CAHPF - Evolution Mining: Ernest Henry Continues To Grow

2023-09-17 07:23:04 ET

Summary

- Evolution Mining has continued its strategy of growing through acquisitions, acquiring assets that are non-core to other producers' assets and divesting less robust assets.

- Unfortunately, the Red Lake deal has not paid off and has overshadowed success at Cowal, but the continued resource growth at Ernest Henry suggests the 2022 deal was a home-run.

- In this update, we'll look at resource growth at Ernest Henry, the asset's bright future & whether CAHPF is offering a margin of safety after its ~20% correction.

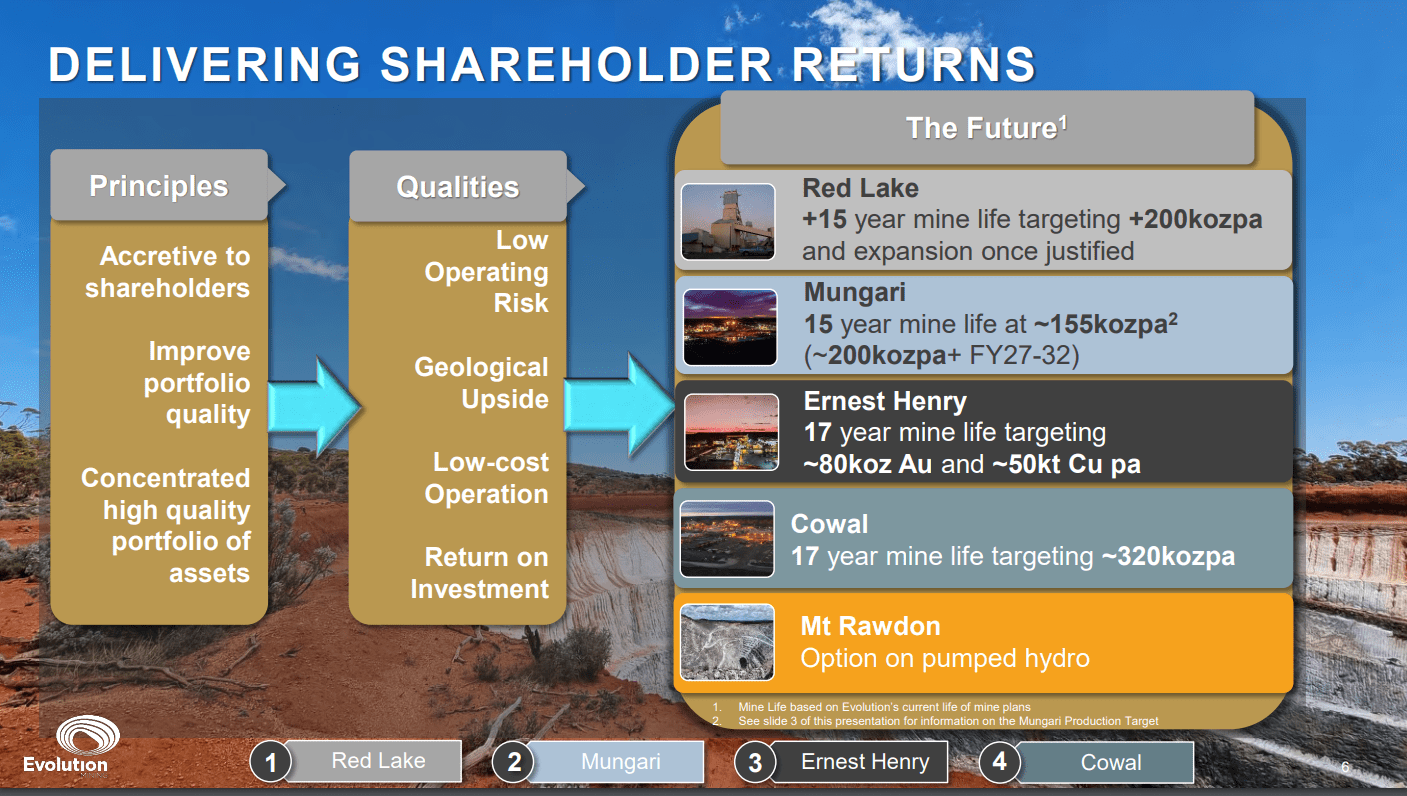

It's been a busy past two years for Evolution Mining ( CAHPF ), with the company continuing its strategy of growing through M&A by adding non-core assets held by larger producers. This began with the acquisition of Cowal and Mungari in 2015 (with the former transitioning to underground), followed by the acquisition of Red Lake in 2019, additional processing capacity in the camp with Bateman in 2021 (former Phoenix Mine), the addition of key assets next door to Mungari in mid-2021, and the acquisition of the remaining interest in Ernest Henry (early 2022). Simultaneously, the company has let go of less robust assets, with the divestment of Mt. Carlton (2022), Cracow (2020), Edna May (2018) and Pajingo (2017). These moves have created a portfolio of larger and lower-cost assets, and Cowal is looking like a home-run for US$550 million (even if it resulted in meaningful share dilution), with the asset set to produce ~320,000 ounces this year at sub $850/oz AISC, making this one of the best gold mines in Australia from a profitability standpoint.

Unfortunately, the Red Lake Complex & Bateman acquisitions have not paid off to date, and four years after its acquisition and with the benefit of another mine and plant, it's still miles below the low end of its long-term goal of 300,000 to 500,000 ounces per annum and at barely half of its FY2026 goal (June 2025 - June 2026) of ~350,000 ounces per annum. This is certainly quite disappointing even if the asset is we're seeing green shoots at this high-cost mine. However, while Red Lake may not have panned out to date, taking full ownership of Ernest Henry is looking like a home-run, with it looking like the mine life will be extended to 2040 (17 years), up from the ~8-year mine life envisioned previously. In this update, we'll dig into the recent PFS, continued resource growth, and how Evolution Mining stacks up relative to peers on valuation.

{kind=link}

All figures are in United States Dollars unless otherwise noted at a 0.65 AUD/USD exchange rate.

FY2022 Results & Ernest Henry PFS

Evolution Mining released its FY2022 results last month, reporting annual production of ~651,200 ounces of gold at industry-leading costs of ~$945/oz despite a tough year at its flagship operation, Ernest Henry. This was related to extreme weather that led to a temporary evacuation, but the results were helped by a massive year from Cowal, which has an even stronger year on deck in FY2024 with higher grades from Cowal Underground. And while Ernest Henry was briefly sidelined (~6 weeks) due to flooding resulting in a $100+ million impact on sales, the asset was still the lowest-cost producer sector-wide, with FY2023 production of ~64,700 ounces at [-] ~$1,500/oz, easily beating out other low-cost mines like Cadia at sub $100/oz costs, Fosterville at sub $500/oz (H1 2023), and several mines in Polyus' portfolio that also reported sub $650/oz AISC (Olimpiada, Blagodatnoye, Verninskoye). However, the bigger news was the recent PFS released for Ernest Henry supplemented by a further resource update last month which pushed resource tonnes above 100 million.

{kind=link}

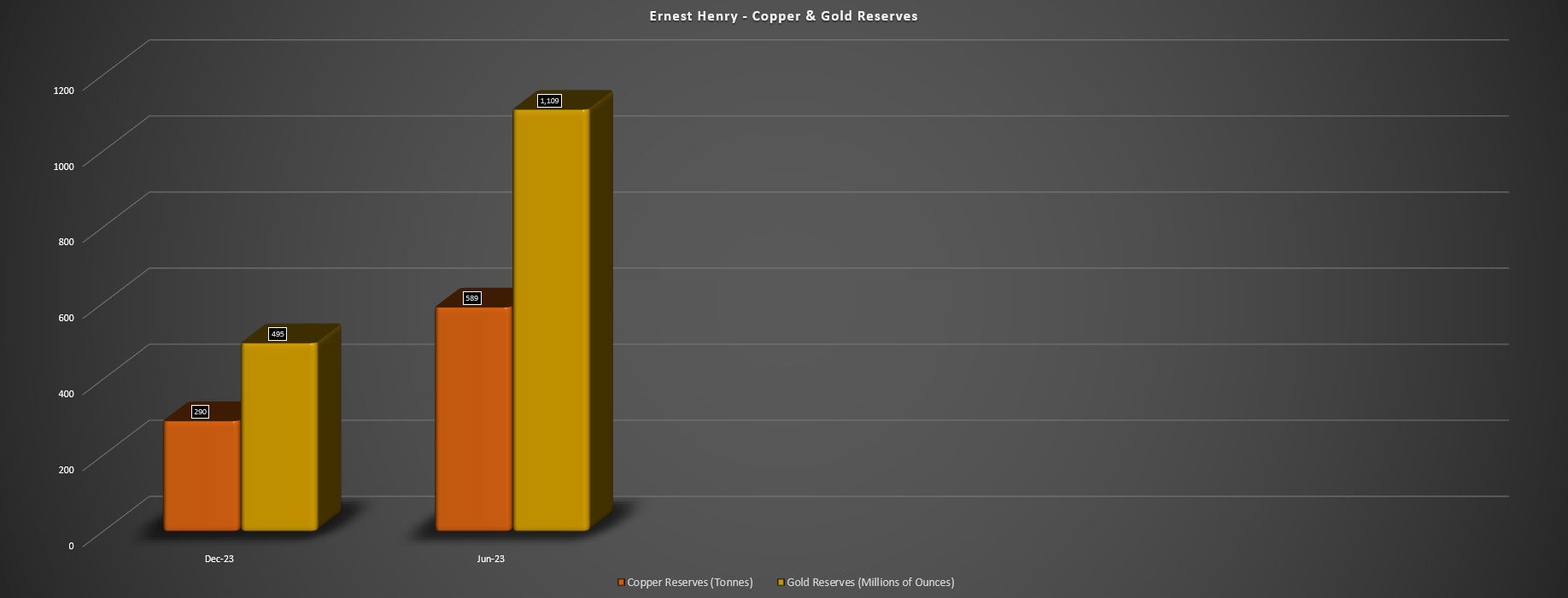

Beginning with the Pre-Feasibility Study, Evolution reported extremely robust economics with the PFS delivering an incremental NPV of ~$850 million (~33% IRR) even using a conservative gold price of $1,750/oz. This was driven by a doubling in the asset's total reserves to ~77.4 million tonnes at 0.76% copper and 0.45 grams per tonne of gold (~589,000 tonnes of copper and ~1.11 million ounces of gold), translating to well over a 16+ year mine life assuming a constant throughput rate of ~6.0 million tonnes per annum. Notably, this doubling of the reserve vs. year-end was despite mining depletion and capital expenditures to extend the mine life are relatively modest at ~$325 million (high end of estimated project capital). Just as importantly, the payback is less than one year at spot gold prices, given that the mine life extension will generate revenue from trucking prior to the commissioning of the new underground crusher.

As noted by Evolution Mining, the plan is for levels to be developed between 1100 meters RL and 750 meters RL utilizing the same mining method (sub-level caving). The addition of the new crusher will be near the base of the production horizon, connecting to the existing hoisting shaft (6+ million tonnes per annum) using an extension of the associated conveyor system. The company will also need to complete upgrades to ventilation and dewatering systems and workshops, as well as TSF raises to support the longer mine life. In addition, Evolution noted that while conventional trucking vs. a crushing/conveying system were both viable options, it is leaning towards crushing and conveying given that it offers greater economic upside, especially if resource growth continues (which looks highly likely).

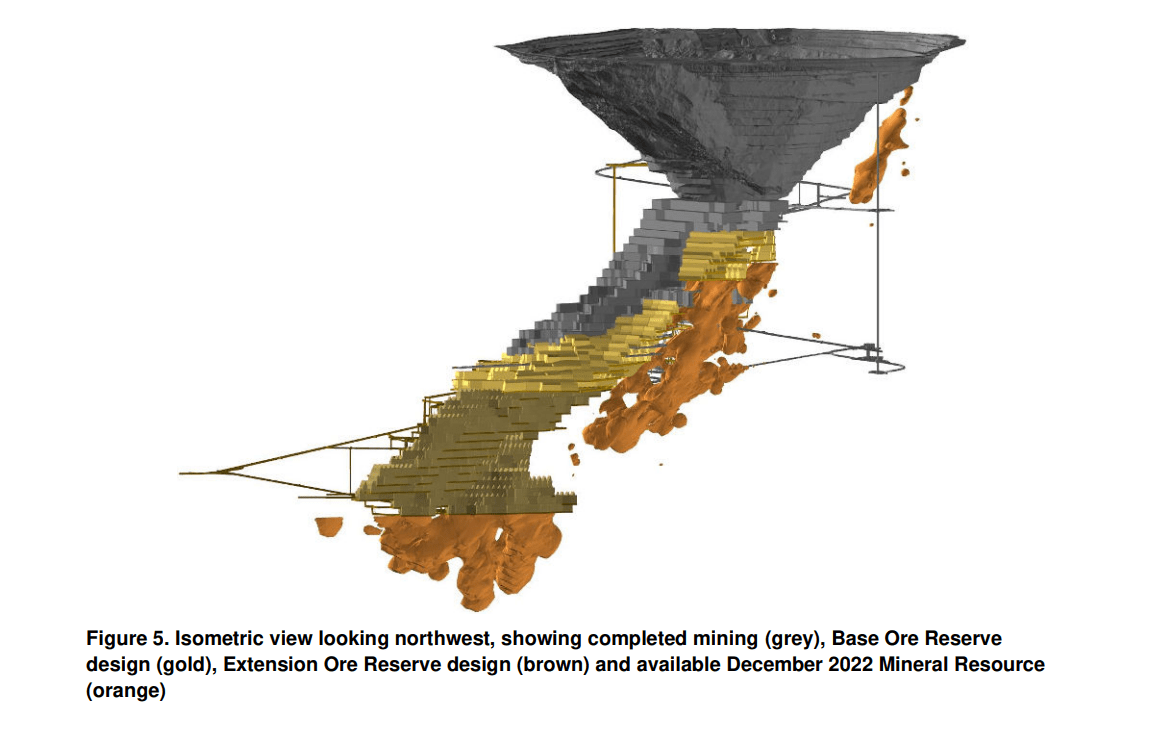

Ernest Henry Pit, Ore Reserve Design & Resources (Orange) - Company Presentation

{kind=link}

Sub-level caving is best suited for steeply dipping ore bodies and is an ultra-low cost underground mining method, allowing Ernest Henry to maintain an ultra-low cut-off of ~0.70% copper-equivalent, well below the 4.0+ gram per tonne gold cut-offs for most underground mines sector-wide.

Based on the economics from the recently released PFS, the value is an additional US$0.46 per share to Evolution Mining (~$850 million / 1.84 billion shares) even using conservative gold prices, which certainly validates the company's decision to take full control of this asset last year, a move that may have seemed bold at the time with the asset having already produced for ~25 years (open-pit began in 1998) and passing from multiple operators. In summary, I see the PFS as a great outcome for Evolution Mining, with the ability to access an additional ~655,000 ounces of payable gold at deeply negative AISC, making these very valuable ounces regardless of the relatively low production profile on a gold-only basis (~80,000 ounces per annum).

Continued Resource Growth

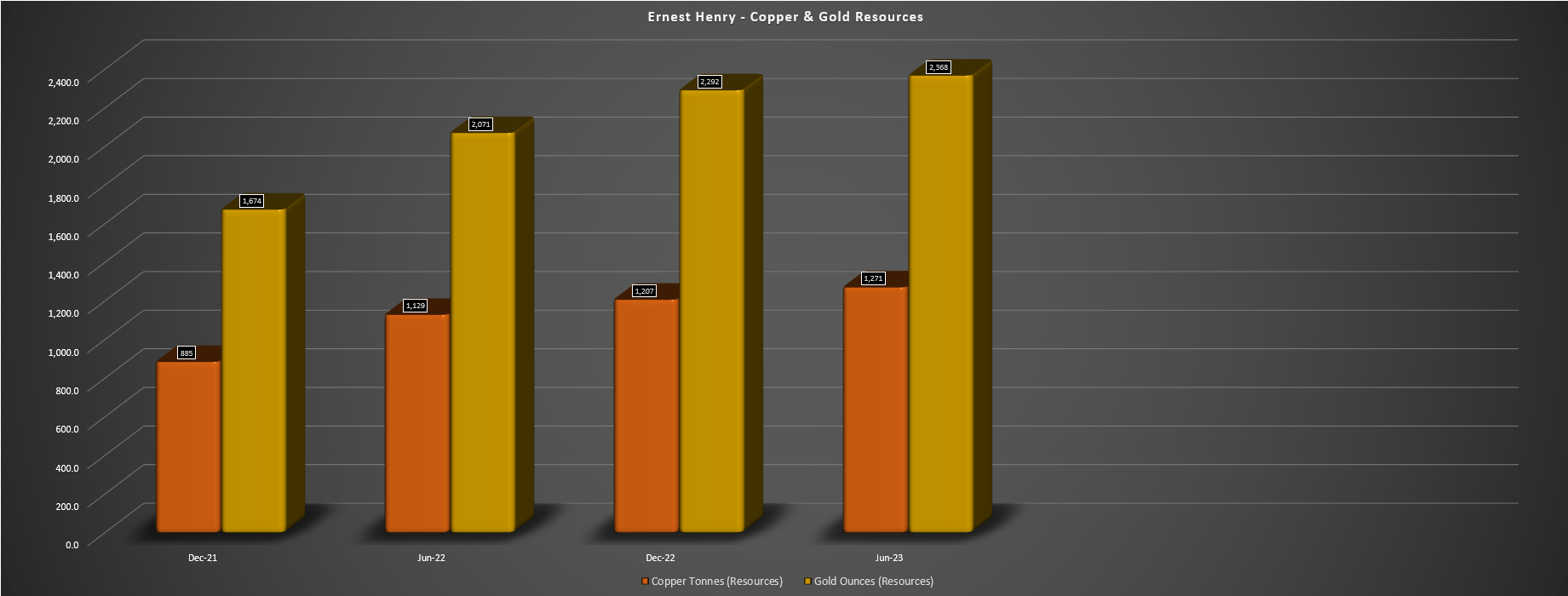

Although the PFS release was certainly positive when combined with the mine life extension at Mungari also released this summer, Evolution noted that it saw a high likelihood of extensions to mineralization above the December 2022 resource estimate. In some cases it's best to be skeptical of these types of forward-looking statements, but Evolution has certainly delivered on its promises, and especially its statement in FY2021 that the current drill program hoped to expand to deliver 3-5 years of mine life extension below 1200 meters RL. In fact, as the below chart shows, resources have increased nearly ~40% from December 2021, with the current resource sitting at ~1.27 million tonnes of copper and ~2.37 million ounces of gold, up from ~885,000 tonnes and ~1.67 million ounces, respectively. Meanwhile, reserves have more than doubled, increasing to ~589,000 tonnes of copper and ~1.11 million ounces of gold.

Ernest Henry - Copper & Gold Resource Progression - Company Filings, Author's Chart Ernest Henry - Copper & Gold Reserves - Company Filings, Author's Chart

{kind=link}

{kind=link}

Digging into the numbers, the most recent update added ~76,000 ounces of gold and ~63,000 tonnes of copper to resources, more than replacing mined depletion in FY2023, with gold and copper resources up by 3% and 5%, respectively (net of mined tonnes). The company noted that the bulk of this growth came from connecting Ernie Junior to the lower lenses of the Main Zone, in addition to expansion of the Main Zone below 775 meters RL. However, the mineral resource estimate only includes 26 new holes from January to March (drilling was impacted by the flooding and subsequent evacuation), and there's considerable upside to this resource from depth extensions below the Main Zone and between the Main Zone and Ernie Junior as well as the potential to fill in Bert which could offer a new parallel orebody to the current reserve base.

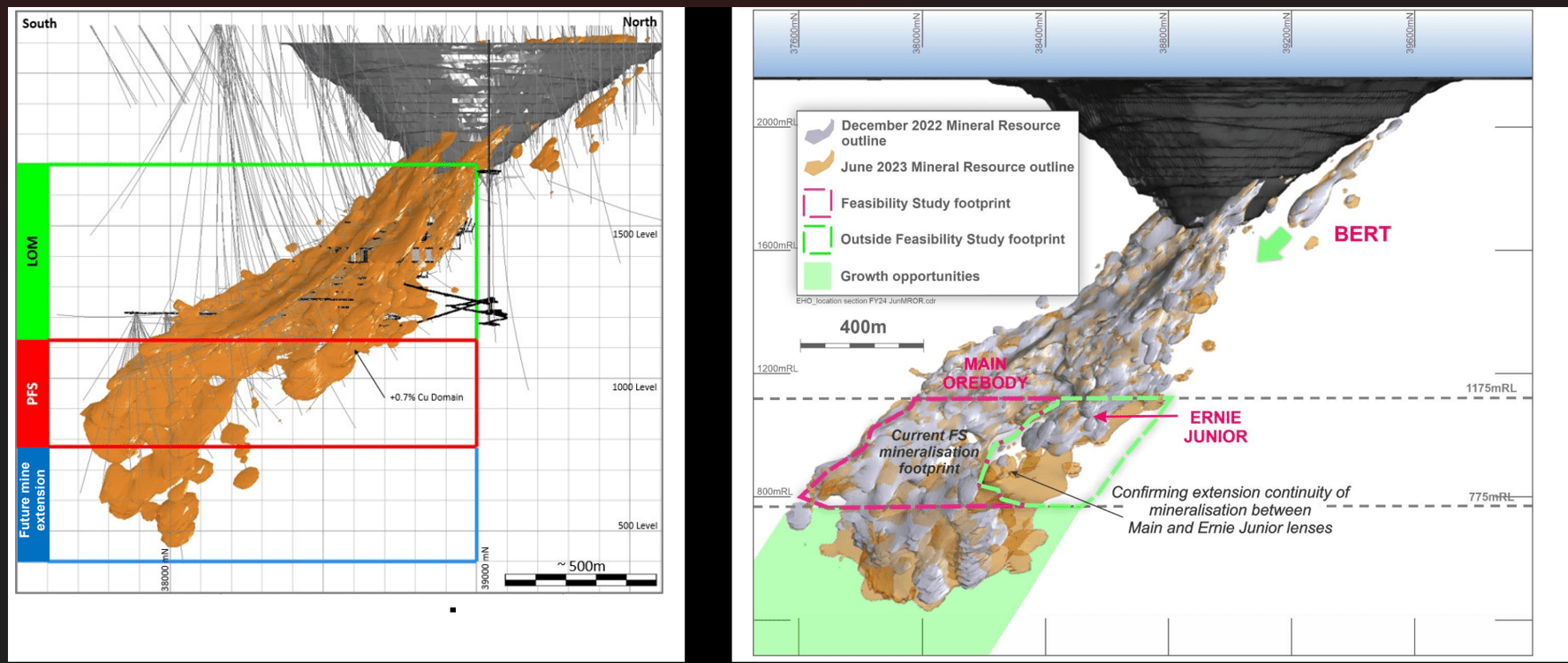

Ernest Henry - December 2022 Resource, June 2023 Resource, Ex-FS Footprint & Growth Opportunities - Evolution Website

{kind=link}

Digging into the above image, we can see how Ernest Henry has progressed from the left image to the right image, with considerable growth below 1100 meter RL, with the additional opportunity to fill in the Ernie Junior to Main Zone connection area (green dashed area). In addition, the ore body has become much meatier at depth, pointing to the potential for further extensions below 775 meters RL to potentially extend the mine life past 2044. Finally, the company hasn't even scratched the surface at Bert (closer to surface near the mined out open-pit), with highlight intercepts of 64 meters at 0.76 grams per tonne of gold and 1.39% copper and 50 meters of 0.68 grams per tonne of gold and 1.12% copper, with even higher-grade intercepts along the Bert Hanging Wall at even higher gold grades.

This is extremely encouraging, and given the considerable endowment at the main underground ore body, the down-plunge potential of Bert shouldn't be ignored, with the possibility of further growth in resources and NPV at this key operating asset. And while FY2023 results at Ernest Henry may have come in below expectations due to lower copper prices and the necessary evacuation, this has been easily made up for with continued exploration success and significant resource growth. To summarize, Evolution looks to be solidifying its position as a low-cost producer looking out to 2040 with multiple low-cost assets (Mungari, Cowal, Ernest Henry mine life extension), and if it can turn around the one problem child in the portfolio, Red Lake, Evolution could potentially maintain one of the lowest-cost profiles sector-wide, with AISC consistently below $900/oz despite the impact of three years of inflationary pressures.

{kind=link}

Let's take a look at the valuation and see whether this is priced into the stock:

Valuation

Based on ~1.84 billion shares and a share price of US$2.35, Evolution Mining trades at a market cap of ~$4.3 billion and an enterprise value of ~$5.5 billion. This makes it one of the most expensively valued 600,000 to 800,000 ounce producers (FY2024 guidance: ~770,000 ounces), well ahead of SSR Mining ( SSRM ) at ~$3.0 billion (FY2024 guidance: ~740,000 ounces), OceanaGold ( OCANF ) at ~$1.7 billion (FY2024 guidance: ~600,000 ounces), and Iamgold ( IAG ) at ~$1.7 billion. At first glance, this might suggest that Evolution is overvalued, trading at double the average market cap of peers in the 600,000 ounce to 800,000 ounce peer group. However, like Northern Star ( NESRF ), Evolution is unique for several reasons, with two clear differentiators being its cost profile and jurisdictions. Not only is it the lowest-cost miner among 500,000+ ounce producers with FY2024 AISC expected to come in near ~$900/oz, but it also operates out of solely Tier-1 ranked jurisdiction profiles (Australia & Canada), suggesting the stock should trade at a premium.

{kind=link}

That said, while a premium is justified, Evolution Mining is one of the most leveraged miners sector-wide (~$1.2 billion in net debt) and the premium is excessive relative to its peers. This is because the stock trades at over 23x FY2024 free cash flow estimates on an EV/FCF basis, and also trades at ~1.1x P/NAV based on an estimated net asset value of ~$4.0 billion. And even if we assume a fair multiple is 1.30x P/NAV, this leaves very little margin of safety relative to a fair value estimate of US$2.80. So, while Evolution Mining is certainly one of the lower-risk names sector-wide with lower sensitivity to gold prices (industry-leading margins), long mine lives, and a very low-risk jurisdictional profile, I see much of this as priced into Evolution at current levels. In addition, with many miners trading at less than 12x forward free cash flow, it no longer stacks up attractively on a relative value basis vs. when I highlighted the stock as attractive when it sat at US$1.20.

Evolution Mining Update September 26th, 2022 - Seeking Alpha Premium/PRO

{kind=link}

It's certainly possible that I could be wrong that Evolution Mining is best to avoid chasing above US$2.40, and as we recently saw from the acquisition of Newcrest Mining ( NCMGF ), suitors will pay up handsomely for quality gold/copper assets in Tier-1 jurisdictions. That said, outside of M&A or gold hitting new all-time highs, I don't see a clear path to Evolution trading back above US$3.00 in the next 12 months. And with several of the larger producers already transacting over the past two years, M&A does not look likely. So, while I think Evolution is undoubtedly one of the better names in the sector given its superior jurisdictions, margins, and long-life assets, I would need to see a pullback below US$1.75 to become more interested, which would leave the stock offering an adequate margin of safety. Plus, when there are other high-margin producers trading at far higher free cash flow yields, I continue to see better reward/risk setups elsewhere.

Summary

Evolution Mining has improved an already strong portfolio with its continued resource growth at Ernest Henry, and this is certainly the most desirable asset to add meaningful ounces and mine life, with this being the highest-margin asset sector-wide after by-product credits with AISC coming in below [-] $1,200/oz. And given the further upside at this asset, it's certainly possible that it could continue producing past 2045, providing visibility into Evolution continuing to own one of the best assets sector-wide. However, the positive developments at Ernest Henry look mostly priced into the stock following its ~100% rally over the last 12 months, especially when comparing Evolution Mining to peers on a EV/FCF basis. Hence, if we were to see Evolution Mining rally above US$2.74 before year-end, I would view this as an opportunity to book some profits.

For further details see:

Evolution Mining: Ernest Henry Continues To Grow