EVVTY - Evolution AB: Long-Term Compounder Trading At Fair Valuation

2023-12-12 10:33:00 ET

Summary

- Evolution AB is a leading provider of live casino solutions in the fast-growing online gambling industry and has a compelling business model and high profit margins.

- The stock is currently undervalued, down 22% from its peak, and is rated as a BUY with a target price of SEK 1194 or USD 110.

- Evolution benefits from significant economies of scale, a strong competitive advantage, and a management team with a track record of success.

Investment Thesis

Evolution AB (EVVTY) is a best-in-class B2B provider of live casino solutions in the iGaming industry. Evolution benefits from significant economies of scale, an excellent track record and 70% EBITDA margins. Since its March 2015 IPO at SEK 16 (split adjusted), the stock has increased a phenomenal 70x. The market is aware of this darling, however, and Evolution normally trades very expensively. Recently, however, the stock has corrected. At the current price of SEK 1148 or USD 106, down 22% from its peak, we rate the stock as a BUY with a target price of SEK 1194 and USD 110. While our target price is only 4% higher than the current price, qualitative factors such as management's strong execution track record and potential upside scenarios mean we still rate the stock a BUY.

Product Overview

Evolution AB provides comprehensive Live Casino solutions to gaming operators, which include development, production, marketing, and licensing aspects. Real-time streaming of casino tables allows an unlimited number of players to interact with live, professional dealers via desktop or mobile devices. Besides live casino solutions, Evolution also runs RNG (random number generator, e.g. slots) games that account for 15% of its revenue. As a B2B provider, Evolution's games can only be played through a gaming operator, who is responsible for finding and authenticating the end users. As such Evolution is not responsible for most of the KYC ("Know-Your-Customer") regulatory burdens, which are instead borne by its customers, reducing regulatory risk.

Evolution generates revenue by charging commission fees (typically 10%) based on the profits generated by its customers. Evolution also makes money by charging operators monthly fees for dedicated tables, which ensures capacity for gaming operators.

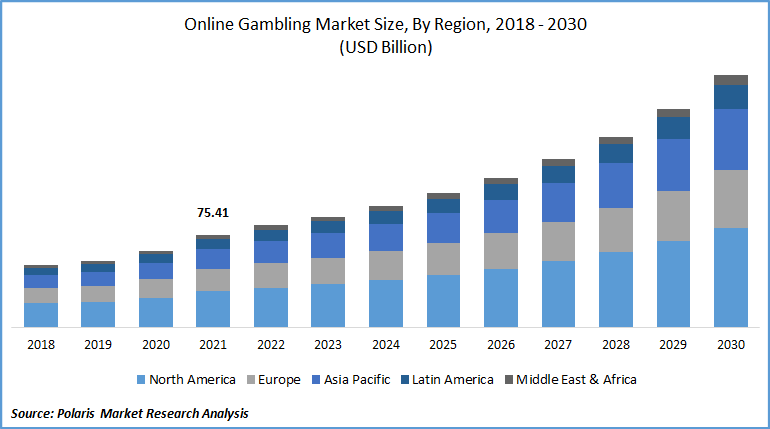

Online Gaming Market Growth Overview

According to a 2022 report from Polaris Market Research, the online gambling market was valued at $75 billion in 2021 to $125 billion and is expected to grow at a CAGR of 12% till 2030. This market size growth is driven by growing broadband usage, continued legalization of iGaming, and general GDP growth.

Graph 1: Online Gambling Market Size by Region 2018-2030 (USD Billion)

Online Gambling Market Size By Region 2018-2030 (Polaris Market Research Analysis)

{kind=link}

The United States is a lucrative growth area, where 80%+ of the gambling is still land-based according to the American Gaming Association. As more states move toward legalizing gaming, Evolution and other iGaming companies should make more inroads from the world's largest economy.

Graph 2: United States: Commercial GGR by Vertical and Mode

United States: Commercial GGR By Vertical and Mode 2016-2022 (American Gaming Association)

Culture and Competitive Advantages

Evolution's Competitive Advantages

Evolution's main competitive advantage is economies of scale. As the largest live casino player, Evolution can spread its costs across more customers and end users. Unlike a traditional brick-and-mortar casino, one dealer can deal with an unlimited number of players, so having more players directly increases revenue without incurring significant additional costs. This is the Netflix or SaaS model, where the same product can be sold an unlimited number of times.

These economies of scale also mean Evolution can release new games and conduct more R&D at lower costs per revenue generated, and Evolution has done exactly that by developing and releasing many more games than its competitors. This furthers its product advantage, which in turn attracts more customers and end users, leading to a positive feedback loop.

Technical know-how is another barrier to entry. Developing live casino dealer games appears deceptively simple, but small details can break a game. In "Wheel of Fortune" type games, the wheel must be crafted precisely and tested to ensure that the wheel is completely symmetrical in weight to avoid non-randomness, i.e. favoring one outcome over another. Small statistical discrepancies are quickly found by enterprising players, reducing the house edge.

Finally, regulations, while a double-edged sword, can protect an incumbent company by raising barriers to entry for competitors. Evolution and its subsidiaries hold 53 licenses from various jurisdictions as a gaming vendor, software provider, equipment manufacturer, etc. (Source: Compliance & Markets ). A new competitor attempting to replicate this would require significant investment in time and money, thus decreasing the attractiveness of entering the industry.

Culture

CEO Martin Carlesund and CPO (Chief Product Officer) Todd Haushalter have each been with the company for 8 years. In addition, the Chief Strategy Officer and CFO have also been with the company since 2008 and 2016 respectively. This team has worked together for a long time and has done an excellent job growing the company, with revenues increasing from EUR 76 million in 2015 to EUR 1.5 billion in 2022 and profit margins from 26% to 58%. Furthermore, of Evolution's three founders, two (Jens Von Bahr and Fredrik Osterberg) remain on the board of directors while the third (Richard Hadida) appears to still be involved in the company as a Creative Director. Overall insiders own about 10% of the company, with most of it held by Jens Von Bahr and Fredrik Osterberg. We believe management and the board are reasonably incentivized to make good decisions for shareholders.

Glassdoor reviews on Evolution AB are weak, with 55% of reviewers recommending the company to a friend and 52% approving of CEO Martin Carlesund. We normally look for companies with 75%+ positive reviews. Many of the negative reviews are from live game presenters, who complain about the long hours and lack of upward mobility. Management appears to have an "everyone is replaceable" mentality, especially for live game presenters. One review negatively described Evolution as the "Amazon of Casinos" as the long hours and grueling pace resemble that of Amazon delivery workers. The flip side of the argument is that Amazon, like Evolution, has done very well despite treating low-level employees somewhat like robots. Overall, we wish the Glassdoor ratings were better but do not see this as a critical negative for our thesis.

Slide 1: Evolution AB's Glassdoor Reviews

Evolution Reviews (Glassdoor)

Source: Glassdoor - Evolution AB Reviews ( Working at Evolution )

Shareholder-Friendly Capital Allocation

We like Evolution's capital allocation strategy. In previous years it was largely focused on plowing back money into growing its business organically, which was intelligent as annual gross profit grew 38 times from EUR 38 million in 2013 to EUR 1.5 billion in 2022. While still investing in its business, Evolution has recently shifted towards dividends and buybacks, with a policy of paying out 50% of net income as dividends. This is a healthy admission that growth will slow in the future, and that this is better than re-investing in questionable internal projects or engaging in reckless acquisitions.

Evolution's acquisition strategy has been a weak point. While their live casino business has grown very well organically, Evolution's RNG business is losing market share to competitors. Evolution has acquired RNG operators such as NetEnt and Big Time Gaming but its RNG revenue growth remains anemic and we suspect competitors such as Playtech are taking market share.

According to Sweden's Finansinspektionen PDMR register, CEO Martin Carlesund purchased in November 2023, 100,000 shares at an average price SEK 1002. Insiders sell stock for many different reasons, but they buy stock for only one reason - they think the share price will increase. A CEO's insider purchase is an important vote of confidence. Furthermore, the company is also buying back its own shares. While a weaker signal compared to insider management buying, it's still a positive development and lends support to the stock.

Financials and Valuation

PE and EV/EBITDA Valuation

With a market cap of EUR 2.81 billion and TTM net income of EUR 1.0 billion, Evolution trades at a P/E of 21x. An Enterprise Value of 21.0 billion and TTM EBITDA of EUR 1.2 billion leads to an EV/EBITDA ratio of 17.3x. We think these metrics are reasonable for a high-quality company that last grew revenues 19% YoY in Q3 2023 and that should generate mid-teens revenue growth in 2024.

DCF Valuation

Using a 5-year DCF approach we get a target price of SEK 1,194 or USD 114 using the below assumptions:

- Annual revenue growth rate of 16% for the next twelve months and decreasing 1% per year thereafter to 12% by Year 5, or a revenue CAGR of 14%. This is in line with general online gaming market growth forecasts of approximately 12%, with additional credit given due to their current above-market growth rates.

- 63% operating margins and 53.4% net margins in the long term. We assume current operating margins remain. Due to the introduction of global minimum taxes in 2024 ("GLoBE"), we assume a tax rate of 15% (up from the current 7%) which reduces future net margins.

- Dividends are 50% of net income, as per Evolution's stated minimum dividend policy.

- The current share count of 213.9 million shares is unchanged as buybacks offset shareholder-based compensation. Evolution may eventually be a share cannibal that reduces its share count over time but due to conservatism, we don't factor this in.

- WACC of 12%, terminal growth rate of 7% (representing continued growth of iGaming past 2028) leading to a terminal PE ratio of 20x.

Table 1: Evolution Valuation Model

Evolution AB Valuation Model (Author Analysis, Company Annual and Quarterly Reports)

Risks

Risks with Evolution include unfavorable regulatory policies, recession, customers attempting to move in-house, and GLP-1 drugs impacting the overall industry.

Unfavorable regulatory changes are the largest risk Evolution faces. Many of Evolution's end customers are based in unregulated markets. If regulatory authorities were to ban Evolution's products, that would clearly impact Evolution's growth trajectory. Furthermore, a slowing pace of legalization, especially in the United States, would also weaken our thesis.

Timing recessions are notoriously difficult, but many economists predict one in 2024. Gambling stocks fare poorly during recessions and Evolution's stock price would also take a significant hit. However, Evolution is somewhat shielded from a recession due to 1) the secular trend towards iGaming, 2) a debt-free balance sheet with EUR 813M of cash and cash equivalents (as compared to capital-intensive, brick-and-mortar casinos which typically carry a lot of debt) and 3) geographic diversification due to revenue growth in fast-growing Asia & Latin America.

Existing customers may also attempt to move their live casino solutions in-house. Evolution's EBITDA margins of 70% naturally attract competition from both other B2B providers and existing customers trying to move in-house. For the reasons in the "competitive advantages" section above, we feel in-house attempts are unlikely to succeed, but that doesn't mean customers won't try anyway.

Semaglutide (GLP-1) drugs, marketed under brands such as Ozempic, Mounjaro, Wegovy, and others, may negatively impact Evolution's revenues. Originally developed to combat diabetes, GLP-1 drugs also successfully combat obesity and anecdotally reduce cravings that spur other unhealthy addictions such as excessive shopping, nicotine, and gambling. Like many other consumer discretionary businesses, Evolution's revenue and profitability from end users follow the 80/20 rule and are heavily reliant on a small percentage of heavy end users to drive revenue and profitability. If GLP-1 drugs reduce the number of these heavy users, Evolution and its customers would be significantly negatively impacted.

These risks, if actualized, would damage our BUY thesis. Evolution stock is not a buy-and-hold forever stock, instead, we need to monitor the stock to ensure the thesis is not impaired.

Conclusions

Balancing the risks with the opportunity, Evolution is still a good investment at current valuations. Based on our target prices, we see about a 4% upside compared to current prices, which means the stock is fairly valued. We struggled with whether to put a HOLD or BUY rating with the stock due to the low upside potential in our base case, but we think Evolution's strong track record of revenue growth, extreme profitability, and potential for upside if there is faster than expected growth means the stock deserves a BUY rating. Evolution is a 2% position in our portfolio. Assuming an unchanged fundamental story, we plan to accumulate on price dips.

For further details see:

Evolution AB: Long-Term Compounder Trading At Fair Valuation