EVF - EVF: Be Patient And Wait For A Good Entry

2023-04-04 12:02:23 ET

Summary

- EVF provides high current income from a portfolio of senior loans.

- The fund pays a generous 9.4% trailing distribution yield.

- However, with the fund only earning 4-5% p.a. over the long-term, the EVF fund shows characteristics of being an amortizing 'return of principal' fund.

- I believe EVF, like most credit CEFs, is a trading vehicle that investors should buy when economic conditions are poor and credit spreads are elevated.

- Due to their mean reverting nature, when credit spreads are elevated, forward returns are usually above average.

The Eaton Vance Senior Income Trust ( EVF ) is a closed-end fund that provides exposure to floating rate senior loans. The fund pays a generous 9.4% trailing 12 month distribution yield.

However, I don't think the EVF fund is a buy and hold investment, as it shows characteristics of being an amortizing 'return of principal' fund. The EVF fund only earns 4-5% long-term average annual returns but has an 8%+ of NAV distribution yield. This causes the NAV to amortize at a 2% p.a. CAGR.

Looking forward, I am concerned that the recent regional banking crisis may turn into a wider credit crunch that can push the U.S. economy into a recession. This may spike credit spreads and cause loan prices to fall.

However, I would be a buyer of EVF in that scenario, as credit spreads are a mean reverting asset and large spikes often lead to above average forward returns.

Fund Overview

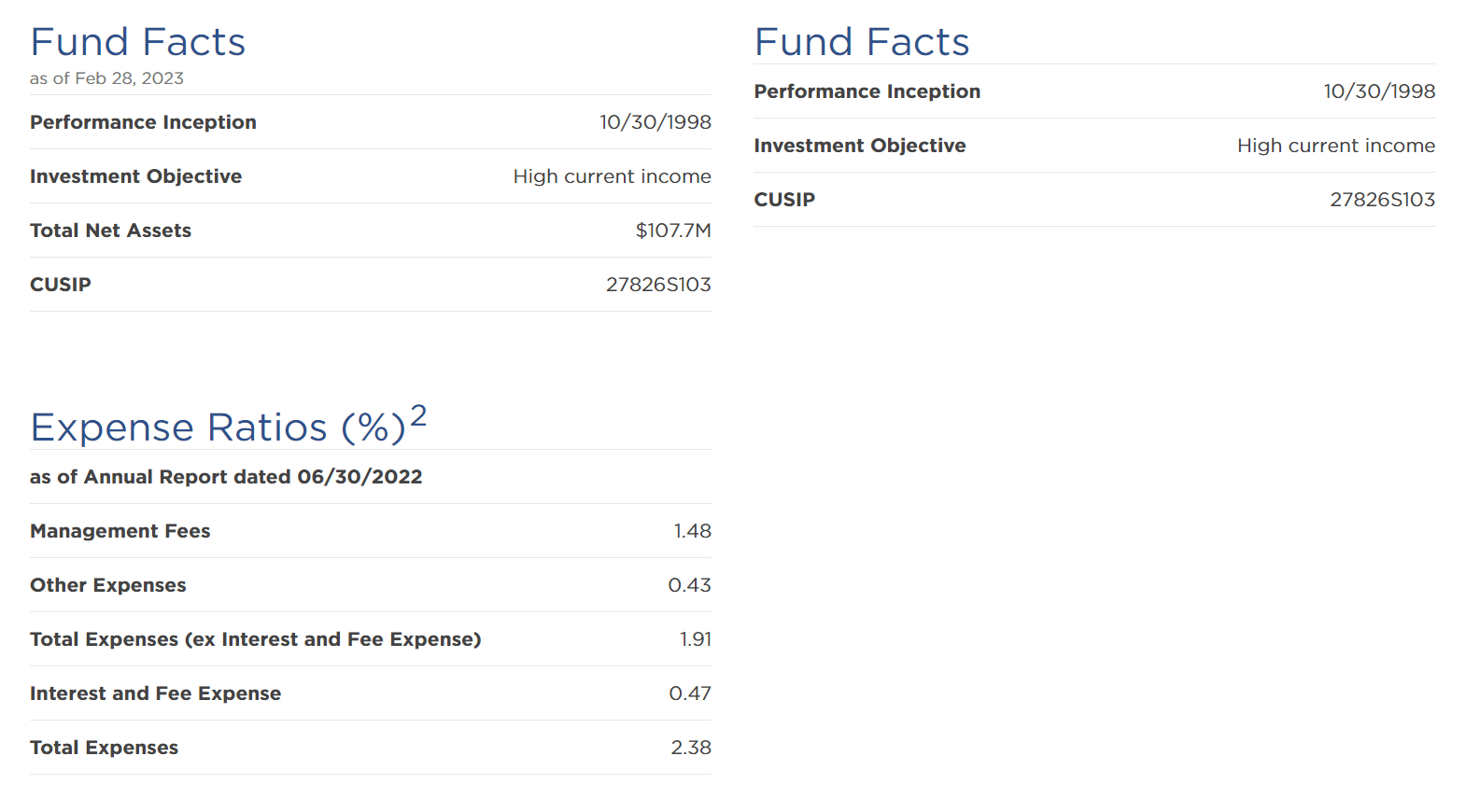

The Eaton Vance Senior Income Trust is a closed-end fund ("CEF") that provides high current income from the floating rate senior loan market. Floating rate loans have low duration risk and may help investors lower the overall duration risk of their portfolios. The EVF fund may use leverage to enhance returns. As of December 31, 2022, the EVF fund had $159 million in gross investments against $103 million in net assets for 35% effective leverage.

The EVF fund charges a 2.38% total expense ratio (Figure 1).

{kind=link}

Portfolio Holdings

In order to generate high income, the EVF fund primarily holds non-investment grade ("junk") senior floating rate loans, with 21% of the portfolio BB-rated, 64% of the portfolio B-rated, and 14% of the portfolio rated below CCC or unrated (Figure 2).

{kind=link}

Returns

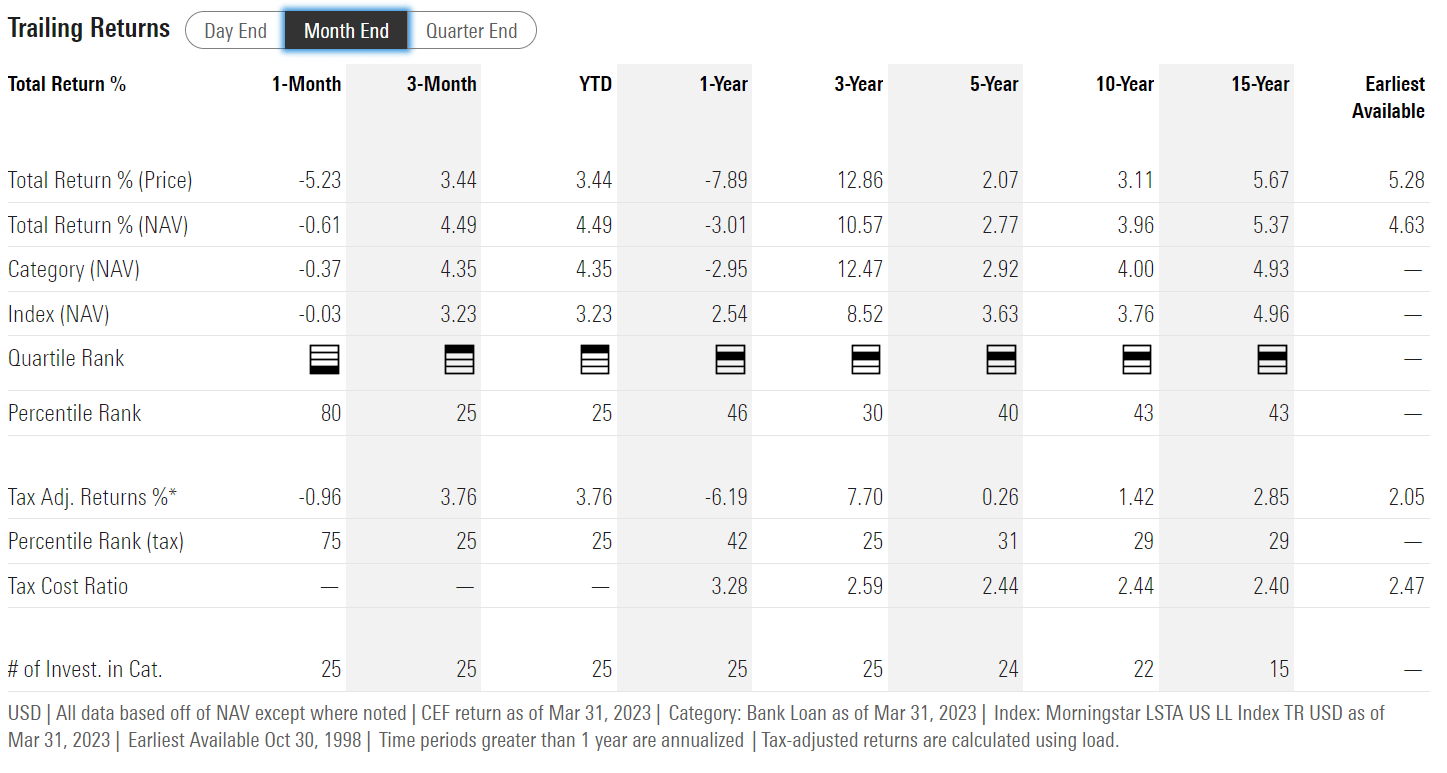

Figure 3 shows the historical returns of the EVF fund. Overall, the fund has delivered modest returns, with 3/5/10/15Yr average annual returns of 10.6%/2.8%/4.0%/5.4% respectively to March 31, 2023.

{kind=link}

Investors should note that the 3-Yr average annual return figure is skewed high because the starting time period was March 2020, which was at the start of the COVID-pandemic when asset prices collapsed and credit spreads blew out. EVF's 10Yr and 15Yr average annual returns of 4.0% and 5.4% are more representative of what can be earned from a floating rate senior loan strategy.

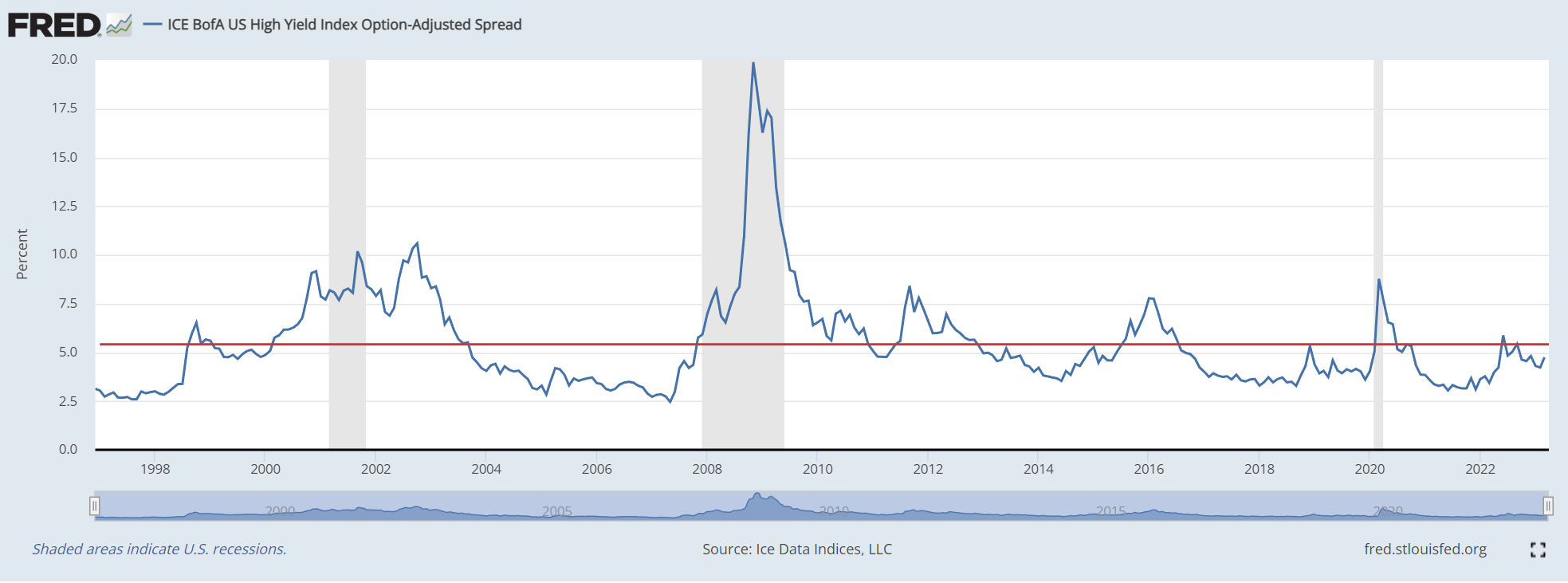

This is because absent interest rate duration exposure, what senior loans offer investors is basically the high yield credit spread, which averages ~5% over the long-run (Figure 4).

Figure 4 - HY credit spreads average ~5% over the long-term (St. Louis Fed)

{kind=link}

Leverage can enhance fund returns, however, credit losses (i.e. defaults) and fees (management and leverage fees) will decrease returns. Overall, investors should expect to earn mid-single-digit ("MSD") annual returns over a cycle.

Distribution & Yield

The EVF fund pays a monthly distribution with a trailing 12 month distribution of $0.50 or 9.4% yield. On NAV, EVF's trailing distribution yields 8.3%.

Although the EVF fund pays an attractive 8.3% of NAV distribution yield, I worry about the sustainability of the fund's distribution. As mentioned above, a properly structured investment fund focusing on senior loans should earn MSD returns through a cycle, yet the EVF fund pays an 8%+ of NAV distribution.

Fund's that do not earn their distributions are called 'return of principal' funds, according to an Eaton Vance whitepaper titled 'Return of Capital Distributions Demystified'. 'Return of principal' funds are problematic because these funds must liquidate NAV in order to fund their (earnings - distribution) shortfall. This reduces income earning assets to fund future distributions, exacerbating the problem.

A classic sign of amortizing 'return of principal' funds is a long-term declining NAV, which unfortunately applies to the EVF fund (Figure 5).

Figure 5 - EVF has a long-term amortizing NAV (morningstar.com)

{kind=link}

Since inception, EVF's NAV has shrunk by 40% from $10.00 to $6.05, or a -2% CAGR. This suggests the EVF fund has been paying more than it earns by an average of 2% p.a.

Economic Weakness Is A Risk / Opportunity To EVF

While investors holding the EVF fund through a cycle can expect to earn MSD average annual returns that correspond to the average high yield credit spread, changes in economic conditions can impact the level of credit spreads and cause large mark to market ("MTM") losses. For example, from figure 6 above, we can see EVF's NAV plunged in early 2020 due to the COVID-pandemic. This was because high yield credit spreads spiked to over 8%, as shown in figure 4 above.

Although credit markets remain benign at the moment, stress is building with the recent regional banking crisis set to tighten bank lending standards and credit conditions.

If the regional banking crisis evolves into a credit crunch and pushes the U.S. economy into a recession, then we should see a spike in high yield credit spreads and sharp MTM drawdowns on EVF.

At the same time, this scenario could set up a perfect opportunity to buy the EVF fund and other credit funds, as the mean reverting nature of credit spreads mean that eventually credit spreads will normalize and investors will earn above average forward returns. Empirically, this is the reason behind EVF's 3Yr average annual return of 10.6%, which is far higher than the asset class's expected return, as the beginning measurement period was the March 2020 lows.

Conclusion

The EVF fund is a closed-end fund that provides exposure to floating rate senior loans. The fund pays a generous 9.4% trailing 12 month distribution yield. However, the EVF fund shows characteristics of being an amortizing 'return of principal' fund, as its long-term average annual returns are only 4-5%, but it pays an 8%+ distribution. This causes the fund's NAV to amortize at a 2% CAGR.

Looking forward, I am concerned that the recent regional banking crisis may morph into a wider credit crunch that can push the U.S. economy into a recession. This could cause credit spreads to spike and loan prices to fall. However, if that scenario occurs, I would turn from cautious to bullish on credit products like the EVF fund, since credit spreads are mean reverting and a large spike often leads to above average forward returns.

For further details see:

EVF: Be Patient And Wait For A Good Entry