EVVTY - Evolution AB: The Way To Play The IGaming Opportunity

2023-06-17 07:19:12 ET

Summary

- Evolution AB offers a strong investment opportunity in the growing iGaming market, with a dominant market position and fantastic margins.

- The company's global reach and diversification of revenue streams, along with its focus on new markets like the US and Brazil, make it an attractive pick for investors.

- Despite potential risks such as regulatory changes and competition, Evolution AB's current valuation and growth potential indicate a high chance of outperforming the market.

Investment Thesis

-

There is a large and expanding opportunity for as iGaming markets are increasingly legalized and regulated.

-

Evolution AB is a pick and shovels play, as they develop and license the games that sports book and casino operators use.

-

They already have a dominant position in the market and fantastic margins.

Investment Opportunity

Whilst Big Data, autonomous driving and AI may be the sexy growth narratives that are front and centre of many financial news outlets, I want to focus on another huge market that is slightly neglected. IGaming is the name given to online casino and gambling games and the market is due to almost triple in the next decade as more countries' governments legalise and regulate their gambling markets. In this article, I will explain how Evolution AB (EVVTY ) is the pick and shovels approach to playing the opportunity.

The Online Gambling and Betting Market Opportunity 2020-2030 (Globe News Wire)

Gambling may not necessarily be an area of interest for you as an investor, and you wouldn’t be alone. Many ESG indices prohibit investment in casinos and book makers and many individual investors choose to do the same. Personally, I’m fairly agnostic to the sector and appreciate both the risk that addiction can have for people’s lives (my wife is a psychotherapist who works with addicts) and the pleasure that can be found in doing so responsibly. The global regulated gambling markets are providing a unique opportunity for those who are comfortable in the sector; people are always going to gamble, and in my view, better the risk be to a publicly listed company than to a man who owns a baseball bat.

Much like the cannabis industry, retail investors have found their way into many companies seen as being ways to ‘play the opportunity’, and due to the commoditization of both industries, there are very low barriers to entry and lots of competition, which drives prices and margins down. It’s one of the reasons why I rated Draftkings ( DKNG ) a sell , and, despite it being up 30% since mid-April when it was published, I maintain that as a long term oriented investor, it will struggle to beat the market if held for the long term.

Here’s where Evolution AB comes in. It is a business-to-business operator that focuses on the creation, presentation and licensing of iGaming products such as live bingo and poker, virtual slot machines, and roulette tables to the major casinos and book makers. Not directly dealing with gamblers means that they do not have to worry about authentication nor any issues surrounding over use, fraud or arrears, the responsibilities for which lie with the operators themselves. It is the pick and shovel approach to the global gambling opportunity and the best part is that it already has an almost impenetrable competitive advantage, a leading market share and is already very profitable - even paying out a little dividend for those who are into that sort of thing.

To give some numbers to the ‘already very profitable’ line, Evolution AB currently has an EBITDA margin of 65%, a net income margin of 57% and a levered FCF margin of 36%.

Profitability Tab (Seeking Alpha)

They make their money in 2 main ways. From taking a small commission of the winnings that operators receive when ‘the house wins’ during random number generator games such as virtual slot machines as well as from live casino games that are hosted on operators’ apps and websites. They also have a smaller part of their revenue based on monthly fees that can be paid by operators who want to offer exclusive or highly customised tables and games for their clients, including the design of the games and languages spoken by dealers or hosts.

To get an idea of how embedded they are already into iGaming, here are a selection of its current customers: 888 & William Hill ( EIHDF ), Betway ( SGHC ), Draftkings ((DKNG)), Entain ( GMVHF ), Betfair, Pokerstars & Paddypower ( PDYPY ), Penn National ( PENN ) and Unibet ( KNDGF ). In fact, their market share sits around the 40% mark of global regulated markets, and these markets are compounding quickly as more and more nations are reforming gambling laws, including large opportunities in the US and soon Brazil, the largest economy in South America. The company’s biggest costs are in staff, whether as software engineers and game developers or as the aforementioned game hosts.

Evolution AB already has a global reach, which can be seen in the pie chart and stacked column chart below. Management reports their revenues with three different European markets: The Nordic countries, the UK and the rest. I have simplified this to combine each of the European markets. The pie chart shows how Europe currently makes up just over 40% of total revenue.

Revenue by Geographic Area as per FY2022 (Compiled by Author from Information from Company's Earnings Presentations)

What I find quite exciting is how the very large future markets - the US and Brazil and potentially Africa, make up a relatively small part of current revenue but how they are growing very quickly. The stacked column chart shows us how sales in each of these geographic regions are increasing and how the more developed markets within Europe, whilst still growing quickly (around 40% CAGR over the past 6 years), are increasing much less quickly as the new markets in North America, Asia and the rest of the world. This not only indicates that they are increasingly diversifying their sales, but more importantly, they are working hard to ensure that they get their fair share of up-and-coming markets. Further, in their Q4 2022 report, management stated that “Evolution AB’s growth target is to grow faster than the total global online casino market”, indicating that they believe that they can not only grow but also further increase their market share.

Simplified Model of Revenue by Geographic Market Since Data was reported in FY2019 (Compiled by Author from Information from Company's Earnings Presentations)

Investment Risks

I’ve spoken already about the global diversification of revenue streams being a positive for the company. On the other hand, there are some diversification risks with Evolution AB. As of the end of FY 2022, around 30% of its sales were generated by its top 5 customers. I don’t believe that is a major risk, but with consolidation in the sector likely due to the large amount of competition, it is something to be aware of. A major merger between two operators where one used Evolution AB and want did not and the larger new company moved away, could potentially have a large impact on sales.

The company itself identifies a major risk that as it grows very quickly, it may struggle to find sufficiently skilled staff to join its international teams. It has grown at a compounded rate of 30% over the past few years and is currently working hard to recruit Brazilian Portuguese speakers for the Brazilian iGaming markets. Competition for skilled staff = potential wage inflation, which as aforementioned is a major expense for the company already. Again, this risk isn’t major as they do not have high levels of stock dilution from stock-based compensation and have margins that can cope with these increased expenses.

Employee Growth Since 2017 (Compiled by Author from Information from Seeking Alpha)

The biggest risk as I see it is regulatory. In the same way as this huge and growing addressable market has arisen from governments looking for new sources of income and moving gambling away from the shady black markets to regulated and taxable markets, public pressure and media controversies could potentially see these steps reversed. At risk of repeating myself, I do not believe that this is a genuine existential risk to Evolution AB. The cat is rather out of the bag and in my personal opinion, the legalisation, regulation and taxation of the Sin Industries is far better than allowing crime to run these markets.

A final risk is competition. I believe that sports betting has a low barrier of entry. I’m British and live in Germany, and for those who do not reside in a developed gambling market such as those found in Europe, it can be overwhelming how many different companies there are who basically do the same thing. Other than celebrity adverts, the UI of the app or website, or a catchy logo, if I place a bet with company X or company Y there is no discernible difference to my experience. AI and data are helping sports book operators to offer more profitable odds for events and as such most have very similar offerings to punters. As a result these operators dive deep into their pockets to attract customers. Free bets and new customer bonuses are used to incentivise loyalty, but there really is none to be had.

For Evolution AB as a provider of games to these operators, there is less competition; however, it does not mean that there won’t be in the future. This is a large and growing industry and I do wonder whether innovative companies who could potentially use AI or image use of celebrities and deep fake technology could maybe disrupt and offer operators either cheaper experiences or more personalised ones than Evolution AB. The company has recently rolled out their ‘Smart Lobby’, which sounds like a step towards this by using AI to personalise and individualise experiences, but the future in this regard must be considered a risk.

Valuation and Chances of Beating the Market

Evolution AB is certainly well priced right now. My favourite metrics would be that the trailing GAAP PE ratio is around 30, its FCF yield is around 3.6% and its EV/EBITDA is 25. This is not a cheap company by any stretch of the imagination.

For comparison, its market cap is at time of typing more than MGM and Draftkings combined.

Valuation Tab (Seeking Alpha)

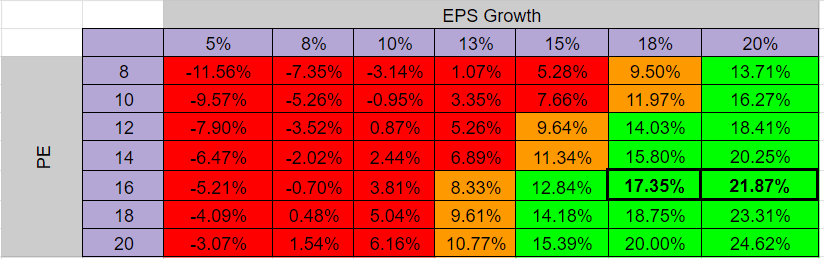

This is my 4th article on Seeking Alpha, and I’m continuously trying to work out the best way to show valuation models that are accurate and helpful for those taking the time to read them. Some on the site, I find too fiddly and/or convoluted, so I would like to present an adaptation of what I use as a ‘smell test’ for my forecasts for my own personal investing. Simply, I work out the future value of the company's EPS over 10 years based on the following CAGR 5%-20% from the current TTM EPS of $3.01. Then I apply a range of potential PE multiples that the market may pay for those earnings out a decade. Finally, as presented below, I work out the annual rate of return from the current EPS and stock price to these hypothetical ones. As I’m a very visual person (hence I like slideshow presentations), I then colour code these as:

Red (below 8%) - unlikely to beat the market

Orange (8.01% - 11.99%) around the market

Green (12%+) should beat the market

My assumptions here are that as the total addressable market will grow around 12% and Evolution AB a) will gain market share b) will become more efficient and c) will start to reduce share count. Resultantly, it will likely grow its EPS over the next decade at a rate of around 15%-20%. I also believe that due to the market position and high margins, it will likely be awarded a slightly above market PE ratio of between 16-18, even if growth has slowed down by then.

Potential Annual Share Performance Over the Next 10 Years Based on Hypothetical Growth Rates and Earning's Multiples (Author's Work)

{kind=link}

As a frame of reference, the company’s current compounded annual growth rates can be found below. I doubt that these growth rates will continue to be this high, but as you can see, the stock has potential for significant outperformance against the market.

Growth Tab (Seeking Alpha)

Investment Summary

Evolution AB is a great way to play the online iGaming opportunity. It is already profitable, growing quickly, reasonably priced in relation to its potential growth and has a strong market position.

If it can grow market share and the regulated iGaming markets continue to grow as expected, then an investment today at these prices, even after the run up of over 30% YTD is likely to beat the market quite handsomely. If the prices retract from here, it becomes even more attractive.

For further details see:

Evolution AB: The Way To Play The IGaming Opportunity