NDAQ - Exchanges If You Don't List You Don't Matter

2024-01-17 04:48:06 ET

Summary

- Electronic trading has significantly reduced the cost of matching buyers and sellers.

- Yet, the proliferation of multiple stock exchanges owned by a single firm has created inefficiencies and hindered competition.

- The introduction of a new exchange, ENEX, that focuses on the needs of investors could improve market structure and reduce trading costs.

Introduction

The effects of the introduction of electronic trading are overwhelmingly beneficial. But anything can be further improved. This post identifies the pros and cons of the existing market structure. It then proposes an improvement that shifts the focus to exchange new issues and trading structure to better serve the needs of investors.

The effect of electronic trading on cost

Back when exchange trading was by voice, the cost of matching buyer with seller was a substantial share of total transaction cost. The rest, the cost of clearing (transfer of possession), was also significant and remains significant today. However, clearing is separate from matching and less visible to investors. The result is that overpriced securities market clearers are getting away with murder.

The change to electronic trading dramatically reduced the cost of matching to the point where everyone and his brother were adding a matching platform to services. As the cost of matching fell, the prospect of creating a matching platform was no longer daunting. The predictable result was platform proliferation - over 15 SEC-approved stock exchanges and any number of dark pools - matching platforms not SEC-approved for exchange designation. Most major broker-dealers have at least one dark pool. As of December 2022, there were close to 70 dark pools.

This development brought the issue, “How many exchanges is the ideal number?” to the fore. The ideal is many fewer than the current number. One obvious inefficiency is the purported “competition” between multiple exchange subsidiaries of a single firm. The exchange parent firms, call them exchange management firms (EMFs), own multiple exchanges, all trading the same securities. The big EMFs are the Intercontinental Exchange (ICE), Nasdaq (NDAQ), and CBOE Global Markets (CBOE). Of course, multiple exchanges owned by a single firm are not there to compete but to add to EMF profits at the expense of the rest of the market.

How did this nonsense happen? It was a negative by-product of electronic trading. Electronic trading took the speed of matching from minutes to the speed of light. That meant that a computer loaded with programs called algos, when located at the same spot - colocated - as an exchange transaction platform could execute a trade with one exchange, and an offsetting trade with another, at a speed thousands of times faster than the speed with which a human could execute that same trade.

There were good outcomes and at least one bad outcome of electronic trading. The good outcomes included speedier matching and dramatically lower matching costs. The bad outcome was that humans placing market orders could no longer rely upon trading at the price shown on their computer screens. The price could change hundreds of times before the order reached the broker’s chosen exchange.

Speed excluded investors from insider price access.

The disastrous result of extreme matching speed was two kinds of investors - insiders (colocated traders now called high-frequency traders (HFTs)) and outsiders (investors not colocated). This was problematic for the Securities and Exchange Commission ((SEC)) because the SEC is responsible for seeing that brokers show investor-outsiders the best prices market-wide, called the National Best Bid and Offer ((NBBO)).

The rule that requires brokers to provide investors with prices no worse than the best bid or offer turns out to be unenforceable in a world where HFTs rule the inside market. By simply waiting for the exchange prices to travel to the SEC computer, the SEC provides the marketplace with obsolete prices.

The evolution of insider trading

The effects of the use of algos to arbitrage (to simultaneously buy and sell an asset in different markets) to exploit the price differentials between exchange-traded securities unfolded gradually. The first result was the desired explosion of HFT arbitrage profits. Then as exchanges got wise, two lucrative opportunities appeared. First, EMFs added as many new exchanges as the SEC allowed, buying up SEC-approved dormant regional exchanges that had become obsolete. Then, the EMFs got greedy. They realized that they could capture much of the HFTs’ profits for themselves by increasing colocation fees.

But never worry about the profitability of the dealer-HFTs. When the exchanges took the profits from interexchange arbitrage for themselves, the HFTs, always resourceful, found a new way to leverage their insider status.

Thus, dealer-insiders turned away from the HFT business and toward the exploitation of investors-outsiders. It was the broker-dealers’ good fortune that the investors’ brokers were being squeezed to reduce the commissions they charge by the new market entrant, Robinhood (HOOD).

In an epic game of Three-Card Monte, the former HFTs changed their spots. They offered to pay the brokers for their unfilled investor orders - an arrangement called payment for order flow ((PFOF)). Most brokers then eliminated their commissions in favor of PFOF but continued to thrive by receiving PFOF from former HFTs, now known as Wholesalers, hiding most of the cost of investor transactions.

Wholesalers replaced their HFT arbitrage profits with the spread between under-market investor prices and better inside prices. The result was a regression of investors’ market access from the tight inside price access at the advent of electronic pricing to the least access, OTC (over the counter) trading. As when 19 th century investors visited a broker’s shop to buy shares on display behind his counter. Once over the counter was just that.

New exchange value added

Is there a way to combine the futures markets’ strengths with securities exchange capacity to increase the capital stock? Yes. Wiser exchanges will crush the Wholesalers by finding a way to add greater value, snatching the lion’s share of value-added. But only something more original, more difficult to imitate, can separate a new exchange from the pack.

Historically, the most reliable source of exchange value added is new listings. The value added by an IPO is the promotion of new issues. Promotion of new issues, however, is never going to be the rock upon which a new exchange is built.

Origination is the road to successful market entry. However, forget about simply promoting IPOs. The NYSE and NASDAQ have tied up IPOs, as new outsider exchanges such as Investors Exchange ((IEX)) and Long-Term Stock Exchange ((LTSE)) have realized regretfully.

But there are other ways to introduce new issues. A better example of new issue success is that of futures exchanges like CME Group (CME). Financial futures match the prices of investments rather than the investments themselves. The futures markets’ many relative strengths:

-

The ability to add a listing at will.

-

The ability to close the door on arbitrage. Other exchanges must list their own version.

-

A listed contract cannot be traded OTC.

-

The listing exchange is the sole and necessary clearing counterparty.

-

Secure inexpensive clearing.

-

The exchange is not hostage to listers.

The weakness of futures trading is its insignificant function. Rather than increasing the capital stock as securities IPOs do, futures only provide a way to place a wager on the future value of a commodity price or a financial index.

Through expanding exchange capabilities to include more than simple matching as both futures and securities exchanges do. There are at least three changes that would put a new exchange (or new component of an existing exchange) into a favorable competitive position.

- Listing new instruments that focus on the needs of investors.

- Combine the best aspects of futures trading technology with the best aspects of securities trading.

- Improve existing investment alternatives.

How would the new exchange operate?

Daily transactions

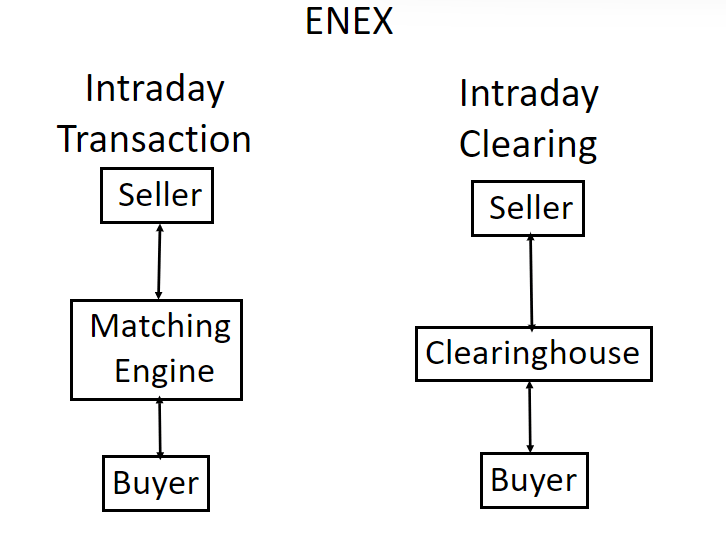

Below is a description of a new exchange called ENEX that combined the advantages of futures trading with the value added of the futures market.

Intraday trading and clearing (Author)

{kind=link}

The graphic above displays the structure of daily operations of the new exchange (call it ENEX).

-

Intraday transactions are no different from those of any other securities or futures exchange.

-

Intraday clearing places an exchange clearinghouse between buyers and sellers at the close of trading (ala futures).

This futures market method cuts clearing costs and increases safety by providing both buyers and sellers with a clearinghouse counterparty not exposed to market risk.

ENEX improvements.

-

Change its focus from issuers to investors. To attract investor interest, list securities that will focus on investors’ needs. The existing EMTs already list securities that appeal to listers. ENEX, by virtue of its independence from IPO issuers, would naturally have a greater interest in attracting investors.

-

Change its operating procedures.

-

Origination . If origination is the key to ENEX's success, origination must provide most of ENEX’s value added.

-

ENEX may borrow procedures from other financial structures such as that of an ETF, but it may apply them to other problems.

-

One financial problem that ENEX might tackle is the replacement of the now-defunct Eurodollar futures market.

-

Intraday trading and clearing . ENEX could borrow intraday trading and clearing operations from futures exchanges.

-

Final settlement. One aspect of futures trading that futures exchanges have not resolved is final settlement or delivery. Current issues (or contracts in the language of futures market) are settled

-

By requiring sellers to buy the “physical” spot market issue, and then transfer it to buyer using the spot market settlement mechanism.

-

Or by paying the spot value of an index.

-

This settlement method is expensive. It may be why the futures markets fail to provide investments to investors.

Conclusion

The superfluous exchanges and their owners, the exchange management firms, can be killed off in the heat of real competition from a new exchange, ENEX. ENEX can succeed by focusing on the needs of investors instead of issuers. Investor trading costs will decline while securities prices will rise, and market risk will fall.

For further details see:

Exchanges, If You Don't List, You Don't Matter