an EPS guidance of $2.53 to $2.64 for FY 2023 against the consensus estimate of $2.58. It also provided the revenue guidance range of $638 million to $647 million.

Bottom Line

In my view, Evertec provides a share of the Latin American economy. The company pushed through macroeconomic headwinds such as inflation, interest rate rises and other factors to deliver solid FY 2022 results. Evertec has a diversified product offering with payment processing solutions. The Puerto Rican business environment has also provided growth for the company with stable economic activity expected in 2023. However, the reliance on Popular as a major revenue generator for the company poses a risk for the company especially if the current MSA is discontinued. Still, I believe that this stock is worth placing on my watch list and I am recommending a hold rating for the stock.

For further details see:

Evertec: A Stock Worth Adding To My Watchlist