EWA - EWA: I See Some Value 'Down Under' In 2024 (Rating Upgrade)

2024-01-22 06:14:49 ET

Summary

- I am upgrading my outlook on the iShares MSCI Australia ETF to "buy" for a number of reasons.

- Gains in US markets are becoming increasingly concentrated in a few stocks, leading me to look for opportunities outside of the US market.

- The Australian consumer is in decent shape, and Australian banks are poised to collect high amounts of interest this calendar year.

Main Thesis & Background

The purpose of this article is to evaluate the iShares MSCI Australia ETF ( EWA ) as an investment option at its current market price. This fund is managed by BlackRock ( BLK ), and its objective is to "track the investment results of an index composed of Australian equities".

A little under a year ago I covered EWA and suggested that there wasn't a strong case for buying the fund. I saw some benefits to owning exposure to Australia, but there were notable drawbacks as well. Looking back, this caution made sense as EWA has largely lagged my benchmark for large-cap non-US stocks (the S&P 500):

Fund Performance (Seeking Alpha)

With 2024 underway and US markets performing strongly, staying diversified is top of mind for me. I imagine this is true for many of my followers, which is leading me to consider amplifying my exposure to non-US developed markets here in Q1. This extends to Australia, and EWA, and I do indeed see a case to be made for this ETF. Thus, I am upgrading my outlook to "buy", and I will list out the reasons why in detail below.

Concentrated Gains In US

While the focus of this article is Australia, I will take the first paragraph to discuss the reasons for diversifying away from America. To reiterate for those who may not follow me closely, I am a net-long US stocks. They make up the bulk of my portfolio and I am definitely not a "bear" on the S&P 500. However, that doesn't mean I see a strong buy case for the index all the time. I rarely sell off my US holdings in the S&P, Dow, or NASDAQ, but as a working professional I have new cash coming in every week I want to deploy. When I see a less-than-favorable valuation metric for large-cap US stocks, I tend to look elsewhere.

That is roughly the case right now. We saw a very strong 2023 for US indices, and 2024 is starting off pretty well too. I will sit back and enjoy the ride to be sure. But I am not ignoring the fact that gains are getting increasingly concentrated in a handful of stocks (i.e. the Mag 7). This will put further gains to the test as we move deeper into 2024, in my opinion:

2023 Returns (USA) (FactSet)

This has pushed up relative valuations for US stocks as a whole, but primarily for the S&P 500 and NASDAQ 100 which are top-heavy those "Mag 7" names. This is not inherently "bad" if investors keep piling into this theme and pushing the stocks higher - but nothing goes up forever. This is central to why I am trying to round out my portfolio with both small-cap US stocks and large-cap international holdings. One way to do this is, of course, Australia.

Aussie Consumer Is In Okay Shape

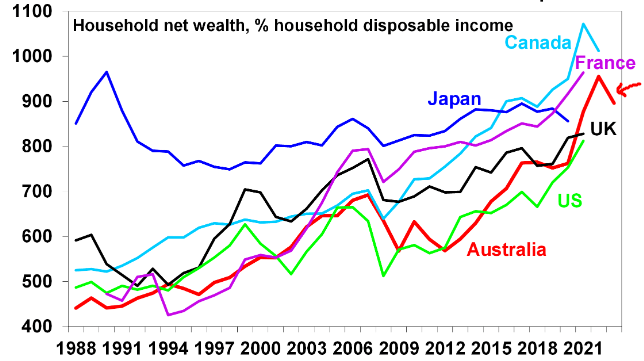

One principal reason for considering EWA at the expense of other developed world options has to do with the state of the consumer. Higher interest rates, inflation, and climbing mortgage costs are all headwinds, similar to what we are seeing here in North America. So I would caution readers not to ignore these risks. But the reality is that Australian households are in decent shape compared to their peers. While net wealth (as a percentage of disposable income) has declined in the short-term, it is still at the top end compared to other nations in the OECD developed world grouping:

Household Debt Figures (FactSet)

{kind=link}

This bodes well for the year ahead and helps set up funds like EWA for continued gains as long as the economy doesn't stall out in a big way.

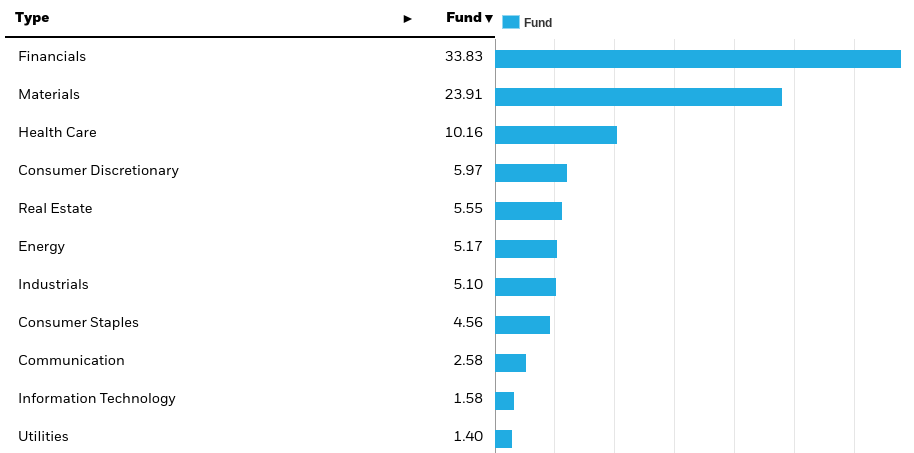

This has positive implications for EWA even though the fund is not directly exposed that heavily to the Australian consumer. While only about 11% of total fund assets are labeled "Consumer Discretionary" or "Consumer Staples", the fund has over 1/3 of its assets in the Financials sector:

{kind=link}

This has plenty of exposure to the health of the Australian consumer as a result. Banks and lenders, including the big 4 banks that predominate this portfolio, will need households to make good on their credit obligations, such as mortgages and car loans. Without a healthy consumer, financial firms will see pressures on their net interest margins and net profits.

However, I don't see this as a major risk in the short term because, as noted above, the Australian consumer is in decent shape. While pressures continue to mount, a full-blown crisis is not an immediate concern. This tells me that returns to equity markets could be positive in the first few quarters of the year.

Opportunity To Draw In Post-China Cash

Another interesting attribute relative to Australia is the opportunity to pick up some of the cash that is currently leaving China. I see this as a reasonable thesis because if investors want Asia-Pacific exposure and are long China, they may want to look at deploying those assets in the same geographical corner of the world. What I mean is, why exit China and go to the US, when other developed markets like Australia (or Japan) are closer to home?

This is not a foregone conclusion by any means, but I do see declining investor confidence in China as a tailwind for equities in other corners of the APAC region. This is a region with impressive growth stories, that is away from the military conflict in Europe and has economies heavily tied to commodities and materials that can perform well during inflationary environments. All of these factors make APAC (which includes Australia) attractive for investors looking to diversify.

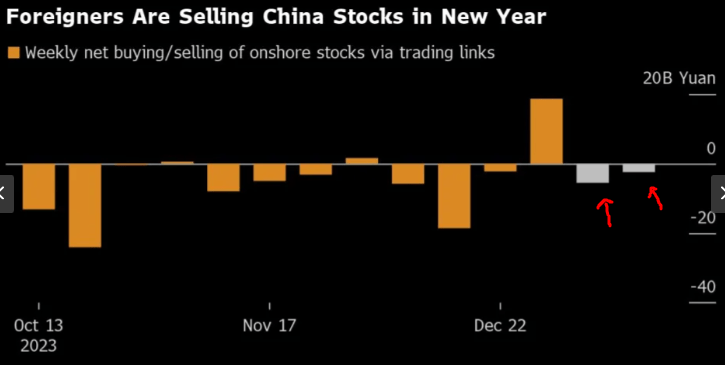

Why does this matter now? Because sentiment continues to be negative on Chinese equities. After a poor showing in 2023, foreign investors started off 2024 reducing their exposure to China's stock market, showing a continuation of a trend from last year:

Foreign Outflows From China (Yahoo Finance)

{kind=link}

What I am taking away from this is that some of this cash could find a home in Australia, among other options. Investors who wanted APAC exposure will probably still want it, even if China is no longer preferable, and that could support a buy thesis for a fund such as EWA.

It's Not Like Australian Equities Are "Oversold"

I have laid out a couple of reasons why I think readers could be served by shifting some assets overseas and selecting Australia as a place to do so. But I want to be careful to manage expectations. Equities across many developed markets are looking at some of the same risks (inflation, high interest rates, geo-political uncertainty), and being cognizant of these risks is critical to proper planning and risk management. Further, I don't want to give the impression that Australian equities are "cheap". While they are relatively attractive, relative is the key word. Australia still saw healthy, double-digit gains in 2023, meaning that investors are buying into a bull market now (as opposed to a deep value opportunity):

2023 Calendar Year Thematic Returns (World Bank)

I bring this up because I think a balanced view is important. Do I believe EWA is a solid "buy" candidate here? Yes, I do. But I am aware of the many articles that come out daily that suggest "buy, buy, buy!!!" or some variety of the same. I don't believe that type of hype is warranted here (if it ever is) so I urge my followers to carefully consider positioning levels for any new purchases as 2024 gets underway. There is plenty to be excited about, but valuations are baking a lot of that in. Knowing your own risk tolerance is important so you don't want to be over-exposed if market sentiment sours.

Business Leaders Are Optimistic

Another reason I'm a buyer of EWA is that the boots-on-the-ground mentality is a positive one. That could signal better times ahead for the Australian economy than some economists are forecasting at present.

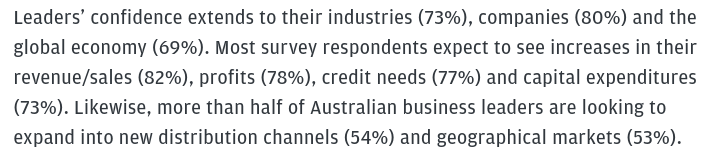

What I am referring to is a recent survey of Australian business leaders by JPMorgan Chase ( JPM ). A quick snap-shot of some of the highlights shows a general sense of optimism regarding their respective industries, the global economy, and the chance to improve profit margins in the year ahead:

Survey Results (Australian Business Leaders) Outlook 2024 (JPMorgan Chase)

{kind=link}

The conclusion I draw here is that those with a sharp sense of potential business activity for the new year are planning for solid performance. They are not predicting a major downturn and are planning to improve margins through sales and by passing on costs to end consumers. That is generally a rosy outlook and strikes me that there is potential for Australian equities if a recession is staved off and executive outlooks come to fruition.

The Banking Story Is Not As Bad As Some Think

As I noted above, EWA is a fund that is very long in the Financials sector. Within Australia, that means a heavy allocation to the "big 4" banking institutions, so one will want to be generally bullish on their prospects before buying this fund. In particular, this is a sector that has seen its share of ups and downs over the past few years. It is heavily regulated, competitive, and doesn't exactly harbor a lot of goodwill among the Aussie public. All of these factors again suggest some level of caution is warranted when buying up these shares.

However, what I want to point out here is that some of the negativity surrounding this sector - both in sentiment and in news headlines - may be a bit overblown. Is the environment challenging? Absolutely. Could net margins take a hit as rates decline and consumer delinquencies rise? Of course. But is this an un-investable backdrop? I don't believe so.

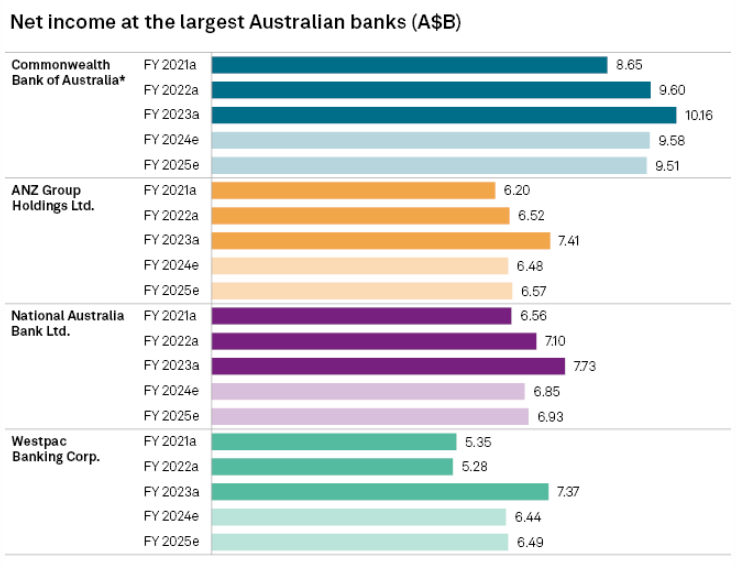

The reason why is that while the largest banks may see a decline in margins this year, overall levels are still very healthy. While the consensus calls for a decline in income in 2024, we can see here that even if those estimates are correct, all of the big 4 will see income levels above 2021 levels:

{kind=link}

What I am getting at here is that while a decline looks inevitable, what should the baseline be? These banks benefited from Covid-related subsidies and higher interest rates for the last couple of years. It is natural now to see a bit of a compression on this front as economies have normalized.

But, looking back further, we see that these banks are still growing income levels above the levels before those subsidies/higher interest rates. The net takeaway for me is that performance is still fairly strong, and there doesn't appear to be a scenario forming where we need to avoid this sector. As a result, I feel comfortable holding EWA in my portfolio.

Bottom-line

EWA has posted modest gains and has been a laggard compared to US-focused options. Rather than be discouraged by this trend, I see it as an opportunity. Australian equities are reasonably priced, could bring in investment dollars previously headed for China, and offer US-based investors a way to diversify from the Mag 7. All of these attributes help support a buy rating in 2024 in my view. Therefore, I am upgrading my outlook, and suggest to my followers they give this idea some consideration at this time.

For further details see:

EWA: I See Some Value 'Down Under' In 2024 (Rating Upgrade)