EVV - EVV: Nice Discount But Best To Sit And Wait For More Visibility

2023-05-05 05:18:18 ET

Summary

- Investors are desperately in need of income as inflation remains high and the markets are challenged.

- EVV invests in a portfolio of bonds that should have relatively low inflation-rate risk, which would have been appealing over the past year.

- The Federal Reserve has apparently paused its rate hike campaign, so the need for a low-duration fund is seemingly less than it once was.

- The fund is heavily invested in junk bonds and floating-rate notes, but credit quality is still acceptable.

- The fund appears to be overdistributing by a lot and it recently had to cut the payout.

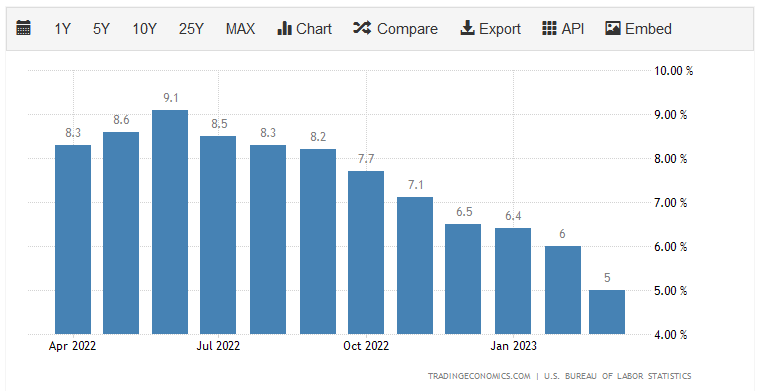

Undoubtedly, the biggest challenge facing the average American household today is the rapidly rising cost of living. This is evident in the consumer price index, which theoretically measures changes in the price of a commonly purchased basket of goods. In eleven of the past twelve months, the index has shown at least a 6% year-over-year increase:

{kind=link}

This is substantially higher than the 2% annual rate that the Federal Reserve attempts to achieve through its monetary policy. It has also been significantly above the federal funds rate for much of the period, resulting in negative real interest rates. This has punished savers and made it quite difficult for retirees and others that are dependent on their savings for their livelihoods. It has also proven difficult for anyone that is still working, as real wage growth was down for 24 straight months as of April 2023. This is the reason why a growing number of people are taking on second jobs or entering the gig economy just to get the money that they need to sustain their lifestyles.

As investors, we have certainly been affected by this as we have bills to pay and require food for sustenance. It is likely that most of us have found that it is more difficult to accomplish these things due to rising prices and the market turbulence over the past eighteen months. Fortunately, there are some solutions available to us that do not require new jobs. After all, we have the ability to put our money to work for us and earn an income that way. One of the best ways to do this is to purchase shares of a closed-end fund that specializes in the generation of income. These funds are unfortunately not very well-followed in the financial media and most investment advisors are not particularly familiar with them. Thus, it can be difficult to obtain the information that we would really like to have to make an informed investment decision. That is a problem because these funds have a number of advantages over ordinary open-ended or exchange-traded funds. One of these advantages is that a closed-end fund can use certain strategies that boost its yield well beyond that of the underlying assets or anything else in the market.

In this article, we will discuss the Eaton Vance Limited Duration Income Fund ( EVV ), which currently yields a very impressive 10.09% at the current price. I have discussed this fund before, but a few months have passed since that time so naturally a few things have changed. This article will therefore focus specifically on those changes and provide an updated analysis of the fund's financial condition. Let us investigate and see if this high-yielding fund could be a good addition to your portfolio today!

About The Fund

According to the fund's webpage , the Eaton Vance Limited Duration Income Fund has the stated objective of providing its investors with a high level of current income. This makes sense considering that the name of the fund implies that it invests in relatively short-dated bonds or other fixed-income securities that are minimally affected by interest rate changes. After all, duration is a measure of the degree to which a change in interest rates affects a bond's price. The fund's fact sheet confirms this, as it specifically states that it will invest in securities that have a duration of between one and five years. As would be expected then, the fund's portfolio is almost entirely invested in bonds, with a small amount of cash:

CEF Connect

Curiously, the fund's fact sheet states that it provides exposure to a broad range of income asset classes. That is probably not the case unless it is investing in things other than traditional fixed-rate bonds. The fund is doing exactly that as 32.4% of the portfolio is invested in senior loans:

Eaton Vance

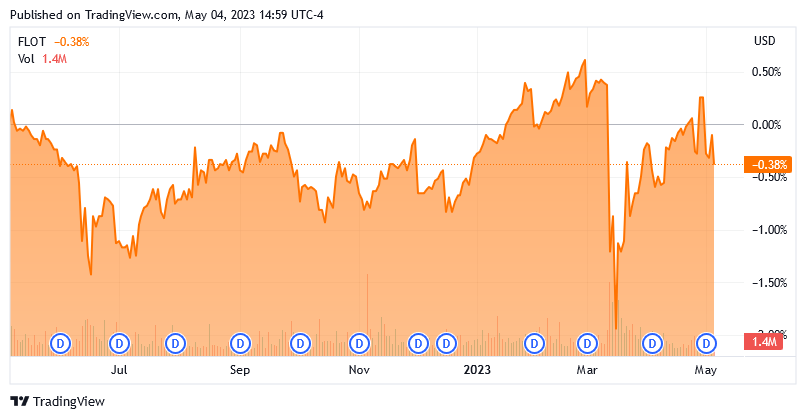

Senior loans are a bit different than traditional bonds. These are bank loans that have been securitized and sold off to investors so that the bank does not have to keep a significant portion of its capital tied up in just a few loans. The same thing is done very often with mortgages, and it is not necessarily a sign that the loans are expected to go into default or anything like that. The defining characteristic of these securities is that they have floating interest rates. Thus, when interest rates are going up, the interest rates that are paid by these securities to investors also go up and vice versa. Thus, by definition, these securities would have a very limited duration since they do not have the usual interest rate risk that bonds have. We can see this in the fact that the Bloomberg US Floating Rate Note < 5 Yrs Index ( FLOT ) has been almost perfectly flat over the past year, significantly outperforming most bond indices:

{kind=link}

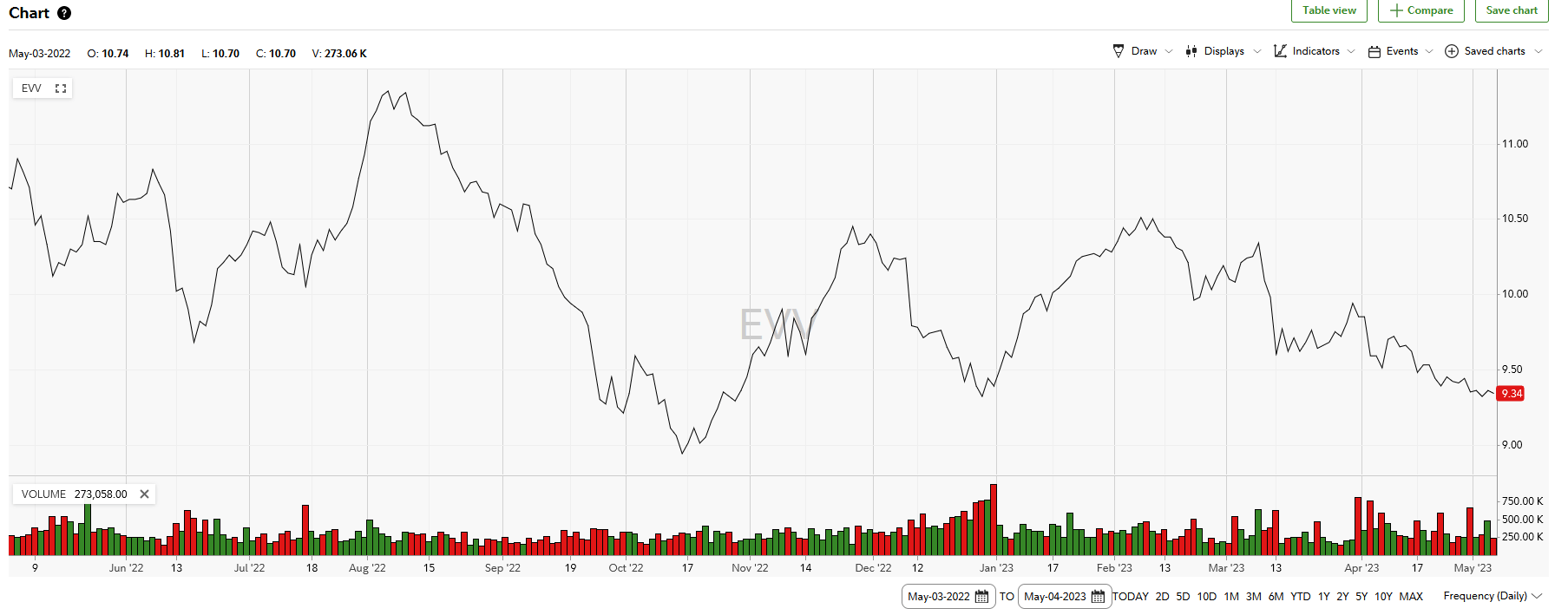

The fact that this fund contains such a high weighting to these securities thus should help this fund to be able to maintain a much more stable asset value over time than a traditional bond fund. That has proven not to be the case though as the fund's share price is down 13.04% over the past twelve months:

{kind=link}

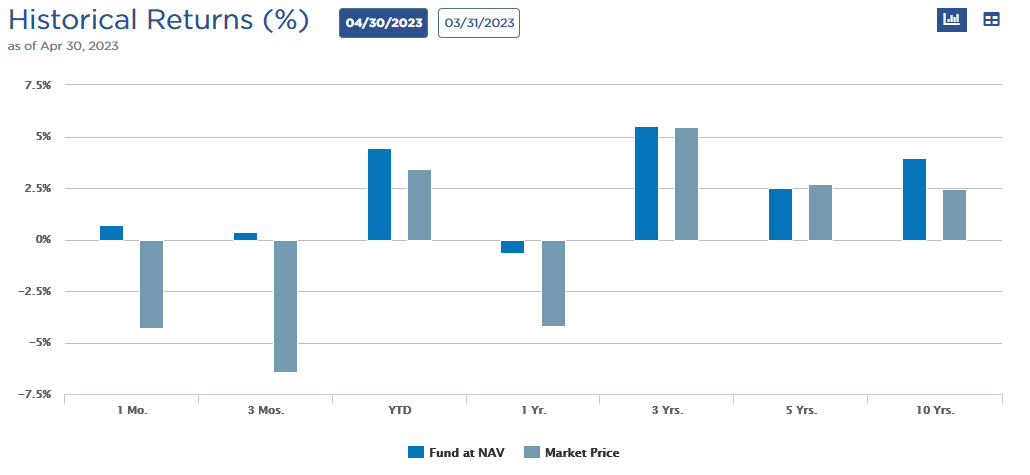

With that said, the fund has paid out a very high yield over that period, so its total return has been better than this chart would indicate. In fact, as of April 30, 2022, the fund's portfolio has delivered a -0.66% total return:

{kind=link}

As we can clearly see, the total return of the fund's shares over the time period has been very different than that. That has generally been the case over most of this year as the fund's shares declined in April as well as in the trailing three-month period, but the portfolio itself actually delivered a positive total return. This is something that is not exactly uncommon for a closed-end fund, and it can sometimes create an opportunity in which we can sometimes acquire the fund's assets for less than they are actually worth. We will discuss that later in this article. The big thing that we note here though is that the fund's portfolio has performed much better than its share price would suggest over most of the past year.

The fact that these floating-rate securities should hold their value reasonably well regardless of interest rate fluctuations is something that will probably appeal to more conservative investors. It is possible that such protection is not needed as much as it once was, though. Yesterday, the Federal Reserve hiked the target federal funds rate by 0.25% and implied that it would pause on further rate hikes. As bond prices move inversely to interest rates, the possibility of no further interest rate hikes could indicate that bond prices are likely to be much more stable going forward. With that said though, we still have numerous risks coming out of Washington with the debt ceiling and signs that inflation may not yet be completely under control, so there are still some possible risks inherent in the bond market and with ordinary bond funds. It is hard to see how those risks would not also affect senior bank loans like the ones in this fund.

One thing that may concern conservative investors, however, is the fact that this fund includes a significant amount of speculative-grade debt. This is inherent in senior loans, which are often taken out by companies that cannot obtain more traditional forms of financing, such as fixed-rate bonds. We also see in the table above that 29.4% of the fund's assets are invested in non-investment grade debt, which specifically refers to junk bonds. As a result, some people might be concerned with the risk that the fund loses money due to defaults. This may be an especially big concern today considering that the shrinking money supply has caused credit conditions to be much tighter than we have seen in years, which has made it challenging to roll over debt. A look at the credit ratings of the securities in the portfolio may exacerbate these concerns. Here is a summary of the credit ratings of the fund's holdings:

Eaton Vance

An investment-grade security is anything rated BBB or higher. As we can see, fully 63.7% of the fund's holdings consist of speculative-grade credit. However, 55.2% of that are securities rated BB or B, which are the two highest ratings possible for junk bonds. According to the official bond ratings scale , companies whose bonds have these ratings have the sufficient financial capacity to afford their current debt loads and can probably continue to do so even in the event of a short-term economic shock. Thus, the overall default risk here should be relatively low. When we also consider that the fund has 1,305 current holdings, we can also see that the impact of a single default on the fund should have virtually no measurable effect. Thus, investors should not really have to worry about losing money because of a single company going into default.

Leverage

In the introduction to this article, I stated that closed-end funds like the Eaton Vance Limited Duration Income Fund have the ability to employ certain strategies that boost the fund's leverage beyond that of any of the underlying assets. One strategy that is employed by this fund to accomplish that is the use of leverage. Basically, the fund borrows money and then uses those borrowed funds to purchase bonds and other income-producing securities. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to excessive amounts of risk. I do not typically like to see a fund's leverage exceed a third as a percentage of its assets for that reason. Unfortunately, this fund exceeds that level. As of the time of writing, the Eaton Vance Limited Duration Income Fund has levered assets comprising 34.94% of its portfolio. Granted, that is not very much above the prescribed limit, and considering that this fund invests in reasonably safe assets, it is probably okay. Thus, the balance between risk and reward is probably okay here, but I will admit that I would feel a bit more comfortable if it were to reduce its leverage.

Distribution Analysis

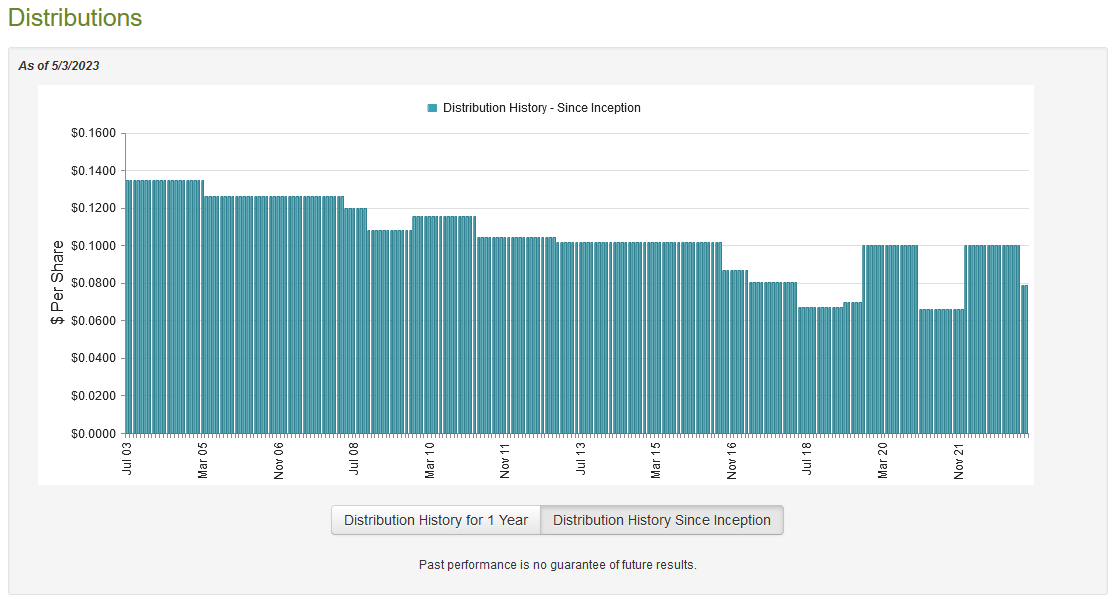

As mentioned earlier in this article, the primary objective of the Eaton Vance Limited Duration Income Fund is to provide its investors with a high level of current income. In order to accomplish that task, it invests in income-producing assets such as senior loans and junk bonds, which tend to have fairly high yields. The fund then applies a layer of leverage to boost these yields beyond those of any of the underlying assets. As such, we would likely assume that the fund itself pays a very high yield to its investors. That is certainly the case as the fund pays a monthly distribution of $0.0787 per share ($0.9444 per share annually), which gives it a 10.09% yield at the current share price. Unlike many of Eaton Vance's funds though, this one's distribution has varied quite a lot over the years:

{kind=link}

We can see that the fund cut its distribution back in April and again for May, which is quite disappointing. However, it is unsurprising since I pointed out in my last article on the fund that it would likely have to cut as its asset base has been steadily declining. Nonetheless, this is likely to be a bit of a turn-off for anyone that was seeking to use the fund as a steady and secure source of income with which to pay their bills and finance their lifestyles. However, it is important to keep in mind that anyone purchasing the fund today will receive the current distribution at the current yield. As such, the most important thing is how well the fund can carry its current distribution, so let us investigate that.

Unfortunately, we do not have a particularly recent document to use to conduct our analysis. The fund's most recent financial report as of the time of writing corresponds to the six-month period that ended on September 30, 2022. As such, it will not include any information about the fund's performance over the past seven months. That is very disappointing as this period would include the distribution cut as well as some volatility in the bond market. During the six-month period, the fund received $1,626,832 in dividends and $51,620,301 in interest from the investments in its portfolio. Overall, this gives the fund a total investment income of $53,247,133 over the six-month period. The fund paid its expenses out of this amount, which left it with $36,661,543 available for the shareholders. That was, unfortunately, nowhere close to enough to cover the $69,722,076 million that the fund distributed to its shareholders over the period. At first glance, this is likely to be concerning as the fund's net investment income was nowhere near sufficient to cover the distribution. This is a problem for a bond fund as we usually want these funds to at least be able to come close to covering their distributions solely through net investment income.

Naturally, though, the fund does have other means through which it can acquire the money that it needs to cover its distributions. For example, it might have earned a significant amount of money through capital gains. Despite the fact that the fund's holdings should have held up reasonably well in a rising interest rate environment, it still reported net realized losses of $11,090,983 and had another $189,511,356 net unrealized losses. Overall, the fund's assets declined by $236,400,482 over the period. Thus, the fund clearly failed to cover its distribution, which was also the case in the twelve-month period that directly preceded the period that was covered by this report. This certainly explains the fund's distribution cut last month, although it is difficult to fathom why it waited so long when it is clearly bleeding money. It remains to be seen how sustainable the new distribution will be and we will certainly want to review the full-year 2023 report when it is released.

Valuation

It is critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Eaton Vance Limited Duration Income Fund, the usual way to value it is to look at the fund's net asset value. The net asset value of a fund is the total current market value of all of the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. As we saw earlier, the fund's portfolio has generally outperformed its market price over the past several months so this could be the case today. As of May 3, 2023 (the most recent price for which data is available as of the time of writing), the Eaton Vance Limited Duration Income Fund had a net asset value of $10.48 per share but the shares currently trade at $9.36 each. This gives the fund's shares a 10.69% discount to net asset value at the current price. This is certainly a respectable discount that is very much in line with the 10.87% discount that the shares have had on average over the past month. As such, the current price looks reasonable.

Conclusion

In conclusion, the Eaton Vance Limited Duration Income Fund appears to be using a reasonable strategy for a rising interest rate environment. In particular, it should not be as affected by rising rates as most bond funds. However, the fund is clearly overdistributing as it is unable to sustain its distribution and is bleeding money. That was probably also the case over the past several months despite the fact that the fund did not cut its payout. The price currently looks reasonable, but I would wait for the fund to release a more recent financial report before buying in as its financial condition very likely deteriorated.

For further details see:

EVV: Nice Discount, But Best To Sit And Wait For More Visibility