GLNG - Excelerate Energy: A Lot Of Potential But Looks Expensive

Summary

- Excelerate Energy is the largest owner/operator of FSRU units in the world.

- These vessels are necessary for the LNG trade as they convert the compound back into a usable form.

- The company enjoys stable revenues and significant growth potential, courtesy of its business model.

- The company has a very strong balance sheet, which should provide some comfort to investors.

- The company is rather expensive compared to other LNG infrastructure firms at the current price.

Excelerate Energy, Inc. ( EE ) is a liquefied natural gas infrastructure company that specializes in the ownership and operation of floating storage and regasification units. This is a very different function than that performed by liquefied natural gas producers like Cheniere Energy ( LNG ) or tanker operators like Cool Company, which was formerly part of Golar LNG ( GLNG ). That does not mean that the function performed by Excelerate Energy is not important, however. In fact, the company has been benefiting from the European demand for liquefied natural gas which has been growing rapidly ever since the Russian invasion of Ukraine. Excelerate Energy itself has not really been benefiting from this as the stock is one of the few in the energy sector that are down over the past twelve months. Despite this, the company’s near-term valuation looks fairly high. The company could still prove to be a good investment over the long term though and it has been growing quite rapidly, which could pay off for investors.

About Excelerate Energy

As stated in the introduction, Excelerate Energy is a liquefied natural gas infrastructure company that specializes in the ownership and operation of floating storage and regasification units. These are marine vessels that take liquefied natural gas off the ocean-going tankers that transport it and convert it back into its gaseous state. In many cases, these are old liquefied natural gas tankers that have been converted into a new purpose.

{kind=link}

It should be fairly easy to see why these vessels are necessary parts of the liquefied natural gas industry. After all, natural gas in its liquid state cannot really be used for anything. Rather, natural gas-powered appliances are designed to use the substance as a gas. Thus, it is necessary to convert the liquefied natural gas back into a gas in order to pump it into the distribution infrastructure that already exists in the importing nation.

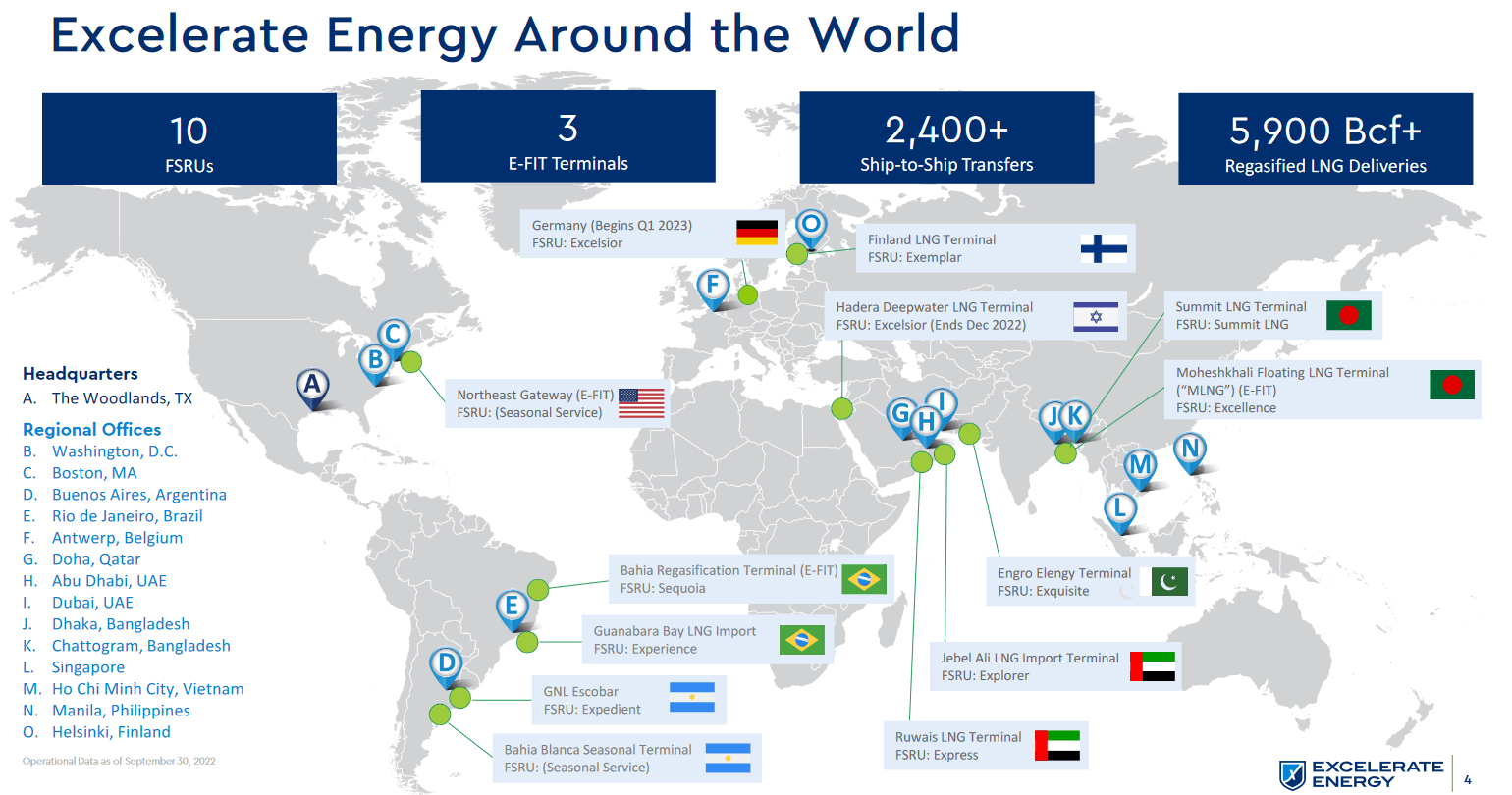

Excelerate Energy currently operates ten of these regasification units, which are located in nations all over the world:

{kind=link}

This is the largest fleet of any company in the industry, although as I have pointed out before, it is not always necessary to be the biggest company in the industry to represent an attractive investment opportunity. In terms of relative size though, Excelerate Energy is only a $2.59 billion market cap firm so it is obviously nowhere close to the largest company in the energy industry.

Excelerate Energy has a business model that lends itself well to stable revenues and cash flows. In short, the company enters into long-term contracts with its customers that wish to use one of its vessels. For example, during the third quarter of 2022, Excelerate Energy entered into a five-year contract for Excelerate Excelsior , which will begin work in Germany during the first quarter of this year. This business model provides Excelerate Energy with a great deal of protection against fluctuations in energy prices since the contracts should be long enough to outlast any short-term economic shock. This is similar to the financial model of pipeline companies like Kinder Morgan ( KMI ) in this regard. We can see the company’s general stability by looking at its revenue over the past nine quarters:

{kind=link}

The other thing that we notice above is that Excelerate Energy’s revenue has been steadily growing over time. This is because the company has been growing its fleet and has not been having any trouble getting contracts. Most importantly though, this growth has allowed the company to grow its cash flow over time. As we can see here, the company reported an EBITDAR of $86.4 million, which is significantly higher than the company had in prior quarters. This represents a general continuation of its long-term growth:

Excelerate Energy

Excelerate Energy is likely to continue this growth trend going forward. As already mentioned, Excelerate Excelsior is scheduled to begin work on a five-year contract in Germany during the first quarter of 2023. This vessel with therefore begins generating revenue for the company as soon as it begins operating, which should also have a positive impact on the company’s profit and cash flow. Excelerate Energy also has an eleventh floating storage and regasification unit under construction at the Hyundai Heavy Industries shipyard.

Excelerate Energy did not specifically state where this eleventh vessel will operate, which is somewhat concerning. In various previous articles, I have discussed the benefits that come with securing contracts before spending a great deal of growth capital. The most important of these is that this ensures that the project will be able to start generating revenue and cash flow as soon as it begins operating and thus ultimately pay for itself. Back in 2013, we saw a large number of offshore drilling companies constructing drilling rigs without having a customer in place for them. We all remember what happened to that industry as it has still not recovered. It would be disappointing if that were to happen to the liquefied natural gas sector. It would be especially devastating to shareholders of Excelerate Energy as the company is spending a great deal of money to construct the vessel. The company has not specified exactly how much it is spending for the vessel but it has stated that it is expected to be ready for its first contract in June 2026. That gives the company about three years to find someone that wants to use this vessel.

The company’s management is naturally optimistic that it will be able to accomplish that. In the press release during which the company announced the construction of this eleventh regasification unit, Steven Kobos, president and CEO of Excelerate Energy, stated,

“This shipbuilding contract with HHI demonstrates our commitment to grow our FSRU fleet at a time when the world needs FSRUs and flexible LNG infrastructure the most. Recent geopolitical events, including the energy crisis in Europe, have highlighted the essential role FSRUs play in providing energy security and serving as a complementary backstop to balance the intermittency of renewable energy. Upon delivery, this newbuild FSRU will enhance the capabilities of our existing fleet and support the execution of our integrated growth projects.”

Mr. Kobos makes some very good points. As I have pointed out numerous times in the past, one common strategy being implemented by utilities all around the world is to supplement renewable generation facilities with natural gas turbines. This is because solar and wind power are unreliable by their nature and no number of batteries can change that given current technologies. When we consider that Europe and Asia lack sufficient natural gas reserves and production to fuel these turbines, it is very necessary for these two heavily populated regions of the world to import natural gas from overseas. The only way to transport natural gas over the ocean is to convert it into liquefied natural gas. This is obviously causing a great deal of demand for liquefied natural gas infrastructure, which Mr. Kobos certainly indicates. However, the offshore drilling industry was also very well-positioned for a boom until the energy bear market and increasing focus on shale drilling crushed it. While the fundamentals for liquefied natural gas are indeed very strong, I would still feel much more comfortable if the company had a contract in place for this new vessel.

With that said, one possible opportunity for this new vessel could be in Bangladesh. The North-West Power Generation Company Limited is in the process of setting up a 1,200-megawatt liquefied natural gas power plant at Payra in Patuakhali. Naturally, this power plant will need a great deal of liquefied natural gas to operate and it will require a floating storage and regasification unit to be placed at the site to handle the steady stream of natural gas that will need to be imported across the Bay of Bengal:

{kind=link}

Excelerate Energy has stated that it is currently in discussions to be involved in this project in such a capacity, although it has not provided any further information. Nevertheless, this is a logical customer for the company’s eleventh floating storage and regasification unit. Admittedly, nothing has been determined for sure yet but this could very easily play out the way we just discussed. Even if it does not, Excelerate Energy has some other opportunities for its eleventh vessel, such as one in Southern Europe.

Fundamentals Of Liquefied Natural Gas

As I discussed in a recent blog post , the fundamentals for liquefied natural gas are incredibly strong right now. Perhaps surprisingly, much of this strength comes from global concerns about climate change. According to the International Energy Agency, the global demand for natural gas will increase by 29% over the next twenty years:

{kind=link}

The biggest reason for this was already mentioned earlier in this article. Climate change concerns have prompted governments all over the world to impose a variety of incentives and mandates that are intended to reduce the carbon emissions of their respective nations. One of the most common strategies to accomplish this is to encourage utilities to retire old coal-fired power plants and replace them with renewable ones, especially wind and solar power. However, wind and solar power are not reliable enough to provide the “always-on” capability that we have come to expect from a modern energy grid. After all, wind power does not work when the air is still and solar power does not work at night. The usual solution to this is to complement renewables with natural gas-fired power plants. This is because natural gas is reliable enough to ensure a properly functioning electric grid and burns cleaner than any other fossil fuel.

However, many areas of the world lack sufficient natural gas production to satisfy their need for natural gas. For example, the European Union has been dependent on Russia for natural gas for decades. As a result of the tensions between NATO and Russia, the natural gas supply has now been severely curtailed. This has made it necessary for Europe to import natural gas from friendly nations across the ocean, such as the United States. That requires the natural gas to be converted into liquefied natural gas. However, the majority of liquefied natural gas demand growth is expected to come from Asia, which is looking toward natural gas as a potential solution to its smog problems:

Golar LNG

As we can clearly see here, Asia alone is expected to cause the demand for liquefied natural gas to increase by 40% by the end of the decade. Clearly, this represents an excellent growth opportunity for Excelerate Energy as its floating storage and regasification units provide a vital link in the liquefied natural gas infrastructure chain. This should overall position the company quite well for fairly strong growth over the coming years.

Financial Considerations

It is important to examine the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. As this is usually accomplished by issuing new debt and using the proceeds to repay the maturing debt, a company’s interest expenses may increase following the rollover depending on the conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company’s cash flows to decline may fall into financial distress if it has too much debt. Although Excelerate Energy’s business model typically lends itself well to stability, the same is true of Seadrill ( SDRL ) and that company has gone bankrupt twice in the past decade. As such, this is a risk that we very much want to examine.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing itself with debt as opposed to wholly-owned funds. It also tells us how well the company's equity will cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of September 30, 2022, Excelerate Energy had a net debt of $397.8 million compared to $1.6498 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 0.24 today. Here is how that compares to some of the company’s peers:

| Company |

| Net Debt-to-Equity Ratio |

| Excelerate Energy |

| 0.24 |

| Golar LNG |

| 0.11 |

| FLEX LNG ( FLNG ) |

| 1.60 |

As we can clearly see here, Excelerate Energy appears to have a very reasonable debt load relative to its peers, although it does not have the strongest balance sheet in the sector. However, the company’s equity is more than sufficient to cover its debt obligations so that should help keep the company’s debt-related risks down.

However, a company’s ability to carry its debt is more important than the raw amount of debt in its financial structure. The usual way that we judge this is by looking at the company’s leverage ratio, which is defined as debt-to-adjusted EBITDA. This ratio basically tells us how many years it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. As of September 30, 2022, Excelerate Energy had a leverage ratio of 2.5x based on its trailing twelve-month adjusted EBITDA. That is probably reasonable when we consider that the company’s revenue primarily comes from long-term contracts, allowing it to carry a debt load similar to that of a midstream company. Those companies can usually carry 4.0x leverage without any real trouble so Excelerate Energy should be fine here, especially when we consider that the company’s assets substantially exceed its debt.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a sub-optimal return. In the case of Excelerate Energy, we can value the company by looking at its forward price-to-earnings ratio. This ratio tells us how much we need to pay today for each dollar of earnings that the company is expected to generate over the next year.

According to Zacks Investment Research , Excelerate Energy currently has a forward price-to-earnings ratio of 30.05 based on analysts’ expectations of its forward earnings. This seems rather expensive considering that the S&P 500 Index ( SP500 ) has a forward price-to-earnings ratio of 20.15. It also makes Excelerate Energy one of the few companies in the energy sector that do not appear to be incredibly cheap. Here is how it compares to its peers:

| Company |

| Forward P/E Ratio |

| Excelerate Energy |

| 30.05 |

| Golar LNG |

| 17.58 |

| FLEX LNG |

| 11.64 |

Admittedly, this is rather disappointing as it does not appear that Excelerate Energy offers a particularly attractive valuation today. This certainly does not mean that the company cannot offer an opportunity, particularly if one were to purchase on dips but it looks to be a bit expensive relative to some other liquefied natural gas infrastructure companies.

Conclusion

In conclusion, Excelerate Energy is a liquefied natural gas infrastructure company that plays a vital role in the sector. The company is the largest pure-play regasification unit operator in the world and the vessels are vital to anyone that wants to import liquefied natural gas, Excelerate Energy is well-positioned for any liquefied natural gas demand growth. This is likely to be the case as the demand for this substance is expected to surge over the coming years. Excelerate Energy has a surprisingly conservative balance sheet, which is nice to see considering the disaster that befell many other offshore companies in the past. The only real downside here is that the company looks to be rather expensive at the current price. Overall, the company is worth adding to a watchlist.

For further details see:

Excelerate Energy: A Lot Of Potential But Looks Expensive