EXEL - Exelixis: 2024 Looking Good In The Mid-Term

2024-01-18 00:50:47 ET

Summary

- Exelixis recently reported solid but not stellar 2023 financial results and provided guidance for 2024.

- The company expects a 2.5% increase in revenues from 2023 to 2024, with reductions in expenses.

- Key priorities for 2024 include corporate restructuring, share buybacks, label expansion opportunities, and advancing clinical-stage assets.

This is my third Exelixis ( EXEL ) article after downgrading it from "BUY" to "HOLD" in 08/2023's "Exelixis: Predominantly Single Molecule Cancer Franchise". In this article, I review its investment prospects following its 01/08/2024 presentation (the " Presentation ") at the 42nd Annual J.P. Morgan Healthcare Conference and its 2024 guidance.

Solid but not stellar, best characterizes Exelixis 2023 results

On 01/07/2024 in advance of its 01/08/2024 Presentation at the J.P. Morgan Healthcare Conference, Exelixis reported :

- preliminary 2023 financial results and 2024 financial guidance; and

- an outline of key priorities and milestones for 2024.

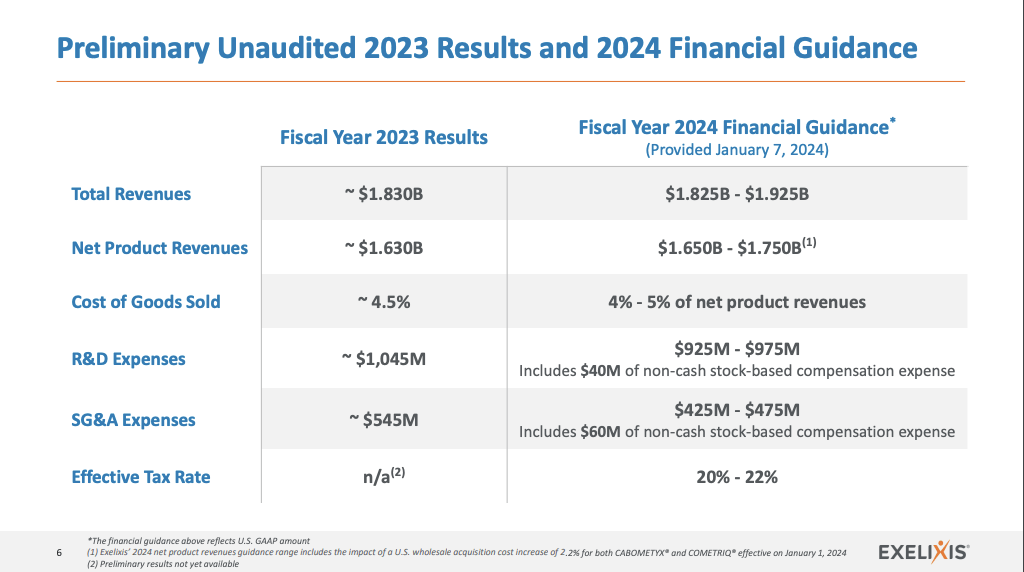

Presentation slide 6 assembles and reports Exelixis' 2023 results and 2024 guidance as follows:

{kind=link}

Seeking Alpha

A review of the product revenue excerpts below from Exelixis' latest 10-K puts the above figures in context:

Seeking Alpha

Total revenues grew 12% from 2021 to 2022. They are preliminarily pegged for a comparable ~12.7% jump from ~$1,611 billion to $1,830 billion as 2022 moves to 2023. The percentage increase from preliminary 2023 revenues of $1,830 billion to the $1,875 midpoint of the guided revenues for 2024 is ~2.5%.

This slowdown in guided total revenue growth is discouraging. On a positive note, management is guiding for nice reductions in both SG&A and R&D expenses. The midpoint of combined R&D and SG&A-guided 2024 expenses are $1.4 billion compared to $1.59 billion combined in 2023 for a savings of $0.19 billion.

Key priorities and milestones for 2024 are limited in terms of near-term catalysts

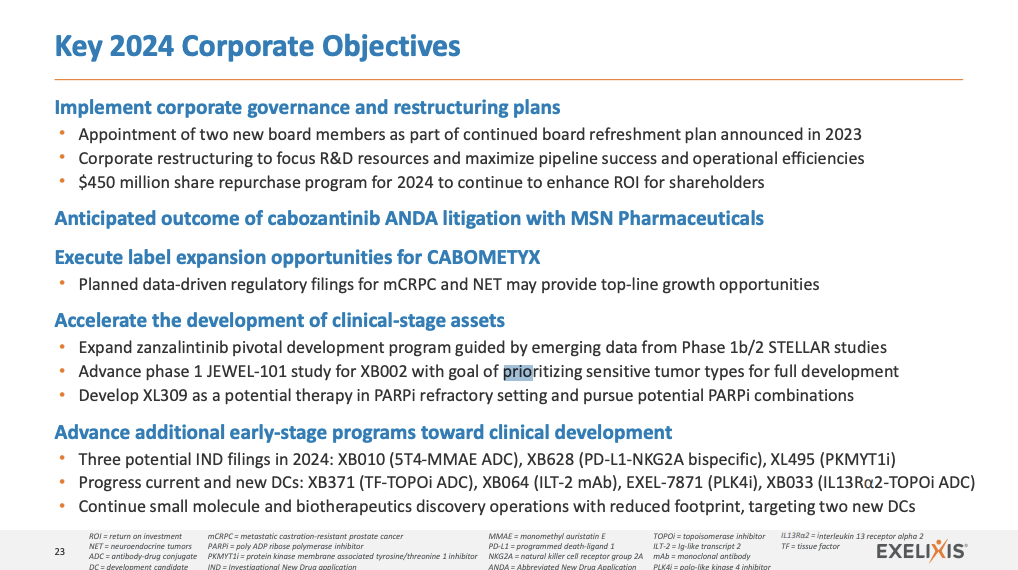

Presentation slide 23 below sets out Exelixis' key 2024 corporate objectives:

{kind=link}

Seeking Alpha

These include 5 separate areas as highlighted in blue above.

The first of these five has two items of near-term interest — corporate restructuring and share buyback. The corporate restructuring explains the R&D and SG&A expense reductions referenced above. The $450 million share buyback follows a $550 million program which was completed as of YE 2023 per slide 7 of the Presentation.

During Q3 it repurchased $280 million of Exelixis shares at an average price of $20.35 as stated in the Call. As I write on 01/16/2024 its shares are trading at $22.48. The Call provides the latest intel on Exelixis' liquidity which it listed at $1.9 billion. It characterized this as ample to:

- invest in internal discovery activities;

- pursue external business development opportunities;

- expand its pipeline, and

- allow it to return capital to shareholders through the $550 million repurchase and presumably its new $450 million program for 2024.

The second item of the 5 in blue refers to its ongoing litigation with MSN Pharmaceuticals. This complicated litigation addresses MSN’s proposed generic cabozantinib product (Abbreviated New Drug Application [ANDA] No. 213878) alleged as infringing Exelixis' patent estate.

The details and likely expected outcome of this dispute are beyond my expertise. In the Call, CEO Morrissey advised that the trial had been recently completed. He declined to comment beyond this advice. I would note that MSN is not the only one to seek an ANDA.

In 07/2023 Exelixis filed a settlement with Teva ( TEVA ) in resolution of its ANDA to market a generic version of CABOMETYX tablets. The settlement gave Teva a license to market its generic version of CABOMETYX in the United States beginning on January 1, 2031.

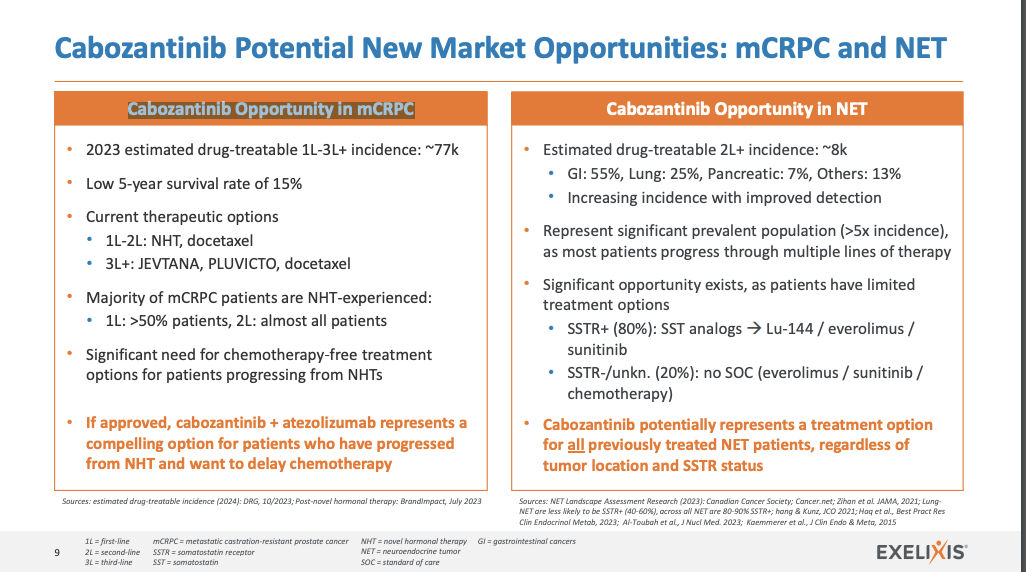

Back to the list of five key objectives in blue above, item 3 addresses label expansion opportunities for CABOMETYX. This is obviously something of major importance for anyone, such as myself, on the lookout for near-term catalysts. It goes on to point out planned data-driven regulatory filings for mCRPC and NET as potentially providing top-line growth opportunities.

No dates are included here. Presentation slide 24 implies that it is directed to 2023. Of course, as I write in 01/2024, 2023 has come and gone with no filing. Presentation slide 9 below is focused directly on Cabozantinib opportunities in mCRPC and NET:

{kind=link}

Seeking Alpha

It offers nothing of substance in terms of a filing timetable. The Call is more helpful but lacking in specifics. It referenced these two as Exelixis' most mature prospects. CMO Peterson advised:

... In late August, we announced positive top-line data from not one, but two phase 3 CONTACT-02 which evaluated Cabozantinib plus atezolizumab in patients with Metastatic Castration-Resistant Prostate Cancer, or mCRPC, and CABINET, which evaluated Cabo in patients with pancreatic or extra pancreatic neuroendocrine tumors. I'll begin briefly with CONTACT-02. This is a randomized open-label study of Cabozantinib plus atezolizumab versus second novel hormonal therapy, or NHT, in patients with mCRPC. This study has multiple primary endpoints of both PFS and OS. PFS is determined by blinded independent central radiology review and per-resist 1.1 So, for example, progression by PSA only was not considered a PFS event to best informed an endpoint. Eligibility was restricted to patients with measurable disease. That is, bone-only, non-measurable disease was not allowed.

She went on to state that when the OS results become more mature it will consider a regulatory submission as it consults with the FDA. When will such a submission actually take place? Not soon enough for investors to consider them in any way imminent. I expect management will be more forthcoming in future quarters when it can set its bead on a specific date. Until then I measure them of minor near-term significance.

Conclusion

With its most mature pipeline asset in an uncertain position timewise, I expect that Exelixis is in for several years of tepid growth. Its shares may well face significant disruption as the MSN litigation results come in. Similarly, if it has good news on the filing front for NET or mCRPC, shares may get a bump.

Otherwise, I expect Exelixis in 2024 to move with the market. I rate it as a "Hold".

For further details see:

Exelixis: 2024 Looking Good In The Mid-Term