EWL - EWL: Swiss Equities Are Undervalued But Nominal Returns Are Unexciting

2023-05-21 03:14:38 ET

Summary

- EWL invests in Swiss equities.

- The fund is likely undervalued, with a theoretical uplift of +30% being possible on valuation alone.

- However, I think that the more likely outcome is a steady '8% plus' average return over the next few years.

- Swiss equities offer good value, but I would prefer to explore opportunities with higher nominal return potential.

Introduction

iShares MSCI Switzerland ETF (EWL) is an exchange-traded fund that provides investors with exposure to Swiss equities. My previous coverage on EWL was published at the end of January 2023 , at which point I was bullish on EWL. Since then, the fund has risen by +6.63% vs. the S&P 500's change of +2.83% per Seeking Alpha data.

However, while EWL has out-performed recently, I think it is worth revisiting the fund. I am more recently placing more confidence in funds with higher nominal returns rather than simply "absolute value". While I thought EWL was undervalued on the basis of low local risk-free rates and an elevated risk-adjusted equity risk premium, my previous forecast suggested a nominal IRR of less than 8% per annum. As the composition of the portfolio and earnings growth estimates will have changed since then, it makes sense to revisit the valuation. In any event, having reviewed many ETFs recently with potential returns of over 10% per annum, this would be a minimum hurdle for me to take any interest in EWL (regardless of local interest rates).

Fund Overview

Before delving into financial information and building a valuation, it makes sense to review the basics. EWL is a fund provided by iShares, who are not known to be especially cheap. I like their funds, but it is important to account for the expense ratio, which is reported as being 0.50%. For a fund offering lower nominal returns, expense ratios become disproportionately expensive. I will include the expense ratio in my calculations.

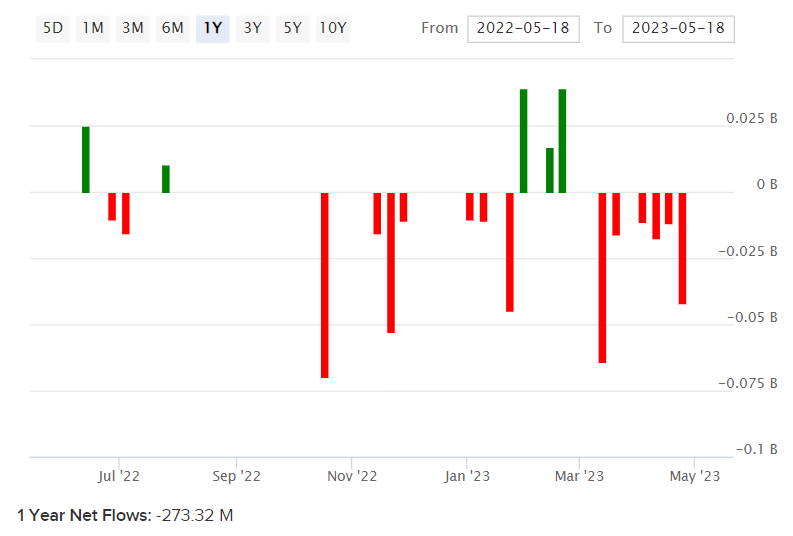

EWL managed $1.26 billion as of May 19, 2023, which is evidence of some material degree of interest in Swiss equities. It is however worth noting that the fund has seen net outflows over the past twelve months of circa -$273 million, as depicted below.

{kind=link}

So, EWL has strangely out-performed while U.S. investor interest (that is, net fund flows into EWL) appearing to wane. It is possible this will lead to forward under-performance, but that has not quite materialized yet.

Return Profile

EWL invests solely in Swiss equities, which is worth noting from a risk perspective. The current 10-year for Switzerland is 1.05% at the time of writing, while Professor Damodaran suggests a zero country risk premium for Switzerland, owing to its higher economic complexity, maturity, and characteristic political stability.

The fund follows the MSCI Switzerland 25/50 Index as its benchmark, however this index does not provide useful financial data in its factsheet. The uncapped version does, so I will use that information as a basis. However, I will also refer to Morningstar's data as a side reference. The uncapped index's trailing and forward price/earnings ratios were 21.63x and 17.49x, respectively, as of April 28, 2023. The price/book ratio was 3.23x. Meanwhile, Morningstar reports a forward price/earnings ratio of 17.75x as of May 16, 2023 (the price of EWL has not changed materially over this time frame between April and May 16). So, the two data sources seem to marry fairly well, and therefore I will proceed with the uncapped index as a proxy for EWL's portfolio.

Bear in mind the uncapped index's reported dividend yield was indicatively 2.95%, which implicitly suggests a high distribution rate of earnings into dividends of over 60%. This is characteristic of mature portfolios. Morningstar provide the chart below which reveals a high exposure to defensive stocks (24% consumer defensive, plus 34% health care). Morningstar also expect three- to five-year earnings growth to average just under 8%.

Morningstar.com

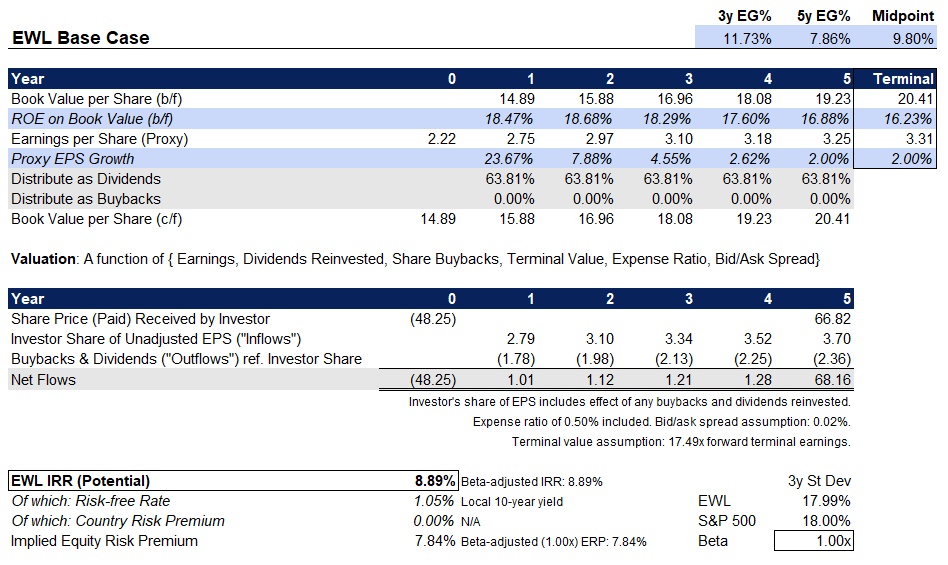

The implied forward return on equity from the above numbers is about 18.5%, which is strong. If we assume earnings growth does indeed drop to an average of about 8% (my midpoint is slightly higher, at 9.8%, because I want to set a floor of at least 2% earnings growth in future years), EWL offers a hypothetical 8.89% five-year IRR as depicted below.

{kind=link}

This forecast is similar to my previous forecast, albeit slightly less arbitrary, using a geometric average (with my 2% earnings growth floor) to estimate forward earnings growth. I am being slightly more optimistic on the tail end for return on equity. If I drop the minimum earnings growth to just 0%, the IRR falls a little to 8.39%. In any event, you have a similar IRR base case as before on a five-year forward basis, which is actually not surprising given EWL's fundamentally mature and low-beta portfolio. (As shown in the bottom-right of the chart above, the three-year standard deviation matches the S&P 500's remarkably closely, for an implied 1x beta.) The correlation between EWL is also about 0.88x over three years.

One could argue, as I did before, that EWL is therefore fundamentally undervalued: if you add a fair equity risk premium of say 5.5% to the local 10-year of 1.05%, you get an implied hurdle rate of 6.55%. Given that EWL is offering 8-9%, you could argue that EWL offers upside on valuation alone of around +30%. However, I think markets are basically pricing in a slightly higher premium into Swiss equities because they're (for want of a better word) "unexciting". You could call this phenomenon the "boring risk premium": high quality but lower return stocks get priced lower such that the underlying return profile becomes more competitive. This is sort of analogous to how more difficult or uncomfortable jobs are paid well; it is a function of supply and demand. So, while EWL is fundamentally undervalued, I think an IRR of about 8-9% on a steady basis is more likely than a sudden uplift on valuation alone.

EWL should perform reasonably well over the medium term, as a result. I do however want to place more weight on higher nominal returns. Therefore, while Swiss equities offer good value, I would prefer to take a neutral stance. It would appear that you can achieve higher nominal returns without taking on much more "beta" by investing in the United States or even other areas in Europe at this juncture, as opposed to investing in EWL's stable, mature portfolio of stocks with lower return potential.

For further details see:

EWL: Swiss Equities Are Undervalued But Nominal Returns Are Unexciting