EXEL - Exelixis: Building On A Blockbuster

Summary

- Exelixis' CABOMETYX is hitting on all cylinders.

- Exelixis has an interesting and highly cabozantinib-centric pipeline.

- Pharma BD is a tricky process that will play a big role in Exelixis' future.

This is my first look at Exelixis ( EXEL ). It is a young commercial stage biopharma that is enjoying success with its CABOMETYX (cabozantinib). In this article, I evaluate Exelixis' investment merits as it both enjoys and struggles with its growing CABOMETYX blockbuster.

CABOMETYX has enjoyed strong revenues over the years

As a newcomer to Exelixis, I am impressed by its CABOMETYX success described in Exelixis' Q3, 2022 earnings call (the " Call "). During Q3, 2022 it generated net product revenues of $497 million for Exelixis and its partners.

The FDA approved CABOMETYX in an expanding group of indications tracing back to its first 04/2016 approval in treatment of advanced renal cell carcinoma. Four additional indications were added over the years including:

- 12/2017 first-line treatment of advanced renal cell carcinoma;

- 01/2019 previously treated hepatocellular carcinoma;

- 01/2021 in combination with OPDIVO in first-line treatment of advanced renal cell carcinoma;

- 09/2021 treatment of locally advanced or metastatic differentiated thyroid cancer ((DTC)).

CABOMETYX was a second comer to market in terms of Exelixis' earlier development of its productive cabozantinib molecule. As disclosed by its 2020 10-K ( p. 2) back in 2012:

...COMETRIQ, our first marketed cabozantinib product, was approved by the FDA on November 29, 2012, for the treatment of patients with progressive, metastatic MTC, and in March 2014, the EC granted COMETRIQ a conditional marketing authorization for the treatment of adult patients with progressive, unresectable locally advanced or metastatic MTC.

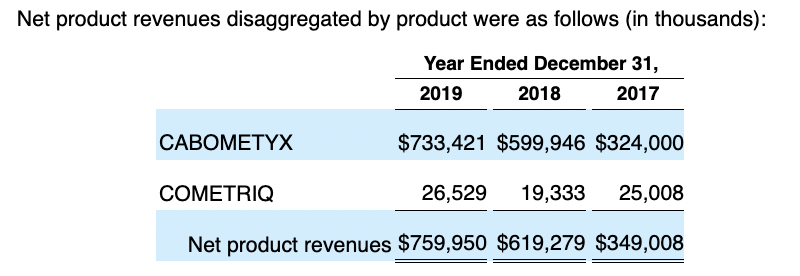

Per its 2014 10-K , Exelixis' first year with net product revenues was 2013 when it received ~$15 million from the sale of COMETRIQ (p. 48). Judging by the excerpt below of Exelixis' disaggregated net product revenues for years 2017-2020 (2020 10-K, p. 87), COMETRIQ revenues have always been modest and have never come close to matching CABOMETYX:

{kind=link}

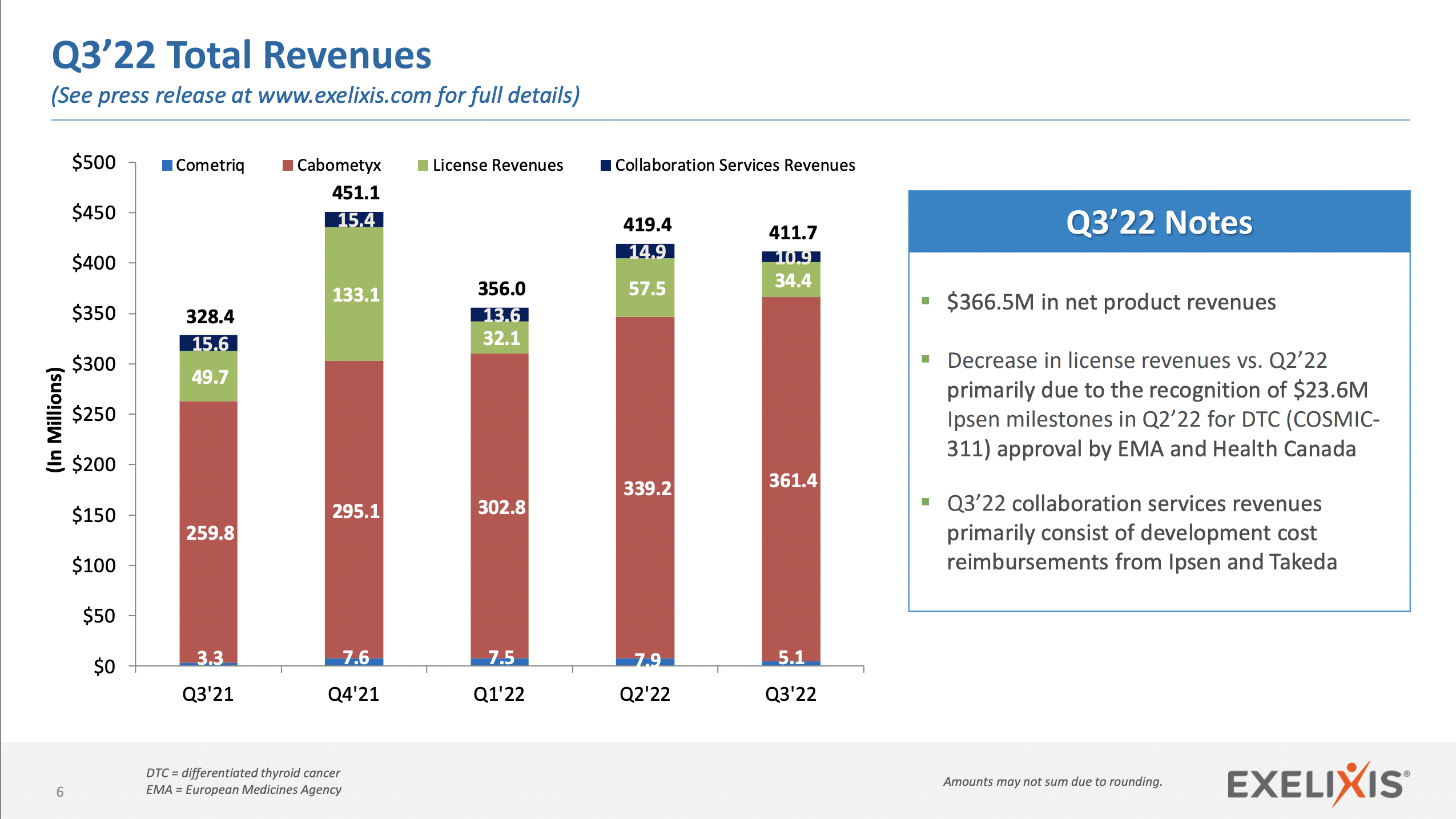

The slide below from Exelixis' Q3, 2022 earnings presentation provides the latest available picture of COMETRIQ/CABOMETYX revenues:

{kind=link}

Exelixis' pipeline coupled with its development resources bode well for its future.

Typically it is easy to get a handle on a company's pipeline. For Exelixis this is less the case than normal. Its website contains no page devoted to a discrete pipeline of molecules targeting specified disease states at various stages of clinical development.

It does include a drop down menu with an entry for "pipeline" under its "Research and Development" heading. Clicking this entry offers several options, including:

- Pipeline Overview

- Early-Stage Compounds

- Cabozantinib Pipeline

- Other Partnered Programs

- Clinical Trials

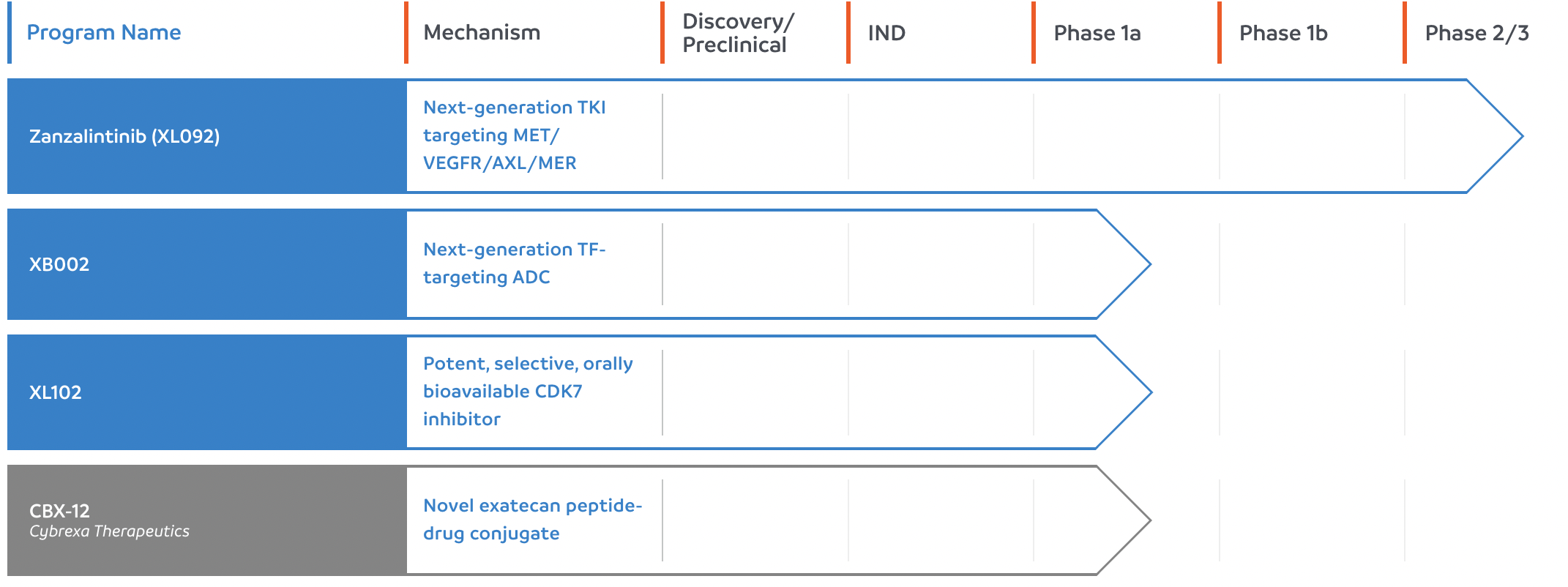

Entries 2 and 3 deliver conventional pipelines as follows. 2. Early-Stage Compounds includes the graphic excerpt below with its four early stage molecules that have reached clinical development:

{kind=link}

It also includes ten programs that have yet to reach the clinic.

Exelixis' 3 Cabozantinib Pipeline lists an incredible array of 69 cabozantinib programs. The majority of these are investigator sponsored . Thirteen are listed as being in Collaboration with NCI’s Cancer Therapy Evaluation Program. A dozen of them are sponsored by Exelixis. Two by Roche ( RHHBY ) and one by Bristol Myers Squibb ( BMY ).

Six of these are phase 3 cabozantinib combination trials with various of the sponsors. There is also a seventh phase 3 trial sponsored by Exelixis assessing cabozantinib compared to placebo in treatment advanced neuroendocrine tumors after progression on Everolimus.

Pipeline entries 1, 4 and 5 lead to prose descriptions that defy ready summarization. Entry 1 includes a "Pipeline Overview" which calls out molecules otherwise discussed. Entry 4 calls out two molecules including:

- Cobimetinib, an Exelixis-discovered reversible inhibitor of MEK, part of the RAS/RAF/MEK/ERK pathway that is frequently dysregulated in human tumors. Cobimetinib is being developed by Genentech, a member of the Roche Group, under a collaboration agreement with Exelixis and is the subject of a broad clinical development program in combination with a variety of investigational and approved therapies.

- Esaxerenone (CS-3150) one of the compounds identified during Exelixis’ 2006 research collaboration with Daiichi Sankyo ( DSKYF ), an oral, non-steroidal, selective blocker of the mineralocorticoid receptor (MR), a nuclear hormone receptor implicated in a variety of cardiovascular and metabolic diseases. MR blockers can be used to treat hypertension and congestive heart failure due to their vascular protective effects. Recent studies have also shown beneficial effects of adding MR blockers to the treatment regimen for patients with type 2 diabetes with nephropathy. This collaboration generated MINNEBRO marketed in Japan with a pivotal trial and other development work in process.

Entry 5 calls out the Exelixis and the NCI sponsored cabozantinib trials included in Entry 3 above.

Exelixis has big business development plans as its solution to its heavy reliance on cabozantinib.

Exelixis recognizes that its current good fortunes derive from its cabozantinib-based CABOMETYX franchise. The bulk of Exelixis' current revenue comes directly from it. Its upcoming pivotal trials as discussed in the Call are all related to expanding indications for CABOMETYX. This is very much a situation where Exelixis has the vast majority of its eggs in one basket.

This spells risk with a capital "R". What could go wrong? It seems unlikely with CABOMETYX's long history and use in treatment of diverse indications and its FDA scrutiny that some hidden toxicity turn up. It is not particularly toxic as cancer therapies go. Its latest label (revised 09/2021) includes a daunting list of "WARNINGS AND PRECAUTIONS" but no black box warning.

No, the principal risk that could knock Exelixis back is its biosimilar competition. I am mindful of AbbVie's ( ABBV ) decade long Herculean efforts to prepare for Humira's US LOE. This brings up two key questions:

- Is CABOMETYX at near term risk of biosimilar competition?

- If it is, will Exelixis be able to mount an analogous protection campaign for CABOMETYX?

Unfortunately, the answer to the first question is unclear. Certainly it is an issue for Exelixis. According to its Q3, 2022 10-Q, there are at least two companies with which Exelixis is jousting over this very issue, MSN Pharmaceuticals, Inc. and Teva Pharmaceutical ( TEVA ).

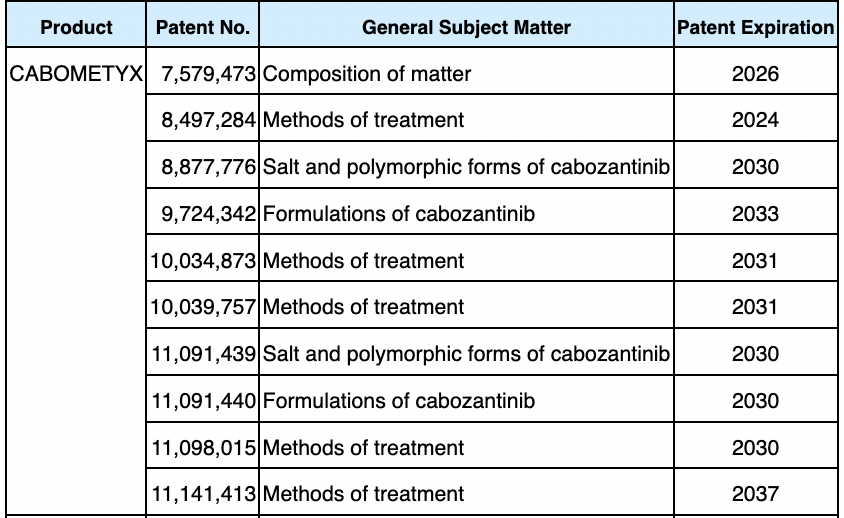

Exelixis' 10-K sets out its CABOMETYX patent estate as including:

...15 issued patents in the U.S., building from U.S. Pat. No. 7,579,473, for the composition of matter of cabozantinib (the ‘473 Patent) and pharmaceutical compositions thereof (p. 40).

It includes the following table listing its patents:

{kind=link}

From this table it seems clear that patent issues will be riling Exelixis and its shareholders at some point between 2026 and 2030. That gives it at most seven years. The second question above then comes to the fore.

This then helps to explain a testy exchange during the Call between CEO Morrissey and analyst Shibutani. The analyst pointed to Morrissey's preferred BD strategy he had described during his introductory remarks. Morrissey had stated how pleased he was to have accomplished option deals with Cybrexa and Sairop:

...which highlight our strategic efforts to access clinical and/or near clinical stage assets that have the potential to provide differentiated benefits to patients with cancer.

He characterized them as:

...ideal for us to employ as we can generate clinical proof-of-concept data with a wide range of experimental agents in a financially disciplined manner and only pay for success if and when that data is available.

Shibutani, likely thinking of how Exelixis' pipeline so thoroughly lacks non cabozantinib late stage clinical candidates, questioned the wisdom of loading up on early stage assets. He asked:

...can you help give a sense into this confidence in to this Clinical Stage Assets more that might ripping towards the back end of the decade, but may not be at the level of the revenues that are certainly demonstrated by the success with cabo thus far? I’m just trying to think about the longer term profile of revenues as we go through the balance of the decade with the decisions that you’re making now in the BD front?

Morrissey responded:

... I would say we probably don’t share your view on timelines to successful implementation and execution around getting the pivotal trials, having those run and readout. So our view is, we’re doing BD on a pretty aggressive scale based upon the conviction we have in the asset pool that’s available broadly within oncology, small midcap biopharma.... I think our view on timing and your view on timing are different, then it’ll be up to us to prove that as we did with cabo in the past.

Morrissey went on to tout the Exelixis BD team's prowess in assessing molecule's potential once they produced initial data as called for in its deals. The unspoken reality is that Exelixis has nice liquidity of $2.1 billion at the close of Q3. However it does not have tens of billions the way a Gilead ( GILD ) or an AbbVie does. Exelixis must stand or fall based on these types of deals.

Conclusion

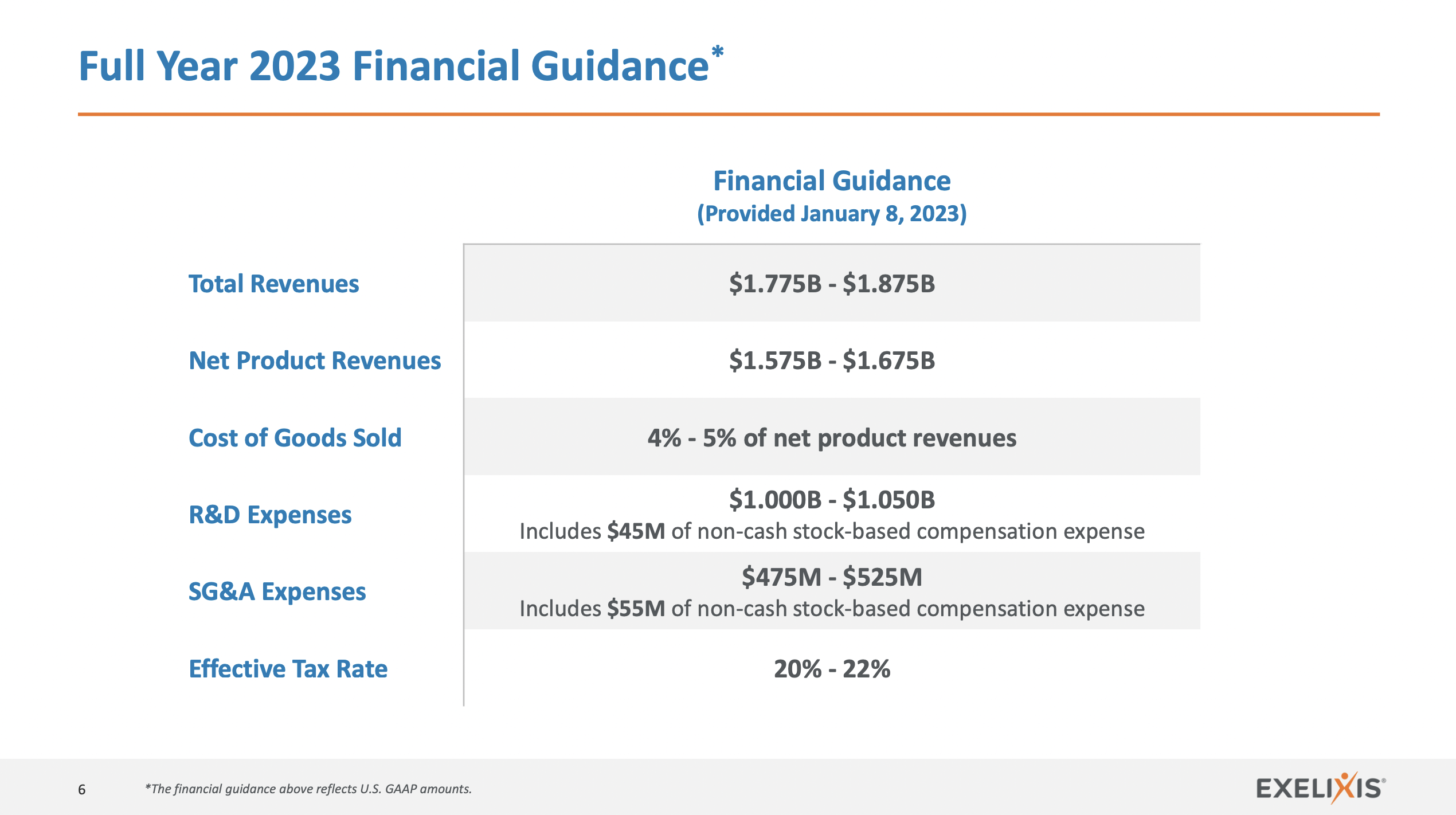

Exelixis included slide 6 below with its full year 2023 financial guidance during its 01/09/2023 J.P. Morgan Healthcare conference:

{kind=link}

With this strong earnings power and its Market cap of ~$5.3 billion it is an attractive buy. It has the lowest market cap of any of its five peers as shown by Seeking Alpha. Its 01/17/2023 quant factor grades, though not its overall ranking, are also much better than its peers.

Its average analyst price target of ~$25 allows for >50% upside. I consider Exelixis a near-term buy, although investors should be cautious of its longer term risks as discussed.

For further details see:

Exelixis: Building On A Blockbuster