EVKIF - Evonik: Building A Position For A Blockbuster 2023-2025 - Buy

2023-07-27 08:19:55 ET

Summary

- Despite a downturn in the specialty chemicals sector, I remain positive about investment in Evonik Industries stock due to strong dividends, a BBB+ credit rating, and strong underlying fundamentals.

- The company's 2Q23 results were weaker than expected, with a slower recovery leading to weak demand for products. However, the overall trend is positive, with sequentially better earnings each month.

- Despite the downturn, I believe Evonik is undervalued and has potential for significant improvements in the long term. The company remains a "Buy."

Dear readers/followers,

Despite a so-far lackluster result from my Evonik ( EVKIF ) Position, I'm in no way discouraged with my investment here. There's no doubt, I've said previously, that we're currently in a bit of a downturn for the sector with plenty of headwinds in the space of specialty chemicals. This is where Evonik operates.

It's equally clear to me that the eventual reversal will send the stock up north again, to trade at levels we've seen during upcycles. Due to the combination of strong dividend tradition and a 6.3%+ yield, a BBB+ credit rating, underlying fundamentals with very strong trends in key attractive sectors, and a double-digit non-dividend related upside to as low a forward P/E as single low double digits, I remain at a positive stance for my position in the company and am busy adding here.

When it comes to Evonik, here is how I see what's going on.

Following up on Evonik Industries

Evonik is a very volatile sort of business. As with any commodity-based sort of business, the ups and downs here can be pretty extreme, and you won't find me arguing that we're on our way into a negative cycle here, with current estimated 2023E results potentially as low as €1.2€-1.4/share.

We have preliminary 2Q23 results (Source: Evonik Preliminary results ), published on the 10th of July. Compared to my expectations and targets, results came in about €10M worse than I expected in terms of company EBITDA. The company previously guided for recovery - and this recovery is proving slower than expected.

This slower-than-expected recovery is what's driving trends for the company at this time because the delayed recovery is causing persistently weak demand for company products - again at this time.

The company also has revised its forecast - and it's my analysis that this is what's caused the drop since that time about 15 days ago. Analysts adjusting their models - as I have - to account for a deeper drop in 2023, and a slower uptake in the 2024-2025 periods.

Does this make Evonik "not" a "BUY"?

I say no.

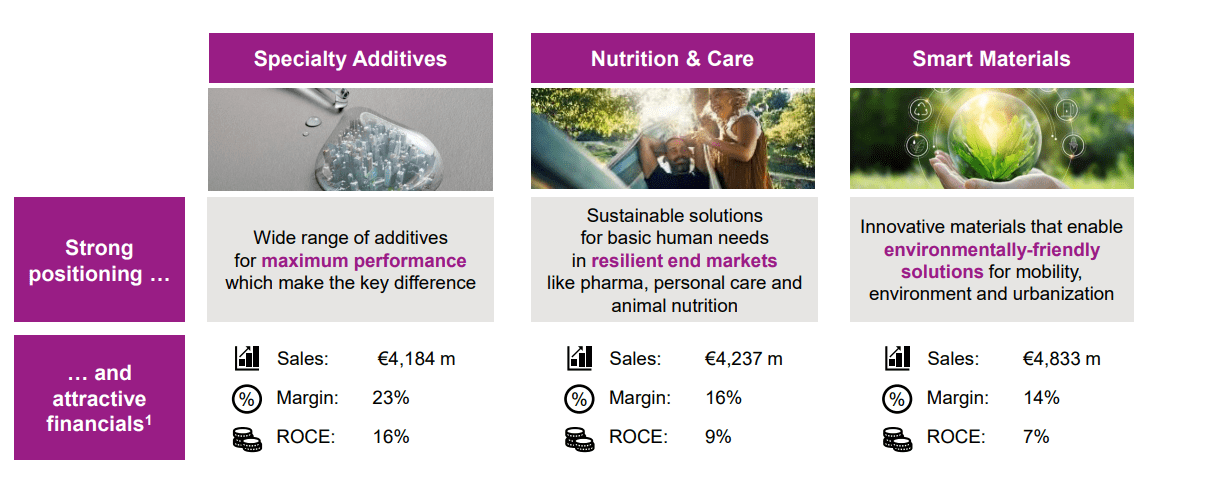

Despite some negative trends in animal nutrition, slow starting in Speciality additives, and overall lower volumes than expected, the overall trend is a positive one. Through every month, the company is seeing sequentially better earnings. It's just that the trends are not as quick as the company expected.

{kind=link}

But it doesn't take away from the basis of my positive thesis - which is that the company is an undervalued play on key segments that are going to be more relevant on a future basis, not less. A slower uptake or slower improvement isn't cause for me to abandon this thesis - only adjust my expectations.

The biggest result Evonik can be said to have during the 2Q23 period is their performance of keeping product pricing at a stable level. Top-line sales reflect the overall weak economic trend, at around €4B for the second quarter.

Evonik already was in damage control mode and is going deeper in 2Q. This includes not filling vacancies, limiting external services, and cutting travel - and these economic effects will ramp up during 2H23. Working capital will be reduced, and CapEx will be limited. Smaller expansions will be postponed in the light of weak demand and moved up to a timeframe when there's better visibility. CapEx expectations are down to about €850M for the year, and that's another €100-€125M cut from the already revised expectation.

This is how commodity businesses work in lean economic periods. I can say with certainty that I would not be happy if I had bought Evonik at a €35+ share price, or even a €30/share price that we saw as late as 2021.

However, the company is trading at ranges from €17-€22/share, and that's where I established the lion's share of my position. That means when the uptick comes - and it will come, no doubt to me there - this has the potential for the triple-digit RoR inclusive of dividends of which I speak.

The current expectation for the company is an EBITDA upwards of €1.8B, which is down €300M from the previous estimate, with annual sales at the run-rate of €4B quarterly, which is down around €1-2B.

However, stringent measures are likely to keep cash conversion rates at the target of 40%, which is up 8% from previous years.

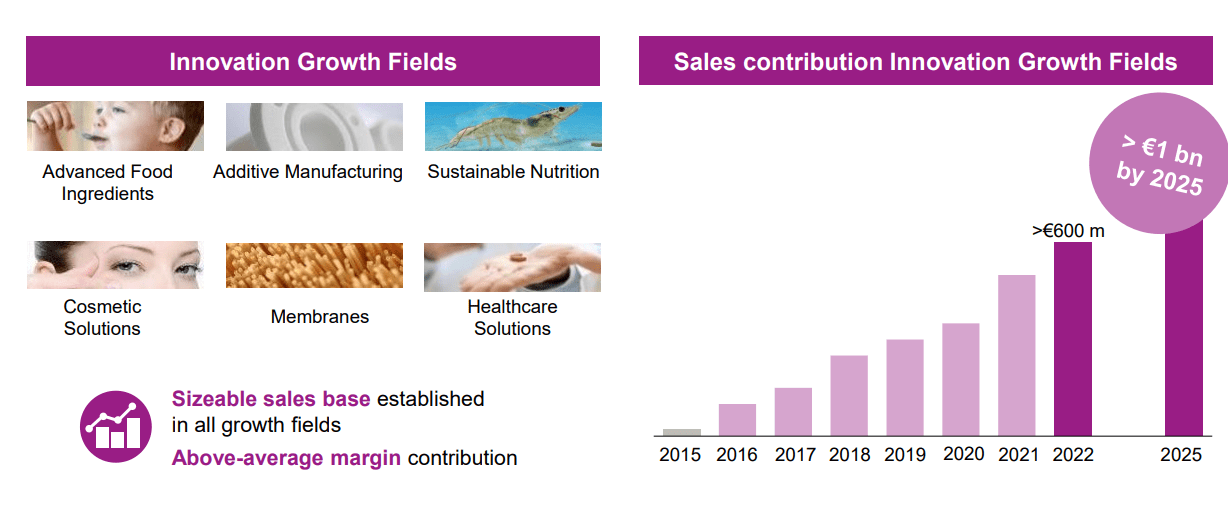

The market is, of course given its tendency towards extreme reactions, treating this as a massive impact. But the market underestimates and fails to mention several things, including the growth trajectory from growth fields...

{kind=link}

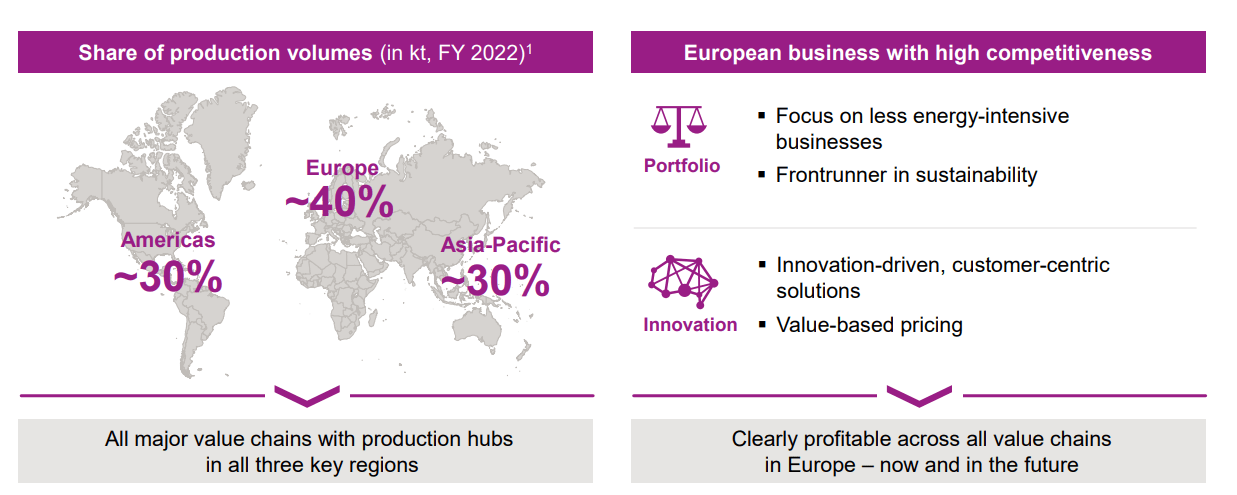

...to its fundamentally extremely balanced footprint, with profitability in every region. It speaks to the company's quality and efficiency that despite trends that the company, in its own words, " We haven't seen such persistently weak sales volumes in a long time, perhaps never before over such a long period, (Source: 2Q23 Evonik Industries) ", there is never the question of not being profitable as a business, as some investments that are being touted are.

{kind=link}

The company's short-term financial targets, including a 4% organic growth rate of above, and an 18-20% EBITDA margin may be impacted for some time, but none of the fundamentals are, as I see it, in danger here.

The company is actively divesting non-core assets - €2B in cyclical sales as of the previous few quarters, which were sold at very good multiples of 8-9x EV/EBITDA and an EBITDA margin of 15% - below the company's target. (Source: May Presentation, Slide 16 )

At the same time, Evonik is acquiring new core assets at more or less the same multiple (premium of 0.1-0.6x) but with both synergistic advantages and 7-9% EBITDA margin improvements compared to the divested assets/operations.

The company's target is reduced cyclicality, with more resilient earnings and FCF profiles and even better cash conversions. This is not a new target - it's what the company has been doing for years.

In a way, I welcome declines here. 2Q23 was not a "good" quarter, and I hope the company in fact drops more so that I can add even more and reduce my cost basis. Remember, my holding target is usually at least 3 years. And in that timeframe, I see the clear potential for significant improvements as both the cycle moves back, as the company adds some of these operations, and delivers on synergies.

The full 2Q23 presentation won't be out until about 2 weeks - but these prelims are definitely clear enough to work on, and have done their share of "preparing" the share price for this.

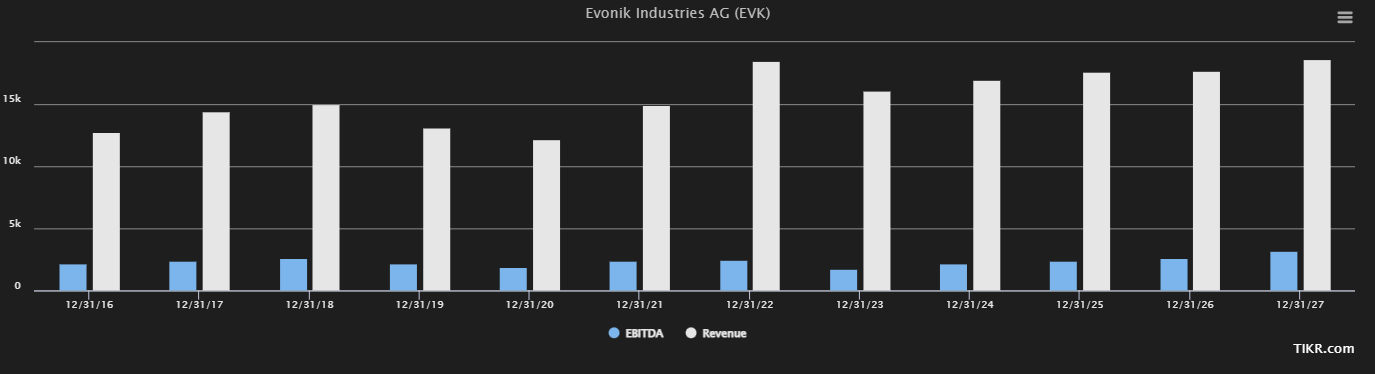

Here are current S&P Global estimates for the company's results and EBITDA for the next few years. And I want to emphasize how "little" I care for such a small drop when the bigger picture looks like this.

Evonik Estimates (S&P Global/Tikr.com)

{kind=link}

It's a drop in the ocean - and if you have a long enough timeframe as your target, and view it far bigger as some seem liable to do, the upside becomes clearer - especially with that 6%+ yield that the company offers.

Going forward, I would pay extra attention to signs of recovery - because this will likely signify a turnaround in the stock.

Let's look at company valuation.

Evonik - The valuation remains compelling despite the downturn

So, first off, most S&P Global analysts have already adjusted their PT to account for the prelim 2Q23 and 2023E weakness. From having a €32/share PT about 1 year ago, the analysts are now down to an average of €20.46, with a low of €15 and a high of €26/share. That's from a high of €44 12 months back, and it really showcases the volatility of how some of these analysts work and how short-term in nature their theses can be.

My own PT is based on a much longer-term upside. Still, I find it fair to adjust my PT somewhat based on this serious guidance change - but not by much - I choose to go about by 7% and reduce it to €26.5 from slightly over €27 in my last article. But that's all I'm going to do in terms of the price target.

The vast majority of analysts are advocating a "HOLD" rating here. I don't view this necessarily as being completely wrong, because in case the company drops in 3Q as well, there is a potential for new lows as the market digests these 2023E numbers. But for me, considering establishing a large stake of 2-4% over a long time for a 100%+ RoR in 3-4 years, I'm more concerned with establishing a solid foundation below that €20/share - and we're there already.

Because I consider the company's premium not unlikely to hold in the long term beyond this cycle, especially with a vastly improved EBITDA margin and stability, I forecast at 15-17x P/E, which is highs the company has reached before - and this gives us that 101-105% potential RoR in 3-years.

Even the base case of 12-13x P/E for the company here gives us 16-17% annualized, or close to 45-47% total RoR in a few years. Even if this was the case, I would still consider this a good investment to come away with.

Remember that company peers, which include some of the largest and most storied cyclical out there, are trading at higher premia with lower yields, and similar or lower fundamentals. Evonik is a stand-out in terms of quality and price. It doesn't have worse fundamentals or a worse credit rating, not materially. It doesn't have worse sales. It's not substantially less efficient - often better in fact, but there's a high "transformation" discount. I obviously do not agree with this substantial transformation discount.

Also, Evonik has very motivated large owners in the form of RAG, which traditionally have been very shareholder-friendly stewards of the company.

Here is my current thesis for the company, and it's a positive one.

Thesis

- I've been adding more of Evonik Industries over the past few months, building my position slowly.

- I view Evonik as a substantially undervalued, quality enabler of renewables and ESG-based technology, which puts it on a trajectory for growth for the next decade and more. The yield is another big advantage here.

- I use both common share investments, and I've also written PUTs, taking advantage of the weakness in the share price.

- My PT for the company is now at a conservative €26.5/share given the lack of visibility for some of the divestment and trends in 2023. I've now impaired it slightly, but it doesn't change my overall thesis and upside.

- The company remains a "BUY" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Evonik fulfills every single one of my investment criteria here.

For further details see:

Evonik: Building A Position For A Blockbuster 2023-2025 - Buy