NFLX - EVT: Solid CEF Offering From Eaton Vance With A 7.78% Yield

2023-04-17 18:39:10 ET

Summary

- Investors today are starved for income, as the persistently high inflation rate is eroding our purchasing power.

- Eaton Vance Tax-Advantaged Dividend Income Fund invests in a portfolio of dividend-paying stocks intended to provide investors with a growing level of sustainable income.

- The closed-end fund actually obeys its dividend mandate, unlike some of Eaton Vance's other funds.

- The fund has a reasonable chance to outperform if the Federal Reserve sticks to its guns this year and does not pivot.

- The fund is trading with a sustainable 7.78% yield and at an attractive valuation.

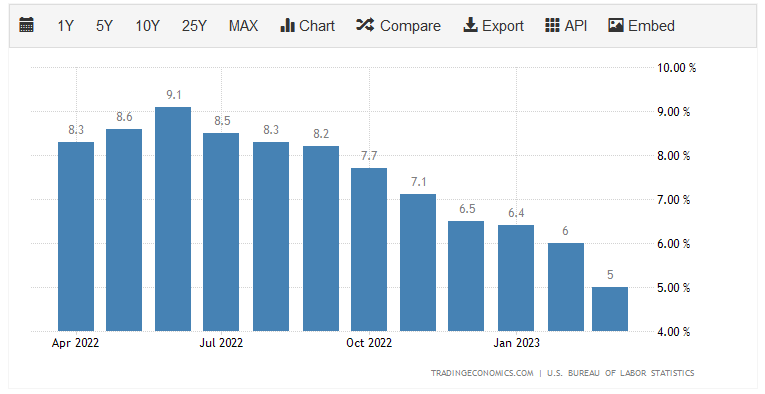

It is a point of little dispute that one of the biggest problems facing the average American today is the rapidly rising cost of living. This is quite clearly showcased in the consumer price index, which is risen by 6% or more year-over-year in eleven of the past twelve months:

{kind=link}

This has had a devastating impact on those of limited financial means due to the fact that food and energy have seen some of the greatest price increases. As I pointed out in a recent blog post , this high inflation has forced many people to take on second jobs, go into debt, or draw down their savings just to maintain their lifestyles and keep their families fed.

As investors, we are certainly not immune to this. After all, we all have bills to pay and need to keep ourselves fed too. Fortunately, we do have somewhat better methods that we can employ to obtain the extra income that we need to accomplish these things. This is because we can put our money to work for us and have it earn us extra income. One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in income generation.

These funds are, unfortunately, not very well-followed in the investment media and many financial planners are unfamiliar with them. As such, it can be more difficult than we would like to obtain information about these entities. This is quite unfortunate, as closed-end funds offer a number of advantages over the familiar open-end and exchange-traded funds. The most important of these advantages is that these companies have the ability to employ certain strategies that allow them to pay out a much higher yield than pretty much anything else in the market. That makes these funds ideal for any investor that is seeking an income.

In this article, we will discuss the Eaton Vance Tax-Advantaged Dividend Income Fund ( EVT ), which is one CEF that can be used to earn an income. This fund’s income potential is perhaps best illustrated in the fact that the fund has a 7.78% yield as of the time of writing, which is quite a bit higher than the 1.57% current yield of the S&P 500 Index (SP500). I have discussed this fund before, but a few months have passed since that time, so obviously a few things have changed. This article will, therefore, focus specifically on these changes as well as provide readers with an updated analysis of the fund’s financial condition. Let us investigate and see if the fund could be a good addition to your portfolio today.

About The Fund

According to the fund’s webpage , the Eaton Vance Tax-Advantaged Dividend Income Fund has the stated objective of providing its investors with a high level of after-tax total return. It is interesting to note that Eaton Vance is a bit strange among fund providers in that it does not directly provide either the fund’s objective or its investment strategy directly on the webpage. Rather, it is necessary to download the fund’s fact sheet in order to obtain this information. That is admittedly a bit annoying, but it is not the end of the world. The fund’s objective makes a lot of sense as the name implies that the fund is a common equity fund. After all, dividends are only paid by common or preferred equity securities. A look at the fund’s portfolio certainly confirms this as its assets are 78.76% invested in common equity alongside a 13.11% allocation to preferred stock. The remainder of the fund is invested in bonds and cash:

CEF Connect

Common equities are, by their very nature, a total return investment. After all, investors purchase these securities in order to generate an income via dividends paid by a given company as well as benefit from capital gains as the issuing company grows and prospers. This is in line with the fund’s description of its strategy as provided in the fact sheet:

“The Fund invests primarily in dividend-paying common and preferred stocks and seeks to distribute a high level of dividend income that qualifies for favorable federal tax income treatment. The Fund employs a value investment style and seeks to invest in dividend-paying common stocks that have the potential for meaningful dividend growth.”

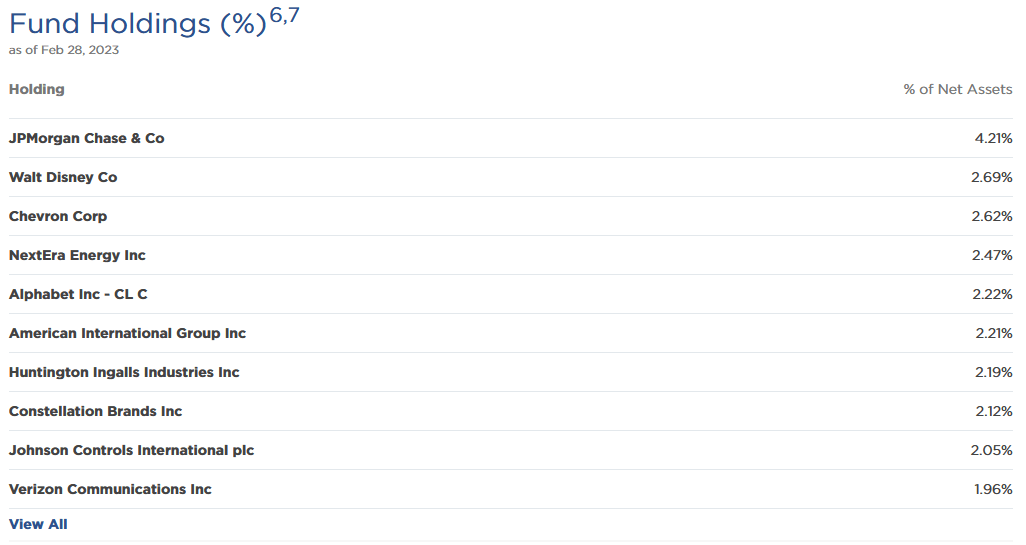

This is a somewhat similar objective to what Eaton Vance provides for some of its other income-focused equity closed-end funds. However, this one differs in that the fund’s portfolio actually aligns with the description provided in the fact sheet. Here are the largest positions in the portfolio:

{kind=link}

The big thing to note here is that we do not see a high allocation to the mega-cap technology stocks, as we do in Eaton Vance’s other equity-income closed-end funds. The fund’s only position to these stocks is Alphabet/Google ( GOOG ), and that accounts only for 2.22% of the portfolio. This is nice because as I noted before , these companies generally underperformed the S&P 500 Index by a significant margin in 2022 and they are still somewhat overpriced given today’s economic realities. They also pay no dividend, which would directly contradict the fund’s supposed focus on dividend-paying stocks. As it stands though, Alphabet and The Walt Disney Company ( DIS ) are the only companies among the fund’s largest position that does not pay a dividend. In fact, most of the companies listed above have fairly respectable yields:

| Company |

| Dividend Yield |

| JPMorgan Chase & Co. ( JPM ) |

| 2.88% |

| Walt Disney Co. |

| 0.00% |

| Chevron Corp. ( CVX ) |

| 3.50% |

| NextEra Energy ( NEE ) |

| 2.40% |

| Alphabet |

| 0.00% |

| American International Group ( AIG ) |

| 2.49% |

| Huntington Ingalls Industries ( HII ) |

| 2.36% |

| Constellation Brands ( STZ ) |

| 1.56% |

| Johnson Controls International ( JCI ) |

| 2.50% |

| Verizon Communications ( VZ ) |

| 6.65% |

As stated earlier, the S&P 500 Index pays a 1.57% yield as of the time of writing, so among those companies that do pay a dividend, only Constellation Brands is below this yield (and not by very much). Walt Disney has paid dividends in the past and many analysts expect that it will once its financial troubles are resolved so that company is likewise not really out of place here. Thus, Alphabet stands as the sole company that does not make much sense for a dividend-oriented fund, but it only accounts for 2.22% of the portfolio so we can excuse that. Overall, this looks like a reasonable portfolio for a dividend-focused fund as we see a nice variety of sectors represented here for diversification purposes.

There have been surprisingly few changes to the portfolio in the past three months since we last looked at the fund. In fact, the only change of note is that ConocoPhillips ( COP ) was removed and replaced with Verizon Communications. We also see several weighting changes, but that could easily be explained by one stock outperforming another in the market. The fact that we do see few changes could lead one to believe that this fund has a fairly low annual turnover. This is, in fact, true as the fund’s 31.00% turnover is one of the lowest of any equity closed-end funds.

The reason that this is important is that it costs money to trade stocks or other assets, which is billed directly to the shareholders of the fund. This creates a drag on the portfolio’s performance and makes management’s job more difficult. After all, the fund’s management will need to generate a return that is sufficient to both overcome these added expenses and still have enough left over to satisfy the shareholders. This is a task that very few management teams achieve on a consistent basis, which tends to result in actively-managed funds underperforming their benchmark indices over time. The Eaton Vance Tax-Advantaged Dividend Income Fund does not specify an actual benchmark in its documentation, but it did perform reasonably well in 2022 as it outperformed the S&P 500 Index:

Eaton Vance

The fund underperformed the S&P 500 Index over more extended periods of time, though. This might be due to its dividend focus. As I pointed out in a previous article , an outsized proportion of the returns of the S&P 500 Index over the past fifteen years came from the mega-cap technology stocks as well as similar companies like Netflix ( NFLX ). For the most part, dividend stocks lagged the broader index over much of that period. However, these stocks also held up much better during 2022 for the same reason. As their valuations were not nearly as artificially inflated by the free money, they did not have nearly as far to fall during the early stages of the bubble bursting. Rather, most of these companies actually have the cash flow and earnings to support their valuations.

These are probably the best companies to hold right now, particularly considering that the economy could very easily fall into a recession in the near future. If this happens, and if Chairman Powell’s comments about there being no Federal Reserve pivot in 2023, it seems likely that this fund will outperform an S&P 500 index fund, although it may not beat a more dividend-focused index.

Leverage

As mentioned earlier in this article, closed-end funds like the Eaton Vance Tax-Advantaged Dividend Income Fund have the ability to employ certain strategies that have the effect of boosting their yields beyond that of any of the underlying assets. One of these strategies is the use of leverage. Basically, the fund borrows money and then uses that borrowed money to purchase dividend-paying common and preferred stocks. As long as the purchased assets have a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much debt, as that would expose us to excessive risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. Fortunately, the Eaton Vance Tax-Advantaged Dividend Income Fund fulfills this requirement. As of the time of writing, the fund’s levered assets comprise 20.25% of the fund’s assets. Thus, it appears that this fund is striking a reasonable balance between risk and reward.

Distribution Analysis

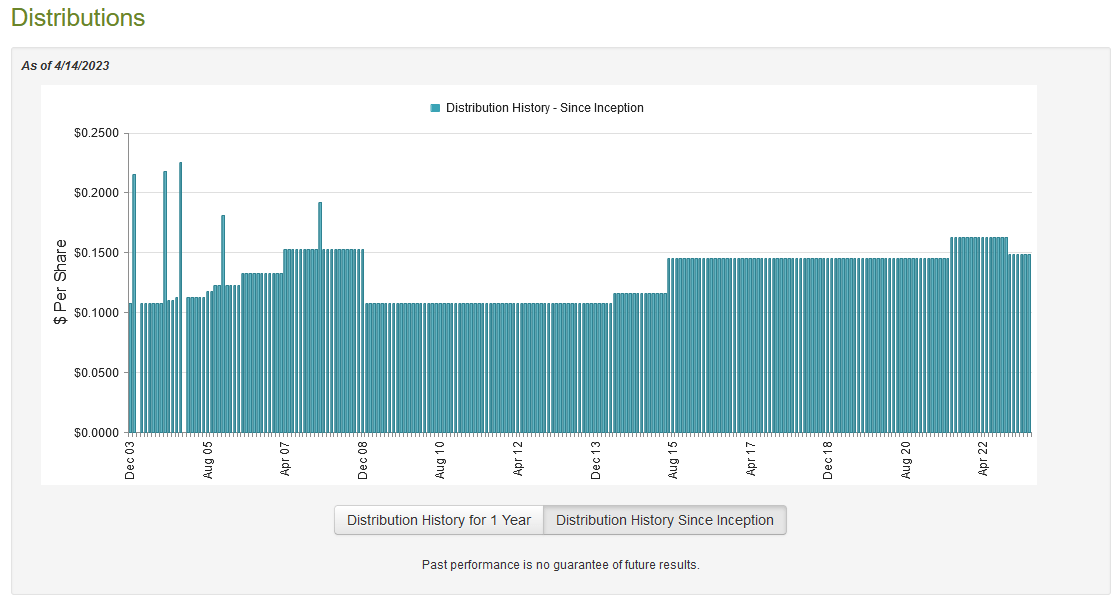

As mentioned earlier in this article, the primary objective of the Eaton Vance Tax-Advantaged Dividend Income Fund is to provide its investors with a high level of total return. In order to achieve that, the fund invests its assets primarily in dividend-paying common and preferred stocks, then applies a layer of leverage to boost the effective return. The twist here is that the fund aims to pay out all of its returns to the shareholders in the form of distributions. Ideally, the fund will retain a stable share price and pay everything out. We can probably assume that this would result in a very high yield, considering that the S&P 500 Index averaged an 11.88% annual total return over the period stretching from its inception in 1957 through the end of 2021. This is certainly the case as the fund pays out a monthly distribution of $0.1488 per share ($1.7856 per share annually), which gives it a 7.78% yield at the current price. While the fund did cut its distribution back in November of last year, its distribution history is generally positive over time:

{kind=link}

As we can see, the fund grew its distribution since 2009, which is a feat that very few closed-end funds have managed to accomplish. The recent cut is disappointing, but the distribution is still higher than it was back in 2020. It appears then that the fund’s strategy of investing in companies that should be able to generate sustainable dividend growth has benefited its shareholders. This is something that is quite nice to see given today’s high inflation rate. This is because inflation is constantly reducing the number of goods and services that we can purchase with the distribution that the company pays out. The fact that it grows its distribution over time helps to offset this effect and maintains the purchasing power of the distribution. However, this is mostly only true over the long term, since it clearly has not kept its distribution stable in terms of purchasing power over the past year or two. Then again, very few companies have been able to accomplish this. The fact that the fund had to cut its distribution last year is likely to concern those investors that are looking for a safe and secure distribution to use to pay their bills or finance their lifestyles, but it is important to keep in mind that anyone purchasing the fund today will receive the current distribution at the current yield. As such, the most important thing is the fund’s ability to maintain its current distribution and not its past history. Thus, let us take a look at that.

Fortunately, we do have a somewhat recent document to consult for the purposes of our analysis. The fund’s most recent financial report corresponds to the full-year period that ended on October 31, 2022. This report will unfortunately not include any information regarding the fund’s performance over the past few months, but it should still give us a good idea of how the fund weathered the incredibly challenging conditions that dominated the market during 2022, as well as the events that led up to the distribution cut. During the full-year period, the Eaton Vance Tax-Advantaged Dividend Income Fund received $51,124,136 in dividends and $18,901,191 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund had a total investment income of $71,564,695 over the full-year period. It paid its expenses out of this amount, which left it with $42,568,109 available for shareholders. This was, unfortunately, nowhere close to enough to cover the $144,381,379 that the fund actually paid out during the period. At first glance, this will likely be quite concerning as the fund clearly does not have enough net investment income to cover its distributions.

However, the fund does have other methods through which it can obtain the money that it pays out to its investors. The most important of these is capital gains, which is a significant percentage of the total investment return that we get from the stock market in a given year. The fund was actually fairly successful at this during 2022, which will probably be a bit surprising. It reported net realized gains of $100,954,837, but this was offset by net unrealized losses of $354,193,412 during the year. Overall, the fund’s assets declined by $332,291,317 over the course of the year after accounting for all inflows and outflows. This is concerning as it clearly illustrates that the fund failed to cover its distribution in 2022. However, there are two points to consider here:

- The fund’s net investment income combined with its net realized gains was very close to the total amount distributed. These two line items totaled $143,522,946, which was almost enough to cover the $144,381,379 that was distributed. In fact, the fund was only $858,433 short, which is not really that much money compared to the size of the fund’s portfolio.

- The fund’s assets as of November 1, 2022, were higher than it had on November 1, 2020. Over that two-year period, the fund’s assets went from $1,544,154,284 to $1,774,707,281 despite the fact that it paid out its distributions all through that period. Thus, the fund did manage to generate sufficient returns to cover its distributions over the two-year period with a significant amount of money left over.

Overall, the distribution is probably fine, and the fund may not have actually needed to cut it. The cut was most likely an attempt to preserve its capital and we may see a near-term increase or a special distribution if the fund performs reasonably well for another year or two. In short, though, there does not appear to be anything to worry about here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Eaton Vance Tax-Advantaged Dividend Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of April 14, 2023 (the most recent date for which data is available as of the time of writing), the Eaton Vance Tax-Advantaged Dividend Income Fund has a net asset value of $23.61 per share but the shares only trade for $23.09 each. That represents a 2.20% discount to net asset value at the current price. This is reasonably in line with the 2.75% discount that the shares have traded at on average over the past month, so the price seems acceptable today.

Conclusion

In conclusion, the Eaton Vance Tax-Advantaged Dividend Income Fund looks like one of the better equity-income offerings from this fund house. The portfolio is reasonably well-diversified across sectors, and it seems likely to outperform the S&P 500 Index unless we get another bubble. As such a bubble would only occur if the Federal Reserve were to pivot, it seems a bit unlikely in the near term. Admittedly, some investors might be turned off by the distribution cut, but Eaton Vance Tax-Advantaged Dividend Income Fund’s finances actually do not look too bad, and when we combine this with a reasonable valuation, there could be a lot to like here.

For further details see:

EVT: Solid CEF Offering From Eaton Vance With A 7.78% Yield