EIFZF - Exchange Income Corporation: Poised For Growth With Growing Aviation Demand And Strategic Initiatives

2023-12-27 11:35:28 ET

Summary

- Exchange Income Corporation is a diversified company focused on aerospace and aviation services and manufacturing.

- Past and current revenue growth is strong, growing by double-digit rates.

- Despite some contractions in gross profit margin, it has maintained stable bottom-line margins through effective expense management.

- EIF:CA's recent bought deal has raised capital for investment in growth initiatives, aligning with the projected increase in global aviation demand.

- Despite being smaller than its competitors, it outperformed them in terms of forward revenue growth outlook. In addition, with double-digit upside potential, it further supports my buy recommendation.

Synopsis

Exchange Income Corporation ( EIF:CA ) is a diversified, acquisition-oriented company focusing on aerospace and aviation services, as well as manufacturing.

EIF:CA's historical financials reveal robust revenue growth. Despite contractions in the gross profit margin, the company has maintained stable bottom-line margins, primarily through effective expense management. Additionally, EIF:CA's debt level has been stable, resulting in consistent interest expenses over the years.

The company's recent bought deal, while diluting its outstanding shares, has raised capital for investment in growth initiatives anticipated to fuel long-term growth. This strategy aligns well with the projected increase in global aviation demand, positioning EIF:CA favorably to capitalize on this growth. Based on its financial strength and growth catalyst, I am recommending a buy rating for EIF:CA.

Historical Financial Analysis

For the last four years , EIF:CA’s revenue growth has been on a recovery path, and it is accelerating. In 2018, it grew ~11.47%, but by 2022, it grew ~45.73%, more than double 2021’s ~22.92%. However, in 2020, its revenue declined ~14.29% due to the COVID-19 pandemic, which dampened demand for air travel and aircraft production due to travel restrictions and required quarantine periods.

Author's Chart

In terms of profitability, it is performing well on the bottom line, although I do notice a slight gross profit margin [GPM] contraction. In 2019, GPM was ~39.73%, but by 2022, it had contracted ~5.2% to ~34.53%. Despite the GPM contraction, its operating income margin [OIM] and net income margin [NIM] remained stable throughout the years, except for 2020, which was impacted by COVID-19. In fact, after 2020, both are recovering and growing, almost reaching 2019 levels.

Author's Chart

Based on the following chart, management did an excellent job managing the company’s SG&A expenses. In 2019, it accounted for ~15.22% of total revenue, but by 2022, it had contracted to ~12.36%. This contraction in SG&A expenses is enough to offset the negative impact of GPM contraction, hence allowing the company to protect its bottom-line margins. I love the fact that it is able to reduce SG&A while at the same time growing its top-line revenue at double-digit rates. This really speaks volumes regarding its products and services’ branding strength and demand.

Author's Chart

In terms of debt level, its balance sheet looks extremely healthy, with the debt-to-equity [D/E] ratio remaining very stable throughout the four years. It hovers around the range of ~51%. As a result of its healthy and stable debt levels, its interest expense as a percentage of revenue is also relatively stable at ~3 to 4% over the last four years, and it is not showing any signs of deterioration that would trigger insolvency risk.

Author's Chart Author's Chart

Analyzing EIF:CA’s 3Q23 Results - Is It Continuing With Its Strong Past Performance?

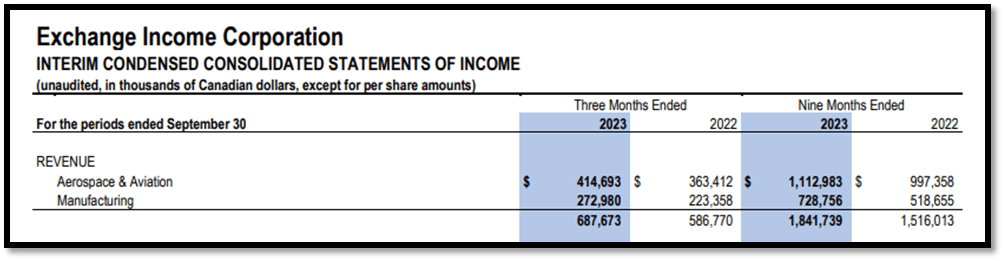

EIF:CA reported extremely strong 3Q23 results. Its revenue grew ~17% year-over-year to ~$688 million, up from the previous period’s ~$587 million. EIF:CA’s revenue can be broken down into two segments: aerospace and aviation [A&A] and manufacturing. For its A&A segment, management stated that this segment grew because of its previous investments to increase the capacity of both fixed-wing and rotary-wing aircraft. These expansion investments translated into higher returns as passenger volumes bounced back, surpassing historical levels. In addition, the A&A segment also experienced strong growth in charter, fire suppression, and rotary medevac revenue because of the investments. As a result of the strong growth in A&A, it supported and contributed to 3Q23's top-line revenue growth.

For its manufacturing segment, management’s strategic decision to acquire both Hansen Industries and BVGlazing also supported its robust revenue growth for the quarter as the acquisitions expanded its market reach and also enhanced its product and service offerings. Additionally, the Multi-Storey Window Solutions business within this segment witnessed an increase in window manufacturing due to a normalization of the production schedule, thus driving revenue growth at the consolidated level for the quarter.

Apart from revenue growth, it is crucial to analyze profitability as well, and to do so, I will look at its NIM for the quarter. 3Q23 reported a lower NIM of ~7% vs. 3Q22’s ~8%, but the contraction is minimal. When I look deeper into its 3Q23 P&L, it is clear that manufacturing expenses as a percentage of revenue increased year-over-year, which offset the decrease in both A&A and general and administrative expenses. As a result, margins for the quarter contracted slightly.

On a 9-month basis, NIM’s contraction is barely noticeable and has remained relatively stable at ~5%. This is because, on a 9-month basis, A&A expenses’ contraction is much more significant and is able to better offset the impact of rising manufacturing expenses. In terms of general and administrative expenses, it contracted slightly as well. Overall, its bottom line looks really stable and robust. Therefore, for the foreseeable quarters ahead, I expect it to maintain its current strong margin levels.

Author's Chart Author's Chart

EIF:CA’s Bought deal Will Drive Growth

Back in June, it announced the completion of its bought deal public offering. As a result of this deal, net income on a per share basis decreased ~12% year-over-year due to the dilution of common shares outstanding. Despite these drawbacks, the capital raised through this deal will be used on growth initiatives that will drive long-term growth.

One of the growth initiatives that was announced is regarding a contract with Air Canada. This contract involves providing regional airline services, which is a key area of EIF:CA’s expertise. The returns from this investment are expected to start materializing in the latter part of 2023. Hence, moving forward, I anticipate that this Air Canada contract will bolster its revenue from 2023 onwards.

Quote : “The financial effects of such contracts will have significant positive effects in subsequent quarters, as we have previously discussed.”

In addition to this, it has also secured medevac contracts with the provinces of British Columbia and Manitoba. These contracts, which are in line with its core competencies in medical evacuation and scheduled flying services, represent long-term engagements, and I anticipate that they will also contribute to its long-term revenue growth, together with Air Canada’s contracts.

Despite the dilution caused by the bought deal public offering, I believe the benefits outweigh the drawbacks. In the short term, shareholders will definitely feel pinched, but in the long term, this capital allows EIF:CA to continue growing. In my previous section, where I analyzed its past and current financial performance, it was clear that management is highly skilled and is making all the right decisions, as they are consistently growing the business revenue at double-digit rates. In addition, margins were very robust, and this was done through effective expense management. Debt levels and interest expenses are managed well also. All of these give me a lot of confidence in the management’s capabilities, and I believe they will deploy the capital raised through the deal carefully, ensuring that it does not destroy value.

Growth in Aviation Demand Will Support EIF:CA’s Growth

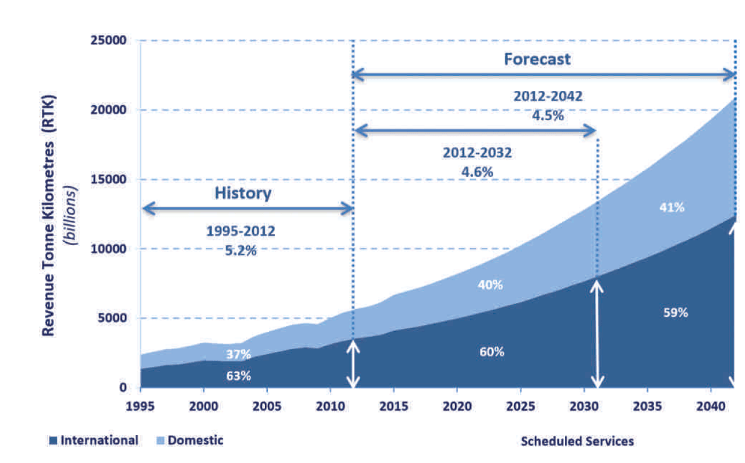

Based on the following chart by the International Civil Aviation Organization [ ICAO ], the aviation market is expected to continue growing robustly. From 2012 to 2032, the CAGR for air transport demand is ~4.6%. For 2012 to 2042, it is also in line at ~4.5%. In short, the A&A segment is expected to continue growing for the next 20 years, and it will grow fast. This growth will provide ample opportunities and also provide a tailwind for EIF:CA to grow its business as well.

{kind=link}

Based on its P&L, it's clear that A&A holds more weight in its total revenue. For both 3Q23 and 9M23, it accounts for ~60% of total revenue. Therefore, I believe the anticipated strong growth in global air transport demand will drive EIF:CA’s future revenue even higher.

{kind=link}

Comparable Valuation Model

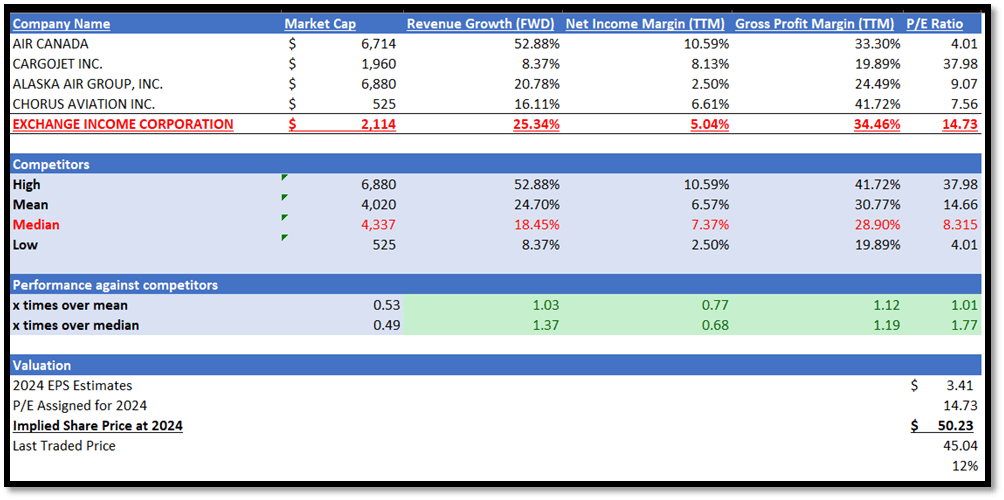

In my comparable valuation model, I will attempt to walk you through the metrics I will be using. I will be comparing EIF:CA’s with its competitors in terms of market size, profitability, and forward P/E ratio. In terms of market size, EIF:CA’s market capitalization is ~$2.1 billion vs. competitors’ median of ~$4.3 billion. This means that EIF:CA is only 49% of their median size.

Despite being half their size, it outperforms them in terms of forward revenue growth outlook. EIF:CA’s forward revenue growth is 25.34% vs. competitors’ median of 18.45%. This means that it is 37% higher than its competitors.

In terms of profitability, it outperformed them in terms of GPM TTM. It has a GPM of 34.46% vs. competitors’ median of 28.90%, 19% higher than them. When it comes to NIM TTM, it trails slightly behind them at 5.04% vs. competitors’ median of 7.37%. Overall, given its size, these performances are outstanding, given that its lack of size means it does not have as large of an economy of scale to begin with.

When I look at its P/E vs. competitors’ median, it raises the concern of overvaluation. However, when I look at EIF:CA’s 1-year average P/E trend, its current 14.73x is actually below it. In addition, it has a much higher revenue growth outlook than its competitors, while NIM is almost in line despite its smaller size. Therefore, these factors support its current P/E ratio that is assigned by the general market, and I find it to be justified.

{kind=link}

{kind=link}

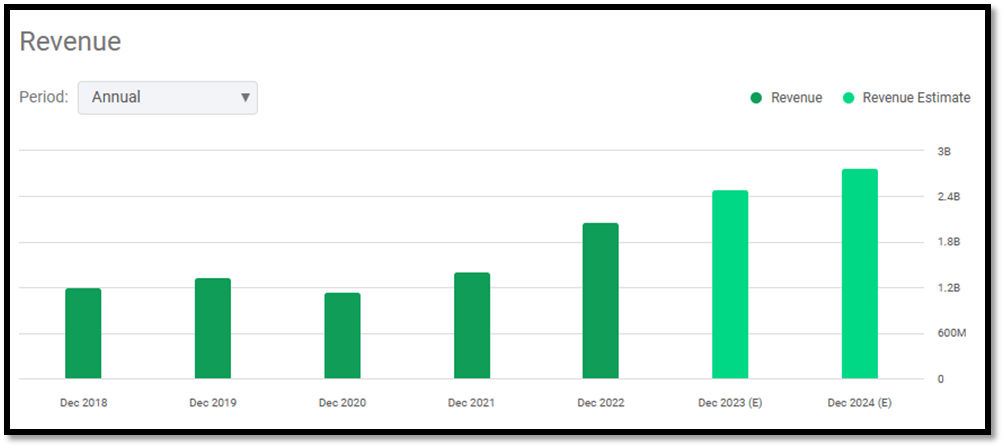

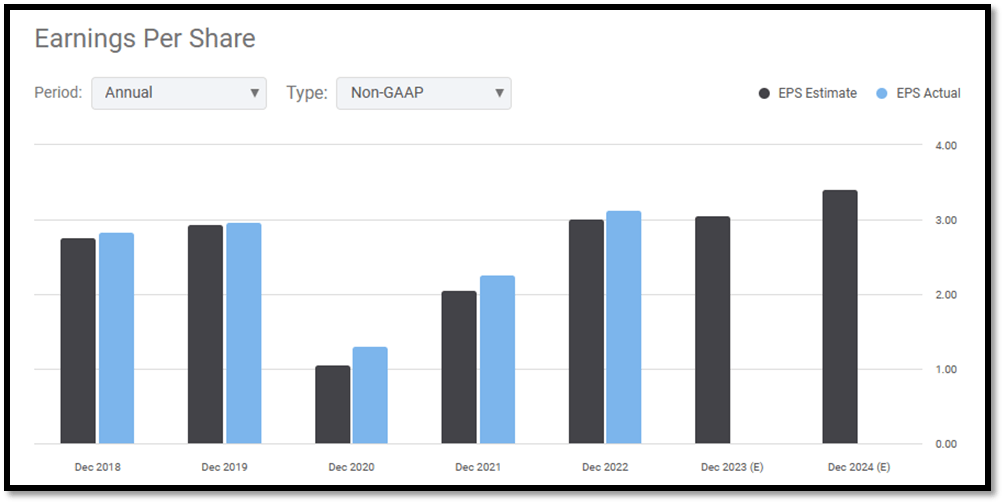

The market revenue estimate for EIF:CA is expected to reach $2.49 billion in 2023 and $2.78 billion in 2024. Moving onto EPS, the market estimate for EIF:CA’s 2023 EPS is $3.06 and $3.41 for 2024. Based on my discussion of its financial strengths and growth catalysts above, I believe these market estimates to be justified and reliable. By applying its current P/E, which is more on the conservative side, to its 2024 EPS estimates, my 2024 price target is $50.23, and this represents an upside potential of ~12%.

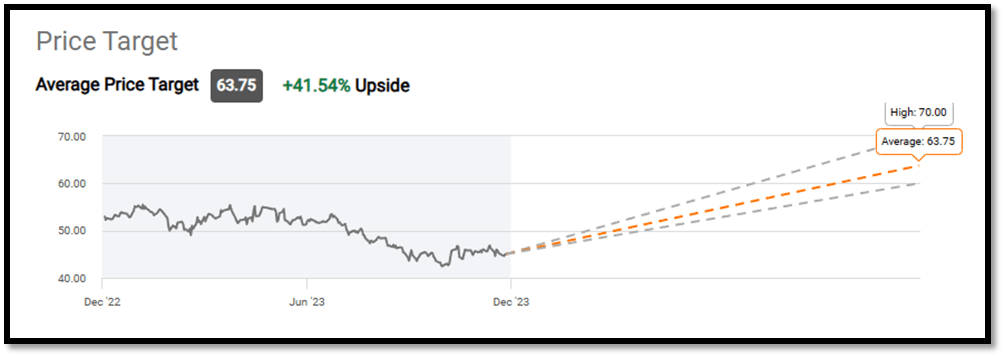

In addition, Wall Street’s target price is $63.75, higher than my personal target price. This comparison serves as a check and balance for my valuation, ensuring that it is reasonable and conservative. Therefore, I believe my target price is well grounded and reasonably justified.

{kind=link}

{kind=link}

{kind=link}

Downside Risk

One downside risk associated with EIF:CA would be rising manufacturing expenses. As stated by management, pricing and demand for its manufacturing segment have moderated from the previous period’s high, and it is now moving towards normalized levels. Therefore, prices for its products in this segment are expected to come down.

In addition, as mentioned above, its manufacturing segment also acquired two companies. While they boost revenue, they would also naturally increase operational and integration costs, which contributed to the overall increase in manufacturing expenses for the quarter.

A combination of lower prices and increased costs would put pressure on its net margins. As I have discussed, its NIM margin is trailing its competitors. Any further compression might lead to share price depreciation.

Conclusion

Over the past four years, EIF:CA has shown robust revenue growth, with growth mostly at double-digit rates. Although GPM did contract over the years, its OIM and NIM remained robust due to its effective expense management. Its debt has been stable as well, resulting in consistent interest expense, and I do not foresee any risk arising from it. For its latest 3Q23 earnings results, it continues to show robust revenue growth and bottom-line margin. Thus, reflecting the robustness of its business model.

Although the bought deal public offering has diluted shareholders, the capital raised will be invested into growth initiatives that will drive long-term growth. This strategic decision ties in well with the anticipated growth in global aviation demand. The aviation sector is anticipated to continue growing for the next two decades. The capital raised through the deal positions it well to capture growth in this area.

When I compared EIF:CA against its competitors, it revealed that it outperformed them in terms of growth outlook despite being half their size. Although NIM trails behind them, it is minimal. My conservative valuation model indicates a double-digit upside potential for EIF:CA, which is conservative when compared to Wall Street's estimates. Therefore, I am recommending a buy rating for the stock.

For further details see:

Exchange Income Corporation: Poised For Growth With Growing Aviation Demand And Strategic Initiatives