EWM - EWM: A Cheaply Priced Emerging Market Growth Play

Summary

- The iShares MSCI Malaysia ETF offers investors low-cost exposure to Malaysian equities, albeit through a concentrated investment vehicle.

- As the ETF retains an outsized exposure to the major banks, it should track the broader economic performance well.

- With valuations also below its regional peers, the ETF is worth a look.

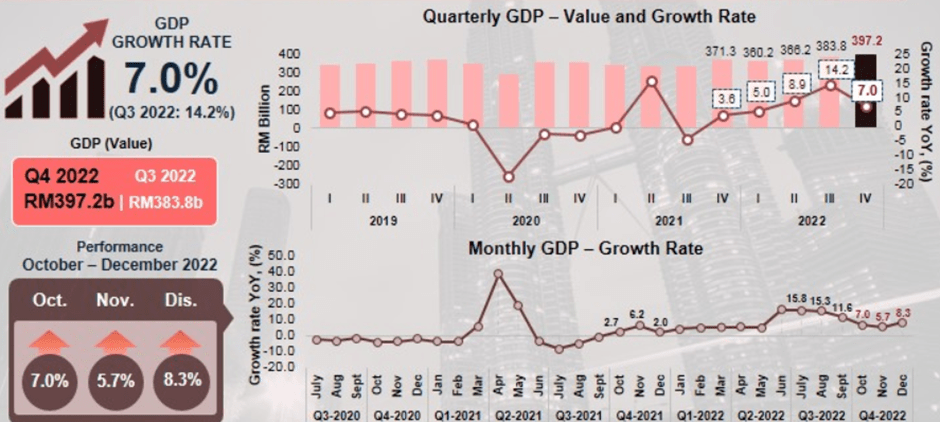

As one of the lowest-cost options available to US investors, the iShares MSCI Malaysia ETF ( EWM ) is worth a look for investors seeking exposure to a cheaply priced ASEAN growth story. Coming off a string of strong GDP releases through 2022 (+8.7% for the full year), Malaysia's economic growth remains on track to outperform the rest of the ASEAN region, supported by private consumption strength. Following the 'prosperity tax' (i.e., a one-off wealth tax) in 2022, which impacted many large-caps within the EWM portfolio, corporate earnings should also benefit from a tax rate normalization this year. Political risk is the only hurdle here – early signs point to a stable 'unity' government for the next four years, but the focus on fiscal consolidation and populist rhetoric could entail unforeseen taxes and other less business-friendly measures down the line. Still, the current low relative valuation (P/E and P/Book), in contrast with the region-leading economic growth, offers investors a good safety margin. And with foreign equity ownership also coming off a low base, EWM looks poised to benefit both ways (via earnings growth and a valuation re-rating).

Fund Overview – A Low-Cost but Concentrated Vehicle for Malaysia Exposure

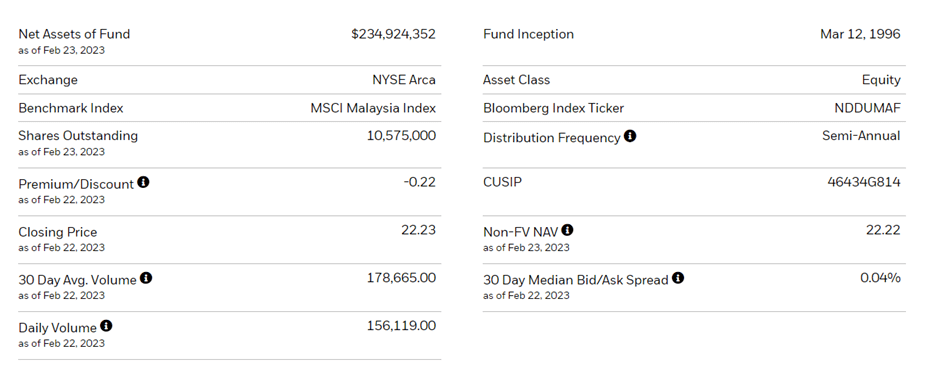

The US-listed iShares MSCI Malaysia ETF seeks to track, before fees and expenses, the performance of the MSCI Malaysia Index, comprising the large and mid-cap segments of the Malaysian market or ~85% of the Malaysian equity universe. The ETF held a $235m of net assets at the time of writing and charged a 0.5% expense ratio, making it one of the most cost-effective options available to US investors looking to access Malaysian equities. A summary of key facts about the ETF is listed in the graphic below:

{kind=link}

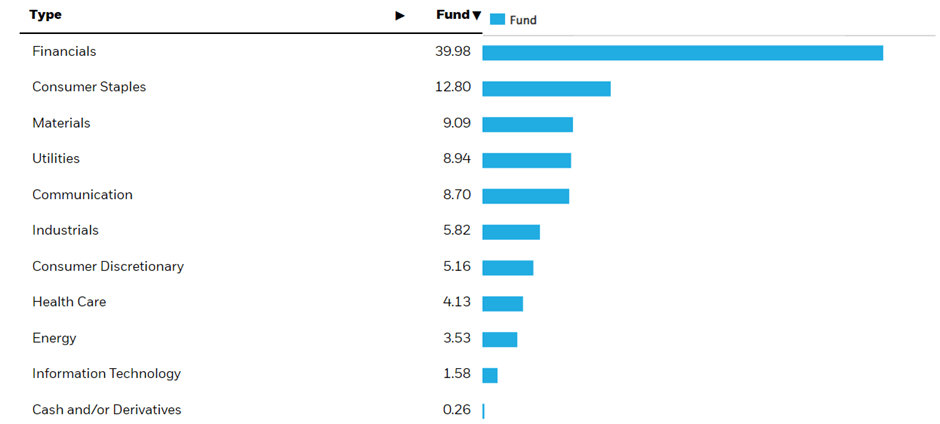

As reflected in the chart below, the fund's sector allocation is heavily concentrated on the financial sector at 40.0%, followed by consumer staples (12.8%), materials (9.1%), utilities (8.9%), and communication (8.7%). On a cumulative basis, the top five sectors accounted for a combined 79.5% of the total portfolio.

{kind=link}

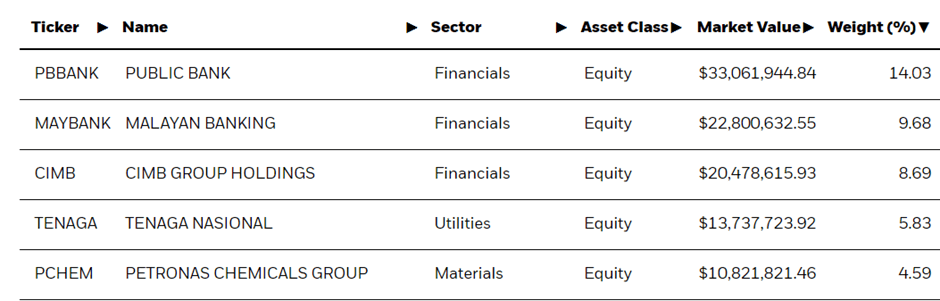

In line with the concentrated sector exposure, the fund is spread out across 34 holdings. The largest single-stock exposure is the following Malaysian banking leaders - Public Bank ( PBLOF ) (14.0%), Maybank ( MLYBY ) (9.7%), and CIMB Group ( CIMDF ) (8.7%). Outside of financials, the ETF also has outsized holdings in electric utility Tenaga Nasional ( TNABY ) at 5.8% and integrated chemicals producer PETRONAS Chemicals ( PECGF ) at 4.6%. The top five holdings account for ~43% of the overall portfolio, so from a single-stock perspective, this ETF is fairly concentrated as well.

{kind=link}

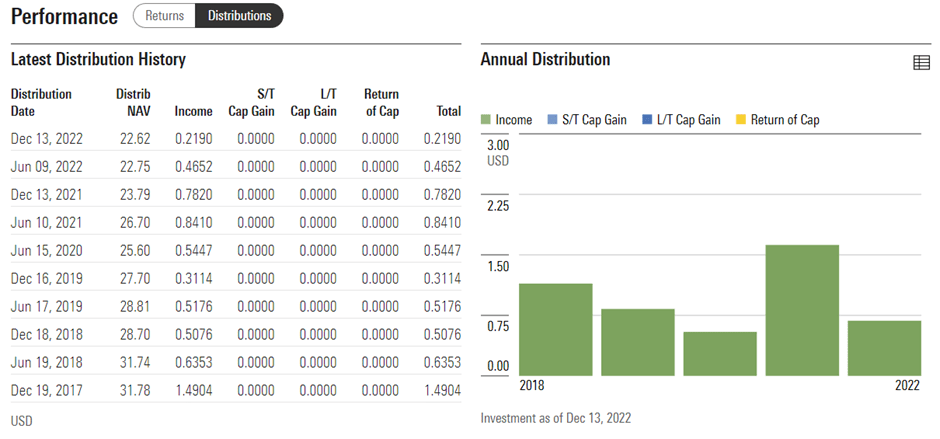

On a YTD basis, the ETF has declined by 1.9% and has compounded at an unremarkable 1.1% pace since its inception in 1996. The long-term performance is broadly in line with comparable ASEAN ETFs like the iShares MSCI Philippines ETF ( EPHE ) and the iShares MSCI Indonesia ETF ( EIDO ), both of which compounded at a similar pace. The fund distribution runs on a semi-annual basis, with the trailing yield at a decent 2.9%, providing a nice bonus for investors looking for an income supplement.

{kind=link}

Financials Concentration Offers a Good Proxy to the Broader Malaysian Economy

At first glance, the ETF's concentrated exposure to the major banks seems like a drawback. Yet, banks tend to track the domestic economy quite well, given their role in the credit creation process. The lending business has also moved beyond the historical reliance on government projects in recent years, so changes in overall consumption and capex will be captured in the sector earnings. External conditions will have an influence as well - with a global slowdown on the horizon for this year, the Malaysian economy's reliance on trade could weigh on growth. That said, the China reopening will offer a positive offset – as Chinese tourists are a major source of arrivals into Malaysia, expect the services sector to directly benefit, while the broader domestic economy also stands to gain from the spillover effects of increased tourist spending. Alongside the improving fiscal position and current account surplus, the health of the banking sector should remain intact.

Department of Statistics Malaysia

{kind=link}

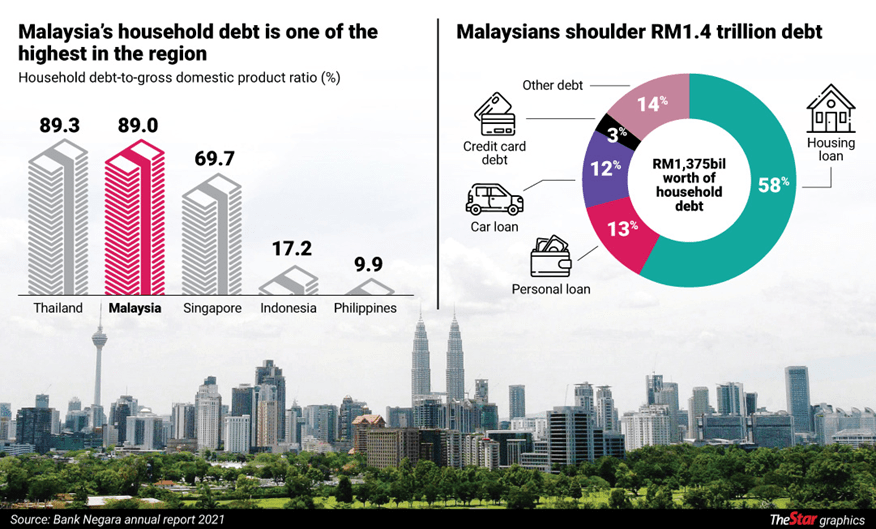

A key earnings growth driver for this year is a tax rate normalization following last year's "prosperity tax" hit, which should drive an outsized YoY bottom-line growth for the major banks in the EWM portfolio. Assuming asset quality also stays healthy as restructured loan levels normalize lower, expect more regulatory leeway from the central bank for higher dividend payouts as well. From here, the key risk to monitor is indebtedness - total debt/GDP is elevated at >120% private debt/GDP and ~89% household debt/GDP. As most of the weakness lies at banks serving the lower-end consumer and small/medium businesses, EWM's large-cap banking exposure should remain relatively insulated.

{kind=link}

One of the More Attractively Valued ASEAN Markets

Political stability aside, the underlying fundamentals of the Malaysian economy are strong, and a reignited Malaysian growth story looks to be on the cards following the 2022 performance. With a China reopening tailwind on the horizon alongside increasingly favorable labor market conditions (gradually improving unemployment rate and wage growth) and inflation-cushioning subsidies, consumer spending should lead the way. Yet, EWM trades at a P/E and P/Book below its Southeast Asian peer ETFs for Indonesia, Philippines, and Thailand despite comparatively stronger economic fundamentals and an improving corporate earnings outlook. Plus, with foreign shareholding at a low point, there is most likely more upside than downside from here.

| P/E Valuation |

| P/B Valuation |

| iShares MSCI Malaysia ETF |

| 14.76 |

| 1.49 |

| iShares MSCI Indonesia ETF |

| 15.25 |

| 2.15 |

| iShares MSCI Philippines ETF |

| 17.31 |

| 1.60 |

| iShares MSCI Thailand ETF |

| 17.29 |

| 1.97 |

Source: iShares

A Cheaply Priced Emerging Market Growth Play

Malaysia's economic growth outperformance in 2022 isn't reflected in its underlying equity valuations – the iShares MSCI Malaysia ETF lags behind its ASEAN peers across P/E and P/Book metrics despite a sustained pick up in private consumption. Also supporting the near-term upside case is a tax rate normalization following the big one-off hit to large-cap corporate earnings from last year's prosperity tax.' Risks from the current coalition government failing to last for its full term (recall the political instability of recent years) or a less market-friendly policymaking approach are valid but counterbalanced by the low valuation and low foreign ownership base. With EWM's outsized banking allocation poised to benefit from another year of growth while maintaining strong asset quality and provision buffers, the ETF is worth a look here.

For further details see:

EWM: A Cheaply Priced Emerging Market Growth Play