EWA - EWA: I Was Wrong - Australia Continues To Be An Effective Diversifier (Rating Upgrade)

2023-04-17 06:04:37 ET

Summary

- Australia, and EWA by extension, had long been a permanent fixture in my portfolio that had served me well.

- However, as 2023 got underway, I moved into what I thought were greener pastures. I surmised continued geo-political risks in Asia would trickle "down under".

- In short, I was dead wrong. Australia and EWA both continue to perform well. This makes the country and this ETF a reasonable option for investors looking to diversify outside US borders.

Main Thesis & Background

The purpose of this article is to evaluate the iShares MSCI Australia ETF ( EWA ) as an investment option at its current market price. This fund is managed by BlackRock ( BLK ), and its objective is to "track the investment results of an index composed of Australian equities".

This is an easy way for U.S.-domiciled investors to gain exposure to Australia, and is a fund I owned for a long time. I was bullish on it for most of 2022 and over the past year the fund wound up performing quite well:

Performance since June '22 (Seeking Alpha)

However, as 2023 got underway, I saw better opportunities (so I thought) elsewhere. I decided there were risks brewing in the Asia-Pacific that were going to disproportionately hurt Australia and I was best to avoid that scenario in the new year. Suffice to say, I was completely off the mark with this prediction as EWA has been soaring since that time:

Performance since November '22 (Seeking Alpha)

As my followers know, I am never one to shy away from the calls I get wrong. This was definitely one of them and I thought it was time to give my updated take on my outlook with Q2 underway. Suffice to say, I am hoping to learn from my mistakes here and I believe Australia's resiliency shows it is a reasonable option for those worried about broader market volatility. Therefore, I am upgrading this to "hold", and will explain why below.

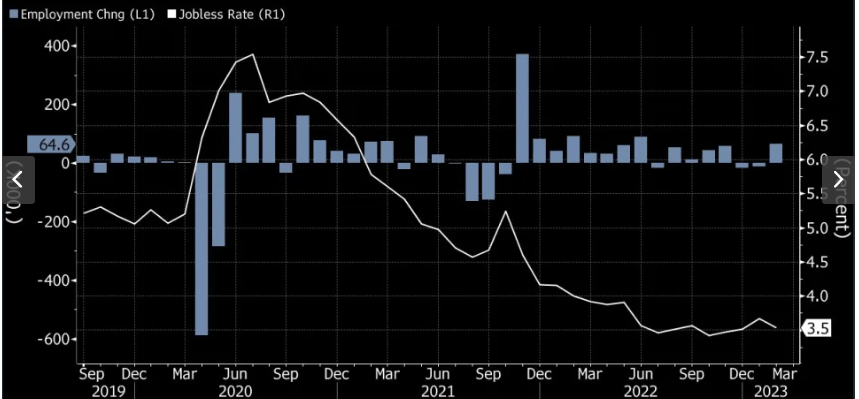

Broad Strength In The Employment Market

Let us start by taking a look at some of the reasons behind EWA's strong performance. In fairness, U.S. equities have done very well over the same time period. My central thesis late last year was that U.S. equities were due for a strong rally and I was shifting assets in to that idea. And I was right about that, with the S&P up almost 10%. Still, EWA performed better. There is no getting around that. Part of the reason for this has been the resiliency in the Australian labor market - similar to what we have seen domestically. There continues to be jobs added most months and the unemployment rate is at historic lows:

Australian Labor Market (Yahoo Finance)

{kind=link}

This is without a doubt a positive sign. Similar to the U.S. it shows that despite all the negative headlines, the economic backdrop continues to be supported by citizens going to work. While we have seen some big layoff announcements in both the U.S. and abroad, the significant labor shortage is simply being evened out. Most job seekers are still able to find employment because the labor market is tight and that supports economic growth and consumer spending. As long as this story remains in place, EWA is supported.

The China Bump

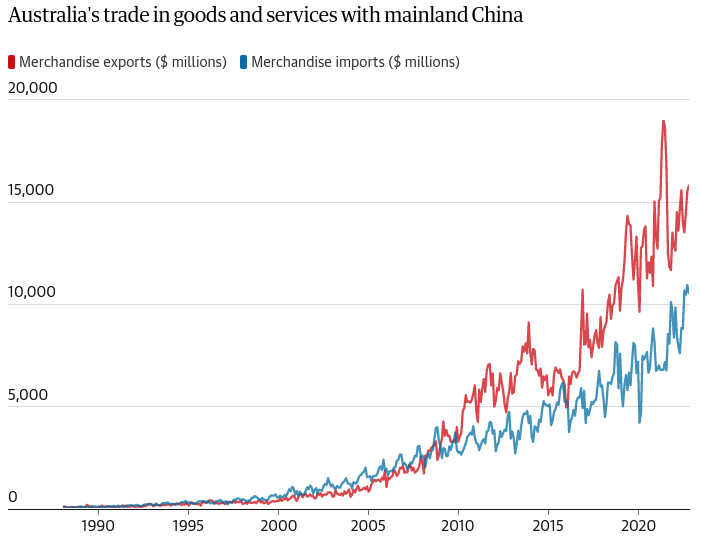

Another reason for my prior concern was the impact of the Chinese economy on Australia. As 2022 was wrapping up I saw instability in China as an issue that would permeate throughout the Asia-Pacific. There have also been signs of a cooling of relations between the two countries. I saw this as having the potential to be exacerbated by the unrest in China and the potential for a conflict with Taiwan. This was a key risk facing EWA because Australia has seen its reliance on China grow steadily over the past decade:

Australia - China Trade Relationship (Australian Bureau of Statistics)

{kind=link}

It should therefore be clear what an important partner China is to Australia. As I saw headwinds mounting, that may be less bullish on EWA by extension.

Fast forward to today and China has actually been a big winner in 2023 in terms of unexpected growth and the future outlook. While the western world - the U.S. and Europe in particular - are facing heightened recession risks, China is anticipated to grow at a relatively faster pace:

Relative GDP Growth Estimates (2023) (IMF)

While this article is about Australia and not China directly, the two are very intertwined as the prior graphic had showed. Therefore, what is good for China bulls often trickles down to being good for Australia as well. That helps explain EWA's out-performance in 2023 thus far.

The central point I am making here is that I saw major headwinds for China going in to the new year and that has completely reversed. China is now a major source of market gains as it is helping drive up oil prices and consumer-driven consumption figures for the global economy. This is helping to counter-balance concerns of recessions elsewhere. As the outlook for China has changed, so too have I adapted my outlook for Australia. This is fundamental to understanding why I believe EWA deserves an upgrade at this time.

Australia Faces Some Similar Headwinds

I have mentioned I under-estimated both China and Australia when 2022 was coming to a close. I also suggested that Australia has been - and therefore could continue to be - an effective hedge for U.S.-oriented investors going forward. However, that is not to suggest this is a risk-free investment. Of note we need to remember EWA has risen by double-digits in the past six months. That, at the very least, proves to things. One, the fund and underlying economy it is exposed to are resilient. Two, investors should exhibit at least a little bit of caution here.

The logic is straightforward. We can't expect such sharp gains to continue forever. I missed the boat on owning Australia so far this year but I am going to stay disciplined and not overly chase returns. Manage the upside as well as the downside when things look too good to be true!

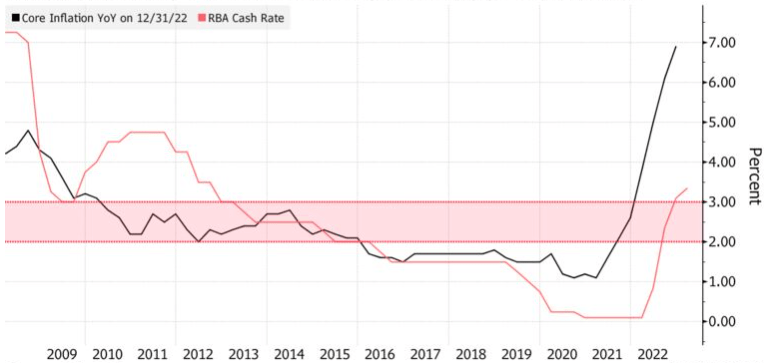

To understand why, let us remember that Australia faces many of the same challenges as the rest of the developed world. This limits the bull case to a degree in the second half of the year. For instance, inflation remains stubbornly high and this has led to the Reserve Bank of Australia (the country's central bank) keeping interest rates at an elevated level too:

Inflation & Central Bank Rate (Bloomberg)

{kind=link}

What I am driving at here is pretty simple. Australia is not immune to the challenges facing the globe. Inflation is a thorn and higher rates will likely persist as a result. This should hopefully help justify why I am not an outright bull at these levels, but rather suggest very selective buying instead. That is where the "hold" rating comes from.

The Materials/Commodity Exposure Cements The Diversification Play

The next thought on EWA leads me to one of the predominant reasons I initially bought the fund many years ago. This has to do with diversification - but that doesn't mean geography. Yes, Australia is far away (from most everywhere) and it means investors can take on developed world exposure without having to buy North American or European companies. But it extends beyond that.

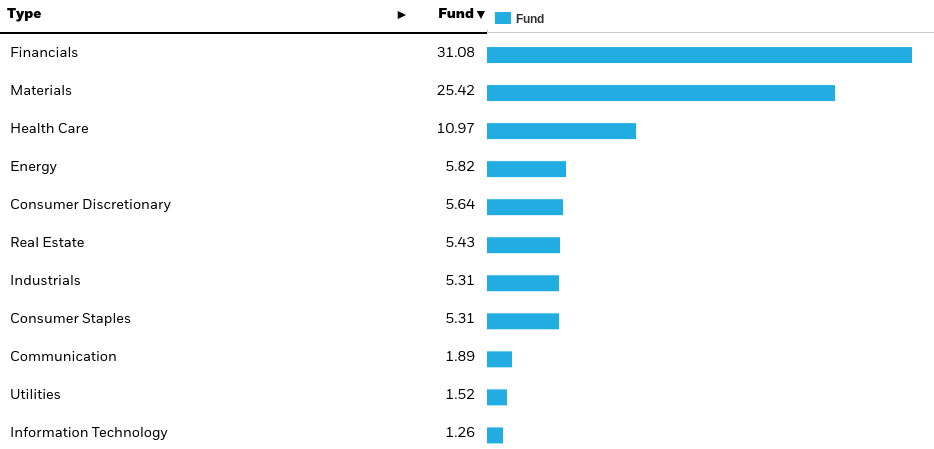

What I am referring to is the country's sector exposure. Unlike the U.S. which is heavy with Tech or Europe which is heavy with Consumer and Financial plays, Australia has a large Materials / Commodities industry. In fact, mining is one of the primary sources of output for the country, as shown below:

Australia's Economic Make-Up (RBA)

This reality is naturally reflected in EWA. While the banking sector continues to be disproportionately important to Australia's economic health, Materials (and mining) are a core component of this ETF. This commodity-oriented area is roughly one-fourth of total fund assets:

EWA's Sector Weightings (iShares)

{kind=link}

I continue to believe readers should own a fair bit of commodity, metals, or materials exposure going forward. This is chiefly due to the elevated inflationary environment and the potential for central banks to begin cutting rates in the year ahead if we do see recessions in America or elsewhere. These sectors act as natural hedges against the dollar and also when supply-chain issues put pressure on producers and suppliers. This is something we have seen for years and while it has let up substantially, it still remains a great challenge for the global economy going forward. Owning the means of production, as miners and material companies do, is a perfect way for investors to protect themselves.

Ultimately, this highlights when EWA is a reasonable option. Investors are getting very different exposure buying this fund if they are like me and are mostly US-centric. This is key to why I buy developed markets like Canada and Ireland as well, since their top holdings are vastly different from the big Tech names we see in the S&P 500. While Australia (and EWA) are by no means the only ways to play this idea we should recognize the nation as a global leader in exploration and production of a host of metals and/or commodities:

Share of Production (By Country) (S&P Global)

It should come as no surprise then that this industry is a leader for overall corporate profits across the country:

Profit Breakdown (Australia) (Australian Bureau of Statistics)

What I takeaway from this is the mining/materials sector is a main source of growing profits across the continent. Without it, Australia's corporate sector would be only modestly growing their profits. Given this backdrop, having all the materials and mining exposure in EWA is a tailwind for now.

Bottom-line

I made a mistake on Australia and have owned up to it. However, while I do see a more favorable backdrop then I did in November, I must reiterate some caution here. The world's problems remain Australia's problems, especially in relation to China. Further, inflation and high interest rates are thorns in the side of growth prospects. Finally, the consistent rise in the share price of EWA suggests a correction could very well occur, so readers need to approach cautiously. Despite all this, Australia has proved resilient, its labor market is strong, and the materials and mining companies that dominate EWA's portfolio are poised to continue to do well in the second half of 2023. Therefore, I believe a rating upgrade on this fund is justified and encourage readers to give this idea some thought at the moment.

For further details see:

EWA: I Was Wrong - Australia Continues To Be An Effective Diversifier (Rating Upgrade)