EWD - EWD: Swedish Economic Data Improved But Look At The Price

2023-06-02 21:42:01 ET

Summary

- Swedish economic data points have improved in Q1.

- But a closer look suggests that some caution is still warranted.

- The iShares MSCI Sweden ETF remains too pricey for my liking.

Recent data points out of Sweden point to some of its major economic woes finally rolling over. Q1 growth surprised to the upside at +0.8% QoQ (vs. a -0.5% QoQ decline in Q4 2022 and the Riksbank forecast +0.3% QoQ), while CPIF-XE (i.e., consumer inflation excluding energy) also came in 20bps below Riksbank expectations at +8.4% YoY in April amid cooling goods inflation. Yet, services ex-housing inflation has been sticky, and that may mean a longer-than-expected Riksbank hiking cycle (post another 25bps hike in June). With the property market also nearing distressed levels (see SBB’s downgrade to junk and dividend suspension last month), the Swedish economy isn’t out of the woods yet. Nor does the equity market screen cheaply on a standalone basis, with the iShares MSCI Sweden ETF ( EWD ) at 16.8x P/E (or 2.0x P/Book). So while the positive growth signals this month indicate Sweden might be nearing an inflection point, I would remain sidelined on EWD ETF (in line with my prior neutral stance ) pending a meaningful pullback.

Fund Overview - Low-Cost, Industrials-Heavy Swedish Portfolio

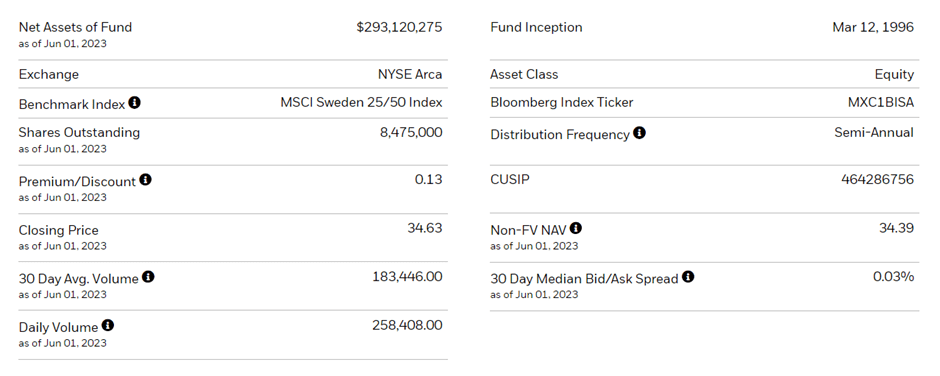

The US-listed iShares MSCI Sweden ETF tracks the performance of the MSCI Sweden 25/50 Index (pre-expenses), an index comprising large and mid-cap Swedish equities (~85% of the free float-adjusted market cap). The ETF has seen its net asset base grow in recent months, reaching ~$293m at the time of writing (up from ~$249m net assets prior). At a 0.5% expense ratio (unchanged), the ETF remains a cost-effective option for US investors looking to express a single-country view on Swedish equities. A summary of key facts about the ETF is listed in the graphic below:

{kind=link}

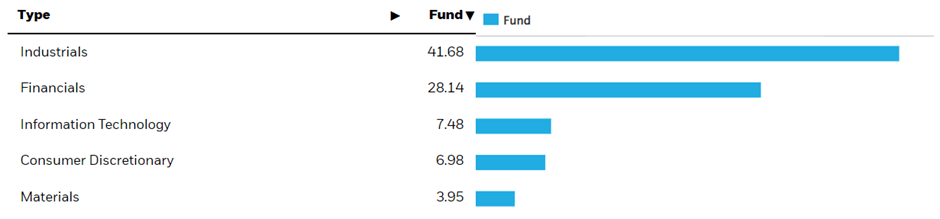

The fund has added one more holding and is now spread out across 46 individual names, with the Industrials sector gaining an even larger portfolio allocation at 41.7% (up from 39.3% prior). Financials remain the second largest weightage, though the current 28.1% is slightly down in recent months. Other key sector allocations include Information Technology (7.5%), Consumer Discretionary (7.0%), and Materials (4.0%). On a cumulative basis, the contribution of the top five sectors has increased to ~89% of the total portfolio, with the top two (Industrials and Financials) contributing an even larger share at 70.0% (up ~1.4 %pt).

{kind=link}

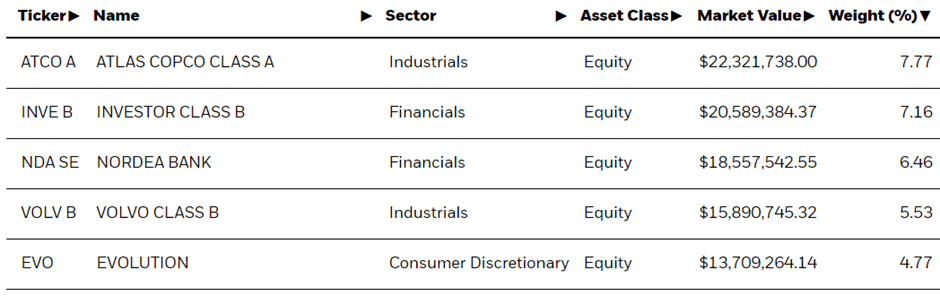

In contrast with the high fund concentration from a sector perspective, the single-stock allocation is more balanced, with the top five holdings accounting for ~32% of the overall portfolio. The portfolio composition has changed since I last covered EWD, with the top holding now Swedish industrial tools and equipment manufacturer Atlas Copco ( ATLKY ) at 7.8%, following a huge rally over the last month. After a similarly strong performance in April/May, Swedish conglomerate holding company Investor AB ( IVSXF ) is now the second-largest holding at 7.2%, replacing Nordea Bank ( NRDBY ) at 6.5%. Volvo Cars ( VOLVF ) remains in the fourth spot at 5.5% (unchanged), while door access solutions leader ASSA ABLOY ( ASAZY ) has been replaced by gaming company Evolution AB ( EVVTY ) at 4.8%.

{kind=link}

Fund Performance – Near-Term Blip in the Long-Term Compounding Story

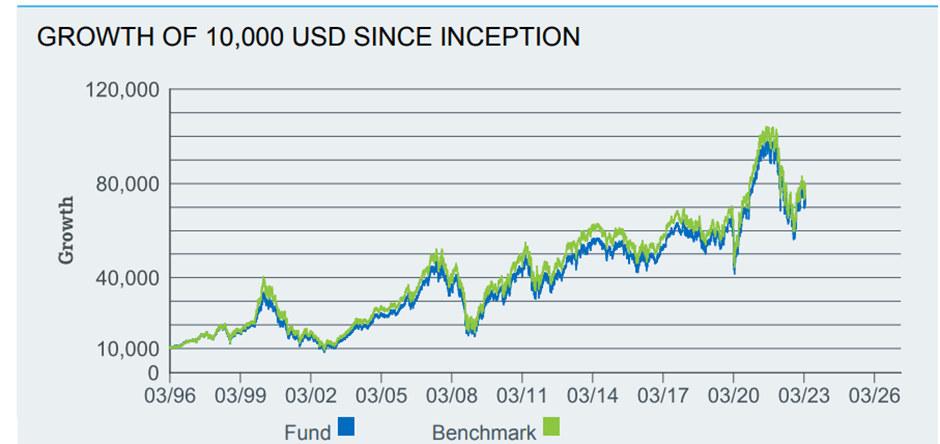

On a YTD basis, the ETF has risen by 5.9% and has compounded at an impressive 7.8% rate in market price and NAV terms since its inception in 1996. Last year’s double-digit % drawdown was a rare blemish on the fund’s track record following three consecutive years of double-digit growth (+22.0% in 2021, +23.3% in 2020, and 22.1% in 2019). The annualized three, five, and ten-year returns are also strong at 15.0%, 5.3%, and 4.7%, respectively. While the steady earnings growth in EWD’s portfolio holdings has been a key contributor, valuation expansion has played a role as well – the P/E and P/B ratios now stand at 16.8x and 2.0x, respectively.

{kind=link}

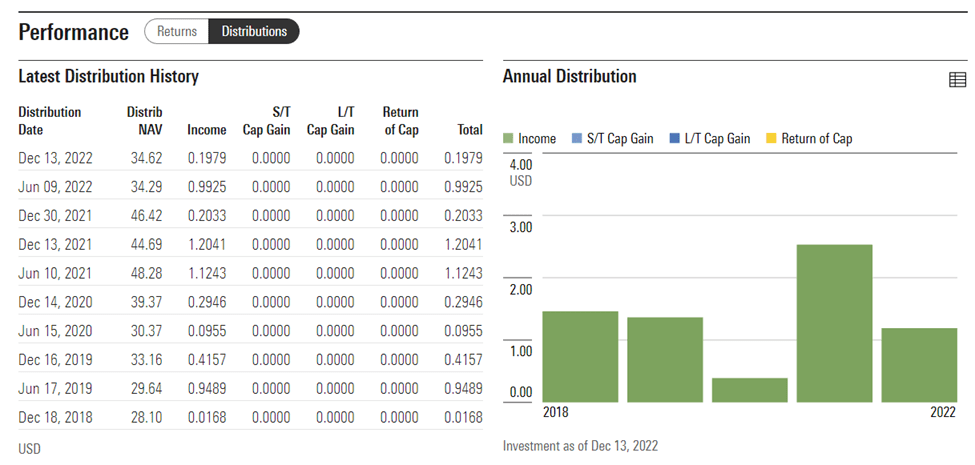

The trailing twelve-month yield screens attractively at 3.2%, but distribution has been historically volatile, in line with the cyclicality of an industrials-heavy portfolio. With payouts moving lower (in line with earnings) in 2022 and this year also likely to be a challenging one given the higher rate/lower growth backdrop, the distribution could trend lower near-term (note the lower thirty-day yield of 1.9%). And at an equity beta of 1.2 vs. the S&P 500 (SPY), defensive investors may want to exercise caution.

{kind=link}

Puts and Takes from the Positive Q1 Growth Surprise and Consumer Inflation Print

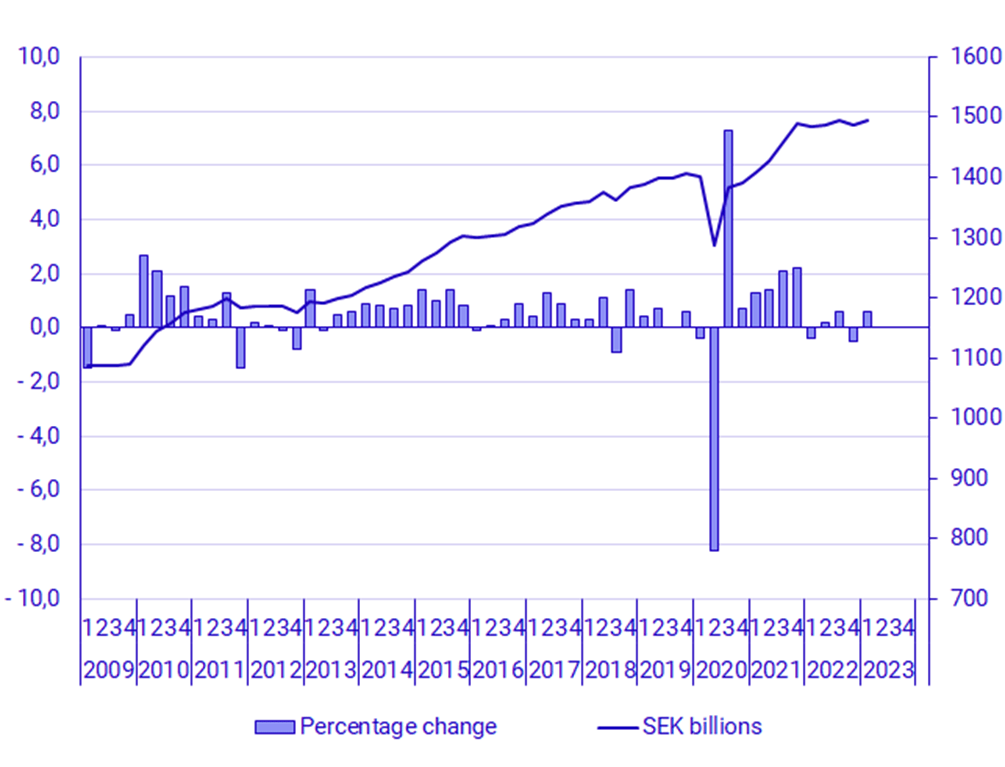

The biggest surprise out of the Swedish economy over the last month was the Q1 GDP print , which came in at an accelerated +0.8% sequentially (vs. a 0.5% QoQ decline in Q4 2022), well above the Riksbank forecast of +0.3% QoQ. Digging deeper, however, it appears that the headline number was propped up by a 0.6%pt contribution from inventories, indicating some pull-forward demand which could normalize in future quarters. Elsewhere, private consumption was down by 1.2% QoQ, suggesting underlying domestic demand weakness. The good news was the increased net export contribution at 0.3%pts to growth, likely helped by continued SEK weakness. But with the labor market still tight (employment and hours worked were also sequentially higher in Q1) and the Riksbank maintaining a hawkish stance, I would question the sustainability of this FX tailwind.

{kind=link}

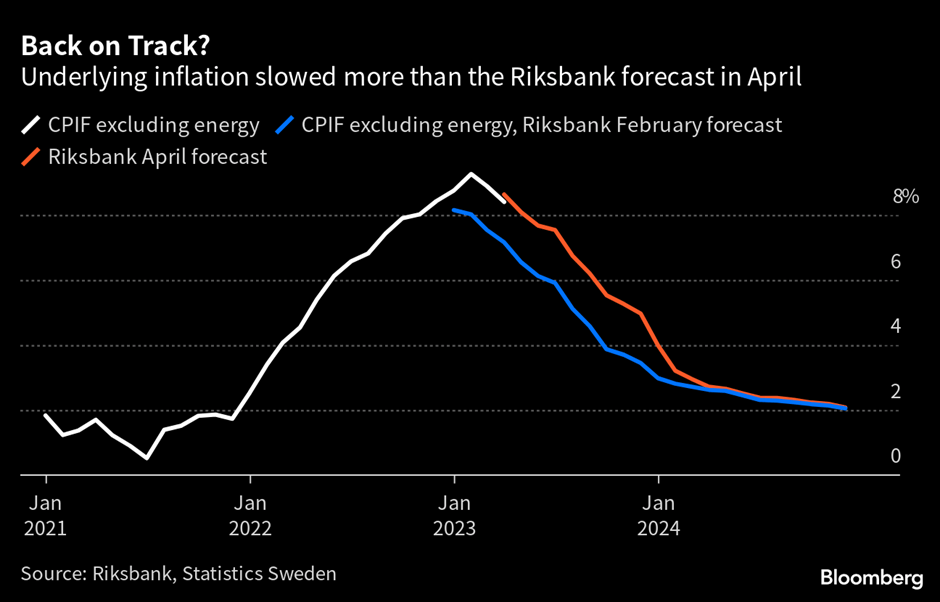

The decelerating headline inflation was another key data point that seemed positive at face value, with CPIF excluding energy decelerating to +0.4% MoM (+8.4% YoY). But beneath the hood, most of the slowdown was attributable to easing goods inflation (flat MoM in April) vs. services ex-housing, which accelerated to +1.0% MoM. Having kept its rate path unchanged at the last policy meeting , stickier core inflation and a relatively resilient Swedish economy could push the Riksbank into a surprise hike beyond June (another 25bps penciled in). All eyes will thus be on the May inflation reading – further evidence of rising core inflation could mean an extended tightening cycle (and vice versa), which would, in turn, weigh on the already fragile property market.

{kind=link}

Conclusion

With Sweden’s latest GDP print accelerating well ahead of expectations at +0.8% QoQ in Q1 (reversing last quarter’s 0.5% QoQ decline), a much-feared recession scenario may now be off the table for the country. But inflation remains an issue – while headline consumer inflation decelerated in April, services ex-housing (i.e., ‘core inflation’) has accelerated, and that could push the Riksbank into an extended tightening cycle. A ‘higher for longer’ rate environment means the troubled property sector, perhaps the biggest overhang on the Swedish economy, is unlikely to get a reprieve anytime soon. Swedish equities don’t screen cheaply either, with EWD at ~17x P/E – a wide premium to the Euro area. Even after accounting for the low-teens earnings growth algorithm (post this month’s big EPS revision) and the quality of EWD’s portfolio of Swedish champions, I don’t see compelling value in the ETF here.

For further details see:

EWD: Swedish Economic Data Improved, But Look At The Price