FLHK - EWH: Hong Kong Is A Contrarian Play Ahead Of Rate Cuts

2024-01-13 21:05:47 ET

Summary

- After another big drawdown in 2023, Hong Kong equities have largely been written off by investors.

- But with the country about to import a big Fed easing cycle, this is a market that could surprise many this year.

- As the largest and most liquid vehicle, EWH remains a great way to express a single-country contrarian view on Hong Kong.

2023 was one of the worst years on record for Hong Kong equities, as a steep H2 drawdown led to the third straight year of losses for iShares MSCI Hong Kong ETF (EWH). With 2024 also starting off poorly, the Hong Kong equity benchmark is now back to price levels last seen at its COVID trough – in contrast with an economy that has seen growth rather than contraction during the period.

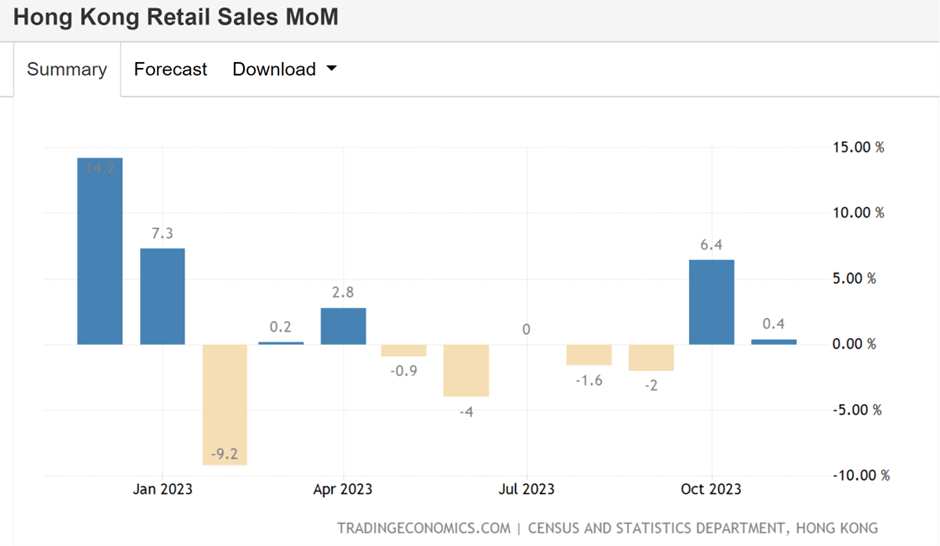

The key issue is contagion from China, a country that Hong Kong is increasingly joined at the hip with ("one country, two systems") and where a worrying slowdown is taking hold. Re-opening has also served as a catalyst for Hong Kong consumers to migrate their spending to cheaper shopping areas in China – likely a key reason for the protracted department store/consumer good-led decline in retail sales in recent months.

{kind=link}

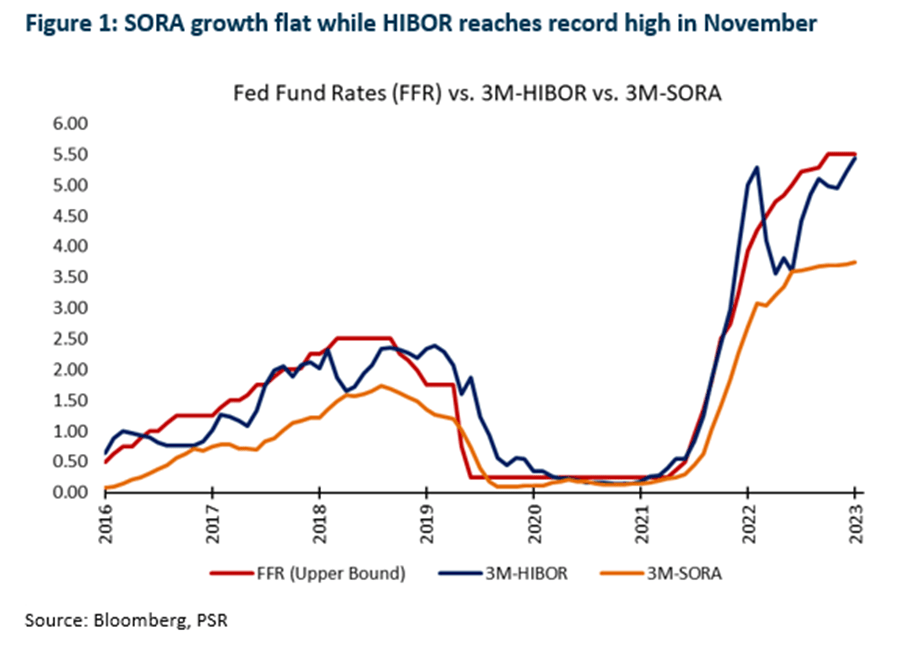

But there are important differences with Hong Kong, as I highlighted in my prior EWH coverage , most notably its peg to the US Dollar and relatively open capital flows. Thus far, the dollar peg has been more bane than boon, as imported monetary tightening culminated in local interbank rates reaching a multi-decade high . This has, in turn, led to Hong Kong's economy taking an inopportune hit; nowhere has this been felt more than the rate-sensitive property sector, a key part of the EWH portfolio.

{kind=link}

The question now is whether we've reached peak pessimism – particularly now that the Fed has committed to a policy pivot. As an easing cycle will also be imported by Hong Kong via its peg, essentially unraveling the damage from the last set of hikes, EWH would make sense as a 'high beta' play on US rate cuts. Current price levels indicate emerging value as well, given that financials/property-heavy EWH is now priced at ~11x forward earnings (vs. low-teens % growth in 2024 and ~10% in 2025). For the contrarians out there willing to look past the China risks, EWH is worth a look as a tactical play into 2024, in my view.

iShares MSCI Hong Kong ETF Overview – The Largest and Most Liquid Single-Country Play

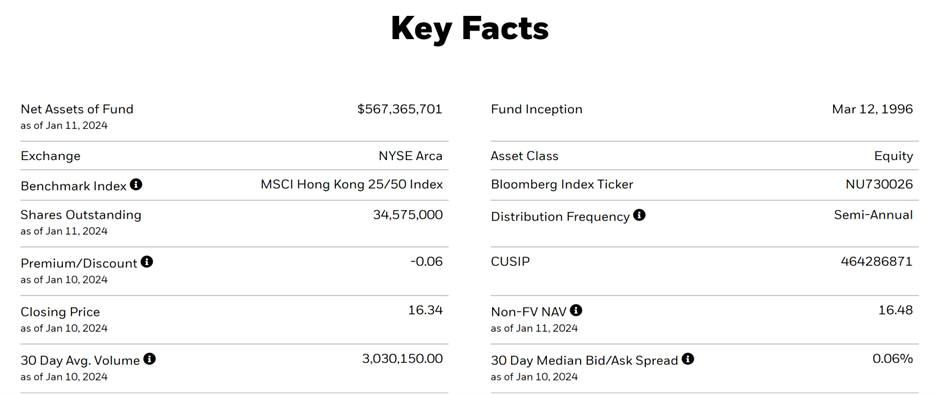

The iShares MSCI Hong Kong ETF, still the only listed MSCI Hong Kong tracker (subject to weightage caps) listed in the US, now manages $567m of assets – down from last quarter amid broader equity market underperformance. The fund still charges a 0.5% expense ratio, which makes it the more expensive of the two passive Hong Kong options – by comparison, Franklin Templeton's FTSE Hong Kong ETF ( FLHK ) charges ~0.1%. Yet, EWH is far more established and liquid; as a result, its significantly narrower bid/ask spread (6bps vs >60bps for FLHK) cancels out the fee premium.

{kind=link}

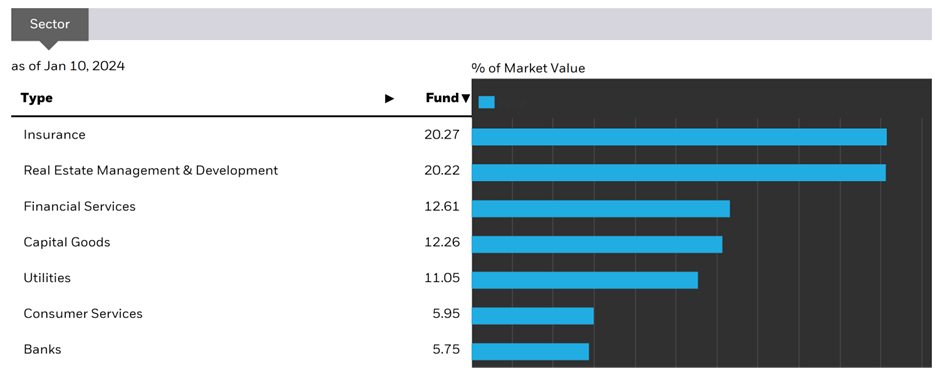

Mirroring the Hong Kong economy, the EWH sector allocation leans heavily on two sectors – financials and real estate. More specifically, insurance (lower at 20.3%) and real estate management & development (higher at 20.2%) are the two largest listed sector weights, respectively. Including financial services (12.6%), banks (5.8%), and real estate (4.4%), the aggregate financials and real estate allocation is down from last quarter but remains very high at a cumulative ~63%. Key comparable FLHK has a slightly lower financials/real estate concentration due to its more rigid weightage caps, though at a cumulative ~57%, it is fairly top-heavy from a sector standpoint as well.

{kind=link}

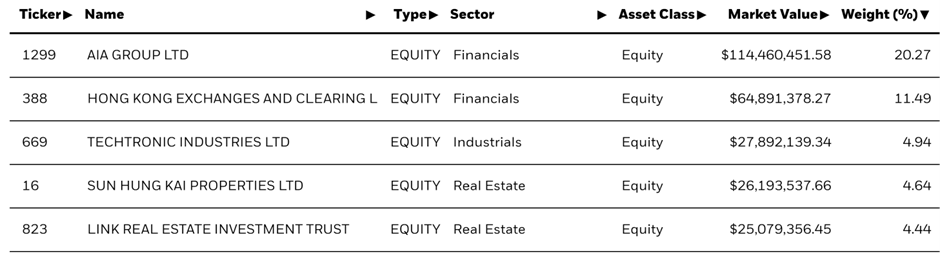

Insurer AIA Group ( AAGIY ) continues to lead a broader 34-stock EWH portfolio, albeit at a much reduced 20.3%. Exchange and clearing house operator Hong Kong Exchanges and Clearing Limited ( HKXCY ) is also lower at 11.5%, while power equipment manufacturer Techtronic Industries ( TTNDY ) gains further portfolio share at 4.9%. Property developer Sun Hung Kai Properties ( SUHJY ) and Link Real Estate Investment Trust ( LKREF ) are new entrants in the top five at 4.6% and 4.4%, respectively, displacing conglomerate CK Hutchison (CKHUY). FLHK offers a similar portfolio composition, though, like their sector breakdown comparisons, EWH has a higher single-stock concentration.

{kind=link}

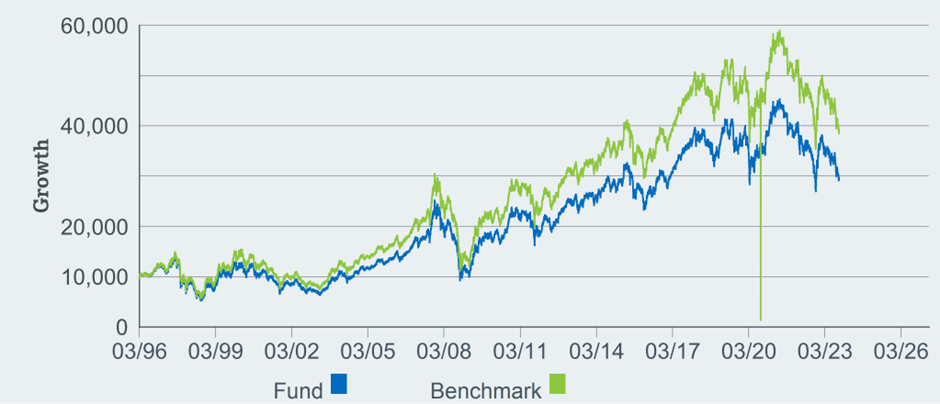

iShares MSCI Hong Kong ETF Performance – Marred by Consecutive Years of Underperformance

EWH saw another steep decline in Q4, as the one-two punch of a slowing Greater China economy and elevated rates (imported via the HKD's peg) led to a low teens % decline for the year. With 2024 to date seeing more declines (-5.9% at the time of writing), the fund's track record since inception now stands at +4.1% annualized. Over the last five and ten years, however, EWH has returned a lackluster -2.3% and +1.5% annualized, offsetting much of the gains seen in the fund's early years. The more diversified FLHK has been slightly more resilient (-11.9% NAV return in 2023), though its shorter track record limits comparisons beyond a five-year lookback.

{kind=link}

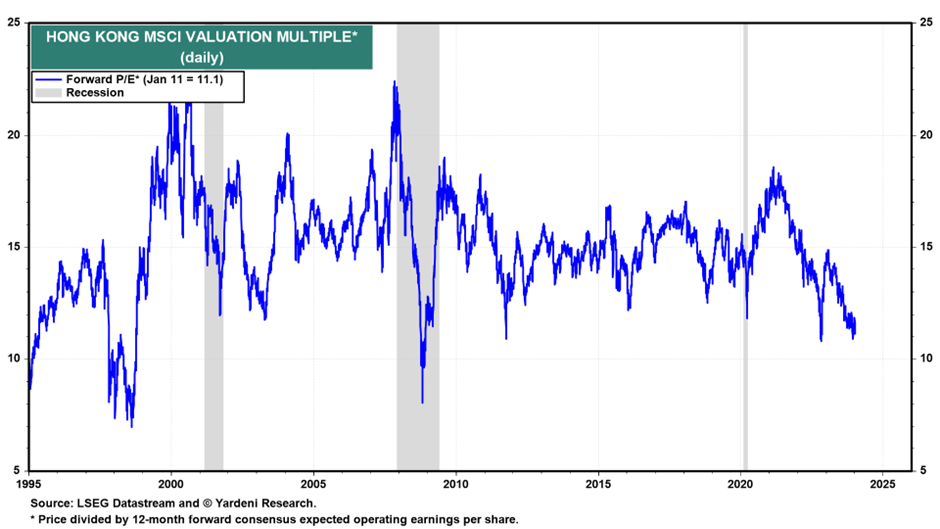

While some of EWH's drawdown has come out of earnings, the lower forward earnings multiple at ~11x (~15x trailing P/E) indicates there's been some de-rating as well. Similarly, the fund's book value discount has also widened slightly, as the market priced in more downward earnings revisions ahead of Q4 2023 reporting.

{kind=link}

The Fed's pivot toward year-end, however, has had a notable effect - after some very steep earnings resets in October, the pace of negative revisions has now begun to moderate. 2025 consensus estimates are also on the mend, with earnings growth now at +12% and +10% for 2024 and 2025, respectively. This should, in turn, bode well for the solid >4% yield, which tracks the portfolio's underlying earnings growth over time.

A Contrarian Play Ahead of Rate Cuts

Hong Kong hasn't been a great place to be in recent years, as EWH's performance shows. That said, there is a price for everything, and I wonder if Hong Kong stocks are close to bottoming out now that the MSCI benchmark is back to levels last seen in the midst of pandemic lockdowns. Valuations are also undemanding at ~11x forward earnings - particularly when you factor in improved forward 2025 consensus earnings growth estimates, and that the economy is about to import a big Fed easing cycle (three cuts per the 'dot plot').

To be clear, there are still plenty of risks investors have to underwrite, including the country's ties to a deteriorating mainland Chinese economy that consensus now deems 'un-investable.' A lot of these risks are likely well-understood, though, and the lack of optimism priced into Hong Kong stocks means it may be a prime contrarian candidate to play a Fed pivot.

For further details see:

EWH: Hong Kong Is A Contrarian Play Ahead Of Rate Cuts