EXEL - Exelixis: Predominantly Single Molecule Cancer Franchise (Rating Downgrade)

2023-08-30 07:00:00 ET

Summary

- Exelixis issued two important releases regarding its lead molecule cabozantinib, showing positive results in prostate cancer and advanced pancreatic and extra-pancreatic neuroendocrine tumors.

- The company's finances and liquidity are solid, with positive earnings and a healthy balance sheet.

- Despite a strong Q2, Exelixis left its guidance unchanged, prompting questions about near-term future growth prospects.

My first Exelixis ( EXEL ) article , 01/2023's "Exelixis: Building On A Blockbuster" gave a positive review of its investment merits following its Q3, 2022 earnings call. Exelixis recently held its Q2, 2023 earnings call (the " Call ") and issued two important releases relating to its lead molecule cabozantinib:

- 08/21/2023 release (the "Prostate Release") indicated a statistically significant improvement in progression-free survival [PFS] in prostate cancer, reaching one of two main goals in a Phase 3 trial, and

- 08/24/2023 release (the "Pancreatic Release") of results from its pivotal advanced pancreatic and extra-pancreatic neuroendocrine tumor trial.

This article discusses the significance of the Releases and the Call to Exelixis' investment merits.

The Releases provide encouraging news in Exelixis' ongoing battles against cancer.

General

Exelixis' lead therapy cabozantinib has sundry FDA and other regulatory approvals as CABOMETYX tablets; its approvals, both alone and in combination with Bristol-Myers Squibb's (BMY) OPDIVO (nivolumab), cover the following indications:

- advanced renal cell carcinoma [RCC],

- previously treated hepatocellular carcinoma (HCC] and,

- previously treated, radioactive iodine [RAI]-refractory differentiated thyroid cancer [DTC] and

- as COMETRIQ capsules for progressive, metastatic medullary thyroid cancer [MTC].

Exelixis began accumulating these important regulatory approvals as early as 04/2016. Its initial approval was as a monotherapy for advanced RCC in patients who received prior anti-angiogenic therapy. Page 5 of its 2023 10-K includes a detailed table listing the indications, approval dates, regimens, and major markets for its various approvals in the above indications.

The Prostate Release

The Prostate Release was a good news/bad news release. It announced data from the first interim analysis of Exelixis' CABOMETYX CONTACT-02 pivotal trial. It indicated a statistically significant improvement in progression-free survival ((PFS)) for prostate cancer. It reached one of two main goals in the Phase 3 trial.

However, it failed to reach statistical significance for the other primary endpoint, overall survival ((OS)). This was exactly the scenario anticipated by an analyst during the Call. He asked whether or not Exelixis would file if data from CONTACT-02 showed PFS but failed to reach statistical significance for OS.

The question was certainly prescient. The answer was predictable. Then CMO Goodman, since replaced by Dr. Amy Peterson, responded noting:

... In terms of would we file on PFS alone or OS? What I would say is, we're going to evaluate the totality of the data, as they come in, in terms of the overall benefit risk profile that we see and if appropriate, we'll have those conversations with the regulatory authorities.

As for the Prostate Release itself, it noted encouragingly that the data had shown a trend towards improving OS. Accordingly Exelixis will continue to watch the trial to see the next readout data on overall survival.

In other words stay tuned. It could be a while before any significant revenue accrues on account of CABOMETYX in treatment of prostate cancer.

The Pancreatic Release

Exelixis first posted its 395 participant clinical trial NCT03375320 dubbed CABINET on cinicaltrials.gov in 12/2017. CABINET evaluated cabozantinib in patients with advanced pancreatic neuroendocrine and carcinoid tumors; it had estimated completion dates of 10/2025.

To the delight of patients and shareholders alike, Exelixis announced on 08/24/2023 that cabozantinib substantially prolonged the time without disease progression or death in both of the trial’s cohorts. It noted:

CABINET trial ...[would] be unblinded and stopped early due to a dramatic improvement in efficacy per a unanimous recommendation by The Alliance for Clinical Trials in Oncology independent Data and Safety Monitoring Board

This favorable report is another arrow in the Cabozantinib quiver. As reported in Exelixis 2023 10-K (p. 3), it generates the bulk of its revenues from cabozantinib. As noted above this powerful cancer fighting molecule has already made its mark in the fight against a variety of cancers.

Insofar as the CABINET trial addresses neuroendocrine and carcinoid tumors rather than pancreatic cancer itself, its economic impact, even if the FDA approves it, will be muted. Such maladies are both rare and slow growing. More information on trial data will be provided at an upcoming medical meeting.

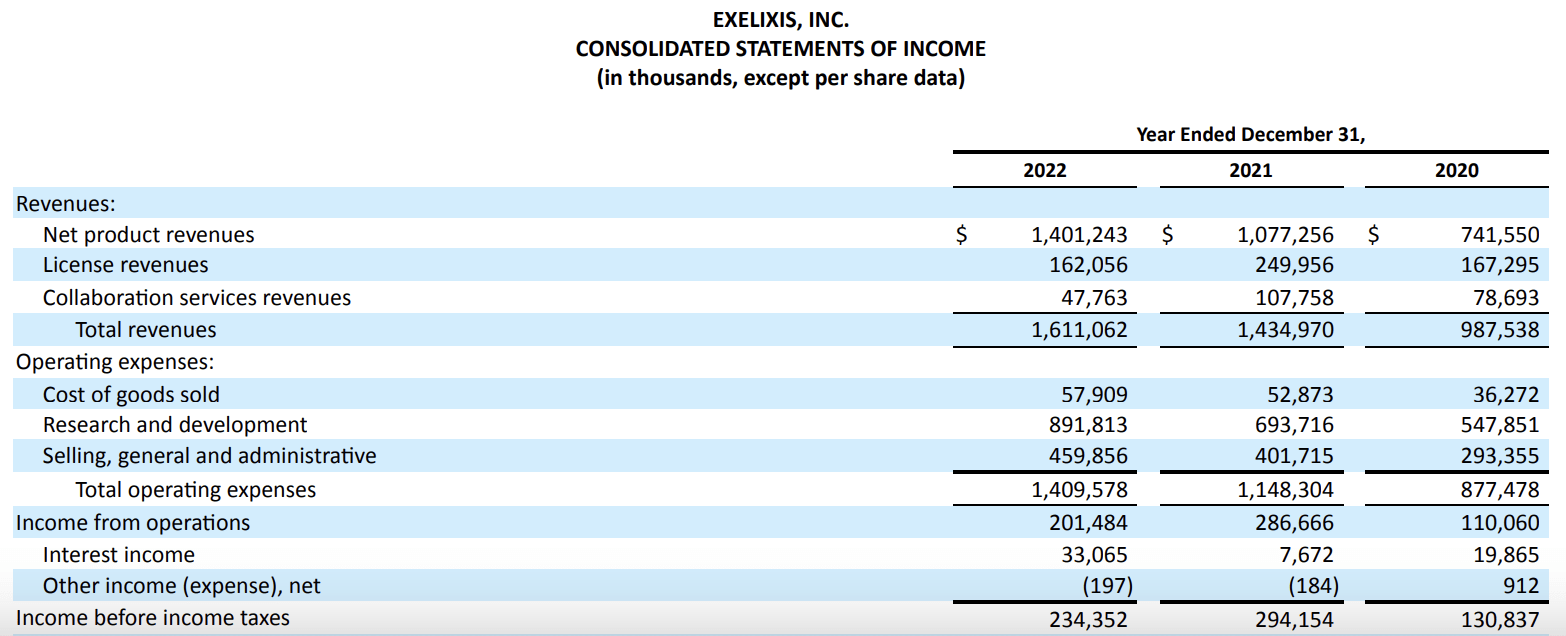

Exelixis' finances and its liquidity are strong.

Exelixis' 10-K (p. 82) provides a helpful three year snapshot of its earnings as set out below:

{kind=link}

Its positive earnings trajectory has led it to an attractive balance sheet as shown at page 81 of its 10-K. It features total assets exceeding $3 billion and total liabilities of <$600 million.

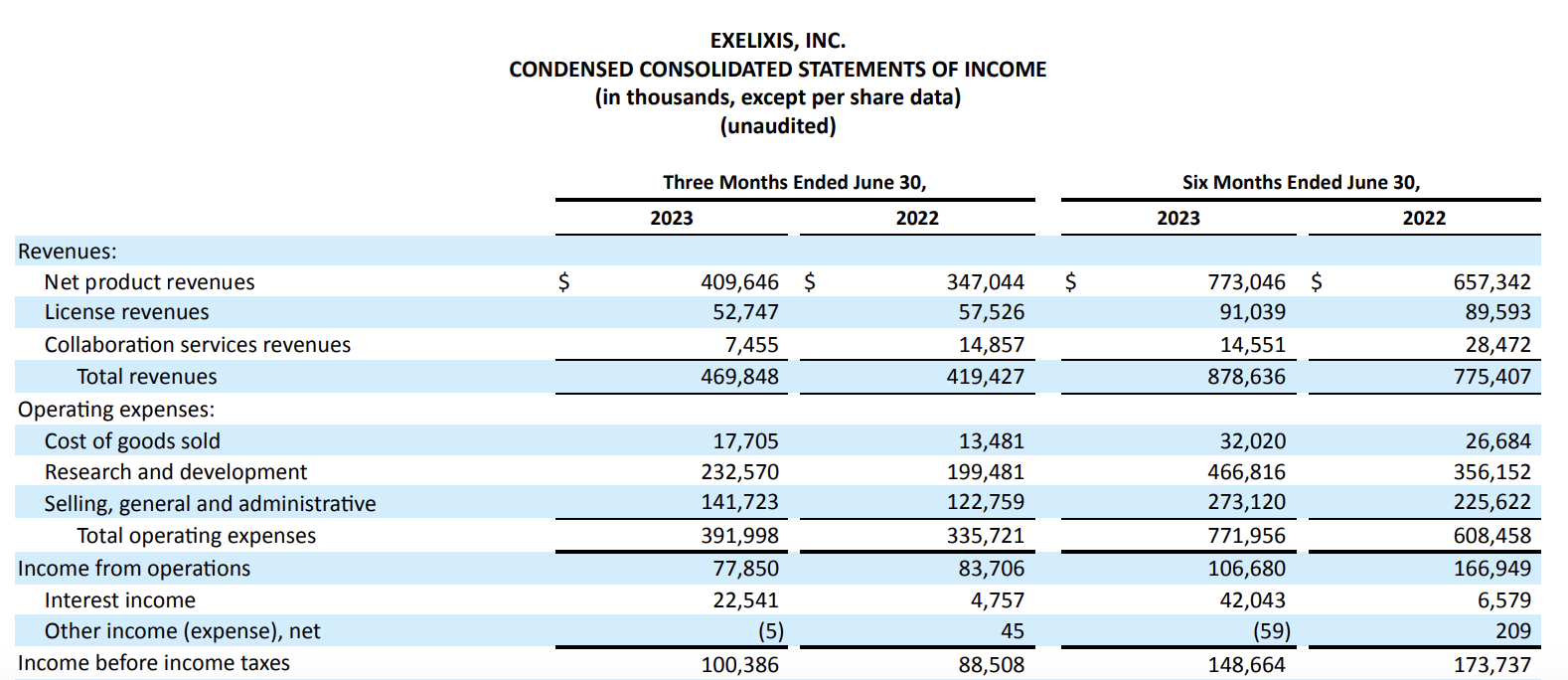

Moving to its Q2, 2023 10-Q (p. 4) brings its reportage up to date through 06/30/2023; its most recent three and six month revenues and expenses are in line with its annual figures as shown below:

{kind=link}

As for its 10-Q (p. 3) balance sheet, total assets clock in at >$3.1 billion with total liabilities at ~$614 million. During the Call Exelixis reports its cash and equivalents at close of Q2, 2023 as ~$2.1 billion, in line with its NOTE 4. CASH AND INVESTMENTS (p. 14) section of its 10-Q.

In response to a question during the Call, CFO Senner discussed Exelixis' capital allocation priorities as follows:

So right now, we are committed to the $550 million share repurchase program, we got authorized in March. And as we -- time goes on, we'll continue to evaluate how we allocate capital across the multiple areas of the business, including potential share repurchase, but also R&D and development and also commercialization

This is indeed an ambitious agenda, particularly insofar as CEO Morrissey is highly committed to business development [BD]. During the Call he noted that BD was a priority. Certainly he is also committed to internal R&D efforts; however he noted that Exelixis had already identified outside molecules that it liked and was pursuing.

While I am always chary of BD activities and the risk they pose to an acquirer's capital structure, Exelixis is an old hand at such efforts. As described in its 10-K at pages 15-22 under the heading "Collaborations and Business Development Activities" it has already notched dozens of deals. Deals are very much engrained in its DNA.

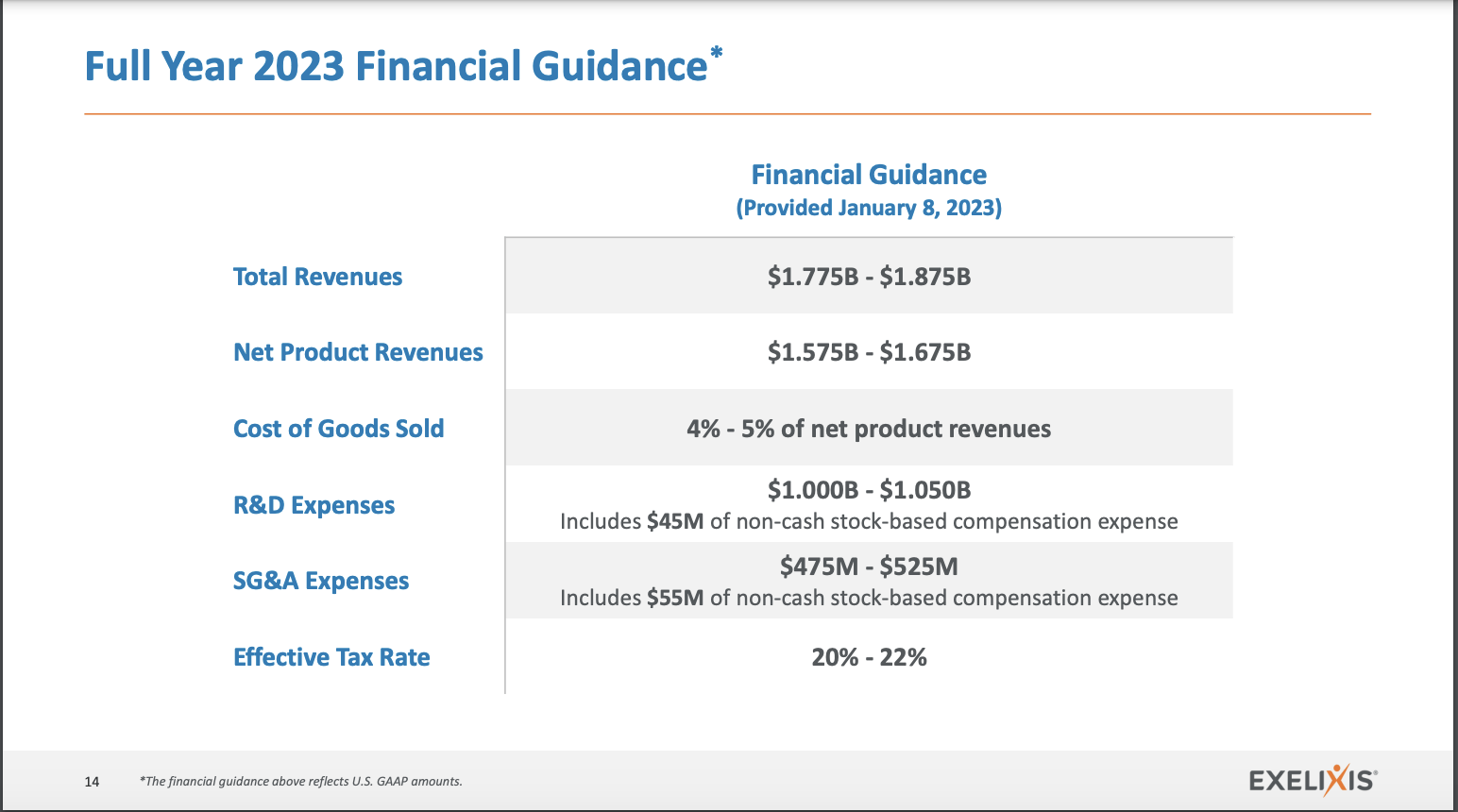

Despite a strong Q2, 2023, Exelixis left its guidance unchanged.

Exelixis scored an impressive Q2, 2023 beat on the top and bottom lines. Instead of projecting its good vibes forward by raising its guidance, Exelixis left it unchanged. Slide 14 below from its Q2, 2023 earnings slide deck sets out this guidance:

{kind=link}

Net product revenues shown on its 10-Q excerpt above for Q3 of 2022 were $409,646. Annualized this would be $1,636,584, a scant $11,000 above the $1,625,000 midpoint of its previous 2023 net product revenue guidance. Apparently, management is not anticipating that its strong Q2 results portend further growth in 2023.

This tepid prediction prompted an analyst during the Call to ask the rationale for keeping the original guidance in light of its strong Q2, 2023. CFO Senner responded:

... from a guidance perspective, ,,, we had a strong quarter. We continue to have strong growth and based on that strong growth that we've seen in the first half of the year, we think we're confident that cabo has the ability to grow into the second half of the year and that's why we reiterated the guidance range we did today.

Earlier this year an activist investor prevailed in a proxy contest with Exelixis. In response, Exelixis refreshed its board with three new directors. The activist also challenged Exelixis >$1 billion in anticipated 2023 R&D spending.

I count this R&D question as unresolved insofar as its guidance for R&D spending remains unchanged. Ironically, during the Call, management blamed its increased SG&A spend on proxy contest expenses.

Conclusion

Exelixis has been on a nice updraft since my previous article in January. Today 08/29/2023 as I write, it trades at $22.34 up ~37% from $16.32 when the previous article was published in 01/2023. Obviously, the future is not ours to see; however we can use our best judgment to assess an investment's forward prospects.

When I look at Exelixis I see no clear catalysts that are primed to propel an upward trajectory over the near term. As the year winds down investors will have important data points:

There are three issues to watch for:

- status of discussions with the FDA on the Pancreatic Release:

- results from expected COSMIC-313 pivotal phase 3 study evaluating triplet combination of cabozantinib as described on earnings presentation slide 33; and

- most importantly — prospects for submission of prostate trial results to FDA.

Exelixis has a deep collection of cabozantinib related therapies. Its pipeline elsewhere as described at earnings slides:

- 22 — Robust Pipeline Beyond Cabozantinib and;

- 24 — Progress ... on Internal Clinical Stage Pipeline Programs.

This pipeline would be more accurately characterized as sprawling and heavily skewed towards early phase assets. Given its current prospects, Exelixis appears fully valued. I agree with its current 08/29/2023 Quant rating of "hold".

For further details see:

Exelixis: Predominantly Single Molecule Cancer Franchise (Rating Downgrade)