NOG - Evolution Petroleum: Interesting Business Model Attractive Yield Reasonable Valuation

Summary

- Evolution Petroleum is an E&P that buys producing properties from other companies rather than developing them itself.

- This is a very profitable business model because it allows the company to avoid the high costs of development.

- The company is currently generating the highest adjusted EBITDA that it ever has in history.

- The dividend varies depending on energy prices and is backed by a rock-solid balance sheet.

- Evolution Petroleum has a reasonably attractive valuation that may make it worth considering.

Evolution Petroleum Corporation ( EPM ) is an independent exploration and production company that has a rather interesting business model. In short, the company invests in, develops, and produces crude oil and natural gas within known reservoirs utilizing conventional technology. This makes it very different from the shale producers that we usually think of when we picture independent energy companies in the United States. However, the company still produces crude oil and natural gas and so has benefited significantly from the steep appreciation that we have seen in energy prices over the past eighteen months. Indeed, Evolution Petroleum's stock is up an impressive 83.69% over the past twelve months, which makes it one of the few bright spots in today's volatile market. Despite this steep appreciation though, the company still appears to be very reasonably priced, which may make it a worthy investment today. When we combine this with some significant growth prospects, there is certainly a great deal to like here and an excellent case can be made for purchasing it.

About Evolution Petroleum

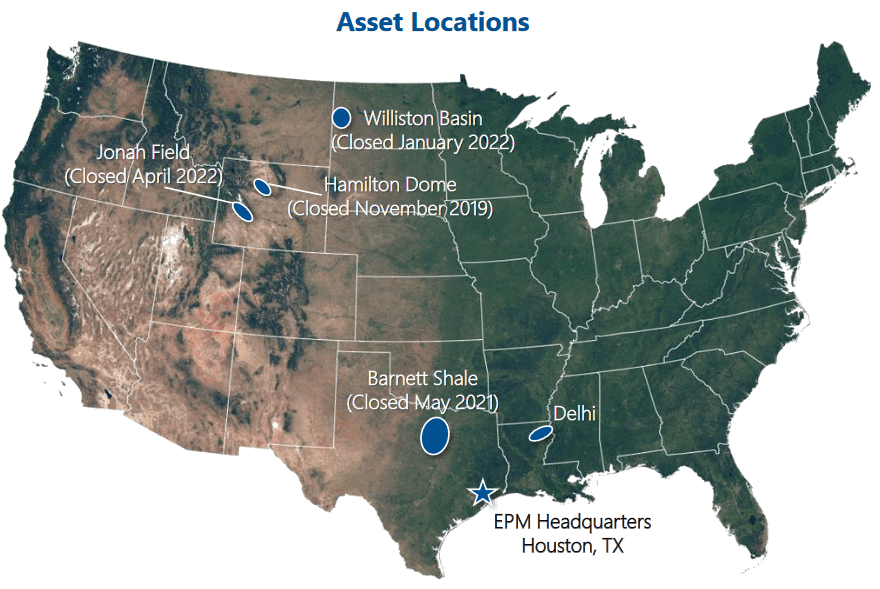

As stated in the introduction, Evolution Petroleum is an independent exploration and production company that has something of a unique business model. Unlike many of its American peers, Evolution Petroleum produces its oil and natural gas using conventional techniques as opposed to the shale drilling companies that dominate the industry. In some ways, this strategy reminds me of Linn Energy and Breitburn Energy Partners, which both collapsed back in 2015. Fortunately, Evolution Petroleum has a much more robust business model as we will see throughout this article. Evolution Petroleum currently operates in the Williston Basin, various fields in Wyoming, the Barnett Shale in Texas, and Louisiana:

{kind=link}

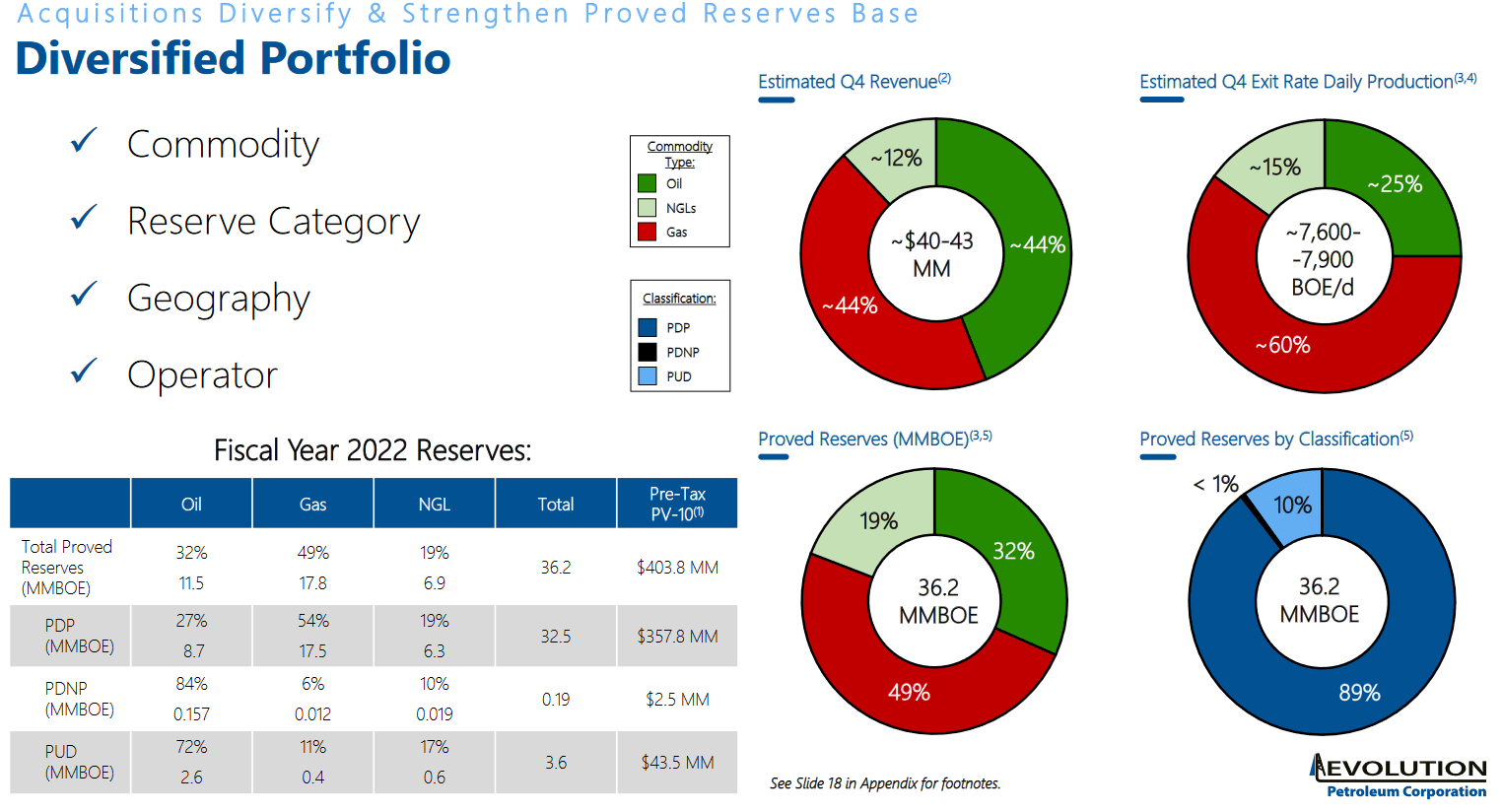

As we can see, Evolution Petroleum's operations are quite well diversified and even include a few areas that followers of the energy industry do not often hear about. This could provide the company with certain advantages, although all of these are generally considered to be crude oil plays. This might make one think that Evolution Petroleum is primarily a crude oil producer, which could actually be a disadvantage in today's market since natural gas has much stronger fundamentals. This would be an incorrect assumption however as Evolution Petroleum's production is in fact quite well-balanced between natural gas and liquids:

{kind=link}

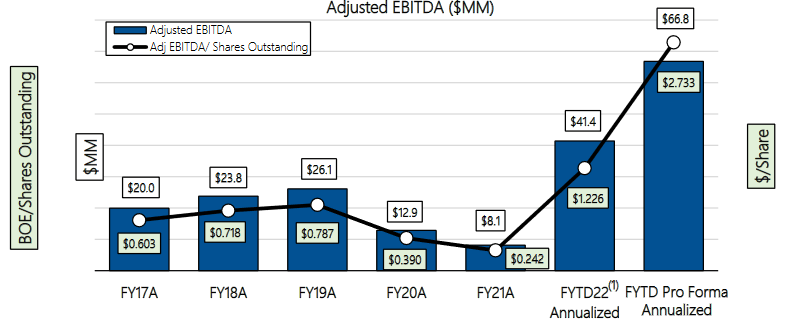

This is nice because it gives Evolution Petroleum exposure to the fundamentals of both hydrocarbon products. A few years ago, this would not have been much of an advantage. As long-time followers of the energy industry may recall, prior to 2018 or so, natural gas was frequently flared off as a waste product, and companies whose production was primarily crude oil were greatly preferred by investors. This was partly because natural gas prices were so low that it was unprofitable to produce it and bring it to the market. That is no longer the case. In fact, despite all the grumbling about rising oil prices, natural gas prices have climbed much more. Over the past twelve months, West Texas Intermediate crude oil has increased by 45.41% but natural gas at Henry Hub has increased by a much more substantial 151.43%. As might be expected, this increase in energy prices has had a very beneficial effect on Evolution Petroleum's cash flows. In the first three quarters of 2022 (the company uses a fiscal year that starts on July 1), Evolution Petroleum has generated an annualized adjusted EBITDA of $41.4 million, which would represent the highest adjusted EBITDA that the company has ever generated:

{kind=link}

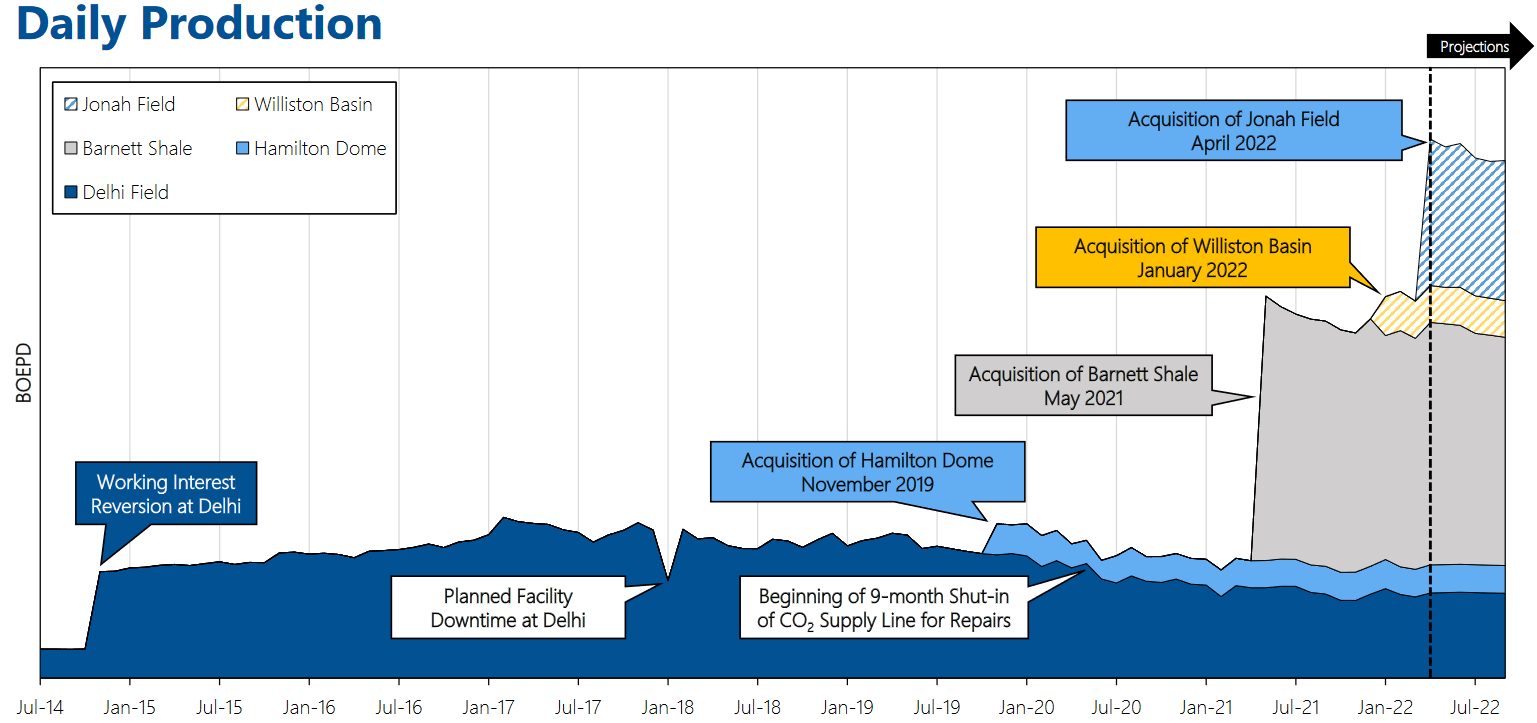

An increase in energy prices is not the only way that Evolution Petroleum manages to achieve growth. Evolution Petroleum also has a long history of acquiring producing acreage from other companies. It should be fairly obvious how this would result in growth. After all, the resources that are being produced by the purchased property directly continue to the company's output, providing it with more products to sell and generate revenue. As we can see here, the company's production increased substantially in 2021 when it purchased its current property in the Barnett Shale and again back in April of this year when it purchased acreage in Wyoming's Jonah Field:

{kind=link}

Thus, we have a situation in which Evolution Petroleum is both benefiting from climbing energy prices and aggressive production growth through acquisitions. The company seems likely to continue to grow its portfolio at a rapid pace going forward, although it has not made public any plans that it has. It is nice to see that the company is probably going to keep expanding its operations in this way because this is one of the only ways that Evolution Petroleum can generate growth that is actually within its control. After all, the company cannot control the global price of crude oil or natural gas. It is, of course, crucial that Evolution Petroleum makes any acquisition at a price that allows it to earn a respectable return but historically it has been fairly good at this.

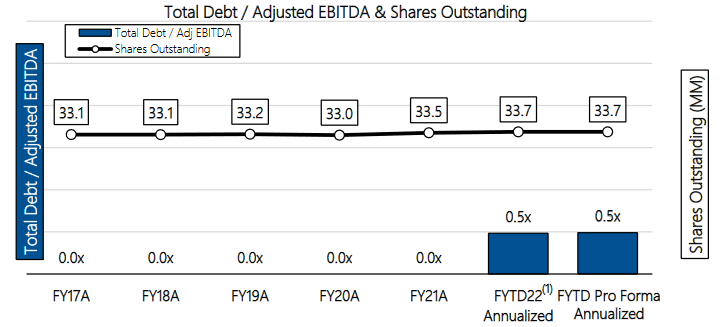

We might expect that a company with a history of growth through acquisitions would have a fairly high debt load. That is not the case here, however. In fact, Evolution Petroleum has a remarkably strong balance sheet. We can see this by looking at the company's leverage ratio, which is also known as the total debt-to-adjusted EBITDA ratio. This ratio essentially tells us how long it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that purpose. As we can see here, the company had essentially no debt throughout its history, although it did take on some this year:

{kind=link}

While the company has taken on some debt this year, it is not enough to be a concern. This is because a leverage ratio of 0.5x is still one of the lowest ratios in the industry. As I have pointed out in a number of previous articles, such as this one , the best-financed companies in the industry tend to have leverage ratios around 1.0x. Thus, Evolution Petroleum has one of the most attractive financial structures in the industry. This could prove to be an advantage for the company as the United States heads into a recession. A recession may mean that energy prices could decline, although the long-term fundamentals point to higher prices than today. The lower the company's leverage ratio, the easier it will be for it to carry its debt should a decline in energy prices cause the company's cash flows to decline. Thus, Evolution Petroleum should have somewhat lower risks than many of its more indebted peers. Any investor should be able to appreciate this.

Fundamentals Of Crude Oil And Natural Gas

As Evolution Petroleum produces a relatively balanced mix of crude oil and natural gas, it would be a good idea to take a look at the fundamentals of these compounds as a part of our analysis. Fortunately, the fundamentals of both products are very strong and point to both rising demand and high prices going forward, although it is possible that we will see a temporary price decline due to the recession in the United States. The fact that these resources have incredibly strong fundamentals is something that may be surprising considering all that we are told about the "greening" of the economy. However, according to the International Energy Agency, the global demand for crude oil will increase by 7% while the global demand for natural gas will increase by 29% over the next twenty years:

Pembina Pipeline/Data from IEA 2021 World Energy Outlook

The demand growth for natural gas will be driven by the concerns about climate change around the world. As everyone reading this is certainly well aware, these concerns have caused many governments to impose a variety of incentives and mandates that are intended to reduce the carbon emissions of their respective nations. One of the most popular strategies is to encourage utilities to retire old coal-fired power plants and replace them with renewables. However, renewables are not reliable enough to support the needs of modern society on their own. After all, wind turbines do not generate power when the air is still and solar power does not work when the sun is not shining. The usual solution is to supplement renewables with natural gas turbines. This is because natural gas is reliable enough to ensure that the grid is able to handle the needs of modern society when renewables are unable to and it burns cleaner than other fossil fuels. This is why natural gas is often called a "transitional fuel" since it provides a way to reduce carbon emissions and ensure that modern society is able to keep functioning until renewables are able to accomplish this on their own.

The case for crude oil demand growth may be somewhat harder to understand since many politicians in the Western nations have been working to reduce the consumption of crude oil within their borders. However, things are very different if we look at the various emerging nations around the world. These nations are expected to benefit from tremendous economic growth over the projection period, which will have the effect of lifting the citizens of these nations out of poverty and putting them firmly into the middle class. These newly middle-class people will naturally begin to desire a lifestyle that is much closer to what their counterparts in the Western nations enjoy than what they have now. This will require increased consumption of energy, including energy derived from crude oil. As the populations of these nations substantially outnumber the populations of the world's developed nations, the growing demand for crude oil from these countries will more than offset the stagnant-to-declining demand in the various developed countries around the world.

It is unlikely that the global production of crude oil or natural gas will grow sufficiently to satisfy this demand. This is because the energy industry has been chronically underinvesting in capacity since the oil bear market back in 2015. In fact, it is so bad that Moody's recently stated that the oil and gas industry must immediately increase upstream spending by 54%, or $542 billion, in order to avoid a supply shortage. In addition, the industry would need to expand its spending on midstream infrastructure in order to ensure the needed capacity to get these incremental resources to the market. It is highly unlikely that the industry will actually do this, however. First of all, energy companies are under tremendous pressure from activists and politicians to improve the sustainability of their operations. Secondly, the energy industry has generally underperformed other sectors in the market over the past decade and investors have begun to demand higher returns. Thus, we have a situation in which the demand for crude oil and natural gas will increase much more rapidly than the supply. According to the laws of economics, this should result in rising prices.

Dividend Analysis

One of the advantages of Evolution Petroleum's business model is that it is highly profitable. This is because Evolution Petroleum does not have to handle the enormous capital expenditures required to actually develop the properties:

{kind=link}

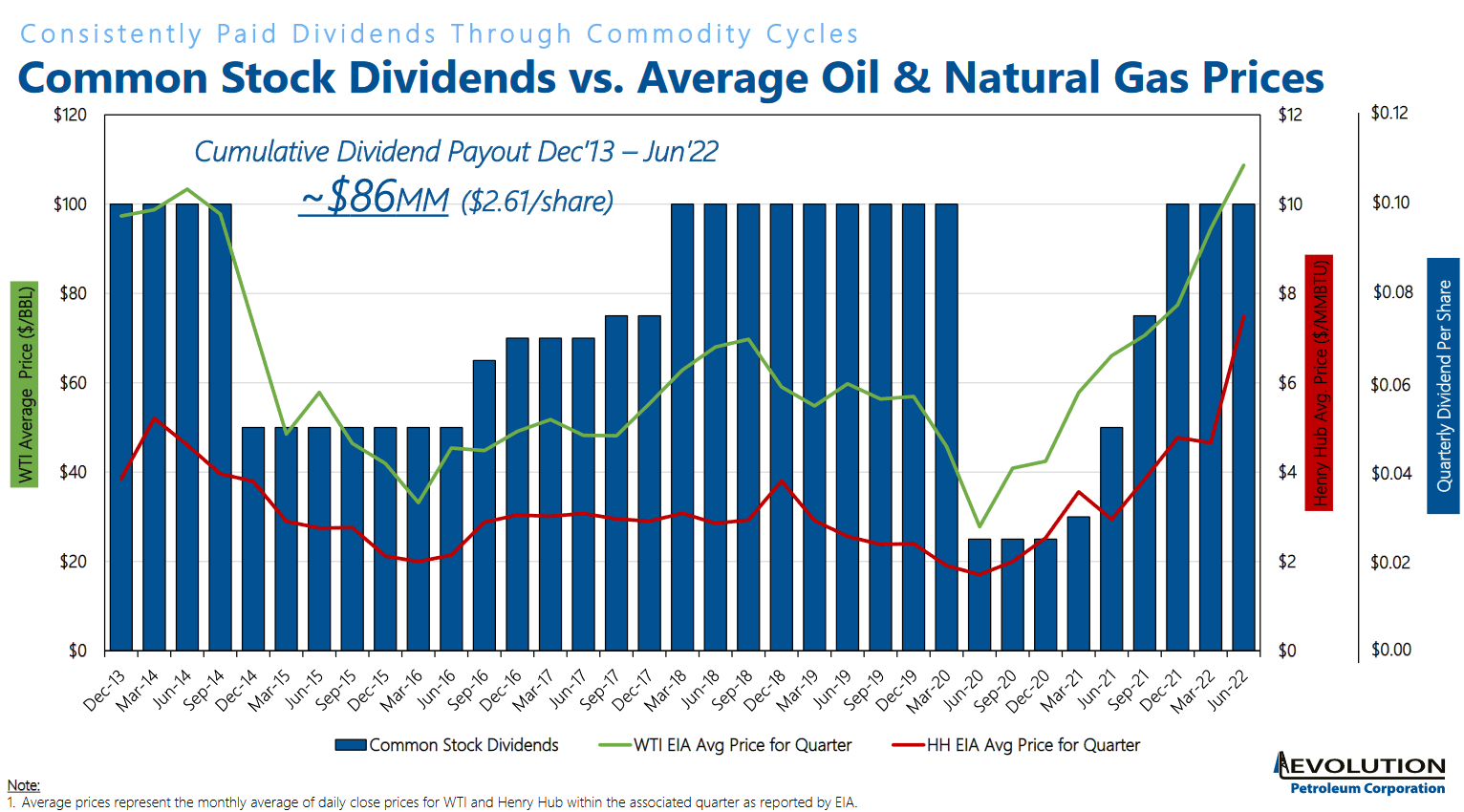

As a result, we might expect Evolution Petroleum to be able to reward its shareholders with a dividend. This is indeed the case as the company currently boasts a reasonably attractive 4.87% yield at the current price. In order to avoid some of the mistakes that were made by companies that have used similar business models in the past (such as the aforementioned Linn Energy and Breitburn Energy Partners), Evolution Petroleum has a variable dividend. In short, the company adjusts its dividend based on energy prices in order to avoid paying out money that it cannot actually afford:

{kind=link}

Admittedly, this model may not be particularly appealing to those investors that are looking for a steady and secure source of income with which to pay their bills. However, many of us are also consumers of both oil and natural gas so our own costs go up whenever energy prices do. The company's variable dividend can certainly help in that situation since the fact that we will receive more money when our expenses go up can help take some of the stings out of those expenses. As is always the case though, it is critical that we have a look at the company's ability to actually pay its dividend. After all, we do not want to get stuck being invested in a company that pays out too much money and finds itself in financial trouble.

The usual way that we examine a company's ability to pay its dividend is by looking at a metric known as free cash flow. A company's free cash flow is the amount of money that is generated by a company's ordinary operations and is left over after it pays all its bills and makes all needed capital expenditures. This is therefore the money that is available to be used for things such as reducing debt, buying back stock, or paying the dividend.

During the company's third quarter of 2022, which ends on March 31, 2022 (the most recent quarter with information available as of the time of publication), Evolution Petroleum reported a negative leveraged free cash flow of $12.9 million. This was obviously nowhere near enough to pay any dividend, let alone the $3.4 million that the company paid out in dividends during the same quarter. This may explain some of the increase in debt, but it is also important to remember that the company made two major purchases this year. Evolution Petroleum did have $14.8 million in operating cash flow during the most recent quarter, which was certainly enough to cover the dividends that were paid out and still leave a large amount of money left over for other purposes. When we consider Evolution Petroleum's strong balance sheet, it can probably maintain the dividend since it will cut it anyway if energy prices fall but I will admit that I dislike seeing a company taking on debt just to pay its dividend. With that said though, any investor should go into this company knowing that the dividend will be fluctuating based on energy prices.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of an independent exploration and production company like Evolution Petroleum, one way to value it is by looking at the company's forward price-to-earnings ratio. This ratio tells us how much an investor would have to pay today for each dollar of earnings that the company will generate over the next year.

According to Zacks Investment Research , Evolution Petroleum has a forward price-to-earnings ratio of 5.06 at the current stock price. This is a remarkably low ratio, especially in today's market as most companies have ratios well into the double-digits. However, as I have pointed out in numerous past articles, pretty much everything in the traditional energy sector is remarkably cheap right now. Thus, it may make some sense for us to compare Evolution Petroleum against some other companies in the sector to see which ones offer the most attractive relative valuations:

| Company |

| Forward P/E |

| Evolution Petroleum |

| 5.06 |

| Northern Oil and Gas ( NOG ) |

| 4.46 |

| Diamondback Energy ( FANG ) |

| 5.04 |

| Devon Energy ( DVN ) |

| 7.51 |

| Continental Resources ( CLR ) |

| 5.76 |

| Matador Resources ( MTDR ) |

| 5.43 |

(all figures sourced from Zacks Investment Research)

We can see here that Evolution Petroleum, admittedly, does not have the absolute most attractive valuation in the sector. However, it does appear to be at least in line with many of its peers so the company appears to have a very reasonable valuation today. Overall, its valuation is attractive enough to make it worth considering.

Conclusion

In conclusion, Evolution Petroleum has a lot to offer an investor today. The company has a somewhat unique business model but also a very attractive one as it provides the company with a significant amount of profitability. It also appears quite likely that Evolution Petroleum will have some growth opportunities ahead of it due to its incredibly strong balance sheet that provides flexibility for acquisitions. Admittedly, the variable dividend may be somewhat offputting for some investors but I see this company as something of a hedge against the higher energy bills that I have to deal with as a consumer. When we combine this with the very reasonable valuation, there appears to be a lot to like here.

For further details see:

Evolution Petroleum: Interesting Business Model, Attractive Yield, Reasonable Valuation