EVEX - Examining Embraer As A Value Buy

2023-04-19 04:19:54 ET

Summary

- Embraer has seen a considerable stock surge in 2023, boosted by a positive Q4 2022 earnings report and an improving balance sheet.

- In the face of an uncertain long-term outlook in the regional jet market, Embraer is ramping up operations in other promising segments—notably in executive aviation and urban air mobility.

- Despite a climbing stock price, Embraer remains an intriguing value opportunity, undervalued by as much as 82%.

Editor's note: Seeking Alpha is proud to welcome AeroCapital Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Embraer ( ERJ ), the Brazilian regional and executive jet manufacturer, has experienced significant stock momentum in 2023, driven by strong Q4 earnings and deliveries that highlight its ongoing recovery from the pandemic. This outlook sets the stage for a deeper analysis of the company's potential.

Recognized as a value buy through the end of 2022, Embraer remains an enticing value proposition as of April 2023 despite its 56.3% YTD share appreciation. Currently, Embraer is benefiting from three distinct factors that, individually, would pique my interest as potential value opportunities:

- Embraer's strengthening liquidity, operating leverage, and overall financial position (i.e., aspects it can largely control)

- A commercial aviation market poised for strong near-term performance, coupled with a rapidly expanding executive aviation market

- A sum-of-the-parts discrepancy with its independently traded eVTOL aircraft company, Eve Air Mobility ( EVEX ).

In this article, I aim to delve further into these points to highlight my optimism for Embraer's operations and provide insight as to why I think the company is currently undervalued.

Recent Financial & Operational Performance

Embraer's stock has climbed 56.3% YTD (as of 16 April 2023), on the back of its robust year-end performance, and is steadily approaching its pre-pandemic trading levels of around $18 per share. The current share price of $16.66 (16 April) more than double its 2022 low of $8.20, an impressive rebound for a company that faced challenges such as reintegrating commercial jet production and indefinitely postponing its highly anticipated turboprop project in the same year.

In 2022, Embraer reported 8% YOY revenue growth, supported by increased deliveries in both its commercial and executive lines, as well as a strong year-end order backlog of $17.5 billion (up ~3% YOY). Embraer recorded an encouraging 17% and 10% growth in those divisions, respectively.

Embraer 2021-22 Net Revenues by Business Segment (Embraer 3/10/23 6-K)

{kind=link}

The company also experienced modest growth in its Services division, which largely depends on the performance of Embraer's other divisions, and a decline in its Defense segment as orders reverted to normal levels following an unusually high number of Super Tucano deliveries in 2021.

Embraer's 2023 guidance projects 65-70 commercial deliveries and 120-130 executive deliveries, potentially generating between $5.2 and $5.7 billion in revenue and representing approximately 14.6% growth in revenue from 2022 (source: 6-K). With Q1 2023 earnings just around the corner, indications suggest that Embraer is off to a strong start .

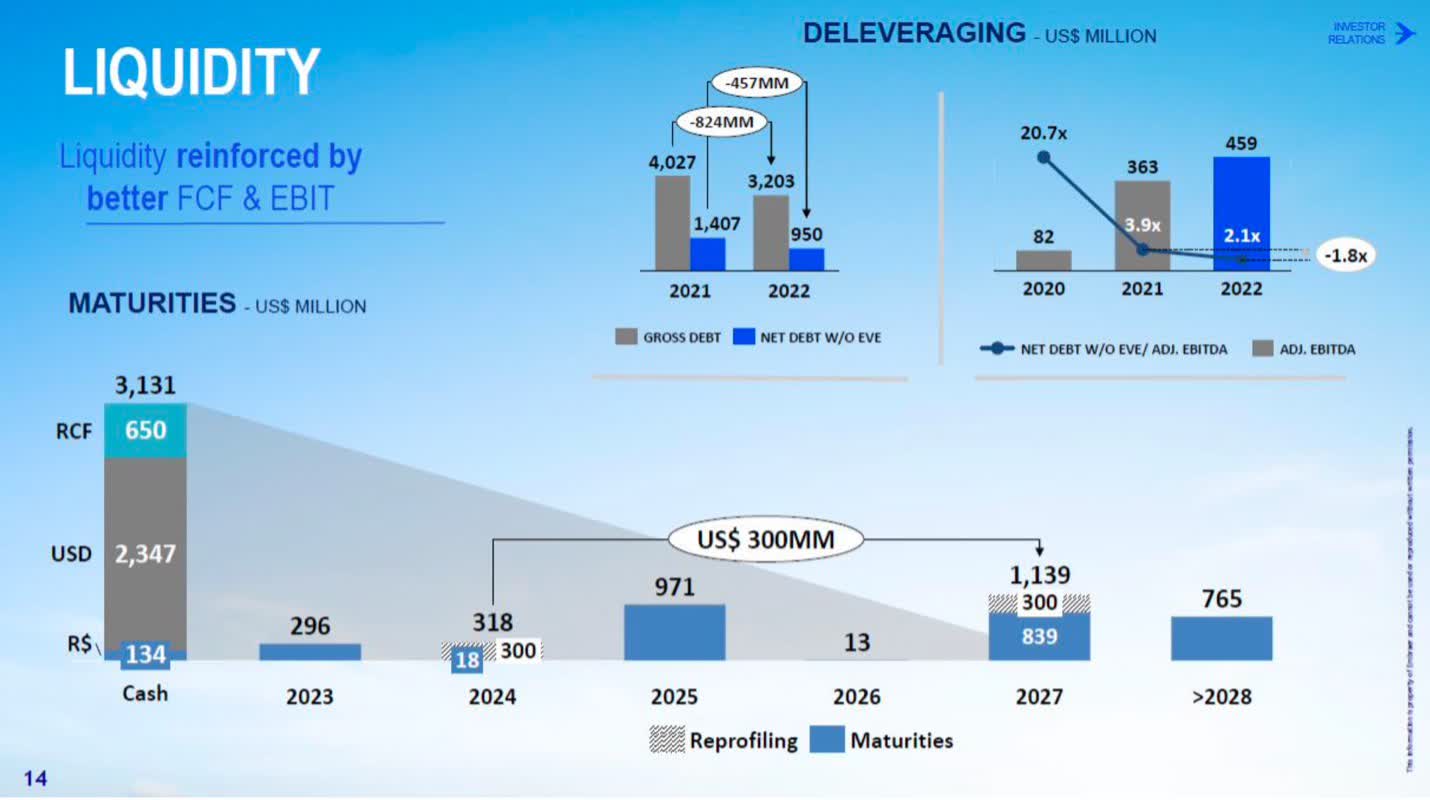

Improving Liquidity

Embraer has made significant strides in improving its liquidity. In 2022, the company reduced its gross debt by $824 million, including a $599 million reduction in long-term debt (a decrease of nearly 30% since Q4 2020) and a $457 million Eve-adjusted reduction in net debt.

Improving Operational Efficiency

The improvements in Embraer's liquidity would not have been possible without the improved operational efficiency demonstrated in 2022. Despite challenges such as the commercial aviation re-integration, ongoing supply chain issues, and a severe pilot shortage in North America, the company reported its seventh consecutive quarter of positive EBITDA.

Embraer also reported notably improved margins across all business lines, particularly in its two main segments. The commercial aviation gross margin rose from 4.0% to 10.5%, while the executive gross margin increased from 18.3% to 23.4%. It remains to be seen how sustainable these margin improvements will be.

These improvements contributed to an impressive free cash flow of $540 million (adjusted due to the Eve transaction), nearly doubling its 2021 free cash flow of $292 million (Embraer 2023 20-F).

(SEC EDGAR Database; ERJ 3/10/2023 6-K)

{kind=link}

Embraer's rising sales, boosted operational efficiency, and improving liquidity should provide the company with the flexibility to capitalize on three compelling business segments, one of which I believe may face challenges in the long run, and two poised for growth.

Regional Jets: Navigating an Uncertain Outlook

Although Embraer's commercial segment is recovering to near pre-COVID levels, I remain somewhat bearish on the company's long-term prospects in the regional jet market.

One key issue is the apparent decline of the regional jet market, which is already relatively small compared to the mainline, narrowbody commercial space dominated by Boeing (BA) and Airbus (EADSF). Oliver Wyman's 2023 Global Fleet and MRO Market Forecast estimates regional aircraft to currently account for only 11% of the total ~$80 billion global annual MRO spend (maintenance, repair, and overhaul) and projects a further decline, predicting a -0.3% CAGR in the MRO market over the coming decade. The forecast also suggests that regional jet deliveries in the next decade will primarily consist of replacements for retiring planes, rather than new growth.

While Oliver Wyman predicts the global regional jet fleet to grow by about 8.5% by 2033, compared to a near-33% growth prediction for the entire global fleet during the same period, this modest growth would cause the share of regional jets as a percentage of the global fleet to decline from around 12% in 2023 to under 10% by 2033.

The relative decline in the regional jet fleet can likely be attributed to the long-term effects of pilot shortages in North America and Europe (where 66% of the global regional jet fleet is based) on the regional jet business, which is particularly sensitive to these shortages. Additionally, regional routes are generally less profitable (and are thus the first to be eliminated), and are becoming increasingly susceptible to legislative disruptions .

The good news for Embraer is its strong market position for commercial jets under 150 seats and its total dominance in the market for commercial jets under 100 seats. Even with the regional jet market in decline, Embraer will likely be able to extract value from its commercial jet segment for some time.

Accordingly, some analysts (BofA Global Research) still anticipate healthy growth for Embraer in its regional jet segment in the coming years. However, Embraer may not have enough operating leverage remaining in its regional jet production to rely on operating in a declining market as a viable primary strategy.

Opportunity in Executive Aviation and UAM

Executive Aviation

The executive aviation market has seen considerable growth worldwide since the COVID-19 pandemic. As the leader in the business aviation space with an estimated 86% global market share of jets under 100 seats-led by the Phenom 300, the bestseller in its category for the last ten years-further growth in this market offers a significant opportunity for Embraer.

Honeywell's 2022 Global Business Aviation Outlook report projects business jet usage to be 9% higher in 2023 than in 2022, with jet deliveries expected to increase by 17% and expenditures by 20% in 2023 compared to 2022. Honeywell forecasts the business aviation market returning to pre-COVID levels in 2023, as demand for business jets has already reached levels similar to 2015, and flight activity at times in 2022 matched levels not seen since 2007, business aviation's busiest year on record.

With a significant market share in the business jet sector, improving margins, and a market set to surpass pre-pandemic levels, Embraer is well-positioned to capitalize on the increasing demand for business jets. BofA analysts project a 10% growth to 120 business jet deliveries in 2023, well above the 109 delivered in 2019.

This surge in demand is partly driven by the influx of new plane owners and private flyers, the rise in services like NetJets, and the growing popularity of fractional plane ownership. And as more companies turn to business jet options to bypass the cumbersome nature of commercial aviation, Embraer is poised to benefit significantly from the executive aviation boom in the coming years.

Urban Air Mobility ((UAM))

Often referred to as "the Uber of the sky," some electric vertical take-off and landing (eVTOL) aircraft manufacturers believe that their prices will eventually compete with those of Uber (UBER) as the urban air mobility industry evolves throughout the late 2020s. Attracted by total addressable UAM market estimates ranging from $750 billion to $9 trillion by 2050 , Embraer launched an independent eVTOL manufacturer called Eve Air Mobility. Eve went public via a SPAC in May 2022 at $10 per share, with Embraer retaining approximately 90% ownership .

Set to begin deliveries in 2026 and not record positive EBITDA until 2028 , Eve represents one of Embraer's most ambitious projects in its storied history of developing cutting-edge aviation technology. eVTOL carries substantial and clear risks-production is at least a year from beginning, industry orders are non-binding, and the R&D costs to make Eve (or any eVTOL) functional and truly competitive with Uber's prices will be massive. It's also important to note that Embraer will likely face competition in this space from Boeing's Wisk, Textron's (TXT) Pipistrel, and venture-backed Joby Aviation (JOBY), among others.

Valuation

In this section, I will outline my valuation approach for Embraer and Eve. Through this exercise, I'll demonstrate my belief that not only is Embraer undervalued on its own, but it becomes even more so when considering its 90% stake in Eve. I will first provide my own valuation for Embraer, followed by a separate valuation for Eve that is guided by management's own forecast.

Embraer

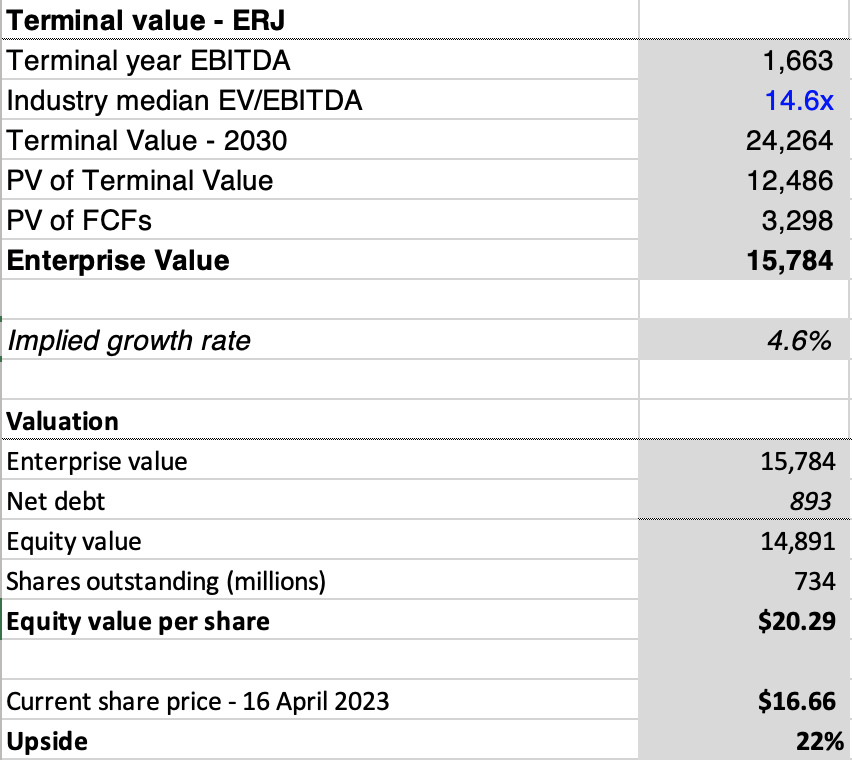

I've attempted to value Embraer using a straightforward DCF projection through 2030, which extends beyond the typical 5-years-or-so time horizon I'm generally comfortable with, given the uncertainties associated with longer-term forecasts. I've chosen to forecast through 2030 to match Eve's management forecasts, which I will discuss in the next section.

Created by author with data from Embraer

{kind=link}

I've forecasted revenue, EBITDA, and capital expenditure using data provided by Embraer and cross-referenced these figures with consensus estimates from CapitalIQ and house estimates from BofA Global Research. I've assumed depreciation & amortization and net working capital to grow in line with revenue and have applied a 9% discount rate.

Created by author with data from Embraer

{kind=link}

My valuation indicates that even after the recent stock price increase, there is still approximately 22% potential upside for Embraer. I understand that the implied terminal growth rate might seem surprising, given the 14.6x industry multiple, but I am reluctant to argue with Damodaran on this point.

Eve Air Mobility

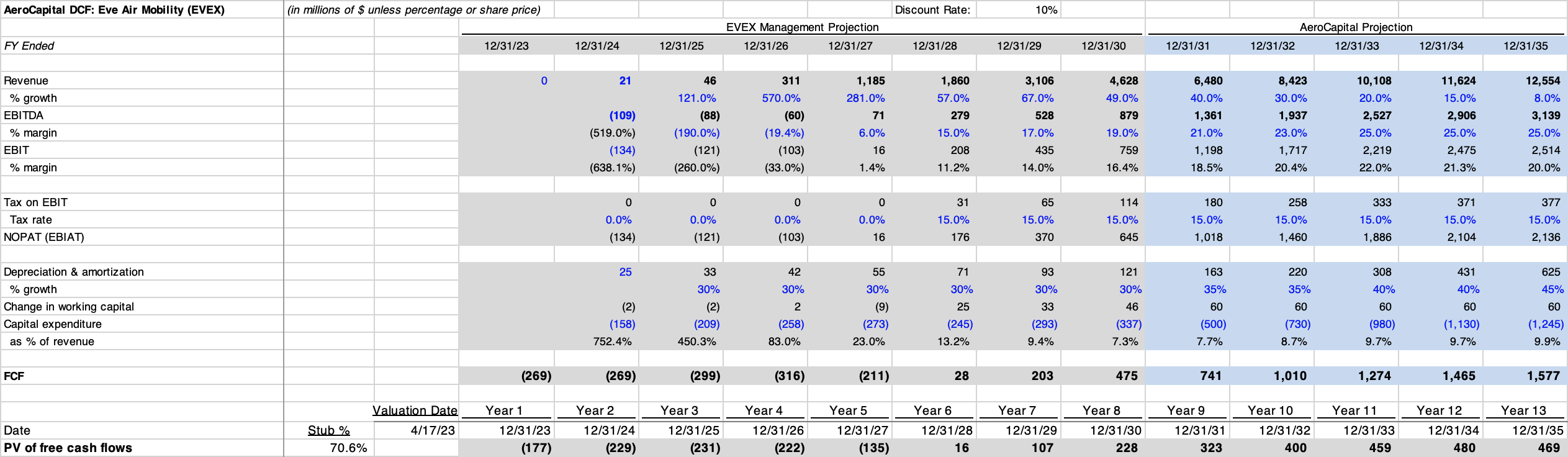

I've also projected Eve Air Mobility's performance through 2035, using management forecasts up until 2030.

Created by author with data from Embraer and Eve

{kind=link}

Forecasting cash flows 7+ years into the future for a company without a product is challenging, so I've attempted to temper the forecasts over the five years following the end of management's projections.

Created by author with data from Embraer and Eve

{kind=link}

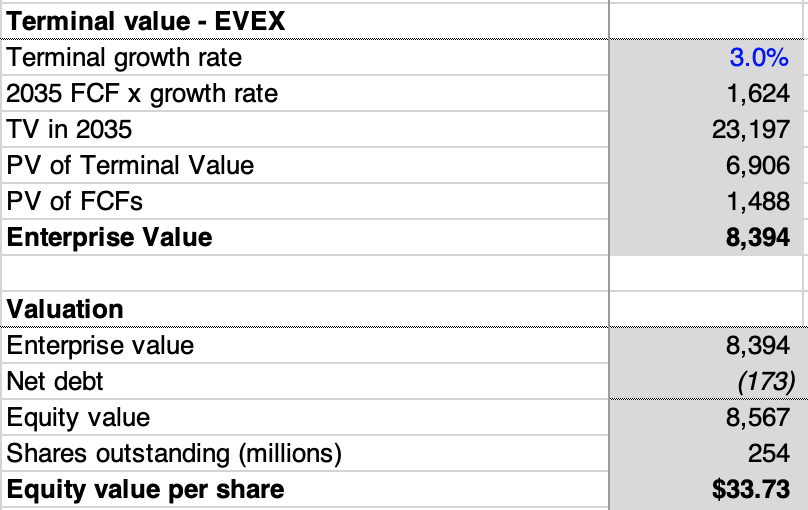

For Eve, I've used a 3% growth rate in perpetuity rather than using the EV/EBITDA approach employed for Embraer, due to the impracticality of using multiples to value a company at Eve's stage of development. Similarly, I've assumed a 10% discount rate, which is higher than my assumption for Embraer, given Eve's riskier profile. This results in a valuation of $33.73 per share.

Assessing the Value of Embraer and Eve Together

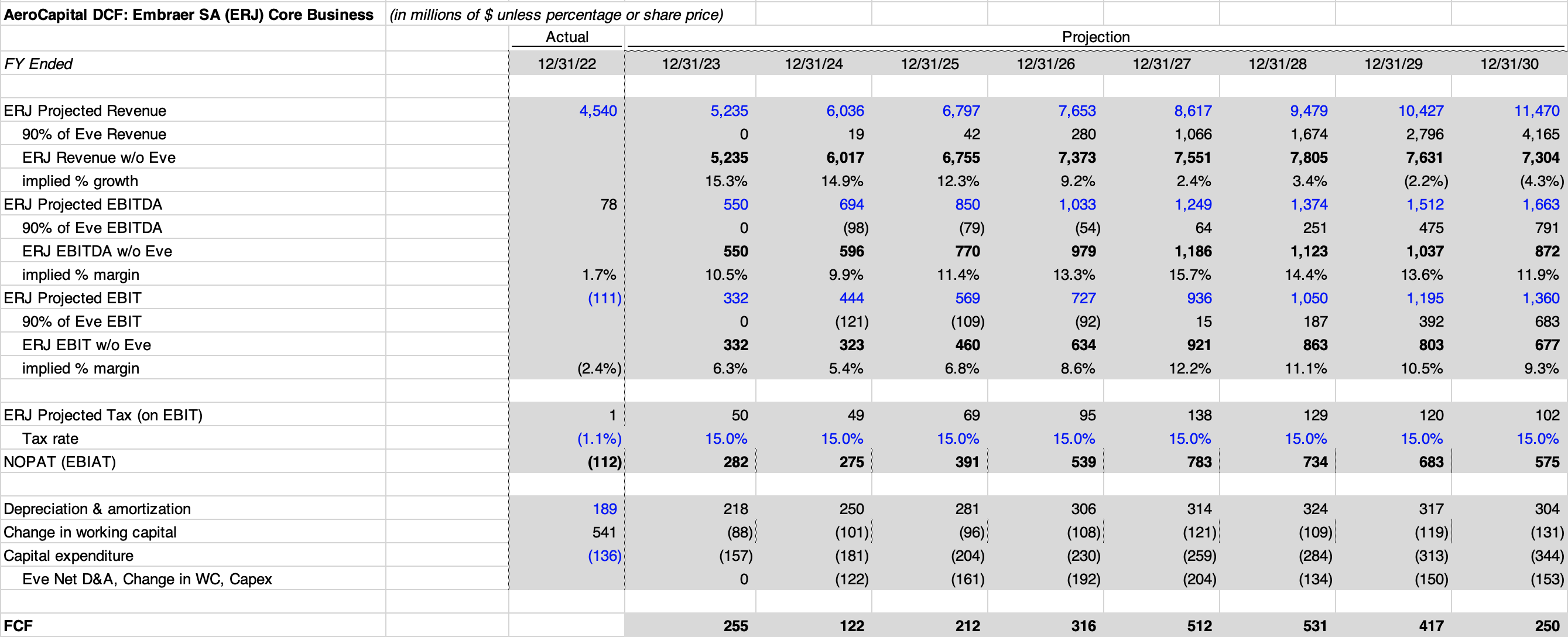

The relationship between my models for Embraer and Eve is difficult to discern, as various assumptions about Eve's performance until 2030 are implicitly included in my forecast for Embraer (i.e., I didn't remove contributions from Eve in my Embraer forecast). If I had assumed Eve's management projections to be spot-on through 2030 and tried to evaluate only Embraer's core operations during that period, my projections would have looked like this:

Created by author with data from Embraer and Eve

{kind=link}

The purpose of the above graphic is to determine how Embraer's non-Eve-related business segments would need to perform to remain consistent with estimates from my original forecast for Embraer, which includes the effects of Eve, when we assume that Eve's management projections are precisely accurate.

The point I want to emphasize is that I find it highly unlikely that Embraer's core operations would struggle to the point of negative revenue growth in 2029 and 2030. Therefore, it is implied through my original valuation of Embraer that I believe Eve's management projections to be somewhat inflated.

By how much, I'm uncertain. I have no more insight than the average aviation investor and don't have a strong basis to differentiate between whether 30%, or, say, 70% of management projections will materialize for a company whose potentially revolutionary product is still in development.

I can propose, however, that I believe ERJ to be undervalued and potentially far more undervalued if Eve's operations play out according to management's plan, as shown below:

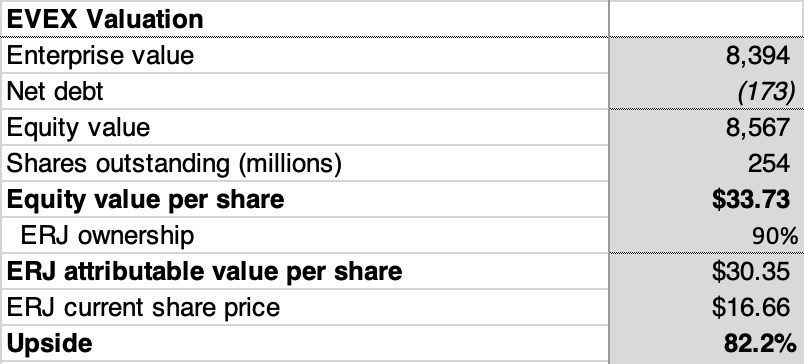

Created by author with data from Eve and Embraer

{kind=link}

This analysis suggests an upside of 82% (as of 16 April 2023) if everything goes according to plan for Eve through 2030. The market seems to be responding to the value mismatch, another analysis conducted in September 2022 suggests an upside of 245%, when Embraer was trading for $10.13 per share.

Valuation Summary

My valuation of Embraer is based on my assumptions about its core (non-Eve) business and is sanity-checked against consensus estimates for revenue, EBITDA, and EBIT. I arrived at a valuation of $20.28 per share, 22% higher than its current trading price of $16.66, suggesting a present value opportunity.

My valuation of Embraer implies that I don't expect my own valuation of Eve to fully materialize, or else my per share valuation of Embraer would be considerably higher. Given that Eve aircraft shipments are years away and its orders are non-binding, I am hesitant to explicitly account for Eve's performance in my valuation of Embraer. However, my separate valuation of Eve, which is based on management estimates, demonstrates a path from modest to potentially massive value for Embraer.

As it relates to valuation, there are two primary items that I will monitor that could change my assessment of Embraer as a value opportunity:

- Given no material changes in Embraer's business, I'd be hesitant to buy past my $20.28 estimation point.

- Significant developments related to Eve. A large portion of Embraer's potential as a value stock is tied up in Eve's performance, so strong negative news regarding Eve (such as, if Embraer were to indefinitely postpone Eve development) would cause me to at least reassess my value proposition.

Risk Discussion

There are several areas that I will closely monitor, in addition to basic financial health data and Eve developments, to determine if my investment thesis for Embraer remains valid.

Regarding financial performance, I will keep a close eye on Embraer's net debt position. It's encouraging to see it improving, as this will support the company's ability to pursue ambitious projects like Eve.

Concerning the commercial and executive jet markets, I will track Embraer's deliveries in these segments to ensure that its production roughly aligns with market growth. Embraer holds strong positions in the commercial segment it competes in and in the executive segment as a whole, so any deviation from this position would be concerning. In the executive aviation space, there is the potential threat of the aviation giants (Boeing and Airbus) targeting Embraer's leading position, although this would likely occur years down the line.

There is also significant market risk at play. While I believe executive aviation will perform relatively well during market downturns due to increased convenience and accessibility through programs like NetJets, this assumption could prove incorrect.

Regarding urban air mobility and eVTOL aircraft, there is the obvious possibility that Embraer's Eve may not succeed or could face stiff competition from rivals such as Wisk (Boeing) and Pipistrel (Textron).

Lastly, it's important to consider that Embraer's stock carries higher betas and increased foreign exchange exposure due to its base in Brazil, which adds another layer of risk for investors.

Conclusion

I believe Embraer presents an attractive opportunity for investors with a long-term, value-focused investment perspective. Embraer appears to be increasingly effective at managing factors within its control, such as strengthening its balance sheet, enabling it to capitalize on opportunities that are largely beyond its control. These opportunities include a shifting commercial aviation outlook and the rapid growth and development in executive aviation and urban air mobility.

As a result, I suggest that Embraer is currently undervalued by approximately 22%, and potentially as much as 82% for those who are particularly bullish about Embraer's eVTOL project or about its penchant for innovation more generally.

For further details see:

Examining Embraer As A Value Buy