CAHPF - Evolution Mining: Solid Cost Control In A Challenging Quarter

2023-05-11 22:07:48 ET

Summary

- Evolution Mining released its calendar year Q1 (fiscal Q3) results last month, reporting quarterly production of ~163,900 ounces of gold at all-in sustaining costs of A$1,291/oz [US$878/oz].

- This represented a significant increase in costs from the year-ago period, with lower costs at Cowal and Ernest Henry offset by elevated unit costs at Red Lake and Mt. Rawdon.

- This was related to a difficult quarter for its Queensland mines because of severe weather, but higher metals prices offset increased costs, resulting in positive net mine free cash flow.

- Still, while Evolution has delivered Cowal Underground ahead of time and within budget and continues to make progress at Red Lake, it's hard to justify paying up for the stock above US$2.65.

We're more than halfway through the Q1 Earnings Season for the Gold Miners Index ( GDX ) and the Australian producers were the first to report as usual, releasing their calendar year Q1 (fiscal Q3) results last month. One of the first companies to report that had an unusually challenging quarter was Evolution Mining ( OTCPK:CAHPF ), which was hit by heavy rainfall and flooding in Queensland that affected its highest-margin operation, Ernest Henry. The result was a cut to guidance and a material increase in costs, with all-in sustaining costs [AISC] jumping 17% sequentially despite higher copper prices. Let's take a closer look at the quarter below and the impact this had on FY2023 guidance.

{kind=link}

All figures are in United States Dollars unless otherwise stated at a 0.68 AUD/USD exchange rate.

Q1 Production & Sales

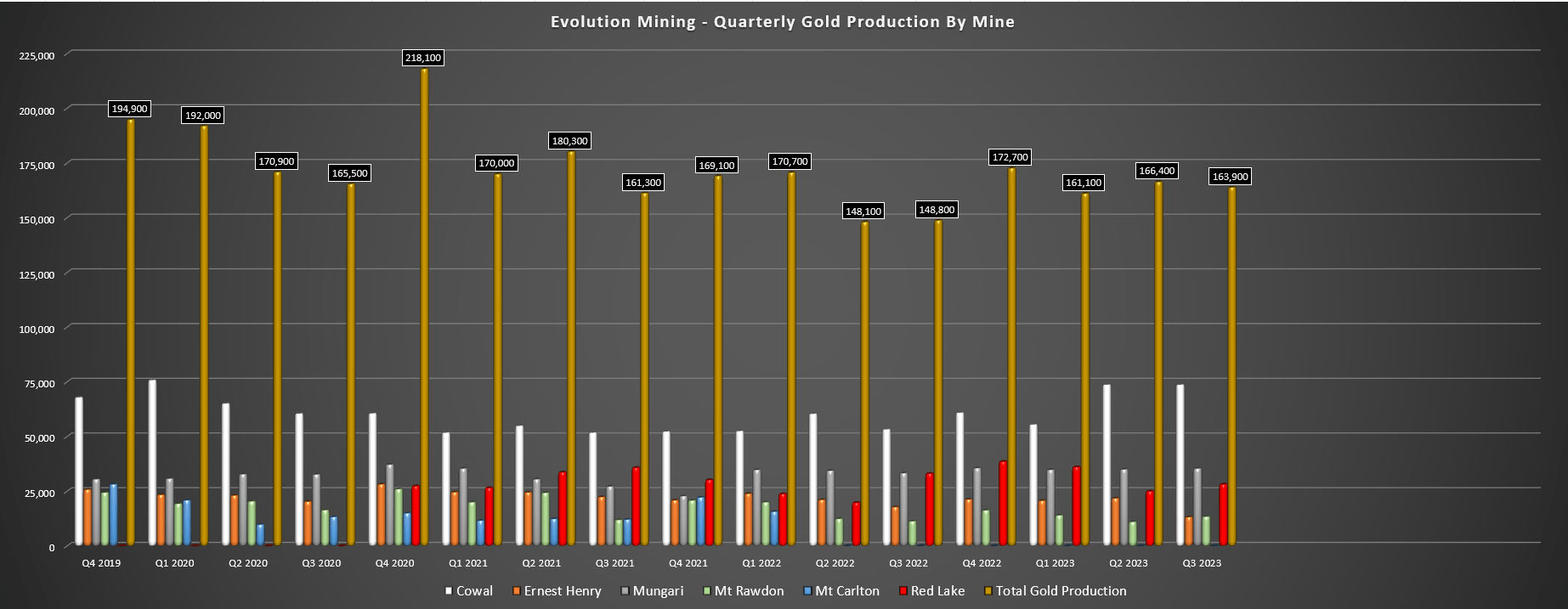

Evolution Mining released its fiscal Q3 results last month, reporting quarterly production of ~163,900 ounces of gold and 9,700 tonnes of copper, an increase from the ~148,800 ounces of gold in the year-ago period offset by a decline in copper production. The increased gold production was related to a monster quarter at Cowal as the first underground stopes were mined earlier than planned, offset by flooding at Ernest Henry because of a severe weather event that resulted in water entering the mine workings and forced the curtailment of mining activities. The impact was 6,400 gold ounces of gold and 4,100 tonnes of copper, with a total impact of ~17,000 ounces of gold and ~10,000 tonnes of copper given that operations didn't restart until late April.

Evolution Mining - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

Looking at the company's other operations, Mt. Rawdon was up against headwinds as well in the quarter, with it being another Queensland operation that was affected by rain events (265 millimeters of rain in the quarter). However, the asset saw increased production on a year-over-year basis (~13,400 ounces vs. ~11,300 ounces), benefiting from higher grades (0.59 grams per tonne of gold vs. 0.52 grams per tonne of gold). That said, the asset was up against easy year-over-year comps because of delayed access to high-grade ore and a 9-day shut for the crusher, affecting processing rates while the crusher was offline. And while Mt. Rawdon's unit costs were elevated at A$2,338/oz, they declined marginally year-over-year.

{kind=link}

Moving over to Red Lake, which continues to be in the turnaround phase, we saw a dip in production on a year-over-year basis, with fiscal Q3 production down ~15% year-over-year to ~28,200 ounces. This was related to fewer tonnes processed at slightly lower grades, with ~206,000 tonnes processed in fiscal Q3, with an average head grade of grade of 4.72 grams per tonne of gold. That said, mined grades improved to 4.74 grams per tonne of gold and while costs increased to A$2,538/oz (fiscal Q3 2022: A$2,394/oz), the company is confident that the asset will see a solid fiscal Q4 with "at least 35,000 ounces", which would place the asset at a ~125,000 ounce run rate for FY2023.

{kind=link}

Overall, this production rate continues to be below investor expectations when the asset was acquired from Newmont ( NEM ) following the Goldcorp acquisition, but Evolution is targeting 160 to 180,000 ounces in FY2024 and significantly higher production long-term if its optimization initiatives are achieved. And while it isn't easy to be optimistic about an asset that continues to operate with razor-thin margins, things are moving in the right direction even if slowly, with improved development rates were consistent year-over-year at ~3,900 meters, two new jumbos have arrived on site for improved production drilling, resulting in improved productivity as the team works towards a goal of ~4,500 meters of development per quarter.

So, while the increase in costs year-over-year despite lower sustaining capital at the asset is disappointing and the costs continue to be well above the industry average at ~$1,725/oz, I remain optimistic about the asset's future. And while some investors might prefer they throw in the towel on this asset given the multi-year turnaround that still hasn't delivered as planned, this is certainly an asset where the prize is meaningful if it can start contributing from a cash flow standpoint given that it has a long mine life ahead of it, with ~12.3 million ounces at ~6.4 grams per tonne of gold across all resource categories.

As for Cowal, the mine had a phenomenal quarter with ~73,700 ounces produced at A$1,072/oz [US$729/oz], with ~43,000 tonnes from its first underground stopes at an average grade of 3.4 grams per tonne of gold, and Cowal Underground delivered on budget and within schedule. During the quarter, the team mined ~152,000 tonnes from underground at an average grade of 2.49 grams per tonne of gold, up significantly from ~2,000 tonnes at 1.80 grams per tonne of gold in fiscal Q3 2022. And while FY2023 is shaping up to be an exceptional year for the asset, FY2024 should be even better with a full year of stope production, with the mine expected to contribute ~320,000 ounces or ~40% of company-wide production at industry-leading costs.

{kind=link}

Finally, while Ernest Henry had a rough quarter due to the weather-related headwinds, the asset still managed to produce at industry-leading costs of [-] A$3,781/oz, and year-to-date costs are sitting at [-] A$3,022/oz. This was helped by a rise in the average realized copper price to A$15,113/tonne, partially offset the lower copper sales in the period. The good news is that mining activities have restarted, and the mine continues to enjoy exploration success that points to meaningful increases in the mine life, which should cement Evolution's position as one of the lowest-cost producers sector-wide well into the 2030s.

Costs & Margins

Moving over to costs and margins, Evolution's AISC increased to A$1,291/oz [US$877/oz] in the period, up from A$1,099/oz in fiscal Q2 2023. This was a significant increase but it's important to note that this cost profile is still ~33% below the industry average of US$1,300/oz. Plus, this was largely due to headwinds outside of the company's control with the extreme weather event in Queensland and 2024/2025 should be better years for the company from a cost standpoint. This is because the low-cost Cowal asset continues to fire on cylinders, Red Lake should see lower unit costs as it benefits from higher sales volumes and improved productivity, and Ernest Henry should continue to operate near A$3,000/oz AISC if the copper price cooperates.

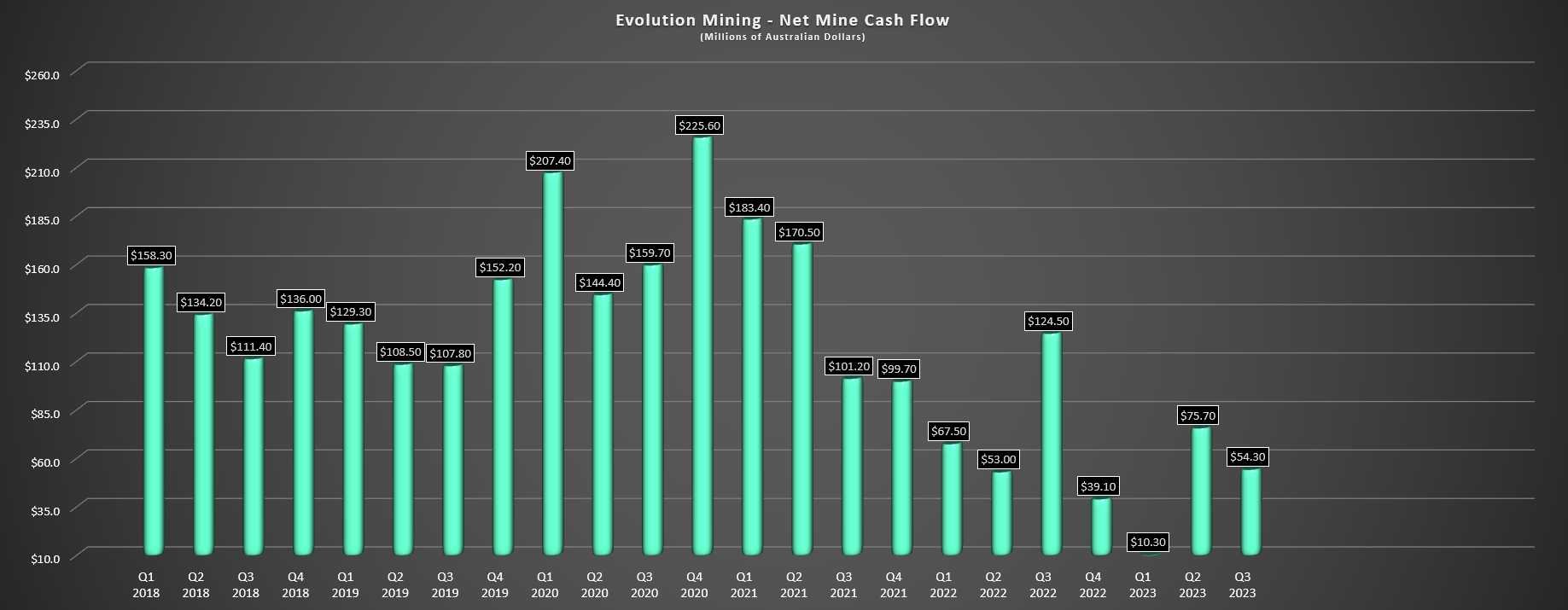

Evolution - Net Mine Cash Flow (Company Filings, Author's Chart)

{kind=link}

As for Evolution's financial results, the company managed to report positive net mine free cash flow despite the difficult quarter at Ernest Henry, with fiscal Q3 operating cash flow of A$269.7 million, fiscal Q3 net mine cash flow of A$54.3 million, and positive group cash flow of A$95.7 million. The return to positive group cash flow was helped by a higher gold price, a tax refund and favorable working capital movements, offset by increased capital expenditures in the period and higher interest expense. The result was that Evolution finished the quarter with A$164 million in cash and A$689 million in liquidity after the final payment to Glencore (GLCNF) related to Ernest Henry and $45 million in debt repayment.

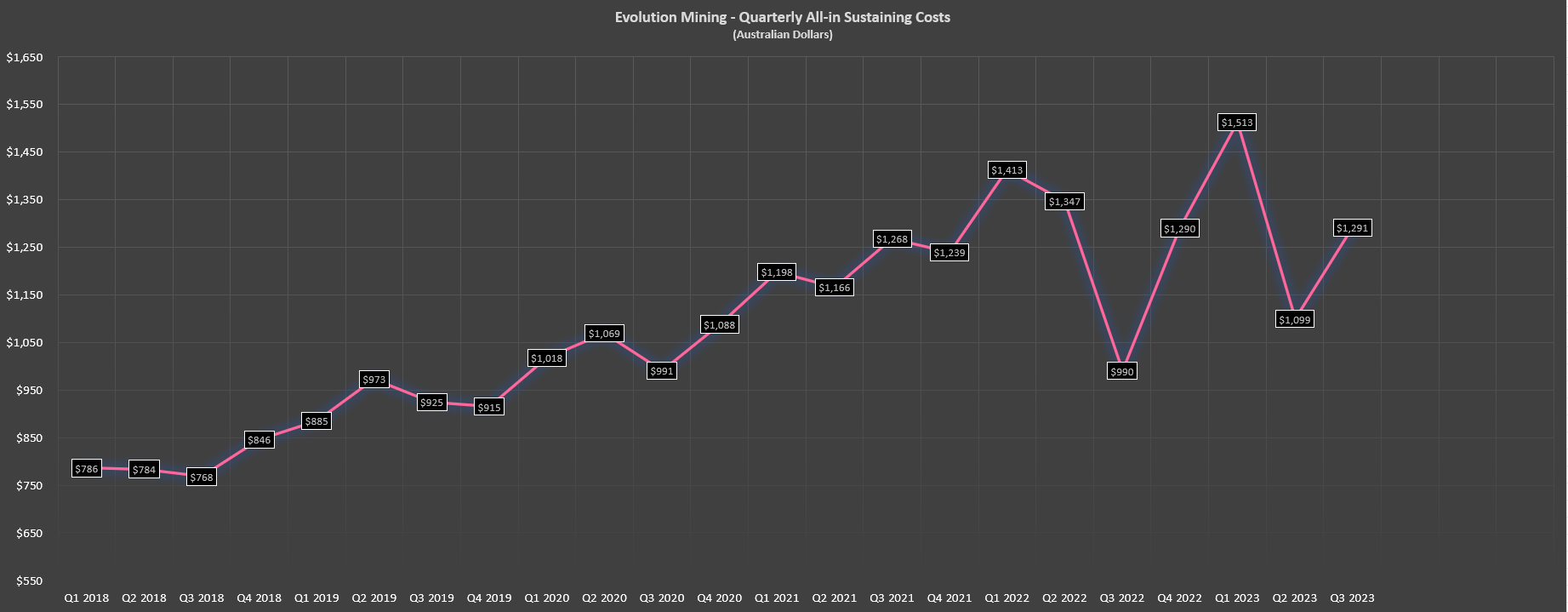

Unfortunately, despite the solid cost control in fiscal Q3 despite its highest-margin operation not contributing as planned, Evolution was forced to reel in its production guidance due to the temporary suspension of mining activities, with guidance now sitting at ~660,000 ounces at an all-in sustaining cost of A$1,390/oz. This is well above the previous outlook of ~660,000 ounces of ~720,000 ounces at A$1,240/oz, and the trend in costs has certainly been choppy with an upward bias. That said, if Evolution manages to have a better year at Red Lake in FY2024, we should see costs drop back below A$1,250/oz, placing them ~35% below the industry average. Let's take a look at Evolution's valuation and technical picture:

Evolution Mining - Quarterly AISC (Company Filings, Author's Chart)

{kind=link}

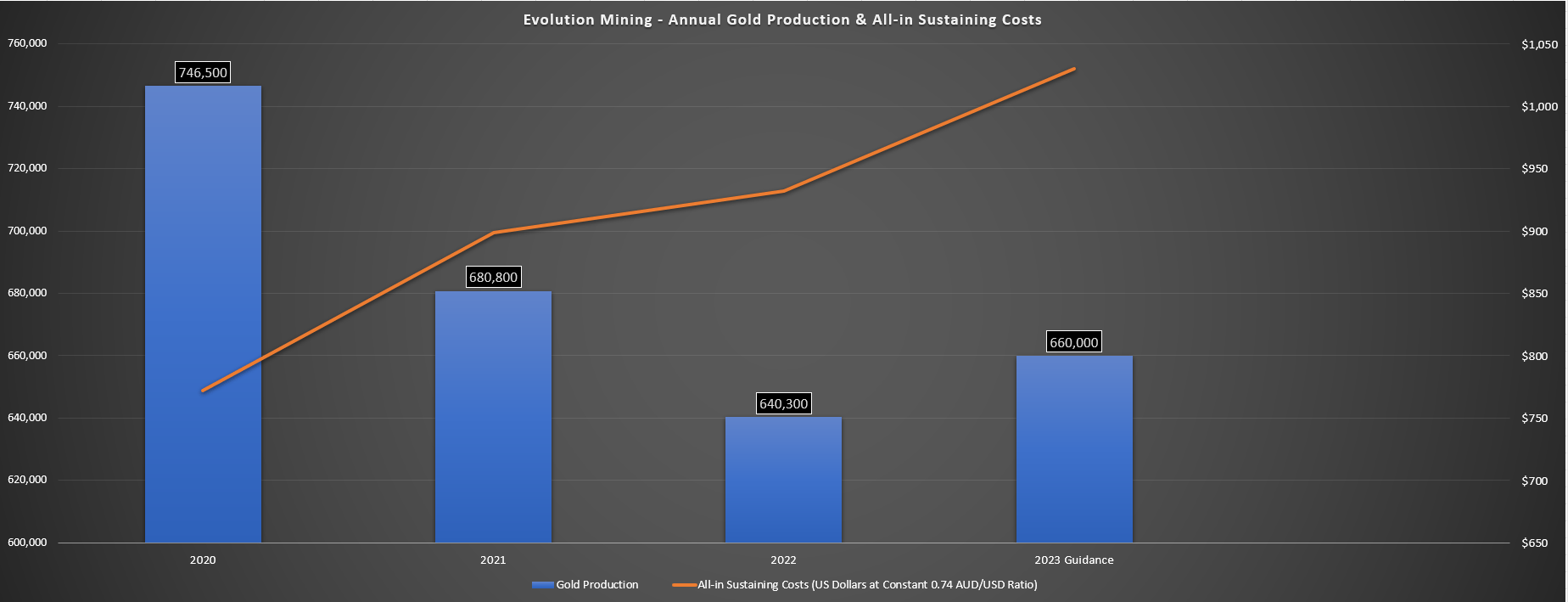

Evolution Mining - Annual Production & Costs & Updated FY2023 Guidance (Company Filings, Author's Chart)

{kind=link}

Valuation & Technical Picture

Based on ~1,835 million shares and a share price of US$2.64, Evolution Mining trades at a market cap of US$4.84 billion and an enterprise value of ~$5.50 billion. This compares unfavorably to an estimated net asset value of ~$3.40 billion, leaving Evolution trading at a meaningful premium to net asset value. And while this is partially justified because of its solid track record of reserve replacement (plus continued exploration success at Ernest Henry) and Tier-1 jurisdictional profile, I continue to see the stock as close to fully valued here. This is because even at a 1.25x P/NAV multiple which is above that of its peers, Evolutions' fair value would come in at US$4.70 billion or US$2.40 per share.

{kind=link}

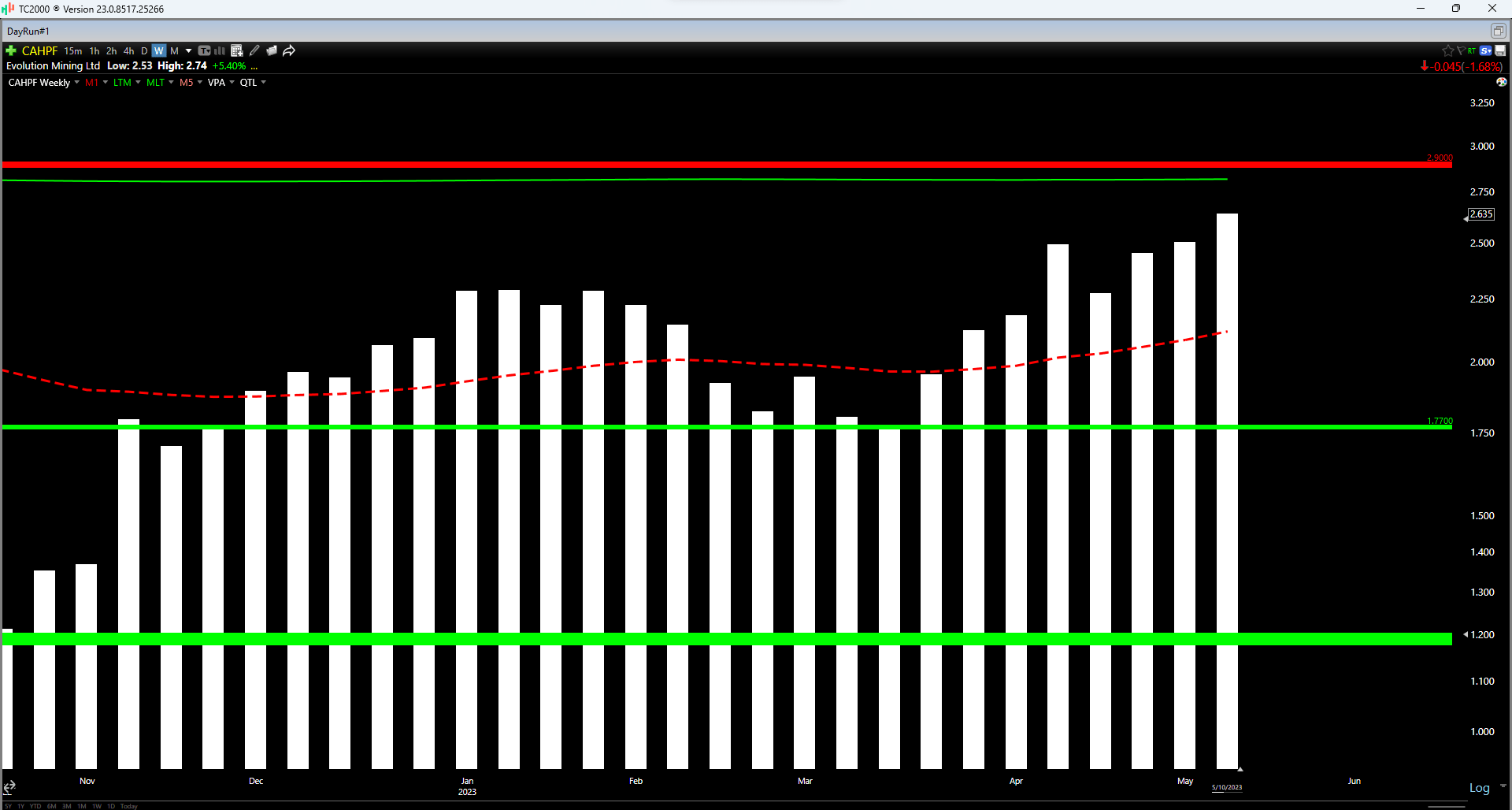

Moving to the technical picture, this corroborates the view that Evolution Mining is nowhere near a low-risk buy zone, with the stock trading in the upper portion of its support/resistance range (US$1.77 - US$2.90). This doesn't mean that the stock can't go higher, and if the gold price remains above $2,000/oz, Evolution may continue to march higher towards resistance. However, I prefer to only start new positions if a stock is trading at a steep discount to fair value and sentiment is in the gutter, and with Evolution sitting 120% above its November 2022 lows and looking fully valued short-term, I don't see any reason to chase the stock above US$2.60.

Summary

Evolution Mining put together a solid fiscal Q3 performance given the heavy rainfall that led to a temporary stoppage of mining activities at Ernest Henry, plus another quarter of inclement weather at Mt. Rawdon, which saw significant rainfall once again in fiscal Q3 2023, similar to Q3 2022. Plus, while Ernest Henry may have seen lower production, a higher realized copper price fortunately offset this, while the higher gold price and lower costs at Cowal benefited margins as well. This led to a better fiscal Q3 report than I had expected and investors can also look forward to an un-hedged Evolution Mining starting in FY2024 (fall of calendar year 2023).

That said, Evolution has now risen over 125% from its Q3 2022 lows, continues to trade at a steep premium to net asset value, and is vulnerable to a sharp correction if we see a retracement in gold and or copper prices. So, while I think Evolution is a top-5 producer among the Australian miners, I don't see any way to justify chasing the stock at current levels. In fact, I see this rally above US$2.65 as an opportunity to book some profits with sentiment in the sector a little overheated short-term.

For further details see:

Evolution Mining: Solid Cost Control In A Challenging Quarter