EIFZF - Exchange Income Corp.: One Of My Favorite Monthly-Paying Companies For 2023

Summary

- My tenure of watching/reporting on Exchange Income Corporation has been one of almost constant positivity, and good RoR.

- Since my last article, the company has seen positive RoR in the double digits, outperforming the S&P 500 by a factor of 3x.

- Despite the company's size, it's one of my favorite Canadian investments, and has been since finding it. Its COVID-19 performance, fundamentals and management convince.

- Here is my thesis for the company for 2023, and it's a mostly positive one.

Dear readers/followers,

At times, you can be amazed by how long a company can go under everyone's radar despite, as it is to "you", clear that said company is of immense quality and has real, convincing upside.

Such is the case I'm continuing to make for Exchange Income Corporation (EIFZF). Over the past few months, I've even seen a few times where I've been tempted to start trimming somewhat as some of my more positive theses have started materializing.

Seeking Alpha Exchange Income (Seeking Alpha)

Being that I seem to be the only one covering this particular business, I feel that it falls to me to continually try to point out the upside, the fundamentals, and what you may get when you invest in Exchange Income Corporation.

Exchange Income Corporation - What there is to like about 2023

So, to be clear - two tickers are relevant here, and as I always do when faced with a native/non-native or ADR choice, I go native whenever I can. In this case, that means investing in the Canadian ticker EIF (EIF:CA). That's where the stock is typically traded.

You could argue, and you would be at least partially right in doing so, that Exchange Income is a riskier play than I usually write about. My long history of covering this stock and the success I've had with it exposes me to the risk of confirmation bias, not to mention a whole other host of issues, the least of which and one I intend to discuss here, is "not knowing when to quit".

Part of my strategy involves trimming when a company reaches heights that I either believe it should not or that I believe it will/likely could drop from. It's been my experience from years of investing that this is a sound strategy to save you from losing paper profits from when your high-conviction holdings go into bubbles.

Do you "have" to do this?

No, of course not. Buy-and-hold-investing is a perfectly valid strategy, and investors will do just fine following that. However, as a valuation-oriented investor, I'm firm in my stance that every company has a state of undervaluation , and one of overvaluation. It's the way the market works - it overreacts, and it does so with unexpected volatility at times.

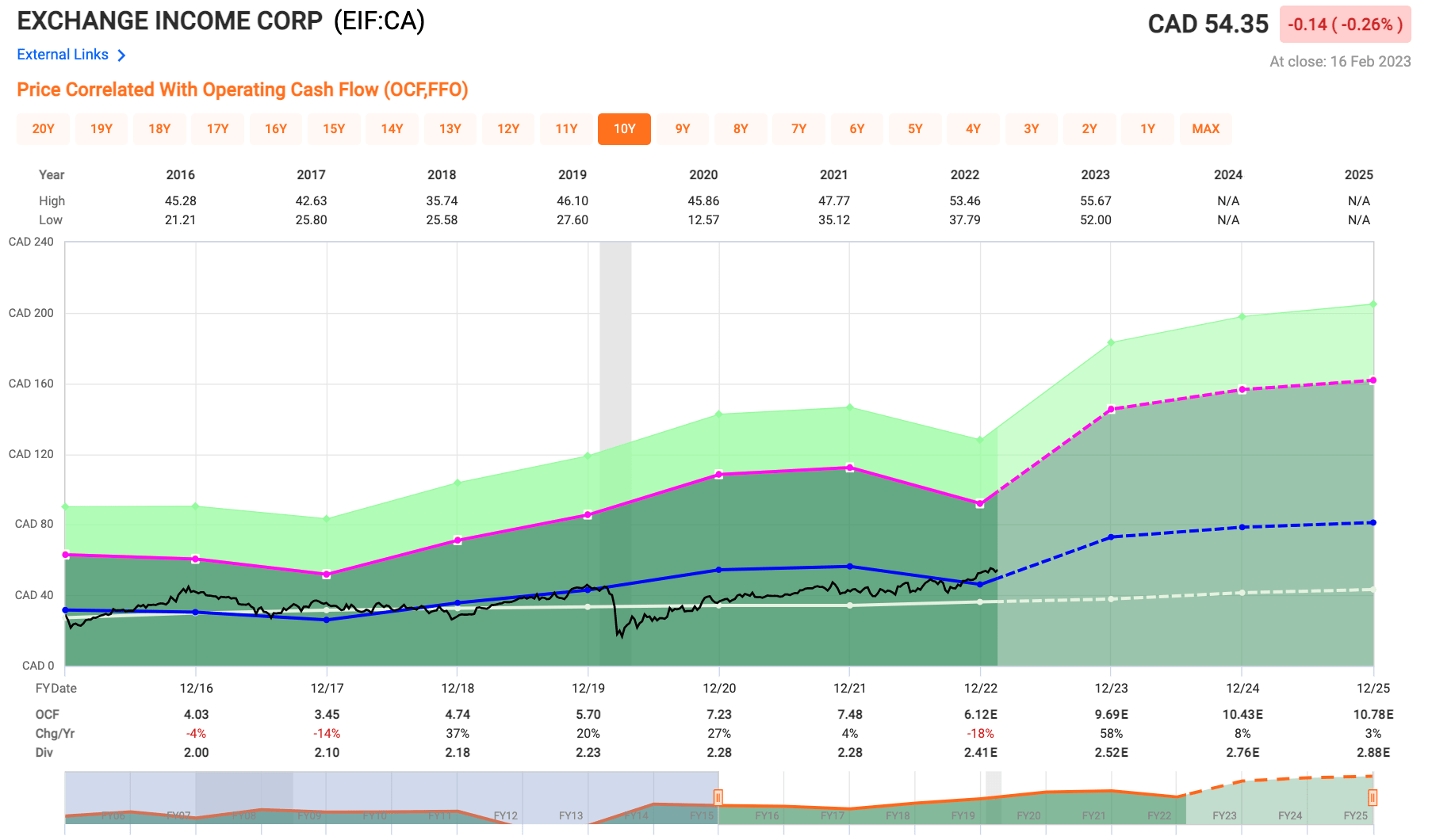

So, let's make something clear here from the get-go and something that will dictate how I write about Exchange Income this year. Because for the first time in over 2.5 years, which is not that far from when I started writing about the company, Exchange Income is actually trading above its 10-year normalized P/FFO level.

More on that later in the valuation section.

For the uninitiated, Exchange Income Corporation is an M&A-focused business with a historical primary focus on aviation, aerospace, and manufacturing. This means there's a certain complexity to understanding the ebbs and flows of the company's P&L because it's cyclical and macro-dependent. It also means that as far as peers go, very few or none actually exist. Comparing this business to anything is a difficult venture at best and a foolish errand at worst.

Instead, we have to look at how the business does in its various segments, then try to compare the segments to macro and to other companies in those segments.

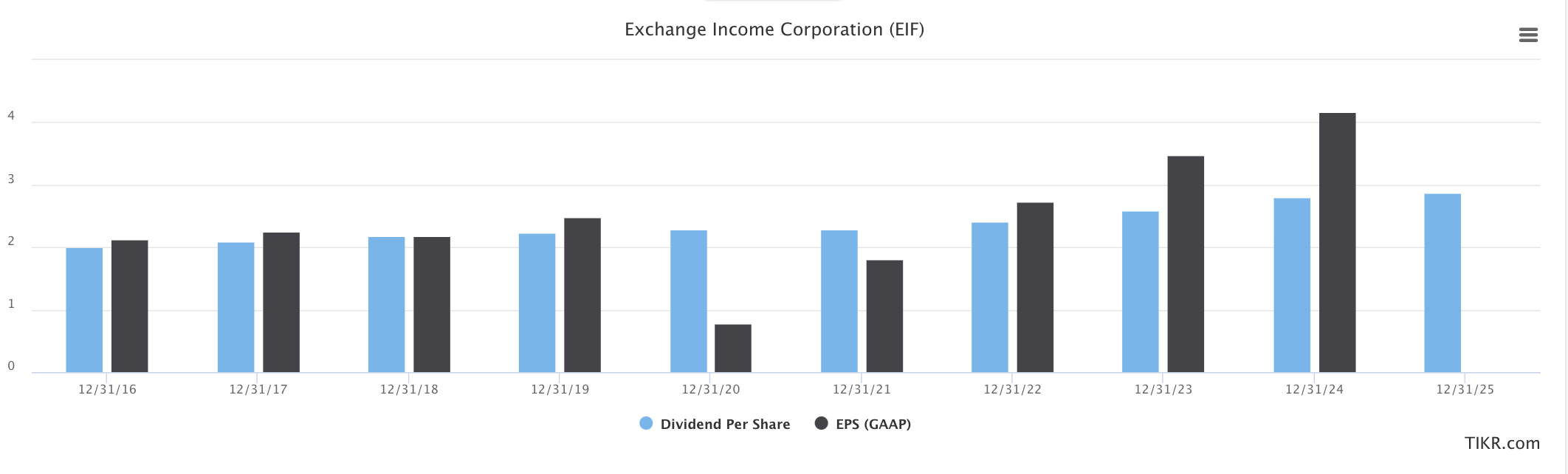

Now, some positives. Exchange has increased the dividend a total of 16 times in 18 years. It has never cut it - not even during COVID-19. While it lacks institutional credit, it nonetheless has a solid financing foundation - many of these positives and numbers are things I go into in my earlier articles on the company, which you can follow.

The company's segments, varied as they are, have been doing well in their own right for the past couple of quarters as well. There have been some sector- and macro-related impacts, but nothing unexpected from the larger perspective given what we're seeing in terms of inflation, the construction sector, and the aviation sector.

4Q22 is out in about a week or so - so I'll likely do a small update to this article at that point if this changes the thesis materially. But I don't expect any massive surprises. As we've seen in the past few quarters, the company is on a growth path with both organic and inorganic growth.

The past quarter of 3Q22 saw some fairly amazing revenue growth - over 40% YoY, but it was still eclipsed by the 58% increase in EBITDA on an adjusted basis, which is among a company record. Despite overall inflationary pressures and other issues. All of the company's positive results contributed to driving the relevant payout ratio metric to less than 55% . For a monthly paying quality company, where my own YoC is almost 9% with the latest dividend increase.

I've seen truly amazing returns from this investment, and current forecasts - both company/management and analyst forecasts, do not suggest that this is going to change anytime soon.

Here are the current analyst forecasts for this particular business.

{kind=link}

As you can see, dividends haven't taken a hit despite lower GAAP, and the future is expecting better GAAP here. There is nothing in the company's recent results, or its forecast that suggests that the company is in for a materially more difficult time. Northern Mat especially has basically been hitting the ground running - as opposed to problems, we're seeing some impressive company execution.

I've been in contact with IR for this company. And what impresses me, for the years I've been covering Mr. Pyle and his team is their almost obsessive focus on getting the right returns on their money. I of course don't know the deals they passed on, or the full extent of their selection process and KPIs when it comes to M&As - what I do know is that almost all of it seems to be working when looking at the bottom line indicators and results. In Europe alone, the company has been scoring contract after contract that will generate long-term returns going into the next decade and more.

The argument against Exchange - or rather, the only one that I've been able to find over the past few years (aside from its size and the aviation/manufacturing sector overall) has been how the company accounts for leases (aviation) and maintenance expenditures. If you're interested in those arguments, the articles on that are still around if you go back a few years on EIF. However, I don't view the points made there as all that valid, and I view the company as being materially different today than it was back then. It's more of a construction/infrastructure mix at this point, compared to what we saw only 3-4 years ago. EIF has really been growing.

I'll be updating where necessary for the 2023E results, but for now, this is where this valuation puts the appeal of the company.

Exchange Income - The valuation is compelling, but it's getting somewhat stretched

So, first a repeat - this is the first time since I started seriously covering EIF, that we're above a 10-year P/FFO average. That in itself marks a bit of a change here because it means that we really want impressive FFO growth estimates from here on out to justify that.

Fortunately, we do have that here, and that makes it easier to justify that I'm still mostly positive. EIF has been a winner for me for years, and the company has delivered TSR of well in excess of 60% for me, with a dependable, high monthly dividend. It's become a bit of a "favorite" for me, and it wouldn't be incorrect to state that I've become somewhat attached to the company.

Dangerous, in more ways than one. So I'm checking my bias here, and making sure that even on today's valuation, there's enough of an upside here to continue to justify holding and potentially buying more of this company.

Even with the dividend increase, the current yield is down to less than 4.7%. This isn't a bad yield per se, it's just very different and much lower from when I bought the company's shares. This graph from F.A.S.T graphs illustrates the change in valuation.

F.A.S.T Graphs Exchange income (F.A.S.T Graphs Exchange income)

{kind=link}

If the company hadn't forecasted a significant change in its operating cash flow going forward, it would be stretched at this point, to the extent that we would want to look at taking home some profits.

Even with those forecasts, it's not an invalid choice to take profits at this point, especially if those returns are high and you can deploy them in cheaper companies. Exchange Income is no longer what I would consider "cheap". The fact that we're above $54 for the native means a very marked change - remember, you could buy this one for under $20/share during COVID-19, and that's what I did.

The underlying case for the growth in FFO is relatively solid. The problem is that the forecast accuracy for how these analysts have been able to estimate this company is low - a negative failure ratio of over 40% on a 1-year basis with a 10% margin of error.

Exchange is starting to show some of the signs I've come to associate with exuberance on a stock. This also includes analysts going higher and higher. Many disliked EIF as an investment when I called for it at $40/share, but they're now calling for it to be worth over $60/share. Why, is my question. Very few new facts have come to light that was outside the realm of forecastability (bullish/bearish theses), and the results we're seeing a well within the realm of my own sensitivity tables.

Rather than being more positive about the company here, I approach this with more care. The conservative upside on an annualized basis is now, as I see it, down to close to 15%. This is still good, and still warrants a "BUY", but it's now based on growth estimates that may not be realized.

My own thesis is that the general direction of the company's earnings will materialize to a degree that makes a double-digit upside possible. I have seen nothing in the latest results, in the current forecasts, or in the macro that suggests we see a material deterioration here. However, because the company depends on a subset of relatively small/nano-cap subsidiaries to generate part of its earnings, the potential for disappointment is very much in there.

For that reason, I'm issuing my first warning that some of the upside may start to be realized at a price close to $55/share native. Still, though - this is my current thesis for the company.

My rating continues to be a "Buy". My own price target, conservative, is $58/share for the Canadian ticker of the shares.

Thesis

My thesis for Exchange Income is fairly simple.

- This is a small operator with a big upside. Fundamentals are solid, and I like their operations and their niche. At an attractive price, and for the right investor, this is a definite "BUY" at a $58 PT. I'm not changing this PT, because I don't see any reason for the time being to adjust it either down or up.

- Risks do exist, but they're on a more subjective and "what-if" level, with very few actual logical risks to the company's balance sheet or operations.

- My stance is a "Buy", but at this level, we're getting pretty close to the company being fully valued.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

EIF is no longer cheap, but it's still solid here.

For further details see:

Exchange Income Corp.: One Of My Favorite Monthly-Paying Companies For 2023