EVG - EVG: Improving Income Generation Is Positive But Still Not Attractively Priced

2023-09-26 13:58:04 ET

Summary

- Eaton Vance Short Duration Diversified Income Fund is a multi-sector bond fund that incorporates various exposures of floating and fixed rates within its portfolio.

- The fund has a flexible investment policy and aims to provide a high level of current income while also seeking capital appreciation.

- EVG has performed well since our last update, but its discount to net asset value per share is not attractive, leading to a "Hold" rating.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Eaton Vance Short Duration Diversified Income Fund ( EVG ) is a multi-sector income fund. They incorporate various exposures of floating and fixed rates within their portfolio as well as up and down the credit quality spectrum - splitting itself between high investment-grade rated debt and below-investment-grade junk.

This sort of diversification usually lends itself to some advantages and disadvantages. As usual, in all investing, there are pros and cons. The basic idea with higher diversification is that while some investments might perform quite poorly, there will be investments that perform better to offset those that act more poorly.

In the middle, you just hope that most of the fixed-income investments here do their job. That is, generate steady interest payments from the underlying securities and, when they mature, receive all your principal back. And then, at the end of the day, you could have a decent performance from your portfolio over time, but you would never really get ahead (or behind).

That's mostly the approach of EVG. At this time, the fund also isn't offering the most attractive discount to its net asset value per share, which has continuously been one area that has kept me from applying a 'Buy' rating to this fund.

The Basics

- 1-Year Z-score: 0.45

- Discount: -2.89%

- Distribution Yield: 9.12%

- Expense Ratio: 1.41%

- Leverage: 19.3%

- Managed Assets: $209.43 million

- Structure: Perpetual

EVG is a relatively simple fund ; they "seek to provide a high level of current income." The secondary objective is to "also seek capital appreciation to the extent consistent with its primary goal of high income."

To do this, their investment policy is rather flexible as well. The fund "will invest at least 25% of its net assets in each of the following three investment categories: [i] senior, secured floating rate loans made to corporate and other business entities, which are typically rated below investment grade; [ii] bank deposits denominated in foreign currencies, debt obligations of foreign governmental and corporate issuers, including emerging market issuers, which are denominated in foreign currencies or U.S. dollars, and positions in foreign currencies; and [iii] mortgage-backed securities that are issued, backed or otherwise guaranteed by the U.S. Government or its agencies or instrumentalities or that are issued by private issuers."

The fund had deleveraged as of their latest semi-annual report . They went from $32 million in borrowings down to $27 million. That was a trend that we saw in our previous update with the fund reducing leverage. However, they have since ramped up borrowings again by the end of Q2 2023 to around $65.25 million or a total leverage ratio of 19.3%

EVG Fund Facts (Eaton Vance)

That being said, this is still a fairly modest amount of leverage relative to some peers. Being more lightly leveraged could also be seen as a positive in this current environment. The Fed is raising interest rates, and that's usually ended with a thud in the economy and increased defaults. Of course, the fund is still leveraged, and that means greater volatility with moves in both the upside and downside.

Swinging To A 'Hold' Again

Since the last time we covered this fund earlier in 2023, the fund has performed quite well. It has topped the S&P 500's performance on a total return basis. While that isn't going to be the primary benchmark, it can provide us some context of what we are seeing from EVG.

EVG Performance Since Prior Update (Seeking Alpha)

However, I have to admit there was a time during this period that saw the fund's discount widen substantially. As we take another updated look today, it's actually swung from being a decently discounted fund a few months back to being a 'Hold.'

The discount more recently sharply closed, with the fund's NAV dropping considerably while the fund's share price moved higher.

Ycharts

Over the long term, this still represents a level where it is trading well above its longer-term average. We can also see how the latest dip brought us right to this long-term average before climbing its way back to this more narrow discount level.

Ycharts

In looking at the fund's longer-term performance relative to its benchmark, we can see that the fund has performed quite respectably. That is to say, the fund performed poorly, just as most fixed-income annualized historical returns look after 2022's shellacking. That's even considering this fund has a short-duration focus, which recently came in at a rather low 2.2 years. The fund still saw itself off -9.38% on a total NAV return basis through 2022.

However, we saw more promising glimmers of hope in the more recent six-month period as recovery started to take place.

EVG Annualized Performance Relative to Benchmarks (Eaton Vance)

{kind=link}

This comparison is from the fund's semi-annual report for the period ending April 30, 2023. The blended index above is "33.33% Morningstar US Leveraged Loan Index, 33.33% ICE BofA U.S. Mortgage-Backed Securities Index and 33.34% J.P. Morgan EMBI Global Diversified Spread Index, rebalanced monthly."

Through the end of August 2023, the fund's total NAV return comes in at 7.12%, so 2023 has still been a fairly decent year for the fund.

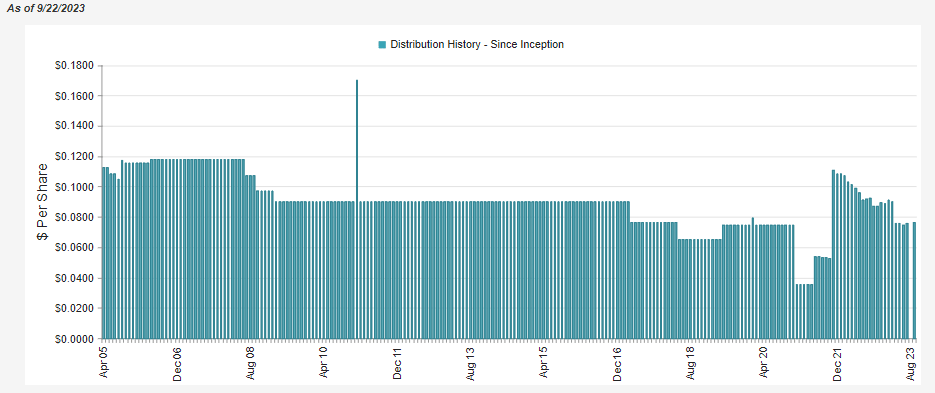

Managed 8.5% Distribution

The fund has a long history and has more recently been changing its distribution policy. This was brought about as Eaton Vance was bought out by Morgan Stanley and some activist pressure to make the fund's distribution more appealing. They had switched to a 10% managed distribution plan as part of the condition for approval for the merger.

However, they have then switched it down to an 8.5% managed distribution based on the NAV. It wasn't a massive change, but it would mean a little bit less erosion would be happening in the fund than previously. The way this managed distribution policy is implemented is the less popular monthly adjustments rather than holding steady for a year and adjusting the following year.

{kind=link}

Based on historical performance, neither of these plans was achievable in the past, but that generally still allows for a fund to see its discount close and push to a premium. At an 8.5% managed distribution policy, that's still a high hurdle to climb, but with higher rates for longer, it may not be impossible to achieve going forward.

With the fund's performance starting to rebound this year from the recovery in the fixed-income market after 2022, the fund's distribution has been relatively more stable this year than previously.

At the end of their last semi-annual report, we see that net investment income was starting to move higher. On a per-share basis, we saw NII at $0.559 last year and this year at $0.366 or annualized to $0.732. The NII ratio went from 4.7% to 6.84%, which also reflects the higher total expenses the fund is experiencing due to higher leverage costs. This is an improvement as well; as we noted in our previous update, the fund's NII slid lower as expenses rose and they deleveraged.

{kind=link}

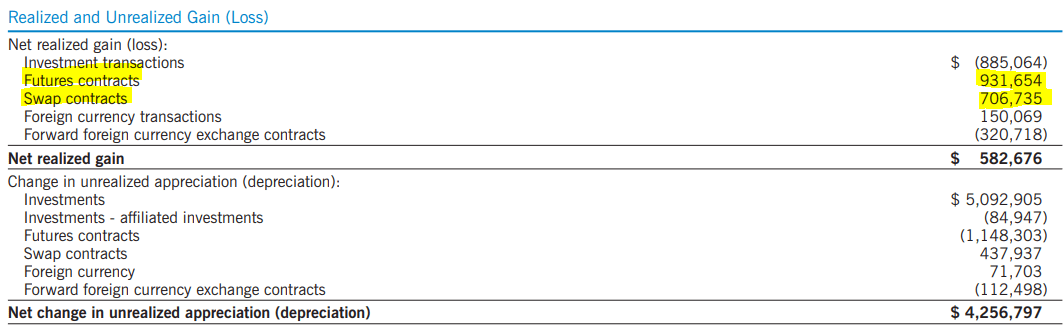

Some of those higher leverage costs were offset in ways that aren't reflected in the fund's NII either. Instead, the futures contracts of going short Treasuries or interest rate swap contracts will show up as appreciation or depreciation, depending on their success. In their last report, they reported some gains in both of these categories, as well as foreign currency transactions.

EVG Realized/Unrealized Gains/Losses (Eaton Vance (highlights from author))

{kind=link}

Despite all that good news, it still means that the payout isn't fully covered by the interest generated in the underlying portfolio. That's often what we'd like to see from a fixed-income fund.

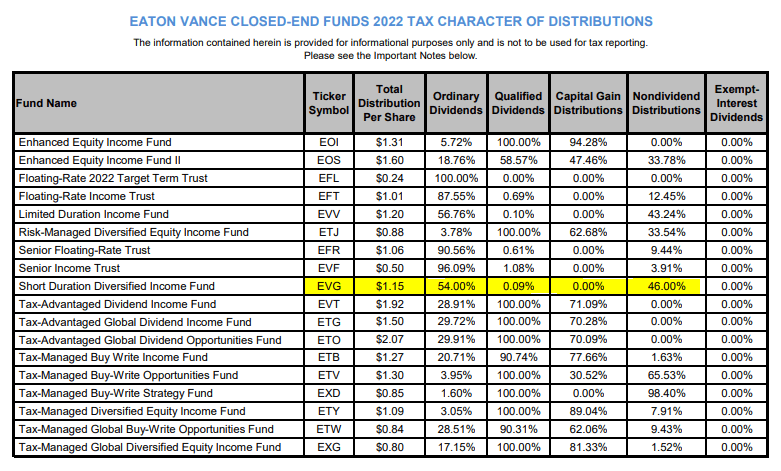

We previously discussed the tax character of the distributions in our prior update. Here's a recap:

With all that being said, it's not too surprising that we would see the fund's distribution classifications show a substantial breakdown to non-dividend distributions (AKA return of capital.)

{kind=link}

EVG's Portfolio

The fund has an incredibly high turnover. Perhaps that's not too surprising, given the multi-sector approach as well as their flexible use of leverage. They seem to always be taking leverage up and down frequently.

However, this latest six-month report shows the fund is on pace for the highest turnover in the last six years, coming in at 121%. That puts it on pace for a potential 200%+ turnover. For some context, for the entire 2022 fiscal year, the fund's turnover came to 182%. To be fair, the prior 2021 year had a turnover rate of 76%, and before that, it was at 47%. So the increased activity really came in the last few years.

The fund is most heavily weighted toward senior loans but also carries a significant allocation to mortgage-backed securities. Additionally, I'd mention that this is where the heavier diversification comes in for this fund, as they also carry meaningful exposure to foreign obligations, collateralized loan obligations, high-yield securities, and commercial MBS. This goes back to the fact that they own a little bit of everything, so the performance might not blow you away, but it also shouldn't blow your portfolio's value away, either.

EVG Asset Mix (Eaton Vance)

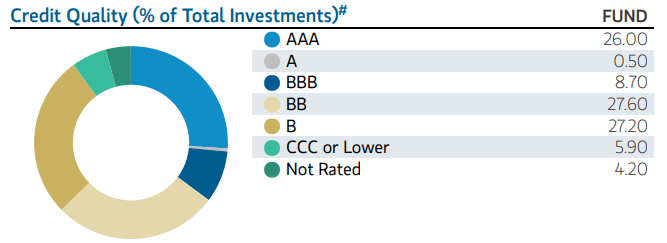

The floating rate exposure presented here is what is really coming in to help the fund; with higher rates and yields, we are seeing the benefit of the increased income generation. The fund's duration comes to a fairly low 2.2 years, even while, at the same time, a sizeable portion of the portfolio is invested in AAA investments. However, note that this allocation was as of the end of the second quarter of 2023 before Fitch downgraded the U.S. in August. The assumption would now be that the AAA should be changed to AA in the next update.

This brings up the safety of the fund by having over a quarter of the fund in the highest rated debt, followed by the overall fund 35.2% allocation to BBB and higher. BBB and higher is considered investment grade. This allocation is quite material as, said another way, over a third of the fund is seen as high quality with a limited chance for default. That could be a benefit if one expects a slowdown heading into 2024 and defaults start ticking higher.

{kind=link}

However, this safety also comes with the idea that these securities aren't likely to generate the highest return or yield for the fund. The highest-rated category is comprised of agency MBS as well as U.S. Treasuries. These yields are moving higher, just as all other fixed-income instruments are, but as of their last semi-annual report, they paid anywhere from about 3 to 9%. After the fund's operating expenses of 1.41%, we'd be looking at the yield to investors of 1.59% to 7.59% on a non-leveraged basis.

Conclusion

Eaton Vance generally offers some solid funds and is considered a decent fund sponsor overall. The rising income generation of the fund's portfolio certainly means it's trending in the right direction. However, with a monthly adjusted distribution policy of 8.5%, which isn't too high, nor is it being covered, I am a bit flabbergasted at how narrow this fund's discount remains. Often, higher yields are chased, but at a sub-10% distribution on the share price, it isn't necessarily in that category.

Still, investors are pushing this closed-end fund to trade at a narrow discount. So that means for me, for now, it would continue to be a fund that I'd be "cautious" on. A discount of between 8-10% could potentially start getting me more interested.

For further details see:

EVG: Improving Income Generation Is Positive, But Still Not Attractively Priced