EVKIY - Evonik: Portfolio Reshaping Continues

2023-05-10 16:53:00 ET

Summary

- Improving trend at the EBITDA level.

- Cost-saving initiatives are underway and Evonik's portfolio improvements continue.

- 2023 guidance was unchanged, and neither was our valuation.

Last year, we analyzed EU chemical companies with the ongoing energy crisis and identified a few players with " margins revaluation from current prices such as Evonik ( EVKIF ; EVKIY ) and BASF ( BFFAF ), and those that are instead overvalued compared to the sector fundamentals, i.e. Arkema ( ARKAY ) ".

Here at the Lab, despite Wall Street's negative sentiment, we were confident in Evonik thanks to an excellent business with a solid track record in the specialty additives/smart materials divisions. Cross-checking analysts' main objection, we provided some relief on Evonik's " ability to achieve turnover growth through the economic cycle" . Since our publication called ' Earnings Defensiveness ' released in September, the company's stock price is up by more than 24%. Our buy case recap was also supported by 1) the company's net debt position evolution with a lower pension contribution), 2) Evonik healthcare division upside, and 3) a good entry point versus its closest peers with a tasty dividend. To support point 3) Evonik's main shareholder is a foundation with an equity stake higher than 50% which relies upon Evonik's capital distribution. These positive performances were also confirmed in the Q4 update. You can check our previous publication titled ' We'll Just Keep On Waiting '.

Mare Evidence Lab's previous analysis

{kind=link}

Q1 results

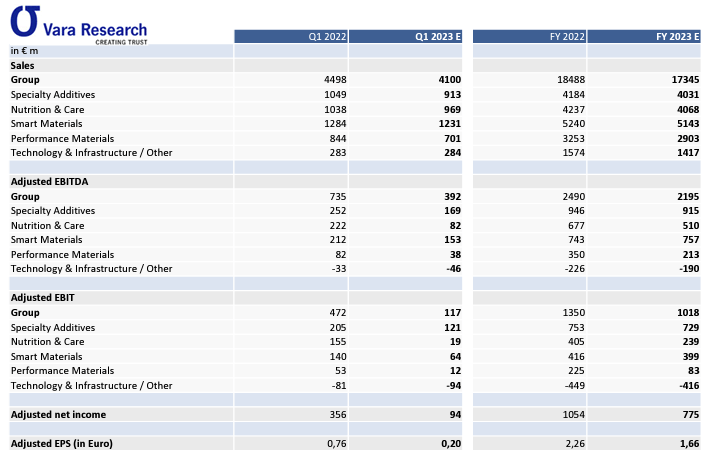

Double-checking VARA consensus expectations (Fig 1), Evonik missed the top-line sales but beat analyst estimates on both adjusted EBITDA and EPS. Despite a difficult first quarter in sales, the company confirmed its 2023 revenue guidance between €17 and 19 billion. Going down to the P&L analysis, it is important to report that our investment upside is well in line with Mare Evidence Lab's expectations. With lower volumes due to customer destocking, the Specialties division recorded positive pricing with a clear positive trajectory in order books for Q2 (emphasized by the management in the Q&A analyst call). In Q1, with clientele destocking activities, the Evonik facility rate declined, and with high production fixed costs, the segment-adjusted margin was lower than anticipated. Looking at Smart Materials, we positively report the PA12 ramp-up. This division was also negatively impacted by lower output but was totally offset by strong pricing activity across all businesses. The adjusted EBITDA margin was back to double-digit and signed a 13.8%. There is a maintenance planned for Q2.

{kind=link}

Source: VARA consensus Fig 1

{kind=link}

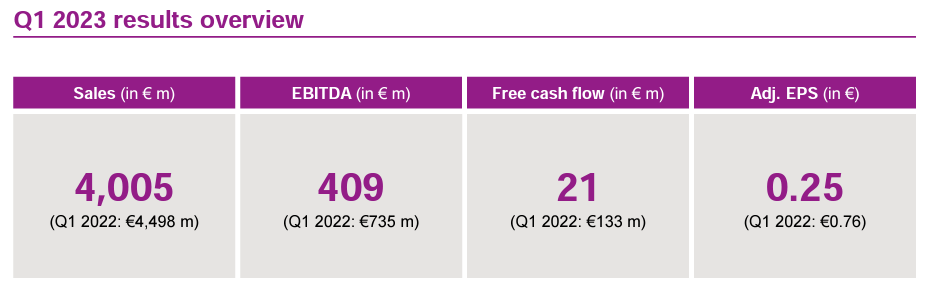

Source: Evonik Q1 results presentation - Fig 2

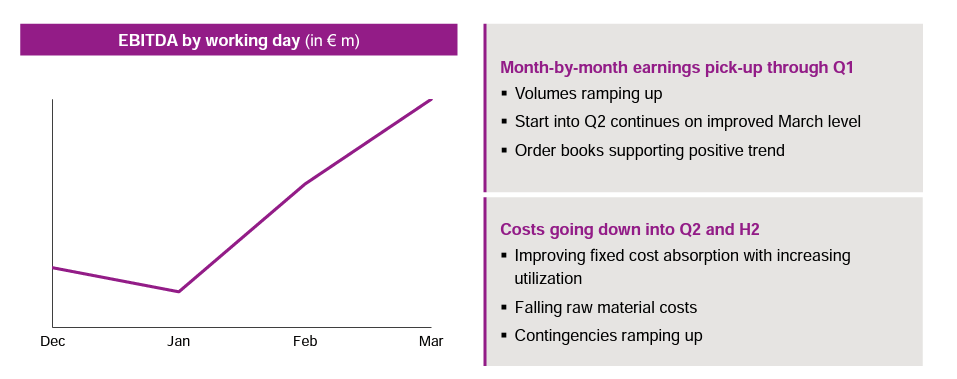

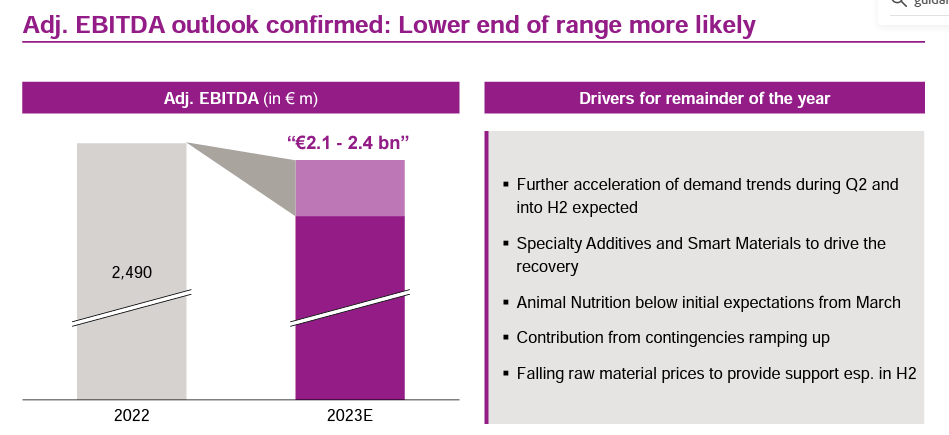

The Q1 was characterized by weak demand, with clients still destocking; however, there is a clear improvement in the EBITDA evolution between early January and March-end (Fig 3). All in all, Evonik reported an adjusted EBITDA of €409 million with a minus 44% on a yearly basis. In Q4, the German chemical player was implying an improving EU demand in the second part of the year. We were already skeptical but this quarter, the company confirmed its 2023 guidance with a likely EBITDA estimate of €2.1 billion (Fig 4).

{kind=link}

Fig 3

{kind=link}

Fig 4

Aside from the quarterly financial consideration, it is key to recap our upside:

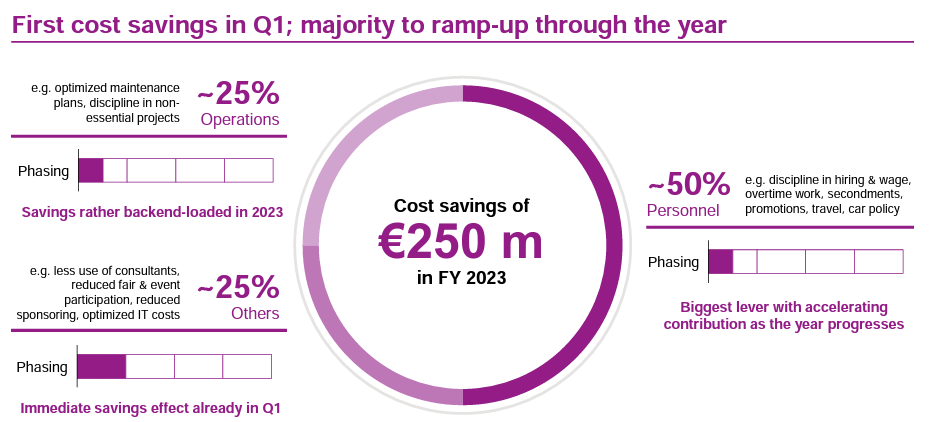

- Cost-saving initiatives are underway. The company confirmed a lower bonus for 2022 and decided to cut its external consultants as well as we are estimating a reduction in business travel. With more discipline in hirings, 2023 targets were confirmed at 250 million (Fig 5);

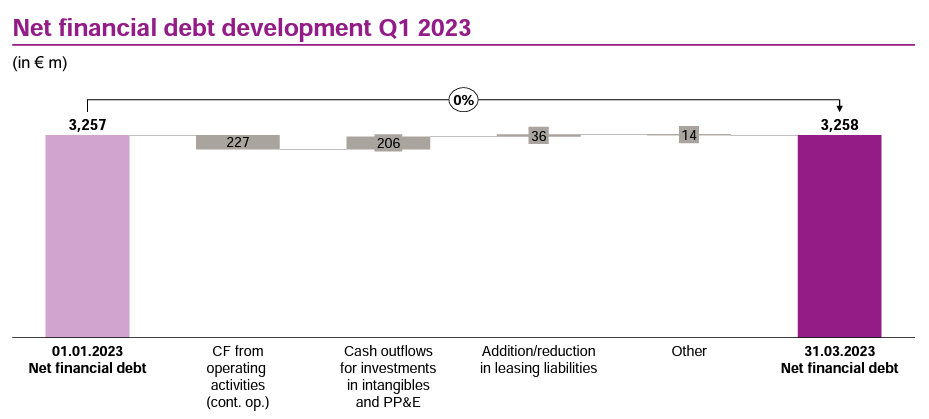

- Debt evolution. Net financial debt was unchanged in the quarter, and there was a net working capital support on a yearly basis (well anticipated in our expectation). In detail, the company's debt has a long duration and pensions obligations have also a higher than 13years duration (Fig 6);

- Evonik's portfolio improvements continue. The company is moving with its announced portfolio disinvestment. Lulsdorf performance material facility was sold . And also, the superabsorbents disinvestment is underway . On the investment CAPEX, the company initiated a new world-scale operation for pharmaceutical lipids in the US and recently inaugurated a facility in Germany. 2023 CAPEX guidance was lowered from €975 million to €900 million.

{kind=link}

Fig 5

{kind=link}

Fig 6

Conclusion and Valuation

Mare's target price of €23 per share ($12.25 in ADR) remains unchanged due to lower net debt and CAPEX evolution that offset lower earnings. Despite positive trends in the mRNA and LNP segments, the company will benefit from the ongoing portfolio transformation. Therefore, we decided to maintain our buy rating. Evonik's dividend was also confirmed and the company continues to trade on average at a 10% discount within its peers. PA12 facility and capacity expansion with lower raw material and energy prices are supportive. Downside risks include higher commodity chemical prices, slower recovery in auto, lower-than-anticipated methionine prices, and higher logistic costs.

For further details see:

Evonik: Portfolio Reshaping Continues