EVGGF - Evolution AB: Capital Allocation Might Improve Soon

2023-11-14 06:10:24 ET

Summary

- Evolution AB may resume share buybacks due to a new incentive program, low valuation multiples, and the huge cash balance.

- The capital allocation strategy, which has been deficient in recent years, has room to improve.

- The roadmap for 2024 is exciting, with more games released than ever and new studios in Europe and America.

- Margins are improving, but revenues in Europe and North America have been disappointing during the last quarter.

- Despite lowering my fair price, I consider Evolution AB stock to be undervalued by 51% with a fair price of €135.

Note: All currencies are denominated in EUR unless otherwise stated.

Evolution AB (EVVTY) is the market leader in the highly profitable live gaming industry, with a great competitive advantage due to its innovative approach and the best Chief Product Officer in the industry, Todd Haushalter.

For those readers who are not familiar with the company, I'd recommend reviewing my first article where I covered it in detail not long ago, since in this one I will focus on the aspect that I believe there is more room to improve, which is capital allocation.

Evolution AB's capital allocation review

Evolution AB's main way of shifting capital back to owners is through its dividend policy. The company is paying 50% of the previous year's net profits to shareholders through a dividend paid in April each year after the Annual General Meeting.

Source: Author (Data from Evolution AB's Annual Reports)

Dividends have been growing at an impressive 67% CAGR over the last 6 years, due to the exponential growth in revenues and margins, since net income margins increased from 34.8% in 2017 to 57.9% in 2022.

For 2023, net income is expected to be €1.07B, slightly above my projections a few months ago, which would represent a dividend per share of €2.5.

From time to time, the company has done share buybacks under the 2021 repurchase program . During 2021 and 2022, it reduced by 0.89% of the share count, spending ~€200MM, which was the maximum under the repurchase program. From 2018 to 2023, Evolution AB has spent five times more in dividends compared to share buybacks.

Even though I believe Evolution AB has an outstanding business model and has executed its growth strategy successfully, I don't like to invest in companies that pay dividends, being Evolution AB the exception in my portfolio. I prefer companies that can reinvest into growing the business and if that is not the case, share buybacks for tax reasons.

Since Evolution AB has an asset-light business model that is expanding without the need for high capital deployments, I understand its reinvestment rates will be low despite growing at fast rates, but this is not the main reason why I am so critical of its capital allocation.

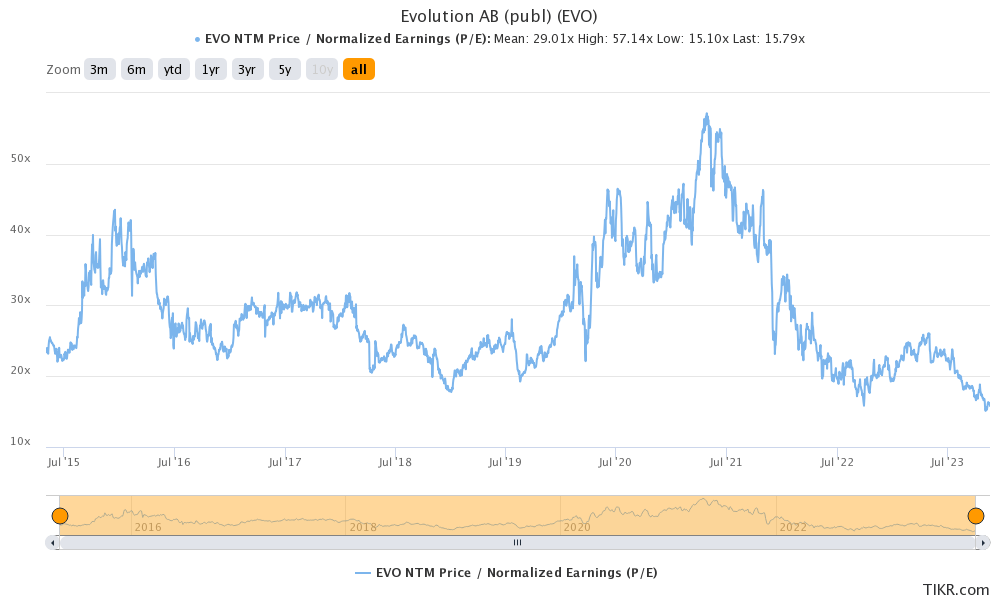

First, the buybacks have not been opportunistic, as can be seen from the chart below. The buybacks were conducted when the valuation was over 30x the next twelve months (NTM) EPS, from December 2021 until February 2022, at an average price per share of SEK 1,082 (~$119 using the exchange rate when buybacks were conducted, $1 per SEK 0.11).

{kind=link}

Secondly, and this I believe is even more relevant, is related to the acquisition strategy.

At the end of 2020, Evolution AB acquired NetEnt for a total consideration of €2,280M by issuing 30.1MM new shares (16.6% dilution). I am completely supportive of Evolution AB's acquisition strategy, even though the random number generator ((RNG)) segment is not performing as expected, I believe this is a good use of capital, it is margin accretive, allows cross-selling and improves the product offering by becoming a one-stop-shop for online casinos.

What I believe is problematic is that the company is diluting shareholder's value through the issuance of new shares while at the same time paying out dividends that are taxed.

Indeed, Evolution AB didn't have the €2.2B to make the acquisition fully in cash, but the company generates strong free cash flows and I believe management was fearful of cutting the dividend, but they would have been creating value for shareholders.

If the management finds a good use for its free cash flows, which I believe acquisitions are, given the low reinvestment rate into its own business, it would generate more value for shareholders than paying them taxable dividends.

Buybacks might resume

Despite my criticism of Evolution AB's capital allocation, I believe there are reasons to expect some improvement.

Currently, the company has no share buyback program in place since they finished buying back shares under the previous program in February 2022, but there might be a reason.

Incentive program

A significant portion of management's compensation comes from the issuance of warrants, which aims to incentivize management to increase share prices and benefit from the difference.

The CEO Martin Carlesund received a base salary of €2.1MM during 2022, which I believe is relatively low taking into account the company generated €843MM in net income during the same year.

Upon full exercise of the warrants within the program 2021/2024, the dilution effect will be approximately 1.6 percent and the exercise price is SEK 1113.8, expiring on April 2024, which doesn't provide much margin for variable compensation given the high exercise price.

To calculate the exercise price, the incentive program takes into account the volume-weighted average price of Evolution AB’s shares on Nasdaq Stockholm for a determined 15-day period and increases it by 30%.

At the last General Annual Meeting in June 2023, it was resolved that the exercise price for the 2023/2026 incentive program would take into account the share price from 1 June 2023 up to and including 15 June 2023.

As shown in the chart above, the 15-day period was the highest price during the year, so it was making it difficult for management to get fairly compensated, which caused the Board of Directors not to proceed with the resolution.

On the 9th of November, the company conducted an extraordinary meeting to resolve a new incentive program that takes into account the exercise price of 130% of the volume-weighted average price during the period from 26 October 2023 up to and including 8 November 2023, which is significantly lower.

Given the relatively low fixed compensation of Evolution AB's management, I find this movement fair, and I am happy for them to receive a higher variable compensation.

The incentive program is relevant to share buybacks since the Board of Directors was not incentivized to buy back shares during this period until the new compensation program was in place, which could trigger an announcement in the following months about a new share repurchase program.

Low valuation

Since Evolution AB became a publicly traded company in 2015, its average NTM EPS valuation multiple has been 29x. While it is true that its growth rates have been decreasing, the current NTM EPS multiple is at 15.8x.

Source: Author (Data from Evolution AB's Annual Reports)

Note: 2023 data is from Q1-Q3 .

Given the current low valuation multiples, the lack of new acquisitions during the year, and the piling cash on the balance could lead to the Board of Directors thinking about buybacks again, which would boost earnings per share.

We have done buybacks in the past, about a year ago, it was the last time. So it is not ruled out in any way, but it's ultimately it's a decision for our Board.

Source: Martin Carlesund, Q3 2023 Earnings Call .

The company finished last quarter with €813MM of cash in balance, plus an expected free cash flow of roughly €250MM for the remaining quarter of the year. The 2024 dividend is expected to cost the company about €500MM, which would leave another €500MM that could be returned to shareholders in share buybacks, reducing outstanding shares by almost 3%.

Q3 2023 Review

This last quarter's earnings report brought mixed feelings to investors.

On the positive side, EBITDA margins have been significantly higher, increasing from 69% in Q3 2022, to the current 70.4%, which is in the high range of management's guidance, and revenues increased by 26.1% YoY organically with a 6% to 8% negative headwind from currency effects.

The growth in revenues has been mainly driven by Asia, which grew at 35% and is already generating similar revenues to Europe. Latin America is also growing above the average rate at 39% YoY and the second studio of the region was opened in Colombia.

Source: Evolution AB Q3 2023 Earnings Report

{kind=link}

Also, the company released more games than ever during the quarter (28 new RNG games and 8 Live games) and included all of its RNG games on the one-stop-shop platform.

On the negative side, North America and Europe slightly declined quarter over quarter, despite growing at 9% and 10% respectively year over year. The company is facing delays in several of its planned studio projects for this year and is having difficulties in increasing the pace of recruitment.

While the live casino is growing at an astonishing 14% quarter over quarter, Evolution AB continues struggling with RNG growth, and the company doesn't seem to be able to hit the right note.

Expectations

For the next quarter, I expect Evolution AB to solve the undersupply problem in Europe, increase the speed of recruitment given it is one of management's key priorities and open one new studio.

For 2024, the company has an exciting roadmap and is expecting to release more games than ever, while opening 3 or 4 new studios between Europe, North America, and Latin America.

In the recent G2E Las Vegas Gaming Expo, where Evolution AB doubled the size of its stand, it presented the new game Red Door Roulette - a mash-up of two of Evolution’s most successful games, Crazy Time and Lightning Roulette - and Video Poker, a live casino version of a classic game.

As Todd Haushalter anticipated during the event, in February 2024 they are expecting to release the biggest and most expensive game Evolution AB has ever made.

{kind=link}

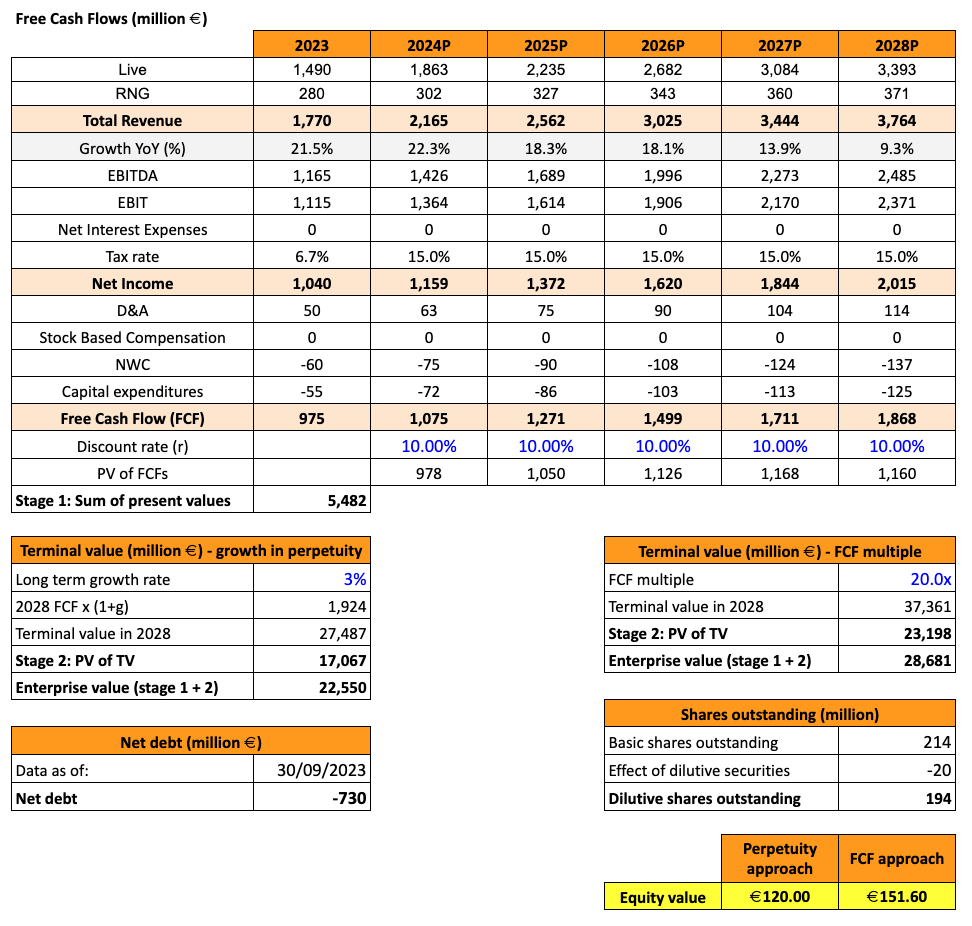

I have updated the DCF model presented in my previous coverage with a decrease in the perpetuity growth rate with lower live and RNG growth rates, according to the recent slowdown in Europe and North America. In the base case scenario, I am not expecting any margin improvements.

Given the lower valuation multiples and the release of the new incentive program, I expect Evolution AB to resume its share buybacks with a 2% annual decrease in shares outstanding.

Overall, my average fair price has decreased to €135 per share ($144), but I consider the stock to be undervalued by 51%, and my expected returns for the next five years are 15% CAGR plus a 2% dividend yield.

Conclusion

While I have no insider information, the recently approved incentives program and the historically low valuation of the company, combined with the past track record of share buybacks and strong cash flows, could lead to an improvement in Evolution AB's capital allocation, boosting its EPS.

Last quarter's results brought mixed feelings. Margins are increasing and some regions are performing better than expected, but Europe and North America's revenues have decreased from the previous quarter. The RNG segment is also struggling to grow as expected by management.

Finally, I lowered my fair price for Evolution AB to €135 per share, but continue to consider it highly undervalued and expect returns above the market average.

For further details see:

Evolution AB: Capital Allocation Might Improve Soon