DBX - Examining Dropbox's Battle For Relevance In A Crowded Market

2023-07-04 09:37:53 ET

Summary

- Dropbox is uncompetitive compared to leading market options, likely due to the poor value proposition.

- Despite these concerns, DBX has shown impressive revenue growth, with a CAGR of 21%. We believe the lack of ARPU development in the coming years will slow this to <8%.

- DBX continues to pay substantial SBC despite the stock price trading flat for an extended period of time.

- Based on our bearish assessment of the business, our DCF valuation implies downside at the current share price.

Investment thesis

Our current investment thesis is:

- DBX is uncompetitive compared to the leading options in the market, as unlike Microsoft (MSFT) and Google (GOOG), DBX does not have related products that it can bundle.

- Further, we are not convinced by DBX's product development, as it is entering highly competitive segments within which we believe the company is not well placed.

- DBX's ARPU is unattractive, implying the company is reliant on Personal accounts.

- DBX is paying substantial SBC despite a poor share price performance.

- Based on our DCF valuation, we believe the company is overvalued.

Company description

Dropbox ( DBX ) is a leading cloud-based file hosting and collaboration platform that enables individuals and businesses to store, sync, and share files securely. Founded in 2007, the company has grown into a trusted brand serving millions of users worldwide, benefiting from a first-movers advantage.

Share price

DBX's share price has performed poorly in the last 10 years, as investor sentiment remains uneasy, fearing competitive threats to the business and thus its growth prospects. Despite this, however, the company has performed well financially.

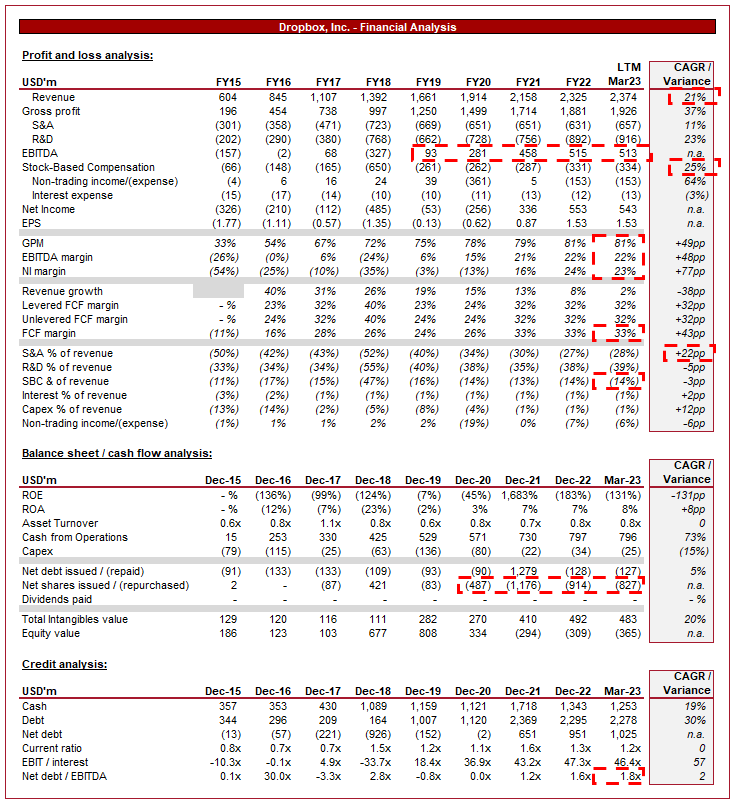

Financial analysis

Dropbox Financials (Tikr Terminal)

{kind=link}

Presented above is DBX's financial performance in the last 7 years.

Revenue & Commercial Factors

DBX has grown revenue at an impressive CAGR of 21% during the last 7 years, with only 1 fiscal year of sub-10% growth. This is a reflection of the company's strong trajectory, as it has successfully transitioned to a profitable business model.

Business Model

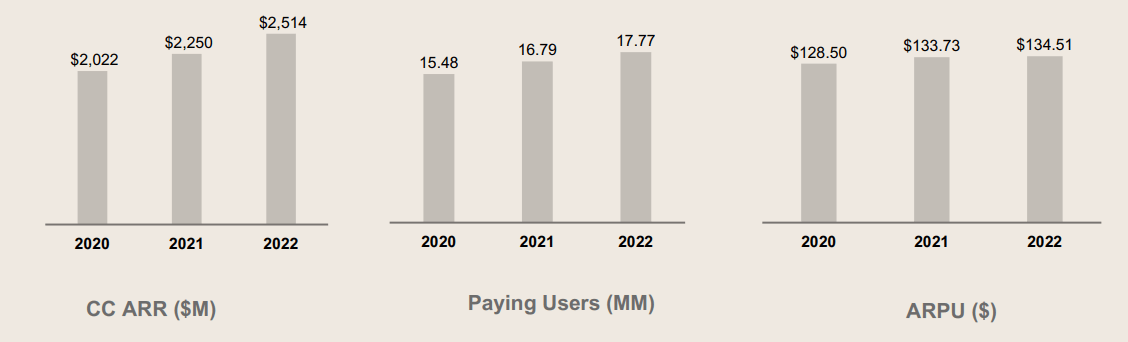

Dropbox operates with a freemium model, providing basic storage and collaboration features for free, while charging a subscription fee for additional storage capacity and advanced functionalities. The objective of such a strategy is twofold. Firstly, it develops a network effect, with a high number of users encouraging others to use the service, enhancing the value for all. Secondly, it acts as proof of quality, providing enough services to be usable but heavily encourages consumers to purchase a subscription to unlock the full potential. This model has been successful for DBX, as the number of paying users has gradually increased over time. In the most recent year, DBX reached 17.8m paying users, up from 15.5m in 2020 and on a total user base of 700m.

{kind=link}

DBX's paying customers are on a subscription model, which means they are paying on a monthly/annual basis for access to their accounts. This creates a lucrative revenue profile, as revenue is recurring in nature. So long as the service remains high-quality, customers will theoretically keep paying forever. Further, it means DBX can focus on winning new customers (rather than replacing and winning) while also developing its value proposition to allow the business to increase prices to all existing users (Avg. revenue per customer). This is why a Software-as-a-Service (SaaS) model is so attractive. DBX's ARR (annual recurring revenue) is $2,514m, 8% above revenue, implying continued healthy subscription growth.

DBX's key value proposition is its brand. The company was an early mover in the market and has developed a reputation for a high-quality and reliable service. This has established DBX as a leading player in the cloud storage and collaboration market.

DBX has been seeking to develop its value through the creation of related services. The company has expanded into the Document Signing segment, as well as other services that leverage its foundation solution of file sharing.

{kind=link}

The company is increasingly focused on its enterprise-grade solutions, including Dropbox Business and Dropbox Enterprise, tailored to meet the specific needs of businesses, with enhanced security and administration features. This is the more lucrative segment, as it allows DBX to charge a premium and by the user, essentially winning several (or hundreds, or thousands) of customers with one client win.

On paper, this business model looks relatively attractive and is developing well, however, we are concerned.

Firstly, the Company's ARPU is fairly underwhelming. DBX is currently generating an average of $135 per customer while its cheapest plan is $120. This is not an unusual skew as weighting will always be toward the bottom but this is extremely so, especially when considering the pricing post this package (see below). This implies the company is essentially a Personal User business.

{kind=link}

Secondly, we are not convinced by the company's brand/relative competitiveness. DBX, at no fault of its own, was unable to gain sufficient market share before the big boys entered the market. Now, DBX competes with the likes of Google, Microsoft, Apple ( AAPL ), and other established businesses (as well as new entrants such as Box ( BOX )). This discards any notion of a moat, especially when you consider this from an Enterprise perspective. With Microsoft, for example, a company gets storage, Office 365, Teams, and a range of other related services for <$15 p/m. With DBX, it's primarily just storage. If anything, the company's service is an inefficient allocation of resources for an enterprise business that uses it.

Finally, product development. DBX is spending just under $1bn on R&D. This is a drop in the water compared to its larger rival, meaning any new service it manages to develop as part of its ecosystem will already be provided by others, and likely at a superior level. Document signing and collaborative video solutions are a highly competitive segment already, making it difficult for DBX to materially gain market share.

Separately from its business model, DBX is currently paying substantial share-based compensation. This currently represents 14% of revenue, consistently exceeding 10%. While this has occurred, DBX's share price has traded flat, implying a misalignment of incentives. This is not the time to engage in a debate as to whether SBC should or should not be included/adjusted for within key metrics but it is worth highlighting to readers that this is a substantial cost to the business.

Software Industry

The shift towards remote work has increased the demand for cloud-based collaboration tools, with a focus on seamless file sharing, team collaboration, and remote access. Covid-19 enhanced this trend but it has been occurring for much of the decade, especially when you consider the internationalization of digital work. We believe this will act as a natural tailwind within the industry, supporting DBX's growth despite the competitive weakness we have highlighted. Market share will lag while absolute revenue growth will remain.

Having touched on this already, we believe the integration of tools and related software to the wider eco-system will drive outsized returns in the coming years, as both enterprise and personal clients seek to consolidate their subscriptions to "one-stop shop" packages.

In particular, we believe collaborative solutions are the next key growth area. Although we are unconvinced by DBX's expansion via its Capture product, we are pleased to see the company at least attempt to gain market share. This is a progressive development as part of the fragmentation of working teams geographically, as well as the continued desire for improving efficiency. Adobe's potential acquisition of Figma for $20bn is a reflection of the value a leading collaborative solution can yield.

Margins

DBX's margins have significantly improved in the last decade, without materially impacting growth, a quality development as the business transitioned to a sustainable business model. The company currently has an EBITDA-M of 22% and a NIM of 23%.

Margin development has been driven by a reduction in cloud-based costs, as illustrated by a rapid GPM improvement, as well as a transition of customers to a paying subscription. Margin improvement has somewhat flatlined in the last 2 years, however, it is too early to imply the company has matured. This slowdown could be a reflection of economic conditions, as DBX's exposure to Consumer accounts causes a slowdown in net paid customer growth.

Balance sheet & Cash Flows

DBX is conservatively financed, with an ND/EBITDA ratio of 1.8x. This affords the business flexibility, which we believe should be allocated to bolt-on M&A to enhance its eco-system (once rates decline).

With consistent cashflows, Management has funded aggressive share buybacks, consistently distributing once profitability was reached.

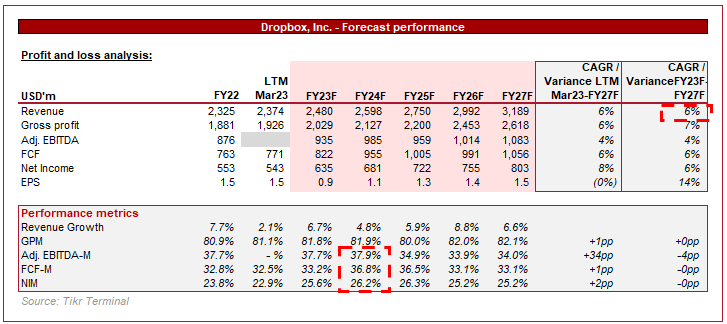

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a reduction in DBX's growth rate of mid-single digits, implying the days of double-digit growth are over. Despite our bearish view, this is slightly surprising to see, implying analysts are not wholly sold on the new software development.

Margins are forecast to remain flat and potentially decline. This is not an explicit expectation on our end although consider it a material risk, mainly due to competitive threats forcing the business to be price aggressive.

Valuation

DBX Valuation (Tikr Terminal)

DBX is currently trading at 20x LTM EBITDA and 11x NTM EBITDA. This is a discount to its 10 quarter average.

DBX's trading multiples have trended down in the last decade, reflecting an improvement in profitability exceeding price action. This is due to the sentiment around the business, with investors unconvinced by the value proposition.

Given the weakness in the brand and poor price action, we have chosen to value the business utilizing a DCF, rather than a multiples approach.

Our key assumptions are:

- Customer growth of low single digits, primarily driven by the general strength of the industry, with DBX outperformed by peers.

- ARPU growth of 1%, as DBX is unable to materially upsell customers due to its poor value proposition.

- Gradual GPM improvement and accelerated OPM improvement, driven by scale economies and the small marginal cost of providing services.

- An exit multiple of 12.5x and a discount rate of 8.55%.

Based on this, we derive a downside of (11.8)%. This reflects how important it is for DBX to improve its ARPU relative to customer growth. Find below a sensitivity of our flexible assumptions.

DCF sensitivity (Author's calculations)

Key risks with our thesis

The risks to our current thesis are:

- Customer growth resilience. Given our bearish view on the company's value proposition, we do not believe the company can materially upsell clients, i.e. increase its ARPU. User growth will soften but even if the company is unattractive, will increase purely from new customers entering the market. There is the risk that new customer growth is sufficient to offset the impact of poor ARPU.

- Acquisition-led development of its products suite, improving monetization.

Final thoughts

DBX has developed a strong cloud offering but we do not believe this is sufficient any longer to operate as an attractive business within the industry. It is critical to have related services that can be bundled together to enhance the value proposition. In this respect, we believe DBX has failed and will face a rapid slowdown in revenue growth.

For further details see:

Examining Dropbox's Battle For Relevance In A Crowded Market