CAHPF - Evolution Mining: A Tough Finish To A Challenging Year

2023-07-25 11:36:24 ET

Summary

- Evolution reported a sharp decline in gold and copper production due to flooding at its Ernest Henry Mine in March and not reaching full capacity until the end of June.

- Unfortunately, this disappointing performance which was out of its control combined with a weaker year at Red Lake overshadowed an exceptional year for its Cowal Mine.

- The good news is that the recent margin compression was largely due to an event out of its control and FY2024 will be much better financially.

- However, while Evolution may be down following earnings, I still don't see nearly enough margin of safety, and I would need to see a pullback below US$1.85 to become more interested in the stock.

The Q2 Earnings Season for the Gold Miners Index ( GDX ) has finally begun and one of the first companies to report its results was Evolution Mining ( CAHPF ). Like Newmont ( NEM ), Evolution had a rough June quarter (fiscal Q4 2023), impacted by lower contribution from one of its key assets but for different reasons. In Newmont's case, the company had a strike at its massive Penasquito Mine that severely impacted overall production and costs. For Evolution, mine production at Ernest Henry was derailed following flooding in March, with the asset coming back online in late April but operating at lower levels during the quarter. And given that this was Evolution's highest-margin and most productive asset from a cash flow standpoint, this put a severe dent in fiscal Q4 margins and cash flow. Let's take a closer look at the quarter below:

{kind=link}

All figures are in United States Dollars unless otherwise noted at an exchange rate of 0.67 AUD/USD.

Q4 & FY2023 Production

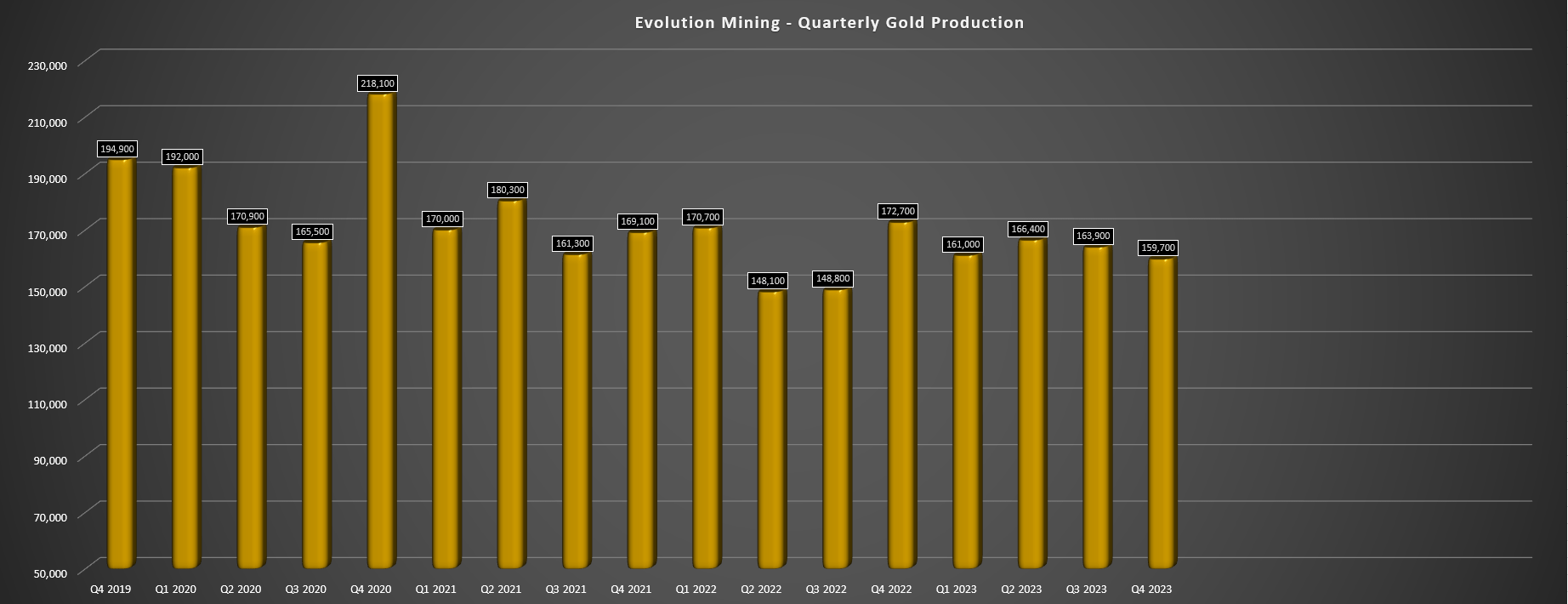

Evolution Mining released its fiscal Q4 2023 results last week, reporting quarterly production of ~159,700 ounces of gold and ~7,700 tonnes of copper, a significant decline from ~172,200 ounces of gold and ~15,300 tonnes of copper in the year-ago period. As the chart below shows, this was the worst quarter of FY2023 despite the company typically finishing on a strong note, and this was despite what should have been a much better year for its Red Lake Mine and what was a record year for its Cowal Mine with the asset benefiting from higher grade ore from Cowal Underground. The reason? As noted earlier, Ernest Henry didn't ramp up to full capacity until the end of June, putting a severe dent in total production. And making matters worse, Red Lake didn't finish as strong as expected, with just ~31,600 ounces produced.

Evolution Mining - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

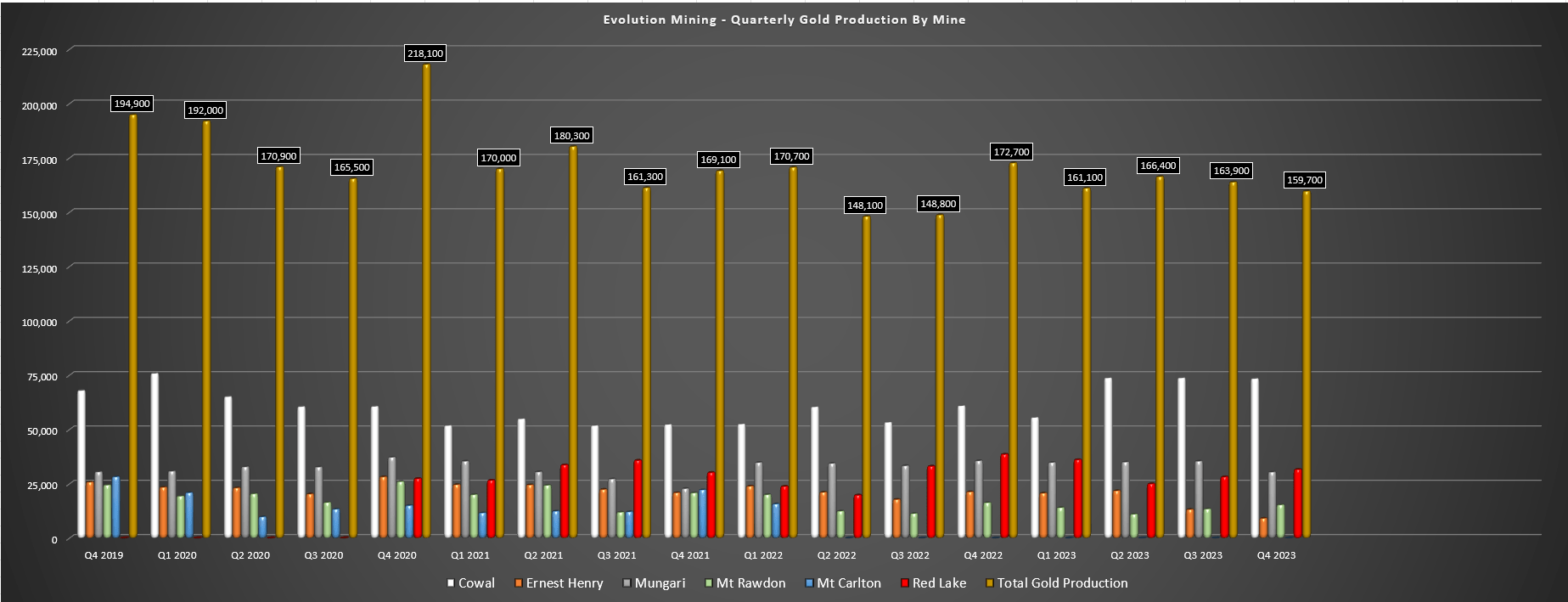

Digging into the results a little closer, the star performer was Cowal with quarterly production of ~73,400 ounces of gold which helped the mine to deliver record production under Evolution ownership of ~276,300 ounces. The phenomenal performance was driven by significantly higher grades and improved recoveries with a ramp up in production at Stage H and the start of production from the much higher-grade Cowal Underground. This higher grade ore delivered to the mill helped to offset the slight dip in throughput (~8.63 million tonnes vs. ~8.64 million tonnes), and underground mine production in Q4 came in at an impressive ~145,000 tonnes at 2.34 grams per tonne of gold (albeit slightly behind fiscal Q3 2023 levels), helping the asset to finish the year strong (Q4 output up 21% year-over-year) with industry-leading all-in sustaining costs of A$1,138/oz. Just as importantly, FY2024 is expected to be a huge year, with guidance of ~320,000 ounces at sub A$1,300/oz costs.

Evolution Mining - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

However, while Mungari and Cowal had solid years overall, Ernest Henry finished the year on a weak note with fewer tonnes mined and processed and much lower grades (copper grades of 0.88% vs. 0.99%). The result was that production came in at just ~9,100 ounces of gold and ~7,700 tonnes of copper, less than half of the ~21,300 ounces of gold and just over 50% of the copper production (~15,300 tonnes) in the year-ago period. And given the increased sustaining capital in the period (A$25.2 million vs. A$6.2 million), all-in sustaining costs soared, with a further impact from a lower realized copper price given the softness in the commodity during the June quarter. On a positive note, production has ramped up with a much better year on deck, with Evolution guiding for ~80,000 ounces of gold and ~50,000 tonnes of copper, a material increase from the ~64,700 ounces of gold produced in FY2023 due to the brutal finish related to the flooding in March.

{kind=link}

Finally, at its Red Lake Mine in Ontario, Canada, it was another disappointing year. This was evidenced by annual production of ~120,800 ounces at all-in sustaining costs of A$2,620/oz, which was only a minor improvement from an output standpoint the ~115,300 ounces produced in FY2022. Worse, this was a massive miss vs. the FY2023 guidance of 160,000 ounces at A$1,880/oz and although FY2023 should be much better at ~170,000 ounces, this is 15% below the previous FY2024 guidance outlook of 200,000 ounces provided last year. In fairness, Evolution reported a record ~4,170 meters of development in fiscal Q4 to give the mine momentum heading into FY2024, and fiscal Q4 guidance was lower because of an unplanned ore pass outage in Cochenour. That said, this was a ~3,500 ounce headwind and still wouldn't have placed the company anywhere its FY2023 guidance when adjusting for this hiccup.

{kind=link}

The good news is that Evolution has since appointed John Penhall as VP of Red Lake Operations, providing strong leadership to this underperforming asset, with Penhall previously being GM at Cowal and GM of Evolution's Australian mines. In addition, the company is in the process of completing a right-sizing of its workforce to sync up with its reduced fleet, which is expected to translate to a 10% reduction in the workforce and annual savings of A$12 million. The take-away is that while Red Lake may look like a struggling asset at its current production rate with costs well above the industry average (~US$1,755/oz), this should be a much better-looking operation with a 40% higher production rate and lower sustaining capital this year, with the potential to finally bring all-in sustaining costs [AISC] below A$2,000/oz [US$1,340/oz]. And given that this is Evolution's highest-cost asset by a wide margin, this will provide a boost to margins if executed successfully.

Costs & Margins

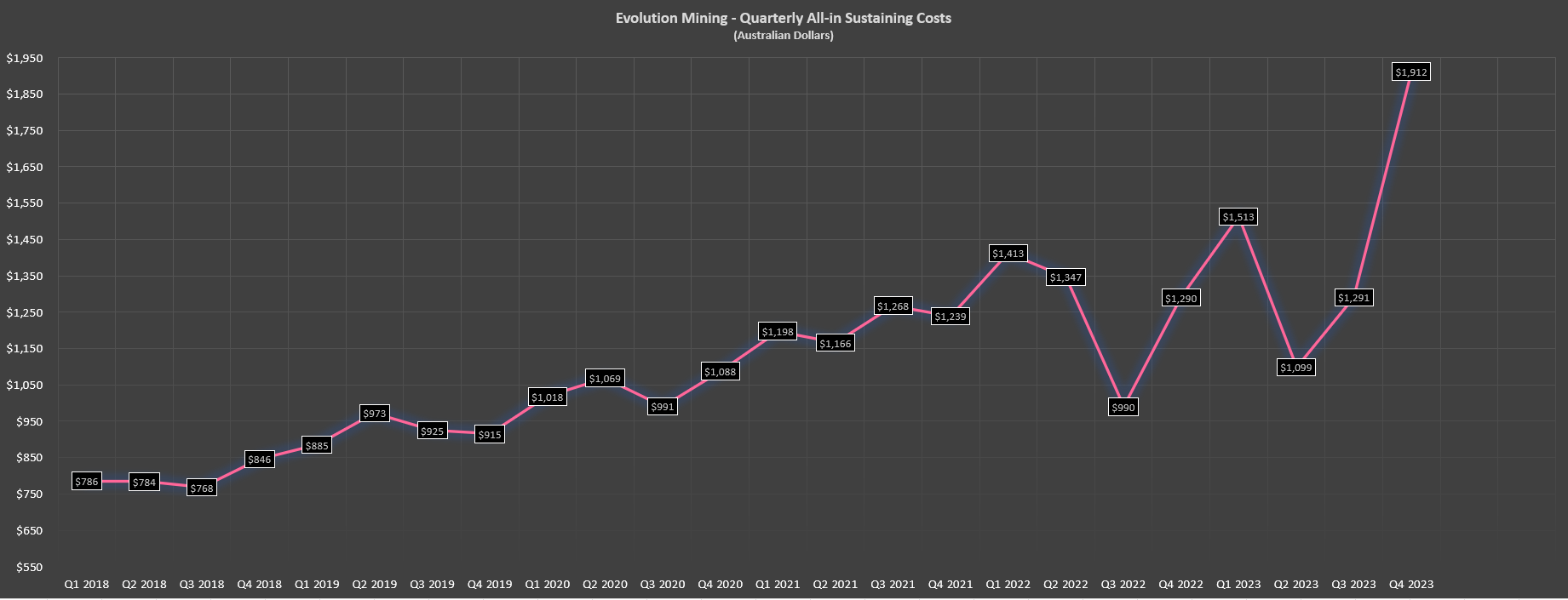

Moving over to costs and margins, fiscal Q4 was not a pretty quarter, with all-in sustaining costs soaring to A$1,912/oz, a massive deviation from a range of A$915/oz to A$1,513/oz over the past three years. However, this spike in costs was related to this being an abnormally difficult quarter for Evolution, with several things working against the company. For starters, its ultra high-margin Ernest Henry Mine had a weaker quarter due to the slow ramp-up from the flooding event, with lower gold and copper production and a lower average realized copper price weighing on its costs. The result of reduced by-product credits and less contribution was that AISC soared to A$2,286/oz, a severe departure from the [-] A$2,137/oz costs reported last year. Fortunately, Ernest Henry is back to full capacity as of the end of June after its restart on April 18th, and on track to deliver a solid year and help pull down Evolution's AISC.

Evolution Mining - Quarterly AISC (Company Filings, Author's Chart)

{kind=link}

The second headwind in fiscal Q4 2023 was that Red Lake didn't deliver to expectations because of the unplanned ore pass outage discussed previously, with the ~11% lower production putting a dent in its expected cost profile. However, like Ernest Henry, this was a rare event that is not an accurate representation of the mine's overall profitability, and it was a solid quarter otherwise at Red Lake. Finally, the third item that contributed to the higher costs in fiscal Q4 was elevated sustaining capital, with sustaining capital of A$73 million in fiscal Q4 2023, a 66% increase year-over-year. So, with lower overall production, less by-product credits, and a material increase in sustaining capital, it's no surprise that costs blew out to the upside and put a severe dent in fiscal Q4 margins which dipped to A$857/oz (A$1,201/oz in fiscal Q4 2022).

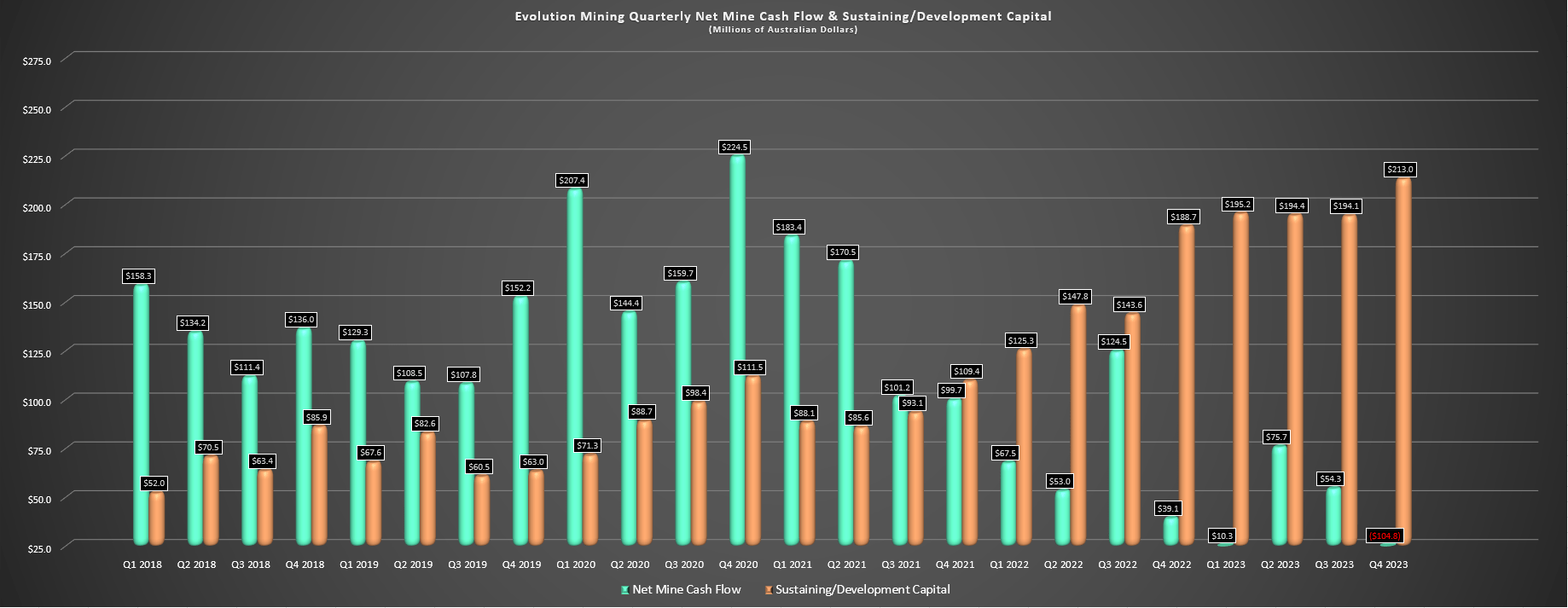

Evolution Mining - Quarterly Net Mine Cash Flow & Capex (Company Filings, Author's Chart)

{kind=link}

Given the weak quarter operationally and the elevated capex in the period, it's no surprise that the financial results were just as ugly. As shown above, Evolution Mining reported net mine cash flow of [-] A$104.8 million in fiscal Q4, a significant decline from the A$39.1 million reported in the year-ago period despite the benefit of a higher gold price. This performance was especially disappointing, given that Cowal had a solid year, generating over A$300 million in operating cash flow in its first year benefiting from higher-grade underground ore. Unfortunately, given the weak Q4 report with little help from Ernest Henry, Evolution's FY2023 results disappointed, with annual net mine cash flow down 87% year-over-year to A$35.5 million and group cash flow negative at A$116 million vs. A$284.1 million and A$110.6 million in FY2022, respectively.

2024 Outlook

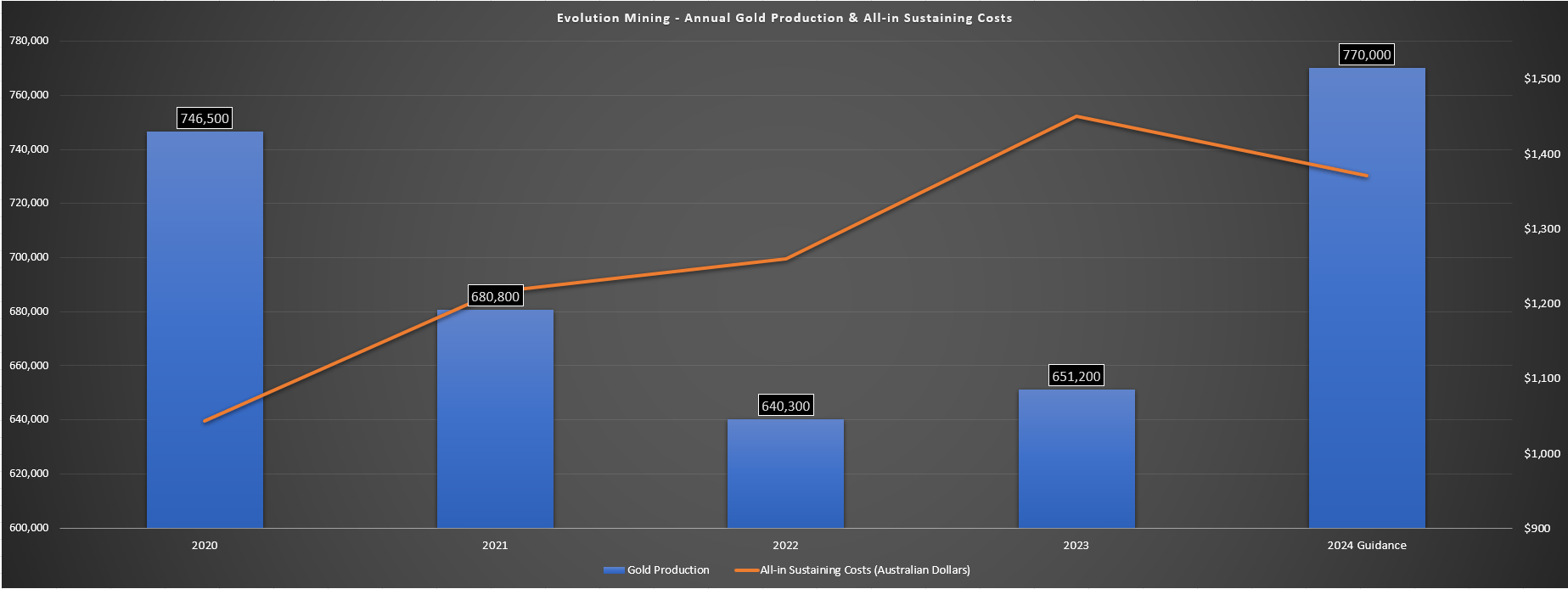

Fortunately, while FY2023 was a tough year for Evolution despite Cowal's solid performance, the FY2024 outlook is much brighter. This is because the company is expecting to see a full year of contribution with 100% ownership from Ernest Henry (its lowest-cost mine), it's set to see a monster year from Cowal with ~320,000 ounces at industry-leading all-in sustaining costs of sub US$870/oz, and Red Lake (highest-cost asset) should finally start performing closer to its initial expectations. The combination of increased production from its high-margin Cowal Mine and ultra high-margin Ernest Henry Mine, combined with increased production from Red Lake should allow Evolution to return to its industry-leading cost profile from July 2023 to the end of June 2024 (FY2024). And while the company has struggled to meet guidance the past two years, even a miss vs. FY2024 guidance will translate to a significantly better year.

Evolution - Annual Production & AISC & FY2024 Guidance (Company Filings, Author's Chart)

{kind=link}

As shown in the chart above, Evolution Mining is guiding for FY2024 production of ~770,000 ounces at all-in sustaining costs of A$1,370/oz [~US$920/oz], and this is despite expectations of 7% higher sustaining capital using its guidance midpoint of A$210 million (FY2023: A$196.9 million). And given that the company has missed on guidance in the past two years, it is likely being a little more conservative than it has been to ensure it doesn't miss guidance for a third consecutive year in my view. Notably, Evolution also noted that turnover has improved at Mungari (its asset with the highest turnover) and things finally appear to be turning the corner at Red Lake. So, assuming the gold price can hold up and Evolution Mining can execute better in FY2024, the difference in its FY2024 financial results vs. FY2023 should be night and day, with the potential to generate up to A$1.2 billion in operating cash flow.

Valuation

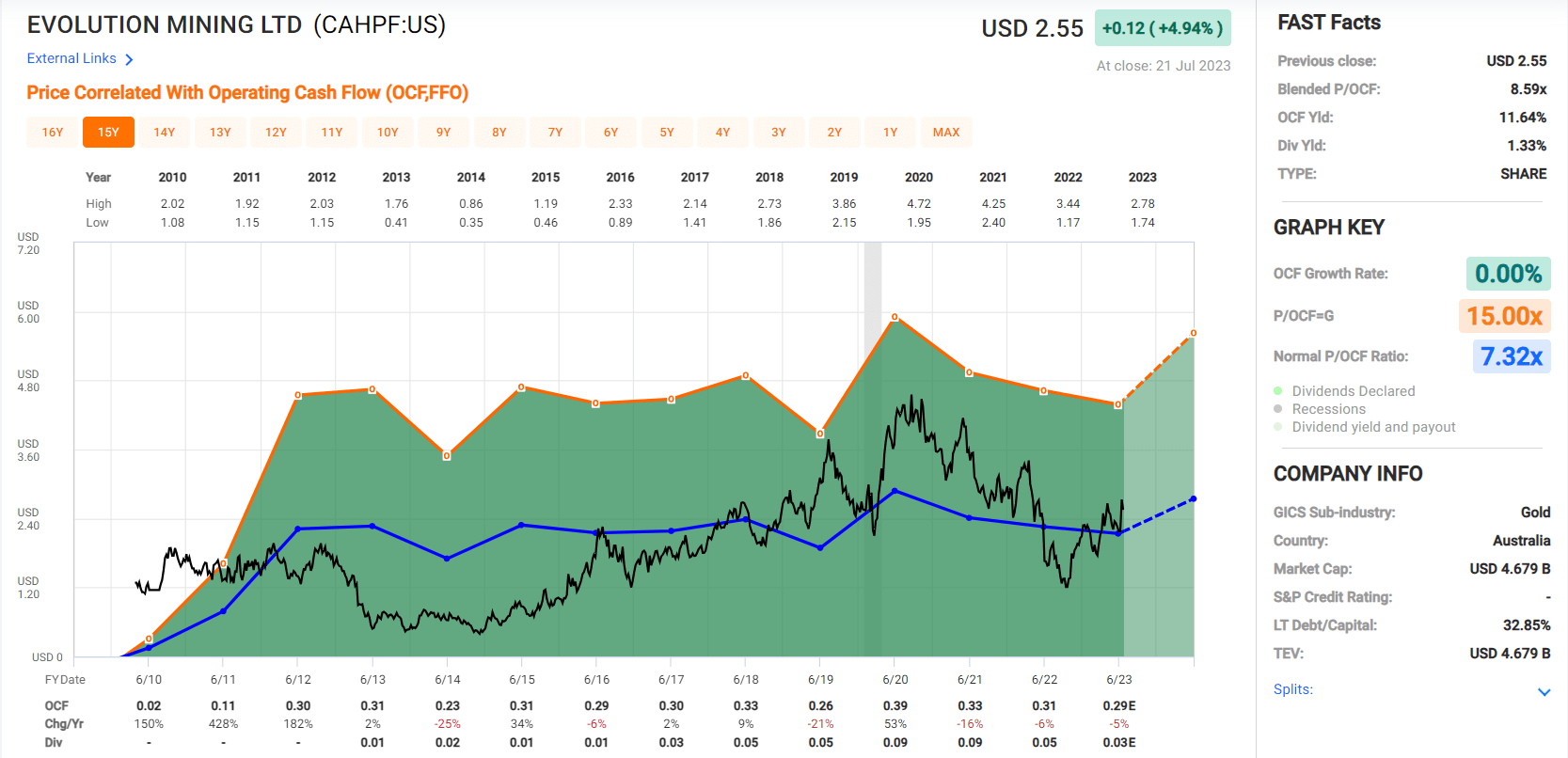

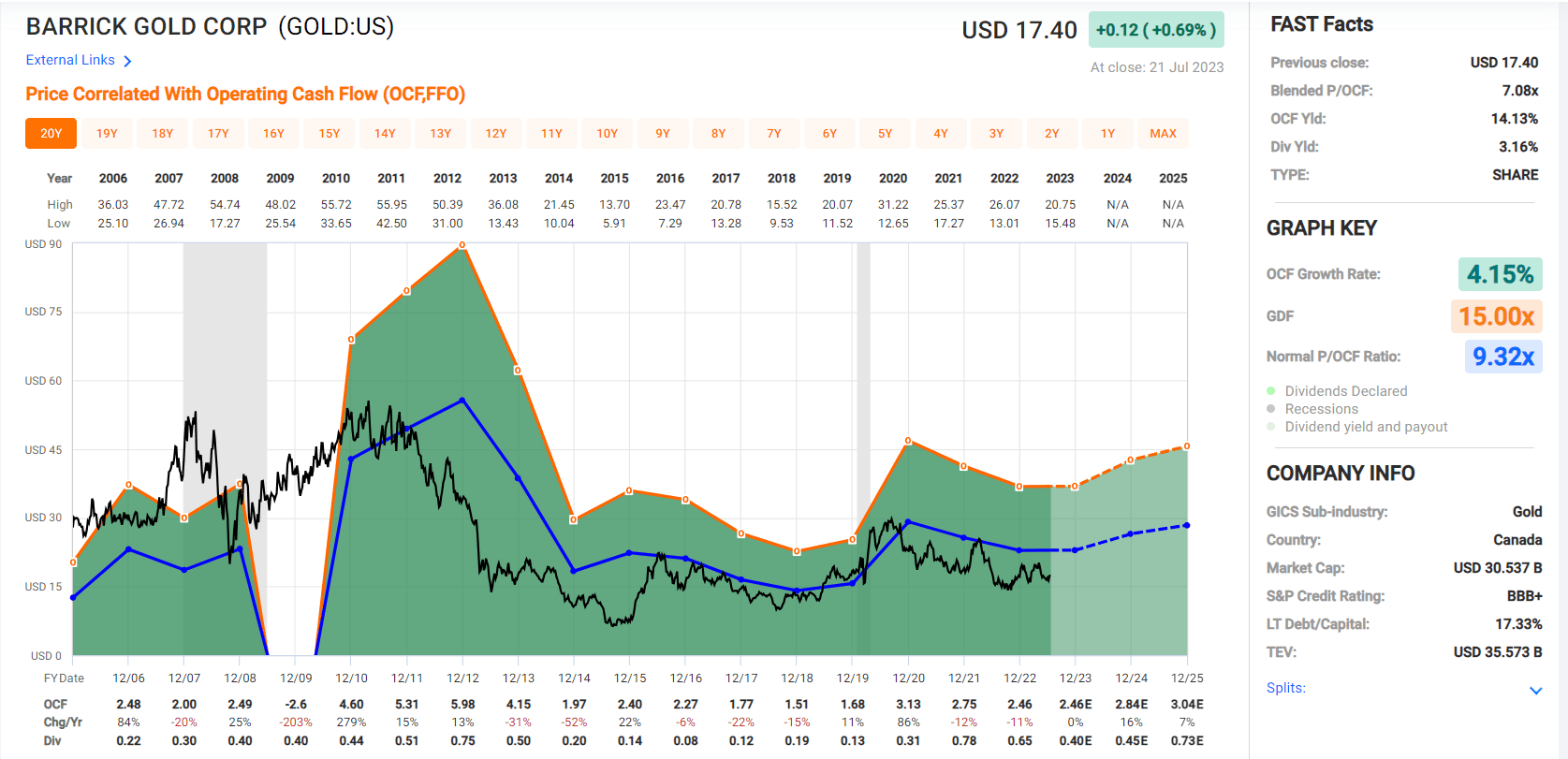

Based on ~1,835 million shares and a share price of US$2.55, Evolution Mining trades at a market cap of ~$4.7 billion and an enterprise value of ~$5.7 billion. This leaves the stock trading at a premium to its estimated net asset value of ~$4.0 billion despite its recent correction and ~6.3 FY2024 cash flow estimates of ~$740 million. While this is a very reasonable valuation for one of the sector's lowest-cost gold producers that operates out of solely Tier-1 jurisdictions, Evolution is more leveraged than its peers, suggesting it should trade at a lower multiple. Plus, we currently have a setup where some of the largest producers trade at very attractive multiples, with Barrick Gold ( GOLD ) trading at barely 6.0x FY2024 cash flow per share estimates while returning ~3% a year to shareholders. Hence, with Evolution well off its lows and at a higher multiple, I see Barrick as the more attractive bet on a risk-adjusted basis.

Evolution Mining - Historical Cash Flow Multiple (FASTGraphs.com) Barrick Gold - Current & Historical Cash Flow Multiples (FASTGraphs.com)

{kind=link}

{kind=link}

Using what I believe to be a more conservative multiple for Evolution Mining of 7.0x forward cash flow and FY2024 estimates of US$0.40, I see a fair value for the stock of US$2.80, pointing to a 10% upside from current levels. And although this may be attractive to some investors, I am looking for a minimum 35% discount to fair value for mid-cap producers in Tier-1 jurisdictions to ensure an adequate margin of safety. If we apply this discount to Evolution's estimated fair value of US$2.80, this translates to a low-risk buy zone of US$1.80 or lower, suggesting that the stock would need to decline towards its March 2023 lows to become more attractive. Obviously, there's no guarantee that the stock pulls back by this magnitude, but I prefer to pay the right price or pass entirely, and for now I don't see nearly enough margin of safety here at US$2.55.

Summary

Evolution Mining's fiscal Q4 and FY2023 results provided little to write home about and while the company gets a pass on the major weather event at Ernest Henry, the performance at Red Lake has continued to disappoint, overshadowing what was a great year for its Cowal Mine. However, the pieces finally appear to be in place for a turnaround at Red Lake, with new leadership, improved development rates, and access to higher-grade Campbell ore. So, while it's easy to be negative about the FY2023 results, this was an abnormal year with the company's strongest cash flow generator unable to pick up any slack. Plus, FY2024 should be a much better year at multiple operations, and Mungari's future looks quite bright with the planned expansion approved.

All that being said, I believe the best time to buy miners is when they're hated and deeply undervalued, and while sentiment may be negative short-term for Evolution following a miss on FY2023 guidance, the stock is nowhere near hated, with Evolution Mining still up ~100% from its Q4 2022 lows. Meanwhile, from a valuation standpoint, the stock may be reasonably valued relative to some of its intermediate peers that have outperformed, but some of this discount is justified because of its sub-par execution over the past two years and its higher leverage. Plus, on a relative and risk-adjusted basis, larger producers like Barrick Gold look more attractively valued and are also up against easy comps after a disappointing past 12 months. So, while I would consider Evolution Mining if the stock were to dip below US$1.85, I don't see any reason to pay up for the stock here at US$2.55.

For further details see:

Evolution Mining: A Tough Finish To A Challenging Year