AWK - Evoqua Water Technologies: Great Results Do Not Translate To A Great Prospect

Summary

- Evoqua Water Technologies continues to generate strong sales, profit, and cash flow growth.

- This trend will probably continue, but it's important to keep in mind the price being paid for growth.

- At the end of the day, shares aren't affordably priced at this point in time.

Although water makes up around 70% of the surface of the planet, it truly is one of the most vital resources we have. Not only is it necessary in order for life to continue, it's also true that only a small fraction of it is potable. Given the scarcity and significance of water in our world today, it should not be a surprise that there would be a number of companies dedicated to providing various goods and services aimed at handling, cleaning, transporting, etc… the water that we use.

One such firm that warrants attention is Evoqua Water Technologies ( AQUA ), an enterprise that provides its customers with mission-critical water and wastewater treatment solutions. Recent fundamental performance achieved by the company has been robust. This has made shares cheaper as time has gone on. But at the end of the day, shares don't look cheap to me. Although I acknowledge that the company is a high-quality firm that would likely continue to fare well down the road, I do think that shares are more or less fairly valued at this moment. And because of that, I've decided to keep my ‘hold’ rating on its stock to reflect my view that shares should generate upside or downside that more or less match the broader market moving forward.

Surpassing expectations

In May of 2022, I wrote an article discussing whether it made sense to buy into shares of Evoqua Water Technologies or not. Leading up to that point, shares of the company had experienced a great deal of downside, with the pain surpassing even what the broader market had experienced. Even though this was what was transpiring, fundamental performance for the company was stronger than it had been one year earlier and the trend for the firm continued to show signs of improvement.

But because of how shares were priced, I felt as though there were better prospects to be had and, as a result, I kept the company at the ‘hold’ level that I had assigned it previously. Since then, the market has disagreed with my assessment. While the S&P 500 is down 2.9%, shares of Evoqua Water Technologies have generated upside for investors of 13.9%.

{kind=link}

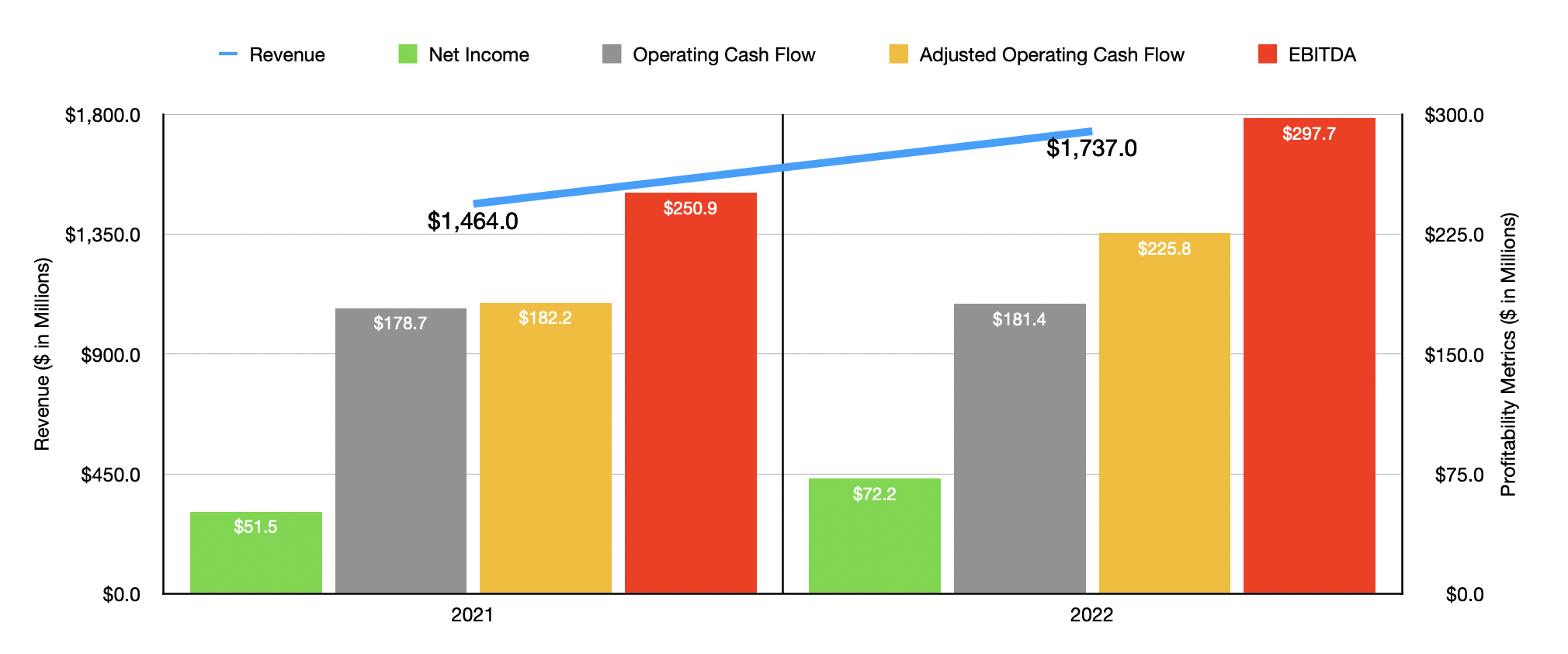

When I last wrote about the enterprise, we only had data covering through the second quarter of its 2022 fiscal year. Today, that data now extends through the rest of that year. For 2022 as a whole, revenue came in at $1.74 billion. That's roughly 19% higher than the $1.46 billion generated in 2021. This increase, according to management, was driven largely by a 22.2% surge in product sales. Services revenue, meanwhile, increased a more modest but still impressive 13.5%.

Most of the growth for the company came from organic means, with higher pricing and higher product and services volume adding 10.2%, or $149.4 million, to the company's top line. Inorganic revenue, largely centered around acquisition activities, added a further 9.4%, or $137.1 million, to the company's revenue. It is worth noting that the firm was hit negatively to the tune of $13.8 million thanks to foreign currency fluctuations.

The rise in revenue for the company, especially since it was driven by both higher pricing and higher volume, resulted in a significant improvement in profitability. Net income shot up from $51.5 million to $72.2 million. Operating cash flow was a bit more tepid, climbing from $178.7 million to $181.4 million. But if we adjust for changes in working capital, the metric would have risen a very impressive 23.9% from $182.2 million to $225.8 million. In addition to that, we also have data for EBITDA. Based on what's provided, this figure rose from $250.9 million to $297.7 million.

{kind=link}

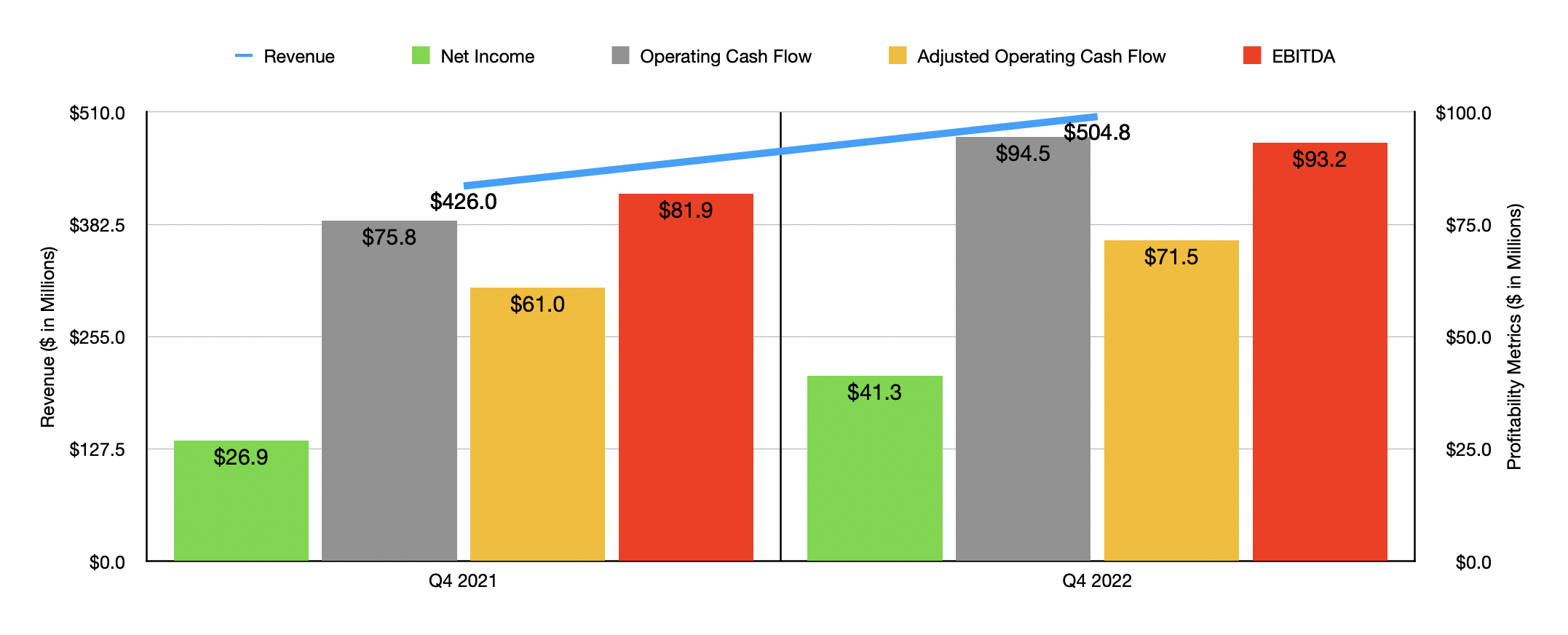

Given current economic concerns, I can understand why some investors would be wondering if the firm was showing any weakness toward the end of 2022. The answer to that would be no. Sales in the final quarter of the year totaled $504.8 million. That's 18.5% above the $426 million reported in the final quarter of 2021. Net income shot up from $26.9 million to $41.3 million. Operating cash flow expanded from $75.8 million to $94.5 million, with the adjusted figure for this increasing from $61 million to $71.5 million. And finally, EBITDA for the enterprise rose from $81.9 million to $93.2 million.

In fact, the picture for the company is going so well that management has provided some fairly detailed guidance when it comes to the 2023 fiscal year. Revenue is expected to come in at between $1.81 billion and $1.89 billion. Using the midpoint for this, sales should increase by roughly 6.5%. The firm is also forecasting EBITDA of between $310 million and $330 million. That implies a year-over-year increase of between 4% and 11%. If we assume that other profitability metrics will rise at the same rate that EBITDA it's forecast to, we should anticipate net income of $77.6 million and adjusted operating cash flow of $242.7 million.

{kind=link}

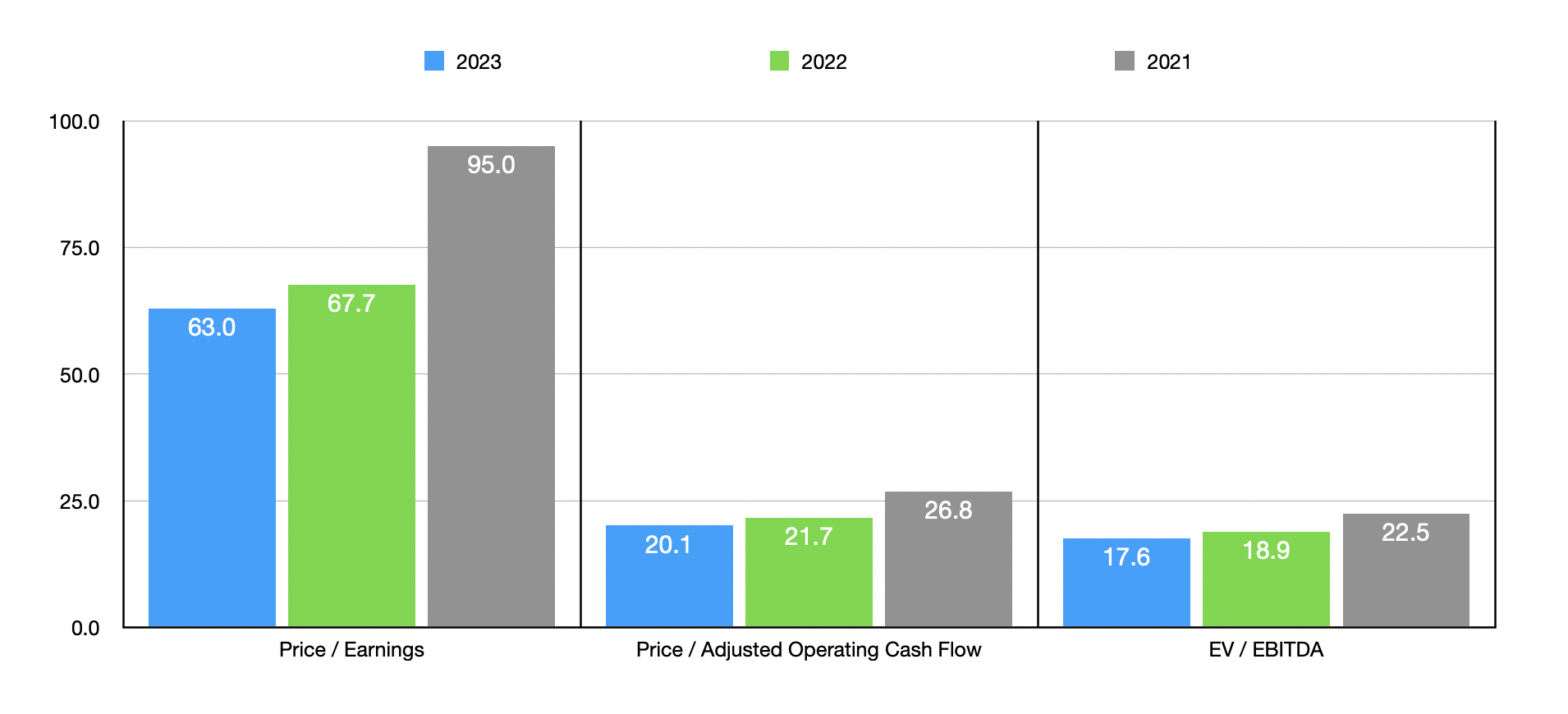

Using these figures, we can effectively price the company. The results can be seen in the table above. Given timing and the uncertainty that the future holds, I would like to emphasize the valuation of the company using 2022 data. At present, this would imply a price-to-earnings multiple of 67.7, a price to adjusted operating cash flow multiple of 21.7, and an EV to EBITDA multiple of 18.9. For context, I also compared the company to five similar enterprises.

On a price-to-earnings basis, these companies ranged from a low of 21.8 to a high of 66.6. In this case, Evoqua Water Technologies was the most expensive of the group. The picture changes when we use the price to operating cash flow approach, with the multiples ranging between 24.5 and 71.6 resulting in our prospect being the cheapest of the group. And finally, using the EV to EBITDA approach, the range came in at between 14 and 28.2. In this scenario, two of the five companies were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Evoqua Water Technologies |

| 67.7 |

| 21.7 |

| 18.9 |

| Watts Water Technologies ( WTS ) |

| 22.5 |

| 37.9 |

| 14.0 |

| Flowserve ( FLS ) |

| 49.2 |

| 27.4 |

| 20.5 |

| Chart Industries ( GTLS ) |

| 66.6 |

| 71.6 |

| 28.2 |

| Waters Corp ( WAT ) |

| 28.1 |

| 31.0 |

| 20.4 |

| American Water Works Company ( AWK ) |

| 21.8 |

| 24.5 |

| 14.5 |

Takeaway

Based on how things are flowing right now, I can only say that I continue to be impressed by Evoqua Water Technologies from a fundamental perspective. The company is most definitely a healthy player in its space and it has shown no signs of weakness in the current environment. For those who have a very long-term investment horizon, I can understand the allure of the company. But because of how pricey shares are, I cannot get behind it from a bullish perspective. So unless the share price drops from here or fundamentals improve even further, I must keep it rated a ‘hold’ for now.

For further details see:

Evoqua Water Technologies: Great Results Do Not Translate To A Great Prospect