CAHPF - Evolution Mining: Limited Margin Of Safety At Current Levels

Summary

- Evolution Mining is one of the best-performing gold miners since its October lows, rallying over 90% in the past 60 trading days.

- This strong performance is attributed to the fact that Evolution was one of the cheapest intermediate producers heading into Q3 and that we've seen a recovery in gold/copper prices.

- However, while Evolution has a strong 2023 ahead and is finally hitting its stride at Red Lake, an operation with significant organic growth potential, the stock looks fully valued here.

- So, while I see Evolution as a solid buy-the-dip candidate in periods when the sector is heavily out of favor, I think it's prudent to take some profits here above US$2.25.

While investors had to endure a rollercoaster ride over the past year in the Gold Miners Index ( GDX ), the past two months have made up for being thrown violently in each direction, with the GDX trouncing the S&P 500's ( SPY ) performance and soaring ~50% from its Q3 lows. One of the outperformers during this rally is Evolution Mining (CAHPF), a miner that actually broke its March 2020 panic lows despite the gold price being ~$200/oz higher. However, while this outperformance has helped investors to claw back any short-term losses, the stock is now looking vulnerable short-term above US$2.25, suggesting it might be prudent to book some profits.

Unless otherwise noted, all figures are in United States Dollars, with AUD/USD conversions at a 0.70 exchange ratio for operating costs.

A Bright Future Ahead After A Tough Year

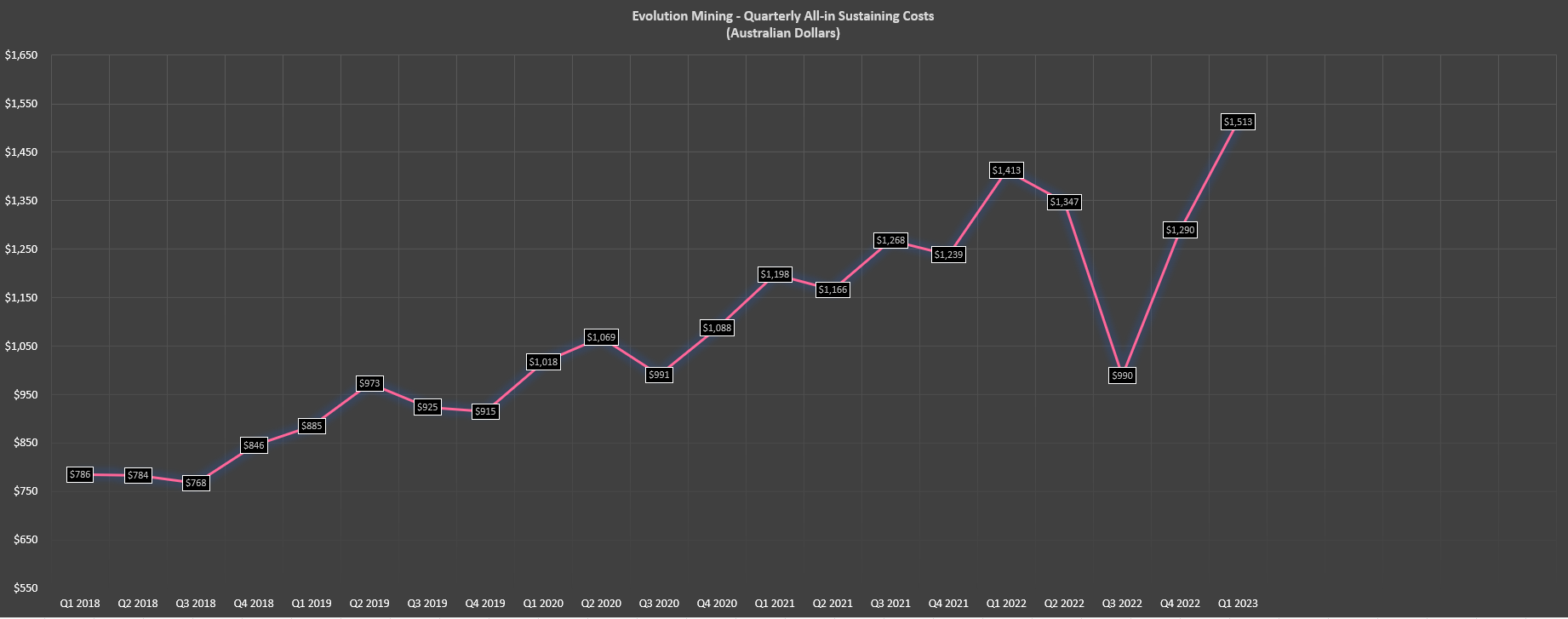

FY2022 was a year to forget for Evolution Mining shareholders from an operational standpoint, with inflationary pressures and labor tightness leading to a miss on cost guidance and a slow start at Red Lake leading to a miss on production guidance. Unfortunately, while FY2023 production is expected to rebound to ~720,000 ounces (FY2022: ~640,000 ounces), costs pressures are expected to persist, with labor costs expected to be at least 5% higher this year, resulting in a similar cost outlook (A$1,240/oz in FY2023) despite the step-up in annual production. Having said that, these costs are still well below the industry average, even if the trend is clearly up.

Evolution - Quarterly AISC (Australian Dollars) (Company Filings, Author's Chart)

{kind=link}

While Evolution's fiscal Q1 2023 all-in-sustaining costs [AISC] might have put a further dent in sentiment regarding the ability to meet its FY2023 cost outlook. However, it's worth noting that this was an unusual quarter and we should see a steady improvement in operations going forward. Not only was the Mt. Rawdon Mine impacted by heavy rainfall, but the company had multiple maintenance shuts across its operations, leading to a temporary dip in throughput. Finally, the copper price took a detour from its prior uptrend in fiscal Q1 2023, resulting in a ~$150/oz impact on costs from lower by-product credits at the Ernest Henry copper-gold mine. Fortunately, copper and gold prices have improved since - setting up a robust quarter from a cash flow standpoint in fiscal Q2 2023.

{kind=link}

Meanwhile, regarding Evolution's two major growth projects, mine development at Cowal Underground remains on budget and schedule. Plus, the company secured a long-term power supply agreement fixed for eight years, reducing uncertainty about power costs at this asset. Meanwhile, at Red Lake, a thorn in the company's side from a margin standpoint, the asset finally looks to be hitting its stride. During fiscal Q1 2023, the first stope ore from Upper Campbell (highest-grade area) was mined and processed, and grades exceeded expectations (7.9 grams per tonne gold). Meanwhile, while tonnes processed were lower in fiscal Q2 due to the Campbell Mill tertiary crushing circuit upgrade, it is now commissioned, which sets the plant up for improved performance in the future.

{kind=link}

Notably, we are still in the early innings regarding Red Lake optimization. This Canadian operation could ultimately see production lift to ~350,000 ounces long-term once fully optimized, more than double its FY2023 guidance level (~160,000 ounces). This is based on the fact that the company has ~1.6 million tonnes per annum of total plant capacity in the area (Bateman, Red Lake, Campbell mills) after a recent approval to increase Campbell Mill throughput (2,200 tonnes per day vs. 2,000 tonnes per day). So, while investors might not be elated with the state of this operation today, which is dragging on consolidated margins (FY2022 AISC: ~US$1,764/oz), I think it's unfair to judge this asset on its FY22/FY23 results while it's in its turnaround phase.

{kind=link}

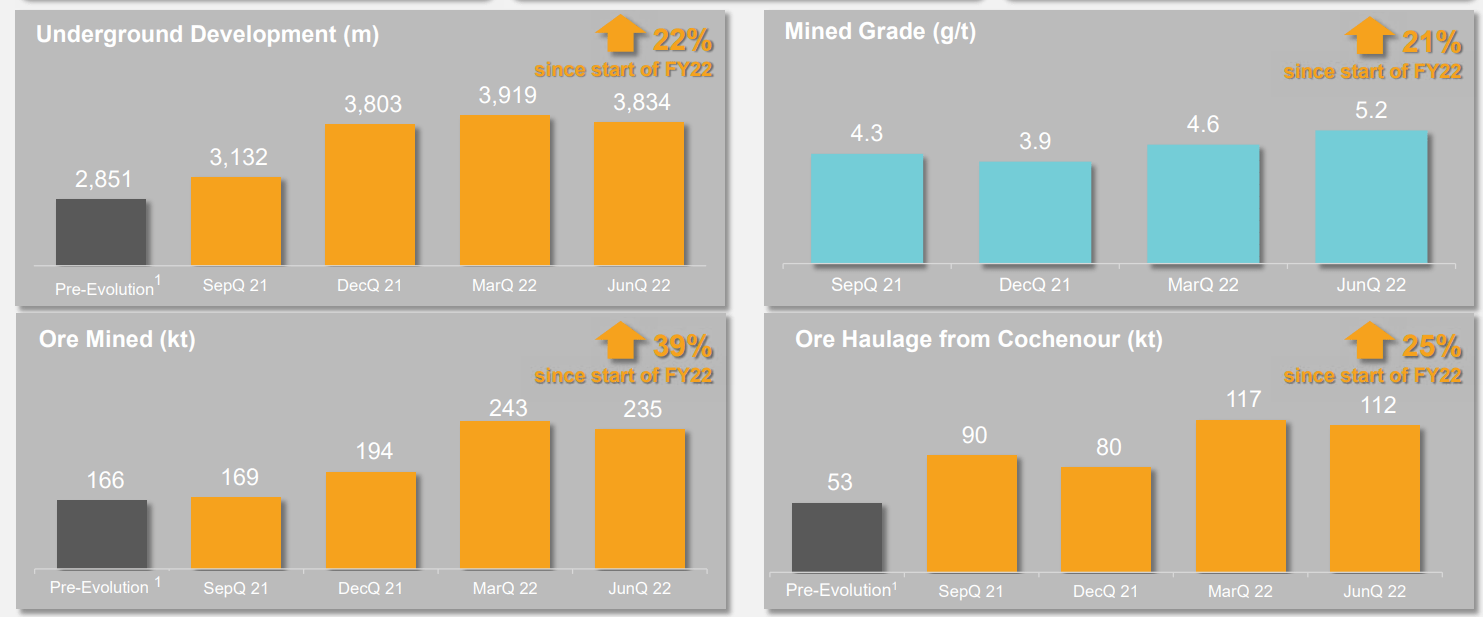

So, while AISC may remain elevated currently, and investors might still have reservations about this acquisition, we can see that under the surface, key operating metrics continue to trend in the right direction. Underground development averaged ~3,720 meters in the past three quarters, ~30% above pre-acquisition levels. Meanwhile, mined grades have consistently trended higher, and they will improve further as contribution increases from Upper Campbell, and they jumped another ~10% sequentially to 5.81 grams per tonne of gold in fiscal Q1 2023 and 6.5+ grams per tonne of gold in September 2022. As this asset benefits from economies of scale and is a more efficient operation (less mining dilution and improved productivity), we should see unit costs follow and drop materially.

To summarize, while the FY2022 results were not what investors have come to expect from Evolution and the fiscal Q1 2023 results might have spooked investors with ~$1,060/oz AISC vs. ~$870/oz guidance, I would expect consistent improvements in operations and costs going forward. As noted above, this is expected to be driven by higher grades from Cowal Underground, higher grades from Upper Campbell and increased throughput, and increased by-product credits from Ernest Henry, which is now benefiting from a rebound in copper prices, with copper prices back above A$12,000/tonne.

Recent Developments

While higher production, higher metals prices, and an improvement in the labor situation are all positive, we've seen other positive developments across the portfolio, with a major one being exploration. In November, Evolution announced new drill results from its now 100% owned Ernest Henry Mine, and the company hit highlight intercepts that included the following:

- 157.0 meters of 1.26 grams per tonne of gold and 1.62% copper

- 102.0 meters of 1.06 grams per tonne of gold and 1.39% copper

- 90.8 meters of 1.42 grams per tonne of gold and 1.54% copper

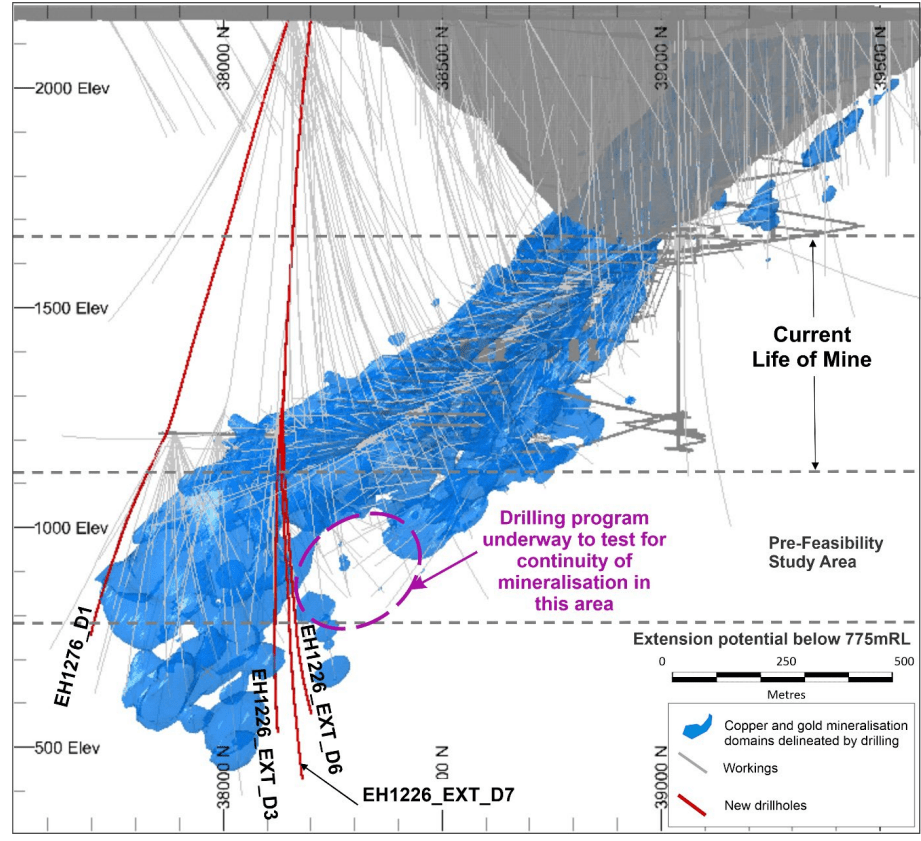

These results are exceptional, and on a gold-equivalent basis, these holes have come in well above 3.0 grams per tonne. However, it's the fact that these intersections are over significant widths and are entirely outside the current mineral resource that is the most exciting, adding meaningful tonnes at attractive grades for the company's upcoming Pre-Feasibility Study that will look at increasing Ernest Henry's already long mine life (2031). As noted by Evolution's Executive Chair, Jake Klein, these results "demonstrate the potential for mineralization to extend up-plunge and at depth."

{kind=link}

As shown in the image above, drill hole EH1276 intersected 102 meters of 1.06 grams per tonne of gold and 1.39% copper and is the southernmost intersection. Notably, it is well above the average reserve grade at Ernest Henry (0.49 grams per tonne of gold and 0.93% copper), and it could extend the mineralized domain further south than previously interpreted in the area being studied when it comes to potentially increasing the mine life at Ernest Henry. Meanwhile, the other even higher-grade intercepts have increased the potential for an up-plunge extension to the mineralized footprint and are also outside the resource base.

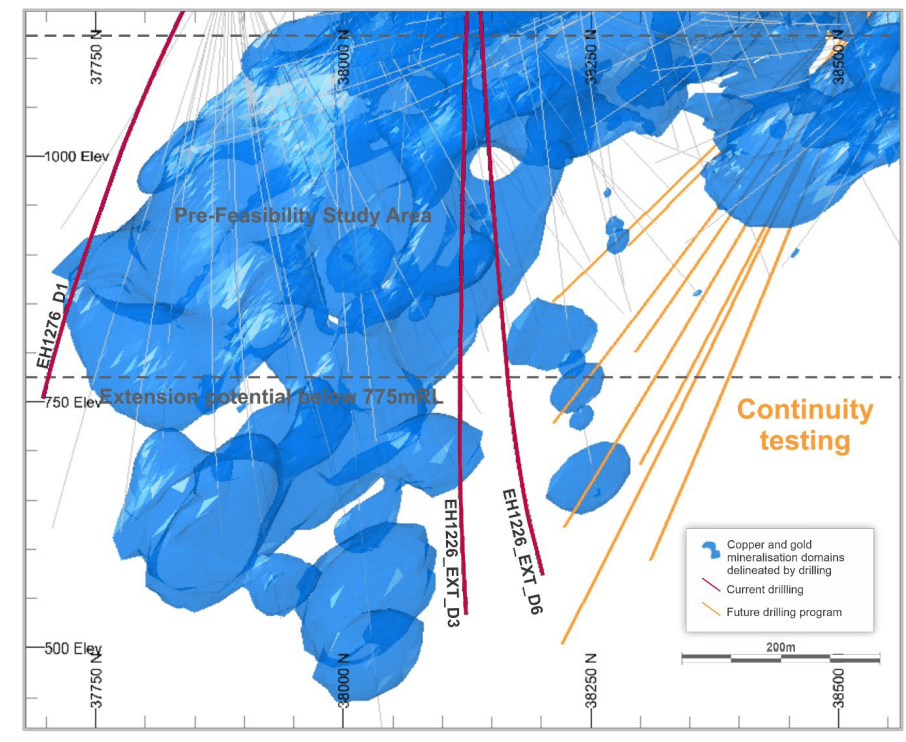

Ernest Henry Intercepts & Up Plunge Potential (Company Website)

{kind=link}

Not surprisingly, Evolution noted that follow-up drilling is underway to test this opportunity to add resources up-plunge from the previously interpreted mineralized footprint. When it comes to Evolution's consolidated cost profile, this news couldn't be more positive given that these intercepts are near current infrastructure and could increase Ernest Henry's mine life but also translate to higher grades. This means the potential for even higher margins at a phenomenal operation (negative $1,000/oz AISC), which helps drag down the company's consolidated cost profile. To summarize, these drill results are encouraging and should certainly excite investors about Evolution's future.

{kind=link}

However, while these results are positive, quite a bit of this excitement is priced into the stock, with Evolution adding ~$2.0 billion in market cap over the past two months. Let's take a closer look at the stock's valuation below.

Valuation & Technical Picture

Based on ~1,835 million shares and a share price of US$2.27, Evolution Mining trades at a market cap of $4.16 billion and an enterprise value of ~$5.0 billion. This leaves the stock trading at a significant premium to its estimated net asset value of ~$3.20 billion, with Evolution trading at ~1.30x P/NAV, a premium to larger producers like Barrick Gold ( GOLD ) and Agnico Eagle ( AEM ). While I would argue that Evolution deserves to trade at a premium to most intermediate or 1.0-2.0 million-ounce producers, given its attractive margin profile and Tier-1 jurisdictional profile, the current premium to net asset values leaves little margin of safety at current levels.

Using what I believe to be a fair multiple of 1.15x-1.25x P/NAV and basing its price target on the low end of this multiple to be conservative, I see a fair value for Evolution Mining of US$2.00, with the stock trading 14% above this level after its near parabolic rally from its October lows. Meanwhile, the stock is rallying into a potential area of resistance at US$2.40 with no strong support until US$1.20 - US$1.30 and multiple unfilled gaps below. So, while this rally could continue, I believe it's prudent to take some profits, and I certainly don't see any way to justify paying up for the stock here above US$2.25.

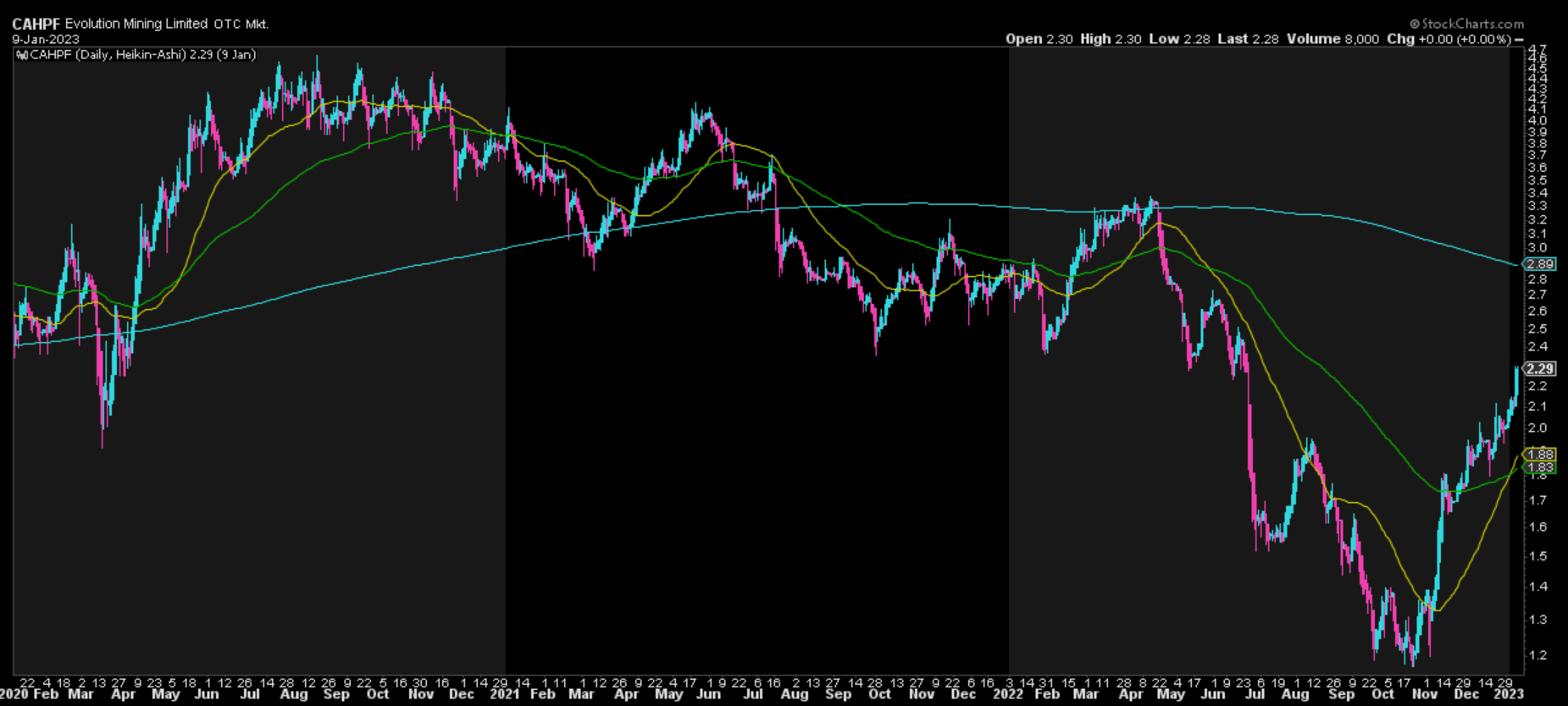

CAHPF 3-Year Chart (StockCharts.com)

{kind=link}

Summary

Evolution has gone from worst performer to best performer with a violent rally off its September lows, and it was one of the few gold miners to break its March 2020 lows, likely due to worries about taking on two major expansions simultaneously in a period of declining gold/copper prices. However, these concerns should be mostly alleviated with the rebound in commodity prices. Plus, Evolution has over $600 million in liquidity to support its growth projects, giving it flexibility even if the investor worries come to roost and the gold price heads back below $1,700/oz.

That said, while Evolution's investment thesis looks better than when gold was hovering near $1,650/oz, much of this positive change in sentiment looks priced into the stock here. This doesn't mean that Evolution can't head higher and make a run for its multi-year moving average near US$2.70 at some point this year, but I don't think it pays to be greedy in cyclical stocks. I also don't think there's much value in holding cyclical stocks when they are trading near full value and relying on the notoriously capricious gold price to drive price targets higher. To summarize, I see this rally in Evolution as an opportunity to book some profits.

For further details see:

Evolution Mining: Limited Margin Of Safety At Current Levels