EWL - EWL: Swiss Equities Offer Healthy Long-Term Returns In 2023

Summary

- iShares MSCI Switzerland Capped ETF invests in Swiss equities.

- The exchange-traded fund EWL is likely undervalued, based on low local risk-free rates and equity risk premia.

- However, the headline IRR potential is not especially exciting in absolute terms.

- I think EWL is an interesting place to park some of one's equity portfolio. Large returns are unlikely, but the risk/reward is sound.

iShares MSCI Switzerland Capped ETF ( EWL ) is an exchange-traded fund that provides investors with exposure to Swiss equities. I last covered EWL at the start of 2022 , from which point I believed the fund was well-positioned. Since then, on a price-only basis, EWL has fallen by -15.09% against the S&P 500 Index's (SP500) move of -16.38% (excluding the effects of dividends in both cases). Last year was bad for investing all round, and unfortunately EWL did not show material out-performance relative to the S&P 500 either.

It is perhaps time to revisit EWL. Earnings expectations will have changed, and further I believe that we are in a bottoming process in equity markets; into the next business cycle, with markets typically leading by 12 months (and sometimes longer), it is likely that now is going to be a good time to be investing over a multi-year time frame. Switzerland is one unique alternative to U.S. markets; it is conventionally viewed as a politically stable safe haven, while the country itself is well developed and ranks highly on a measure of economic complexity (ranking 2nd out of 127 countries in 2020).

iShares MSCI Switzerland Capped ETF is a fund managed by iShares, with an expense ratio of 0.50% and net assets under management of $1.29 billion. That makes the fund relatively popular for a single-country fund, which would lead me to believe that it is viewed as a hedge, by many investors, against U.S. equity markets. EWL is a de facto short-USD fund too, in addition to taking Swiss equity risk, as the underlying holdings are locally denominated in Swiss francs (unhedged). There are only 43 holdings, bear in mind, as the Swiss equity market is not as developed as other markets such as the United States.

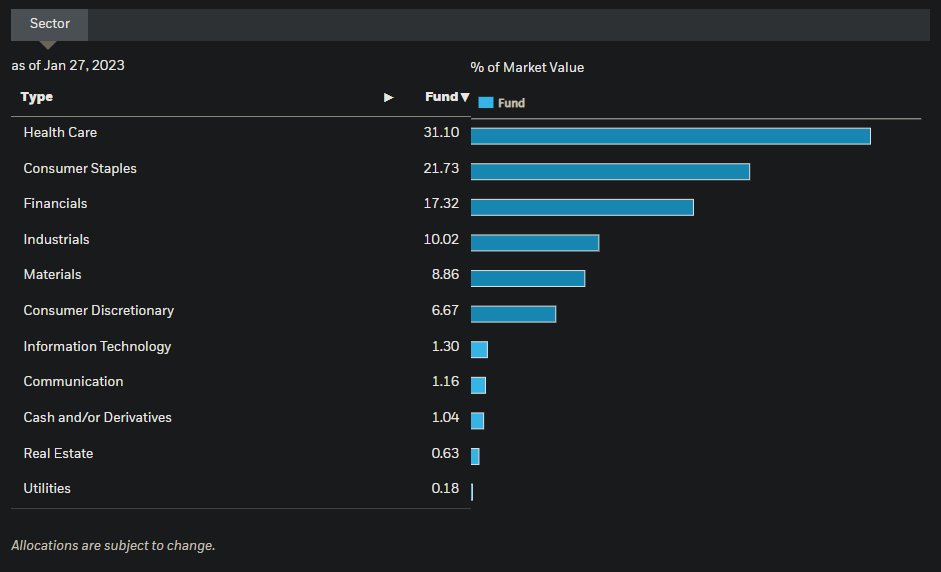

Key sector exposures include health care (31.10%), staples (21.73%), financials (17.32%), and industrials (10.02%).

{kind=link}

The largest holdings include Nestle S.A. ( NSRGY ) at 19.18% as of January 27, 2023, Roche Holding AG ( RHHBY ) at 12.34%, and Novartis AG ( NVS ) at 10.48%. It is worth keeping in mind that concentration risk. However, given the tendency for market-cap weighted Swiss equity portfolios to gravitate toward a high level of concentration in single names, EWL prudently seeks to track its capped performance benchmark, the MSCI Switzerland 25/50 Index. This limits the largest position to 25%, and the sum of 5% or greater positions to 50% in aggregate.

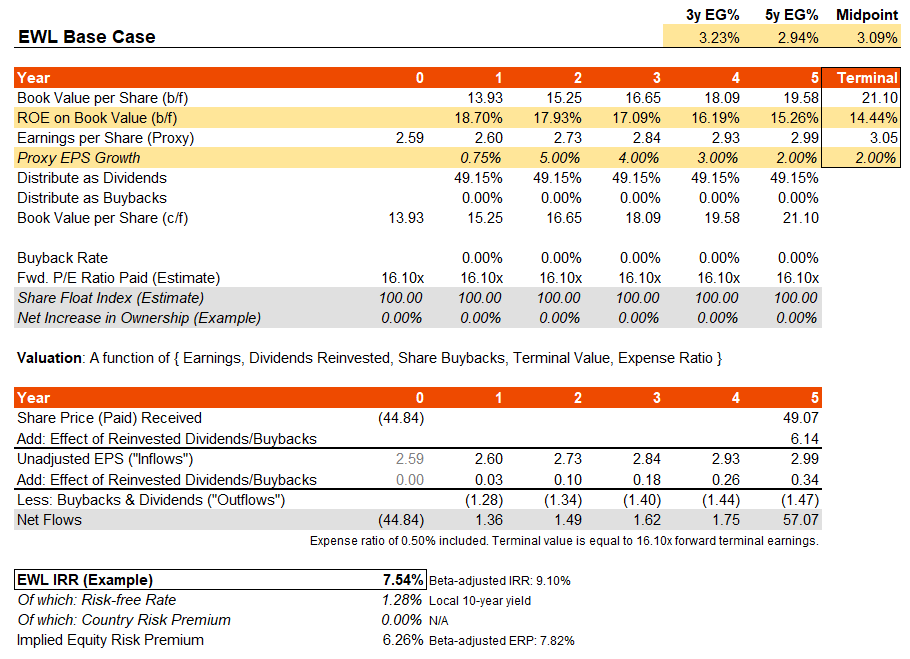

However, in this case, the weightings are very similar to the uncapped version, and hence we can use the uncapped version's recent factsheet from MSCI as of December 30, 2022 as a guide (as it contains financial data we can use). I will revisit an alternative data sources later to ensure the figures are not unduly favorable. The factsheet reveals trailing and forward price/earnings ratios of 16.22x and 16.10x, respectively, with a price/book ratio of 3.01x. The trailing dividend yield was 3.03%.

Morningstar report a lower forward price/earnings ratio of 15.86x even after a recent jump in iShares MSCI Switzerland Capped ETF at the start of 2023. If anything, it is likely our uncapped index-driven forward price/earnings ratio is conservative. Interestingly, our ratios from MSCI suggest forward one-year earnings growth of only 0.75%, which is going to be based on a downturn in earnings growth, as Morningstar's three- to five-year earnings growth estimate for EWL is 5.31%. I am going to assume a lesser average of about 3%, with a jump in year two (hopefully into the next business cycle), and then slowing growth thereafter down to 2%.

One thing I have noticed about mature markets is that, while they might be conservative, their lower long-term earnings growth potential can drive higher equity risk premiums. So, while Switzerland might be considered a safe place to invest, it is not an exciting place to invest. A long-term equity risk premium of 5.50% is, therefore, fair to assume. Assuming the 10-year holds constant (possibly a conservative assumption?), and even zero long-term growth, a fair forward price/earnings multiple might be 16.67x (the inverse of the sum of the ERP and risk-free rate, minus 0% growth). The current multiple is 16.10x (based on the uncapped MSCI index, at least). I will not assume earnings multiple expansion, but I'd say it is possible, which would be another source of potential return.

All considered, and based on these basic and arguably conservative assumptions, the long-term IRR potential of the fund (over the next five years) is 7.54% by my calculations.

{kind=link}

Funnily enough, this 7.5% IRR would suggest undervaluation. Even though the headline IRR is low, the fair value IRR in such a low-rate country that seems almost as if it has been designed for risk-averse investors (perhaps bar the concentration risk) is lower. I would argue an IRR of 5.5-7.0% would be fair. I estimate upside potential on valuation alone of 10-30% or so. Still, we will ignore that earnings multiple expansion as noted earlier. The headline IRR is not high, either (not in absolute terms). For pro-risk investors, EWL is not especially exciting, even if it offers a nice 7.5% per annum opportunity.

I should remind you that my earnings expectations are sub-consensus, and there is further opportunity for share buybacks and so on. Squeezing the model in various places, even within the bounds of reason, might find you another 1-2% of headline IRR potential, but I prefer to err on the side of caution, as always.

Meanwhile, the most recent Big Mac Index (GDP-per-capita adjusted PPP model by The Economist) suggests the Swiss franc is trading at a 37% premium (over-valued). Interest rates remain low in Switzerland, offering negative carry-trade potential (i.e., the franc does not look attractive to hold, except perhaps for the political risk associated with Europe as ever, and most recently the Russo-Ukrainian War). Having said that, the Swiss current account in nominal terms has expanded recently, only not in GDP-scaled terms.

TradingEconomics.com

All considered, the Swiss franc picture is mixed. I would be tempted to suggest the franc offers more downside risk than upside risk, but the U.S. current account has worsened considerably in recent times. So, it is more than possible that the Swiss franc will appreciate, especially if risk-taking activity picks up. Generally speaking, the market cycle and trading activity drives FX prices more than economic fundamentals. Therefore, my bias is on a bullish franc in the medium term, on balance, but my conviction is limited.

All considered, I would take a cautiously bullish stance on iShares MSCI Switzerland Capped ETF. The headline IRR is not super-exciting, but the franc is probably modestly undervalued on a holistic basis, and the EWL portfolio is undervalued on a local basis. iShares MSCI Switzerland Capped ETF seems like a relatively safe place to park some small portion of one's portfolio in.

For further details see:

EWL: Swiss Equities Offer Healthy Long-Term Returns In 2023