EVVTY - Evolution AB: The Best Opportunity I've Seen In A While

2023-10-05 09:57:28 ET

Summary

- Evolution AB is a high-quality business with substantial free cash flow growth, pricing power, and superior returns on capital.

- The company is an online gambling games provider, with a focus on live gaming experiences.

- Live gaming currently represents only 5% of the total casino market but is growing rapidly.

- Acquiring a high-quality business at an attractive price is a rare opportunity.

My Thesis: It Is a Positive One

If you read my previous articles, you will notice my appreciation for high-quality businesses—those capable of generating substantial free cash flow growth, possessing pricing power, and achieving superior returns on capital. In my opinion, the synergy between high returns on capital and FCF growth is an inevitable compounding factor. Moreover, it is currently trading at a reasonable, if not cheap, price.

As we delve deeper into the company's financials and performance metrics, you will gain a better understanding of my enthusiasm.

What Does Evo Do?

Evolution AB ( EVVTY ) operates as an online gambling games provider with a diverse portfolio. It offers classic games like Poker and Blackjack, as well as innovative and unique creations of its own. A significant portion, approximately 84% , of its revenue is derived from live gaming, an engaging and interactive experience that combines virtual elements with live dealers visible on your screen. These live games are sold to online casino operators, making Evolution AB a B2B business. The company produces these live games in its studios worldwide, each characterized by distinct styles and unique designs. You can view an illustrative example here .

While live gaming accounts for just 5% of the total casino market and 24% of the online gaming market, it is experiencing rapid growth. The online casino market has achieved a notable CAGR of 20% over the last five years, while live gaming has grown even faster at a CAGR of 21.5%. In contrast, the RNG segment, which is three times the size of the live gaming segment within the total casino market, has also demonstrated strong growth with a 19.5% CAGR. However, as we will delve into later, EVO faces challenges in achieving growth in this segment.

I appreciate the company's mission as outlined in its annual report:

To increase the gap to our competitors and grow faster than the global online casino market.

Growth in Evolution AB is driven by various factors:

1. Scalability: Unlike land-based casinos, each live table accommodates a significantly larger number of players, and the marginal cost remains relatively low. As the market expands, and assuming Evolution gains market share, its costs are unlikely to grow at the same rate, potentially leading to margin expansion. (This is particularly noteworthy given the record EBITDA margin of 70% achieved in Q2 23.)

2. Innovation: Innovation plays a pivotal role in Evolution's future prospects, but it also poses a risk. In 2022, Evolution introduced 88 new games, reflecting a rapid pace of innovation. However, if innovation becomes a primary driver of growth, any slowdown in this area could have a negative impact on the company.

3. New Markets and Regulation: The entry of new markets with favorable regulations for online gaming presents significant opportunities for Evolution. Legalizing online gaming in new markets creates substantial growth potential, making it a key growth factor for the company.

Is There a Moat Around Evo?

As the company highlights in its annual report:

The barriers to entry are relatively low, while the barriers to success are considerably higher.

To thrive in this industry, a high level of technical expertise, substantial volume, and a skilled management team are imperative. Evidently, Evo has excelled in all these aspects, as reflected in its returns since its inception.

Evo's strength lies in its uniqueness. If a player wishes to engage in live casino gaming, and their current online casino cannot provide it, they can seamlessly switch to a platform that offers Evo's services without any detriment to Evo.

Evo generates revenue through two primary channels: contractual agreements with operators and fee-based revenue. Evo enters into agreements with operators for a set number of years and also earns a percentage ( 10% ) of the operators' winning revenue. Notably, Evo's resilience shines through as it remains unaffected by the operators' losses.

Evo's equipment for their studios is surprisingly manufactured in their Riga-based job shop, and its strength is highlighted in the following text:

A key benefit is the speed at which devices and parts can be made. Often, the Job Shop’s ability to produce equipment in a few days saves the day, enabling a studio and game to meet a demanding launch schedule. Another benefit is assured quality and consistency.

And from another perspective:

The smart design and vast experience of the Evolution R&D team and the precision of the Job Shop’s output means that internally produced equipment delivers better and more consistent results. For example, our automatic dice shaker exhibits 80% fewer ‘dice on edge’ errors than comparable products from known brands. Job Shop is another innovative Evolution success story and its value is undeniable. This in-house facility means shorter product-to-market time and full control over production; the capability to manufacture products that simply don’t exist outside of our imagination; and the agility to respond rapidly to the challenges posed by every new and unique studio build.

Generally, I would assert that Evolution's moat is not as extensive or profound as that of previous companies I've analyzed, such as Ferrari (RACE) and ASML Holdings (ASML). However, it does exist, primarily due to its scale, expertise in the live casino segment, and its dedicated focus on this particular market.

M&A

In general, I'm not a fan of M&A activities; I prefer organic growth. However, if a company has competent management and identifies an opportunity in a new market that would otherwise be inaccessible, it can be beneficial for the firm. In the realm of big tech, we've witnessed significant success stories stemming from M&A, such as Instagram and Meta ( META ), Google ( GOOGL ) and YouTube, and more recently, Satya Nadella's ( MSFT ) strategic move towards OpenAI.

Evolution has made several acquisitions in an attempt to diversify its offerings and expand into various segments of the gaming industry. These acquisitions include NetEnt, Red Tiger, Ezugi, and more.

Every Quality Investor Would Appreciate Evolution's Numbers

What makes this business particularly appealing is the combination of three key factors: high revenue growth, consistently increasing margins, and strong returns on capital.

In my opinion, the synergy between robust returns on capital and steady growth is a recipe for outperforming the market. If you can acquire this stock at a fair price, the potential for remarkable performance is undeniable.

Evolution has achieved remarkable revenue growth over the past five years, with an impressive 53% CAGR. However, it's essential to note that a stock's value is derived from its future cash flows, and I don't believe it will be able to sustain such high growth rates. Consequently, my discounted cash flow model is not based on such growth rates. Analysts also project a more moderate 16% CAGR for the next five years, which seems reasonable given the company's maturing status and past performance.

Evolution has demonstrated remarkable operating leverage, achieving an astounding 91% CAGR in free cash flow over the past five years. Additionally, the company reached a record 70% EBITDA margin in Q2.

Furthermore, in my perspective, Evolution shares a critical characteristic commonly found in typical compounders: high returns on capital that surpass its cost of capital, resulting in value creation. You can observe the return on invested capital ((ROIC)) and return on capital employed ((ROCE)) in the following chart:

From a solvency perspective, EVO is well-positioned in a high-interest-rate environment, with a cash balance of $ 591 million compared to a relatively low debt level of only $87 million. Moreover, the company's liquidity appears robust, with a favorable current ratio in place.

The Altman Z-Score of EVO is also notably high and indicative of a healthy financial position.

When it comes to returning value to shareholders, Evolution has a goal that I find less appealing:

To distribute a minimum dividend of 50% of net profit over time.

While I'm not opposed to dividends, I would prefer that the management's capital allocation strategy be more sophisticated. I would like to see them consider buying back the company's stock when its shares are believed to be undervalued, as I believe they are at the moment. Alternatively, they could consider investing more in the RNG market, where they currently lag behind in terms of growth. The RNG market has seen a 5-year CAGR of 19% , while Evolution's growth in this segment is currently stagnant. In general, I don't believe that a growth-oriented company like Evolution should be bound by a rigid dividend policy. Such a policy may attract dividend-seeking investors, but if the company were to cut its dividend to reinvest in growth or secure cash reserves for challenging times, it could lead to a sell-off by dividend-focused investors. However, this is just my opinion, and it's important to acknowledge that dividend payments do represent a genuine return to shareholders.

Another important aspect to consider is 'skin in the game.' Four key individuals at Evolution have a significant ownership stake in the company. The co-founders, who currently serve on the board, collectively hold 22,400,140 shares, which represents approximately 10% of the company. Additionally, the CEO holds a chunk of 500,000 shares, and the CTO, who has been with the company since 2008, holds 700,000 shares, all without any warrants.

As you may be aware, having a substantial ownership stake can be highly beneficial, at least in my opinion. It incentivizes the management team to perform well and aligns their interests with those of the shareholders. A notable example I admire is Brian Chesky of Airbnb ( ABNB ), who owns approximately 30% of the company and, in my opinion, is an outstanding CEO and capital allocator.

Valuation: Where Things Are Heating Up

Let's dive straight into it: Evolution is undervalued, perhaps significantly so.

When I invest in companies, I like to have three defense mechanisms in place: quality of the business, relative valuation based on past multiples, and a DCF model.

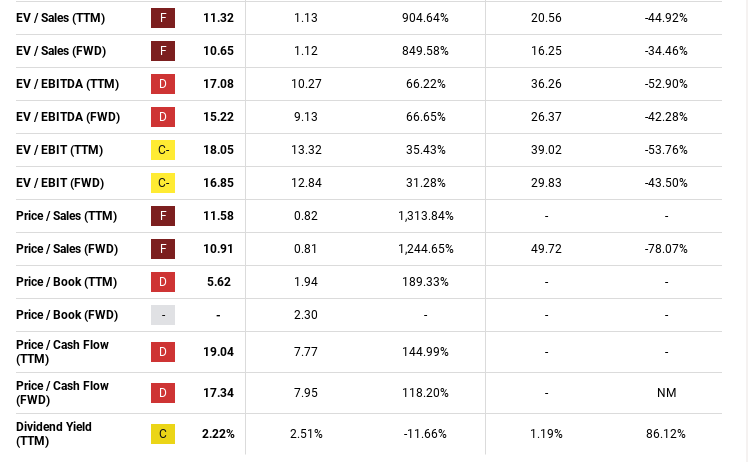

We've already discussed the quality of the business, so let's talk about the relative valuation. Evolution's five-year average FCF yield is 2.6% , and as of now, it's at 5.2%. This suggests that based on this ratio, the stock is massively undervalued. The same holds true for different multiples like EV/EBITDA, etc. The potential for multiple expansion, in addition to business growth, is substantial.

{kind=link}

However, it's important to acknowledge that we may not see Evolution reach past multiples for two reasons: future growth is expected to be lower than in the past, and we are no longer in the Zero Interest Rate Policy ((ZIRP)) era, where the discount rate for companies was lower.

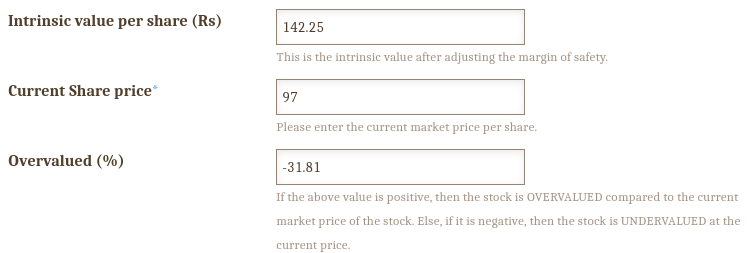

The third defense layer is a prudent DCF model. We will use different growth rates to explore possibilities. I have employed a solid 10% discount rate, which is quite conservative. Evolution is in excellent financial shape and solvent. According to Alpha Spread, their WACC is 7.8%. I used a 16% growth rate based on analysts' revenue projections for the next 5 years. It's worth noting that I didn't assume any margin expansion, which could accelerate FCF growth as we've seen in the past. So, the model is quite conservative. It suggests a stock price of $142, indicating an undervaluation of 31% as of the time of writing this article. This represents a substantial margin of safety, especially for quality companies, which are typically difficult to buy based on conservative DCF models or above a 5% FCF yield.

results (DCF calculator) inputs (DCF calculator)

{kind=link}

Based on a 10% discount rate, the current price ($97) suggests an 11% FCF growth, which is highly unlikely given market growth and Evolution's past and future analyst projections. However, of course, it's possible, although uncertain. We have to make our best estimate. If we assume a more significant 20% FCF growth rate, in line with the market CAGR, we can derive a stock price of $190, which represents a 50% margin of safety.

Based on the two valuation methods, Evolution appears to be undervalued, and there are no apparent flaws in their business that can explain this undervaluation. It is a rare occurrence to find a quality company with such an attractive price based on these two methods, especially when the free cash flow yield is above 5%.

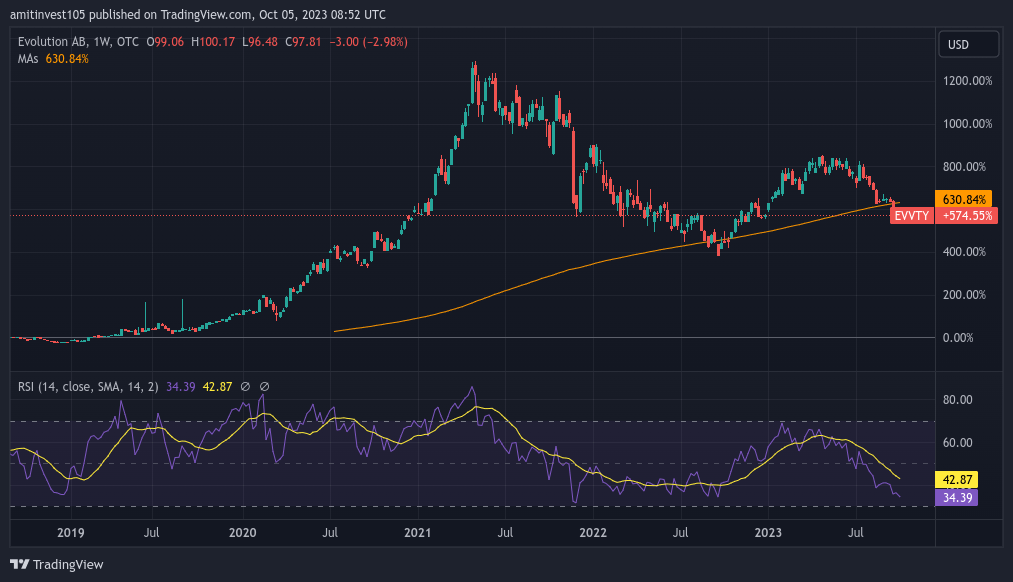

Technical View: My preferred approach involves acquiring companies when their stock prices are in proximity to their 200-day moving averages and exhibit low RSI levels. In the case of Evolution AB, it is noteworthy that the stock currently aligns with both of these criteria, as visually represented in the chart:

{kind=link}

Risks

1. Low Barriers to Entry: While there may be low barriers to entering the live gaming market, succeeding in this competitive space can be challenging. The high level of technical expertise and operational excellence required could deter potential competitors.

2. RNG Growth: The Random Number Generator RNG segment's lack of growth is a concern. It's crucial for Evolution to address this segment's growth to diversify its revenue sources.

3. Regulatory Changes: Regulatory changes in various countries can have a significant impact on Evolution's business. Evolving regulations can either open up new growth opportunities or create obstacles.

4. Mergers and Acquisitions: M&A activities always carry risks. Entering new markets or acquiring other companies can be a way to expand, but it also comes with integration challenges and uncertainties.

5. Valuation: While Evolution's valuation may appear attractive, market maturity can pose challenges. As the market matures, sustaining historical growth rates can be difficult.

These considerations highlight the need for Evolution to adapt to changing market conditions, diversify its offerings, and manage potential risks effectively.

Conclusion

Evolution is a high-quality compounder with impressive returns on capital and a promising growth trajectory. These are the characteristics I seek in companies, but finding them at attractive prices has always been a challenge. However, this time, I believe it's different. Evo's valuation presents a compelling opportunity, and there seem to be no inherent flaws in its business model to justify its current undervaluation. As of now, I don't hold any shares of the stock, but by the time this article is published, I may have initiated a position.

I would appreciate reading your thoughts on this matter.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Evolution AB: The Best Opportunity I've Seen In A While